June 2017

Thoughts from NIC’s Chief Economist

Beth Mace

“It’s getting hard to find workers.”

It’s a familiar refrain and one that will become an increasingly common lament of employers. With the national unemployment rate falling to 4.4% in April, the jobless rate is at a 10-year low. Moreover, a broader measure of joblessness, which includes those who are working part time but would prefer full-time jobs and those that have given up searching—the U-6 unemployment rate—also fell in April to 8.6%, its lowest level since 2007. Since February 2010, which marked the low point of the employment recession, 16 million jobs have been created, 7 million more than the pre-recession peak.

Additional downward pressure on the unemployment rate is likely to occur in the coming months as job growth continues to exceed labor force growth. This will put the unemployment rate further below the so called full-employment or natural equilibrium level; indeed, today’s unemployment rate is already below the official estimate by the Federal Reserve of the full-employment level, which is 4.7%. A rate much below this is believed to fuel inflation through upward pressure on wage rates. And this is becoming evident in a number of wage measurements. In the 12 months ending in April, average hourly earnings rose 2.5%, generally on par with the 2.6% average monthly gain in 2016, and up from 2.3% in 2015 and 2.1% 2014. Other wage rate indicators are also strengthening. This includes the year-to-year improvement in private sector wages and salaries, as measured by the Employment Cost Index (ECI), which grew to 2.6% as of the first quarter. The ECI takes into account the changing mix of workers on measured wages.

Despite the reasonably robust pace of employment growth, GDP growth has been lackluster and has averaged 2.1% since the bottom of the recession in 2009. The explanation for the disparate growth rates can partially be traced to uninspiring labor productivity growth. From 2011 to 2016, annual growth in productivity has averaged less than 1%, the slowest five-year pace since the 1977-82 period. Without productivity growth, it’s hard to gain traction in the pace of economic growth. By definition, output growth is the sum of productivity growth and labor force growth. So, either productivity growth has to accelerate from today’s low levels or the labor force has to expand at a more rapid rate.

In a report issued from the Congressional Budget Office (CBO) in January, average GDP growth was projected to be less than 2% per year between 2017 and 2020 due to sluggish growth in the labor force of 0.5% and productivity growth of less than 1.5% per year. By comparison, during the 1991 to 2001 period, when GDP growth averaged 3.3% per year, the working population was expanding at a 1.2% annual rate and growth in output per hour averaged 2.0% per year. The 3.3% figure is notable because it is near the rate being discussed by some in the Trump Administration.

Without aggressive immigration policies, the labor force is not likely to accelerate appreciably—much of the slowdown has to do with demographics and the aging population. This leaves productivity growth as the solution for faster output growth and the benefits associated with it, such as greater prosperity and wealth. Federal government policies that promote capital, R&D, educational and infrastructure investment are solutions that could support stronger productivity growth and subsequently the economy’s long-term potential. A boost in productivity could also potentially have the added benefit of holding back inflation and allowing the Fed to keep interest rates lower for a longer period.

With regard to seniors housing and care, labor force growth and the low jobless rate are expected to make it increasingly difficult to attract and retain qualified and trained staff at all levels of operations. In order to grow NOI, operators will need to boost their operational efficiency and staff productivity likely through technology, training and mentoring.

The Best of Times, the Worst of Times

Depending upon your location, it may be the best of times or the worst of times—at least by measurements of seniors housing occupancy rates. Among the 31 NIC MAP® Primary Markets, four reached near-record high occupancy rates for majority independent living properties in the first quarter of 2017—Seattle, St. Louis, Chicago and Dallas—while two reached record lows — Houston and San Antonio. Meanwhile, San Jose boasted the highest occupancy rate for independent living properties in the first quarter. San Jose was followed by Baltimore, Las Vegas, Washington, D.C. and Sacramento. Three of these markets—San Jose, Sacramento and Baltimore—also ranked in the top five highest occupancy rate markets for assisted living, with San Jose garnering top spot again. At the opposite end of the spectrum were the more poorly occupied independent living markets of Houston, San Antonio, Riverside, Atlanta and Kansas City. Two of these were lowest for assisted living occupancy as well—San Antonio and Kansas City. As with all real estate, location and timing are everything.

Other notable observations of market performance include the 14 majority independent living markets that experienced gains in occupancy in the first quarter of 2017 from year-earlier levels (versus 8 markets for assisted living). This compares to the 16 markets that saw a decline in independent living occupancy from year-earlier levels (versus 23 for assisted living). The most significant deterioration occurred in Houston (down 570 basis points), followed by Atlanta (down 430 basis points), Sacramento, San Diego, San Antonio.

And for assisted living, occupancy rates ranged from nearly 93% in San Jose to less than 72% in San Antonio. Meanwhile, Washington D.C. shifted from a near-record high assisted living occupancy rate one year ago to a near-record low in the first quarter, as growth in its inventory outstripped demand.

A few other markets had record or near-record low assisted living occupancy rates in the first quarter as well. These include:

- San Antonio (72.3%)

- Denver (84.4%)

- Cleveland (83.2%)

- Washington, D.C. (88.2%)

- Pittsburgh (89.2%)

There were also a number of markets that saw significant deterioration in assisted living occupancy rates in the past year. Worse among these was:

- Cincinnati (down 580 basis points)

- St. Louis (down 470 basis points)

- Washington, D.C. (down 460 basis points)

- Riverside (down 440 basis points)

- Denver (down 370 basis points)

At the other end of the spectrum are eight markets that experienced gains in assisted living occupancy over the past year. This list includes Houston (up 310 basis points from the first quarter of 2016), followed by Phoenix (up 200 basis points), and New York and San Diego (both up approximately 100 basis points).

Variation in local market performance is a result of disparate influences, some of which involve supply factors including the ease of development, the cost and availability of debt and equity sources of financing. On the demand side, determinants can include consumer-familiarity with the product offerings, demographic growth drivers and local market economic conditions. A solid understanding of supply and demand determinants and how these conditions translate into performance measurements can make the difference between a successful and a less successful operation.

As always, I welcome your feedback, thoughts, and comments.

Beth

Robust First Quarter Transactions Volume Driven by Institutional Buyers

Bill Kauffman

The first quarter of the year is usually one of the weakest quarters in terms of transactions volume due to the usual rush to close deals at the end of the prior year, leaving the pipeline a bit reduced going into the first quarter. However, this year’s first quarter had one of the strongest starts of the last 5 years. The strong results were mostly due to a few large deals, including one for more than $1 billion.

Transaction Dollar Volume Increases

Transactions volume for seniors housing and care registered a total of $4.6 billion in 1Q 2017. Seniors housing had a strong quarter, accounting for $4.1 billion of the total, but nursing care tallied volume of only $500 million. The total volume was up 45% from the previous quarter’s $3.2 billion, and up 22% from 1Q 2016 when volume totaled $3.8 billion.

Comparing nursing care and seniors housing volume, we see that nursing care volume was down a significant 54% from the prior quarter’s volume of $1.2 billion. Seniors housing was up more than 100% from $2.0 billion to $4.1 billion. Compared to 1Q 2016, nursing care volume was down 77%, and seniors housing was up 218%. The rolling four-quarter volume in nursing care decreased from $6.8 billion to $4.9 billion, and seniors housing increased from $7.5 billion to $10.2 billion.

A significant part of the pick-up in seniors housing volume in the first quarter was due to the sale of assets by the public REITs to institutional buyers. There were a few large portfolio deals in the first quarter which helped to drive the increase in volume.

Several large transactions of note include:

- Blackstone closed on 60 Brookdale properties from HCP representing $1.1 billion in volume, with more than 5,500 units and a price per unit of more than $200,000.

- Blackstone, in another large deal, closed on the Senior Lifestyle portfolio from Welltower for $747 million, including 25 properties with more than 3,600 units and a price per unit again of more than $200,000.

- The Chinese life insurance company, Taikang Life Insurance, purchased a partial interest in the Northstar portfolio. According to a press release, the transaction was valued at about $460 million and included more than 200 properties.

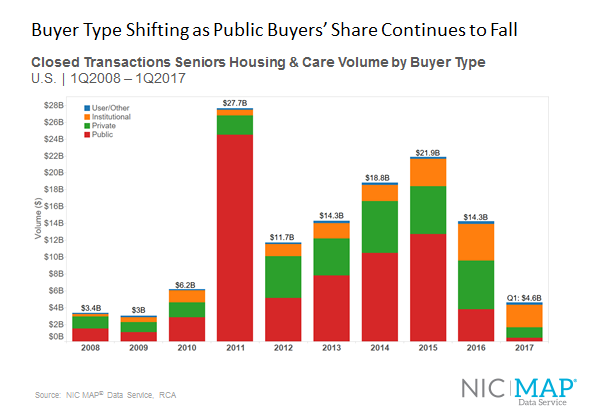

Buyers Shift as Public Buyers’ Share Continues to Fall

The main story is the fact that the public buyers’ share of acquisition volume continued to decrease in early 2017. However, unlike in previous quarters when public buyer activity declined and depressed overall volume, this past quarter was strong because the institutional buyer, as mentioned previously, completed some significant deals.

Public buyers’ volume in 1Q 2017 dropped 31% to only $444 million from what was already a relatively low volume of $646 million in the prior quarter. Each quarter now seems to tally a lower volume than the previous quarter for the public companies, namely the public REITs. When compared to 1Q 2016, with volume of $902 million, the public buyers’ volume in 1Q 2017 dropped significantly by 51 percent. Furthermore, this past quarter was the lowest quarterly closed transaction volume for the public companies since 1Q 2010 when the volume recorded was only $103 million.

Public companies represented only 10% of total buyer closed transaction volume during 1Q 2017. A changing market, including cost of capital increases, new construction coming online, and higher property prices, have made public REITs adjust their strategy. They have decided to be more selective and have now become net sellers in this current market cycle.

On the flip side, the institutional buyers have acquired some of the REIT assets. Active buyers include Blackstone and some international investors. The institutional buyers represented 58% of buyer volume during 1Q 2017, a significant shift from 2015 and 2016 when the group represented only 15% and 31% of volume, respectively.

Purchases by private buyers—private REITs and private partnerships—have started to slow, with private transaction volume declining by 15% from last quarter. However, private buyers have maintained a consistent volume. This was the 15th consecutive quarter with closings totaling $1 billion or more, though the private buyer represented only 26% of buyer volume during 1Q 2017.

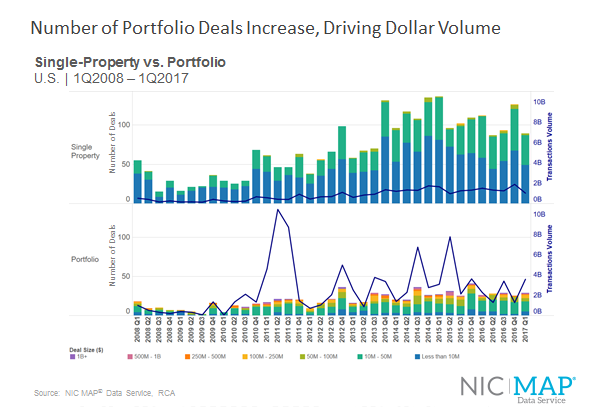

Deal Size

Over the past several quarters, there have been very few transactions of more than $1 billion or in the $500 million to $1 billion range. These big deals can move the dollar volume needle significantly. Not only did we see portfolio transactions increase overall in the first quarter, from 25 to 29 closed deals to be exact, but we also saw large portfolio transactions close in the quarter. In the last quarter, no deals valued at $500 million and up closed, and this past quarter we had two such deals close which drove the quarter’s robust transaction dollar amount.

When it comes to the overall count of transactions closed, the single-property deals still dominate with 89 closed, for a total of 118 deals when including portfolios. In comparison, we had 151 total deals close in 4Q 2016. So, even though the number of transactions was down quarter-over-quarter, dollar volume was up significantly because the large portfolio deals made up for the lower deal count. However, keep in mind that even with deal count down, this was the 14th consecutive quarter with at least 115 deals closing, which tells us that the brokers are still staying quite busy. The dominate deal size continues to be the single-property transactions of less than $10 million as well as those between $10 million and $50 million, which is why the deal counts are keeping up a healthy pace.

Compared to 1Q 2016, closed deal count was down from 138, a number that included 26 portfolios and 112 single-property deals.

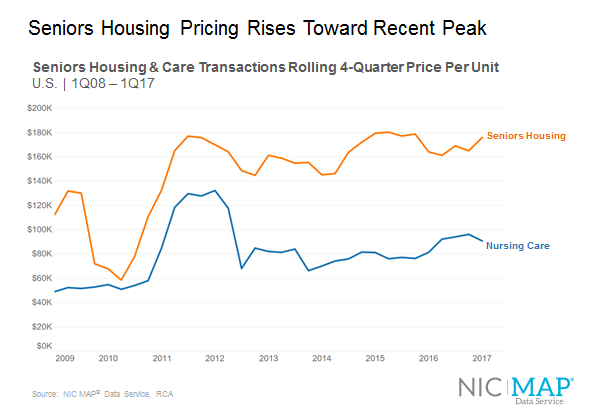

Pricing

Seniors housing price per unit compared to the previous quarter increased this quarter by 6.6% from $165,000 to $175,900. Seniors housing price per unit has basically been hovering around this level for a couple years. Yes, it did see a dip in 2016, but now it’s back up again and approaching the $180,000 level.

As compared to a year ago, seniors housing has increased 7.2% from a price per unit of $164,000 in 1Q 2016.

Nursing care pricing over this past quarter has moved in the opposite direction of seniors housing, decreasing 5.6% to the current price per unit of $90,800. But compared to a year ago, nursing care is up a significant 11.5% from $81,400. This data of course is representative of only what is trading, so most likely this large increase is due to the trading of higher-quality skilled nursing properties, including newer properties, those with a high skilled mix, or some combination of such characteristics.

Overall the first quarter of this year experienced a relatively healthy transactions market with robust deal flow and solid pricing. We look forward to reporting the current trends with the release of NIC’s second quarter data in July.

2017 Spring Investment Forum Recap Series 2

The Future of Senior Care in the New Administration

Though the initial push to repeal and replace the Affordable Care Act failed, many questions remain about where our health care policy is headed under the Trump Administration.

Former U.S. senators Tom Daschle and Bill Frist, both well versed in health care policy, addressed attendees at the luncheon session of the 2017 NIC Spring Investment Forum. Their remarks were moderated by Kenneth Segarnick, chief corporate officer at Brandywine Living.

The $3 trillion U.S. health care system is the largest public-private partnership in the world, noted Daschle, who is founder and CEO at The Daschle Group, a strategic advisory firm. “It’s a big job to make it work more effectively.”

Frist opened his remarks by asking: “What is our social contract with 350 million people?” He suggested that it’s a moral question that we have to answer. “Policy is tough and has huge implications for people,” said Frist, partner & chairman, Cressey & Company, a private equity firm with health care investments.

You can watch the video recording of the entire session here.

Highlights include:

- What will happen to funding? Will Medicaid become a block-grant program?

- Big trends: technology, quality improvement, value-based care

- The four qualities long-term care companies need to survive

The New World of Senior Care Collaboration

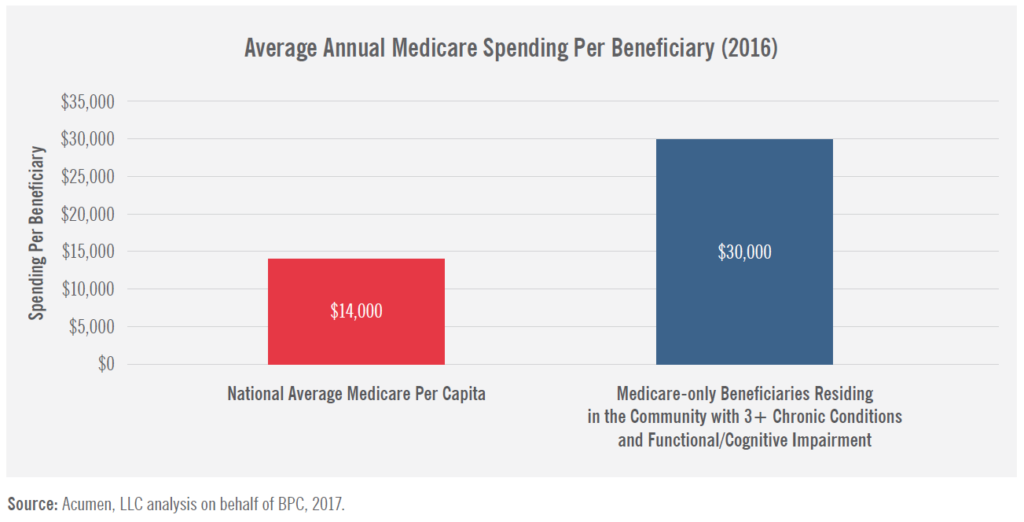

About 5% of the Medicare beneficiaries account for nearly half of the health care program’s expenditures. Not surprisingly, the group is comprised mostly of frail seniors who need help with two or more activities of daily living and have multiple chronic health conditions. This needy population also happens to make up the majority of residents in seniors housing.

“The challenge (for the industry) is to turn this situation into an opportunity,” said Bob Kramer, NIC founder and CEO, during introductory remarks at the opening general session of the 2017 NIC Spring Investment Forum.

Kramer provided context for the meeting’s theme: Unlocking New Value through Senior Care Collaboration. He explained that NIC research has found that the delivery of services to frail seniors has traditionally been split into two silos. Seniors housing and skilled nursing, along with its real estate-based investors, operate in one silo, separate from the silo that includes providers who offer care coordination, enhanced primary care and newly emerging technology-based services.

“Seniors housing and care operators need to connect across the silos,” said Kramer. He emphasized the growing importance of collaboration as health care policy makers seek ways to reduce costs amid the shift from a fee-for-service to a risk sharing payments system.

Collaboration can lead to a win-win situation, Kramer said. Real estate-based providers can act as a platform for the services needed to produce better health outcomes for seniors to enhance their overall quality of life. With this theme in mind, Kramer introduced the first panel discussion of the morning, “The New World of Senior Care Collaboration.”

The session was moderated by Anne Tumlinson, founder of Anne Tumlinson Innovations, LLC. She noted that half of adults age 65 or older will need help at some point with at least two activities of daily living. The cost of that care averages about $138,000. “We need to organize care in a way that makes sense for families and the health care system,” she said. “We need to work together to connect the silos of care.”

Panelist Lynne S. Katzmann, founder and president of Juniper Communities, presented the results of the company’s Connect4Life program which integrates medical services and coordinates care for residents. The three components of the program include onsite services, such as primary care, the use of electronic health records, and a human navigator who ensures access to and coordination with a variety of providers.

Research findings show that the hospitalization rate for Juniper residents is 50 percent lower than a similarly frail Medicare population. Juniper’s rehospitalization rate is more than 80 percent lower than a similarly frail Medicare population.

“We’re excited by the results,” said Katzmann.

As a grandson and tax payer, panelist Kurt Read thought the program showed great promise. But as a real estate investor and principal at RSF Partners, Read expressed his concerns that senior living could be turned into a technology or health care company. “It makes me nervous,” he said.

Panelist Katzmann pointed out that her company has had to address the rising acuity of residents which has impacted their length of stay. Competition from new providers was another factor, she said. “This is a private pay model that enhances our market share,” said Katzmann, adding that the Connect4Life program has lengthened the stay of residents and improved the company’s EBITDA (earnings before interest, taxes, depreciation and amortization).

Home care partners

The panel discussed how senior living providers can partner with home care companies, instead of viewing the services as competitors. “Three years ago, there would have been no interest in having a home care company attend a NIC meeting,” said Kelsey Mellard, head of health system integration at Honor, a San Francisco-based start-up that uses technology to facilitate and coordinate home care, and communicate with families.

Honor currently operates in San Francisco, Dallas, Albuquerque and Los Angeles. The services can be delivered wherever the elder lives, including in seniors housing communities, particularly in independent living, noted Mallard. Honor has raised $62 million from venture capital sources, an indication of the interest among investors in the space because of the growth of the aging population.

Panelist Dexter Braff, president, The Braff Group, noted that private equity investors are pouring capital into home care, hospice, and home health services. “The investment community has realized that the coordination of care is a real opportunity for home care companies to differentiate themselves,” said Braff.

Capital markets operate in silos too, noted panelist Read. “Private equity investors don’t want to invest in real estate,” he said, explaining that property has different valuations and capital needs than a home care or technology company. “That’s really important,” he said. But Read predicted that within five years, investors at the NIC Forum will be seeking partnerships with service providers like Honor. “We can be both real estate capital and operating capital,” Read said. “Our industry needs to change.”

In conclusion, NIC’s Kramer asked how skilled nursing centers in particular can fully participate in care collaboration. Panelist Read answered that skilled nursing operators need to become a dominant player with insurance companies and health care providers. That includes making investments in services such as hospice care and care coordination. Most importantly, he added: “Skilled nursing facilities need to focus on their markets.”

You can watch the video recording of the entire session here.

CMS, Congress Target the High-Need, High-Cost Population

Liz Liberman

In 2014, 15 percent of Medicare beneficiaries had six or more chronic conditions and made up half of the total Medicare spend. Among those seniors who are dually eligible for Medicare and Medicaid (low-income seniors), 23 percent had over six chronic conditions. The Centers for Medicare and Medicaid (CMS) is paying attention to this group as a target population to find savings for Medicare. Congress is also actively considering policy options that can reduce Medicare spend for the high-need, high-cost population, also known as “super-utilizers.” One way CMS can save Medicare spending is by encouraging providers to discharge patients with acute episodes home rather than sending them to nursing homes for short-stay visits.

Skilled nursing visits cost Medicare just over $500 per patient day on average, per the Q4 2016 NIC Skilled Nursing Data Report [1] . Home health, on the other hand, can be much less expensive for Medicare, but only if that setting keeps these complex patients healthy and prevents rehospitalization—a daunting task for a population juggling several chronic conditions. Policy experts are now exploring how home health coupled with home care could further improve outcomes for this target population while still costing less than alternatives.

Home care isn’t the only avenue CMS is exploring; some low-cost educational programs in the nursing home setting have demonstrated value to payors, including Medicare. End-of-life care, regardless of patient setting, has also caught the attention of regulators and lawmakers aiming to reduce high-cost healthcare spending. Seniors housing and care providers have an opportunity to become engaged now to benefit from the government drive to lower Medicare costs incurred by the high-need, high-cost population.

Home care models demonstrate measurable value to Medicare despite barriers

Several recent studies show home care, which includes support for activities of daily living such as eating and bathing, can reduce Medicare costs. One CMS study, which was part of NORC at the University of Chicago’s multi-year evaluation of the Health Care Innovation Awards of CMS, showed that four of five home care models in a pilot program for Medicare fee-for-service patients with multiple chronic conditions returned positive results by saving money, improving outcomes, or both. The study findings will not likely result in an immediate, nationwide adoption of such a model under fee-for-service Medicare, but it could encourage providers already participating in the growing number of risk-based models such as Accountable Care Organizations or Medicare Advantage to incorporate this practice.

In response to a call from the Senate Finance Committee Chronic Care Working Group, the Bipartisan Policy Center (BPC) released a two-part analysis and report that found high-need, high-cost elders benefit from additional supports and services outside of traditional healthcare, and predicts that Medicare could save money in this population by incorporating those services. BPC recommends that CMS alter how Medicare Advantage and ACO’s are regulated vis-a-vis reimbursement for supports and services. The journal Health Affairs also recently published two blogs on the subject, one from Dr. Karen Davis, former president of the Commonwealth Fund, and another from journalist Bara Vaida.

Introduced in April, the CHRONIC Care Act is another example of legislators taking aim at reducing Medicare spending on patients with multiple chronic conditions. This bill proposes several legislative maneuvers to improve care for the target population, the first of which is extending the Independence at Home Model of Care, which is scheduled to sunset in September of this year. (More to come on these and other models in the NIC Blog.)

The takeaway is not to focus on a specific pilot, but instead to recognize that CMS is not alone in pushing for healthcare options that keep costs down by keeping people in their homes and out of nursing homes. Congress is onboard for these types of reforms. Even while embroiled in an existential crisis over healthcare delivery in the U.S., the Executive and Legislative branches can agree on this aspect of healthcare. Regardless of what happens to the Affordable Care Act, reforms to healthcare delivery for the high-need, high-cost population will likely endure.

Nursing homes deliver value, too

CMS funded a study conducted by RTI International that considered a few pilot programs designed to reduce the frequency of hospitalizations for long-term nursing home residents, especially those hospitalizations considered “avoidable.” Hospitalizations for long-term residents are expensive and lead to increased mortality risk for residents (note that rehospitalization refers to situations where a short-term patient getting post-acute care must go back to the hospital, which is not the same as hospitalizations for long-term residents).

Under the umbrella “Enhanced Care and Coordination Provider” model, CMS considered several pilots that did not have financial incentives and only provided education and training. Though results varied among the 143 participant nursing homes across seven states, all states saw a reduction in hospitalizations and avoidable hospitalizations in both study years (2014 and 2015), a promising finding. In other words, a very low-cost program implemented in the nursing home setting resulted in reduced hospitalizations among the high-cost, high-need population (i.e. cost savings to Medicare). While nursing homes may have to compete with home-based care delivery models and sometimes assisted living providers for market share in an environment where cost control is top priority, studies such as this demonstrate that nursing homes provide value to the healthcare system, too.

Lawmakers take a hard look at end-of-life

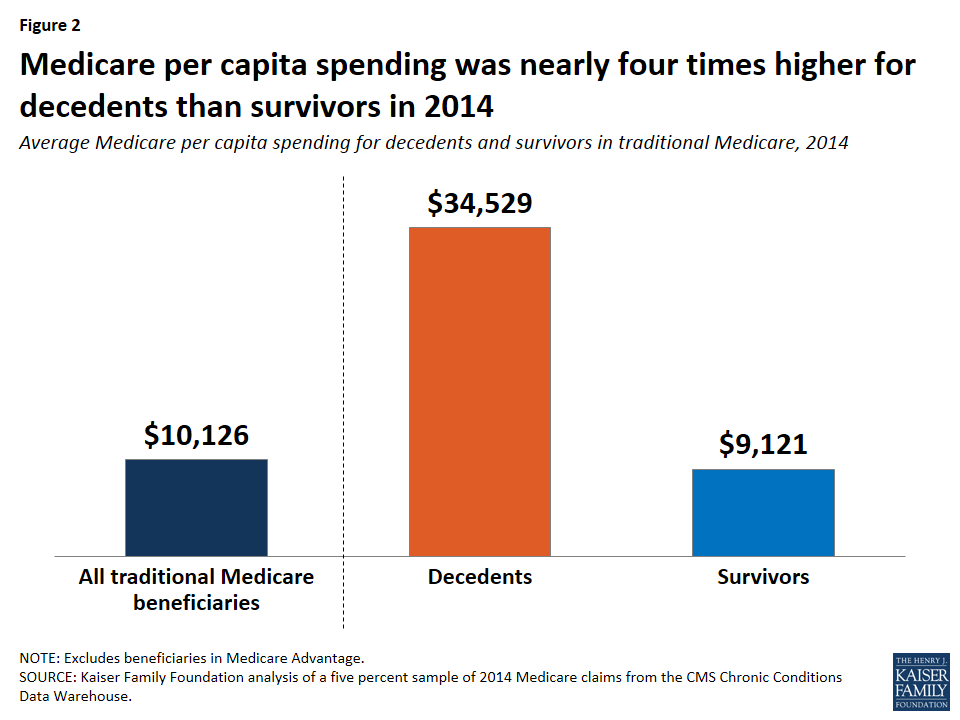

The “super utilizers” make up a large chunk of Medicare spending, but people at the end of their lives spend the most on care in that last year, especially when an advanced illness is involved. The chart below from the Kaiser Family Foundation shows that the Medicare costs incurred in the final year of life among people who died in 2014 was nearly four times the cost for beneficiaries who did not die. Legislators are considering a bill that would help to suppress the exorbitant costs incurred by the very ill toward the end of their lives while supporting patient preferences, which usually do not include spending their final days recycled through the hospital system undergoing a slew of medical procedures.

By creating incentives for physicians to enter the palliative care field and promoting the benefits of palliative care through a national campaign, the Palliative Care and Hospice Education and Training Act serves as another step in the direction of reduced healthcare spending. Introduced in March of this year by a bipartisan group of Senators, the bill aims to develop the palliative care workforce, which can be effective in coordinating care for very ill patients and serving dying patients’ non-medical needs such as their spiritual care. Palliative care teams also function as an advocate for patients to ensure their wishes for treatment (or more often avoidance of treatment) are honored. By ensuring patients who do not want expensive, intrusive medical treatment have their voices heard within the healthcare system, palliative care teams have the potential to save a lot of money for the system while also helping patients get exactly the degree of care they want. Because palliative care involves medical and non-medical professionals, nursing homes and assisted living properties are perfectly poised to provide this high-value benefit to their residents.

Part of the solution: Seniors housing and care already serves the high-need, high-cost population

Any of these initiatives can impact the seniors housing and care industry, and not just nursing homes. Assisted living providers may be able to leverage their value proposition to healthcare payors and customers as a setting with built-in supports that are proven to help keep frail elders out of more expensive settings like the hospital or nursing homes. After all, CMS and Congress are actively targeting the population that already lives in those facilities—frail elders with chronic conditions, functional impairment, dementia disorders, etc. Certainly, some barriers persist in the Medicare fee-for-service payment model that may prevent assisted living providers from capturing revenue right away, but the future of value-based, risk-based, care-coordinated healthcare delivery is on the horizon. Those assisted living operators at the forefront of engagement could reap significant benefits in the near future.

Meanwhile, nursing care providers have already started to feel the pressure on occupancy, driven by declining Medicare patient day mix. That decline can be attributed in part to CMS regulations already in place that encourage hospitals to reduce skilled nursing length-of-stay or bypass that setting altogether. As CMS fleshes out more of these pilot programs and determines which ones work best to reduce Medicare spending, the agency will likely proliferate those practices and programs.

The bureaucratic process of vetting pilots and scaling them up is lengthy, so the impact on skilled nursing will probably be gradual. In the interim, operators can choose to continue with business as usual or they can adapt to the new normal of fewer Medicare patients and shorter Medicare stays. For example, skilled nursing operators can diversify their services to include home health, thus recapturing the lost revenue when patients stay in their properties for shorter stints. Specialized care may be another opportunity for skilled nursing providers to capture market share. High-quality care that avoids expensive rehospitalization will continue to be a major differentiator in terms of referral volume, especially under new payment mechanisms in which medical providers assume risk. Skilled nursing operators that don’t continue to improve on their ability to deliver efficient, quality care for frail elders with multiple chronic conditions may find themselves sidestepped by hospitals, provider groups, and the like.

And by the way, payors aren’t the only entity that wants to keep people out of hospitals. Seniors housing and care residents of all types would rather avoid the unfortunate experience of going to a hospital because of an acute episode—operators who can execute on that customer need will surely have an advantage while simultaneously helping America’s elders experience the best possible quality of life.

Not Your Typical M&A Transaction: HumanGood, A Nonprofit Affiliation

By Anika Hartounian, HumanGood

Changing consumer expectations. Uncertain public and private financing. Disruptive technologies. Rapidly shifting health care alliances. In a dynamic environment where there are more questions than answers, nonprofit affiliations, once rare, are becoming commonplace. Specifically, in the long-term care industry, with rising team member costs and changing demands, more companies feel the need to join forces to remain competitive and, in some cases, to keep their doors open.

Usually when we think of joining forces, we’re thinking of traditional for-profit M&A transactions, where one entity purchases another entity for an agreed upon dollar value in order to improve the financial position of the surviving company. In those cases, the primary consideration is what the transaction will mean for owner or shareholder wealth.

How is this different for a nonprofit entity? The considerations of a nonprofit board are similar to those of a for-profit board when looking at feasibility of business combinations; after all, both companies are looking to run a successful business. However, in a nonprofit setting there are technically no owners or shareholders to consider and there is often no exchange of money. With a nonprofit affiliation, the primary focus is, or should be, mission amplification. Even in situations where one nonprofit is being merged out or is becoming a subsidiary of another entity, the focus of the nonprofit board should relate to the mission of the entity.

HumanGood, now one of the largest nonprofit senior living providers in California, is a product of a recent affiliation transaction between two industry leaders: be.group and American Baptist Homes of the West (ABHOW). John Cochrane, president and CEO of HumanGood, shared his thoughts below about the recent nonprofit affiliation.

What drove this affiliation between two financially stable but independent organizations?

Cochrane: Our affiliation allows us to do more good for more people and remain competitive in an increasingly challenging environment. This was not a takeover by one organization; this was two strong companies with similar missions coming together to do more, do better, and go faster. Our combined organization has the greater strength, stability, scale and resources to meet the changing needs of a growing senior living market. Our goal is to be one company highly focused on being the best at what we do with the support and commitment of our boards, team members and residents.

How did the affiliation transaction unfold?

Cochrane: The affiliation between be.group and ABHOW was completed on May 1, 2016, with final approval from the California Attorney General and the California Department of Social Services. Our respective boards met and approved the affiliation after months of due diligence and integration planning and after all necessary amendments were made to articles of incorporation and bylaws. At this point, Dave Ferguson, ABHOW’s president and CEO was ready to retire and transitioned into an executive advisor role following 25 years of service and leadership, and I was named president and CEO of our combined organization.

What does HumanGood represent and how would you describe its now unified mission?

Cochrane: The new brand symbolizes our deep commitment to the idea of living and aging well for all people in all circumstances. HumanGood is the coming together of our two organizations with rich histories of serving older adults and their families. Developing the new brand took into account our mission to redefine the meaning of aging well for adults 55 and older; and our organization’s winning aspiration is to be the leading innovator in delivering enriched and engaged experiences with optimal health and measurable life fulfillment.

We will achieve our goals by focusing on three areas:

- Reimaging the customer experience in the CCRC

- Growing our national footprint in affordable housing

- Developing new products and services to meet the needs of the middle market

Everyone desires to live a life with enthusiasm, purpose and security, regardless of their circumstances. The products and services we offer are designed to better support our residents and their families, as well as our team members, in the pursuit of an engaged, purposeful life.