A Conversation With Kass Matt, President of Lancaster Pollard: A Capital Funding Provider That Understands the Industry

Kass Matt

Ask Kass Matt what makes capital funding provider Lancaster Pollard different, and his answer is simple: “We understand the complexity of seniors housing and health care.” As president of Lancaster Pollard, Matt and his team recognize the value of knowing the operational details of the industry to create greater value for their clients.

Matt joined the company 12 years ago and has served as its president since 2015. Through its four affiliated companies, Lancaster Pollard offers a full range of investment banking, mortgage banking, private equity, balance sheet financing, and M&A advisory services. Lancaster Pollard is based in Columbus, Ohio.

NIC Senior Principal Lana Peck recently talked with Matt about his firm’s approach and where he sees the market headed. Here are excerpts from their conversation.

Peck: Can you tell us about yourself and your role at Lancaster Pollard?

Matt: I lead the firm’s national efforts in providing capital funding for the senior living and health care sectors. Specifically, I oversee the firm’s senior housing/health care banking, agency, M&A, private equity, and finance company platforms. In my 12 years at Lancaster Pollard, I have served as an investment banker, regional manager, and most recently, as president.

Peck: How long has Lancaster Pollard been involved in the seniors housing and care sector? Why did your organization enter into the space?

Matt: We are celebrating our 30th anniversary this fall. We are dedicated to the senior housing and health care space. Lancaster Pollard’s founders recognized the underserved and largely misunderstood market in health care and senior living financing, but saw the growth potential in those sectors. We took advantage of the opportunity, realizing we could recommend and execute on more advantageous capital funding solutions and outcomes to our clients by specializing in the senior living sector. Our team had the foresight to recognize that most of the financial services firms serving the senior living market were not specialists in the sector. The idea was that if we could focus on a complex and dynamic industry, and we understood it well, then we could create a greater value for our clients. We would be able to articulate the strengths of the projects better and, hopefully, achieve better execution on our client’s behalf.

Peck: What do you like about the seniors housing and care sectors? What are the opportunities?

Matt: Seniors housing and care is growing, and well on track to becoming a widely-accepted asset class. There is great demand for the product. But it is a complex industry that requires deep knowledge of the operations.

Peck: What are the challenges? How are they different today from five years ago?

Matt: Five years ago, we saw a significant growth in demand for services, but there was a lack of new supply largely because of a lack of capital in the space. Today, where we could get worried is when a significant velocity of capital floods the space, and we end up in a situation where capital is chasing deals rather than deals chasing capital. That’s not a healthy balance, and you can get upside down pretty quickly.

Peck: Do you provide debt and equity financing to all seniors housing segments, i.e., independent living, assisted living, memory care, and skilled nursing care? For-profit versus not- for-profit providers?

Matt: We provide financing solutions for both for-profit and not-for-profit providers across the entire continuum of care. Our operations are national, as we have approximately 25 regionally-focused bankers with deep, long-standing relationships in their respective local markets.

Historically we have been more of a long-term care lender, given our experience with HUD programs. The complexities of skilled nursing and the need for that care model intrigues us. Despite some recent negative press, we recognize the significant importance of that care model.

Peck: What about CCRCs?

Matt: We have financed numerous CCRCs throughout the years, with one recent example being a bond offering for Wesley Woods at New Albany, a CCRC that recently opened near Columbus. The bond market is healthy for well-supported projects in good markets.

Peck: Any markets you like or avoid?

Matt: We subscribe to the NIC MAP® service and pay daily attention to the data. Even in markets flagged by NIC, however, we find submarkets that are strong. Such a submarket may have little to no competition for the products one is offering, therefore they represent a market opportunity for the right well-capitalized provider.

Peck: Are you focused more or less on primary or secondary markets?

Matt: Our portfolio is evenly distributed between primary and secondary markets, depending on the operator’s strategy.

Peck: What constitutes a strong operating partner for you?

Matt: We look for a sponsor with a strong track record of development, an effective and successful care model, and best-in-class operations. We have many long-term clients that fit this profile.

The strength and capitalization of the operating sponsor is critically important. We rely on operating partners to bring us projects that they are looking to construct in a certain market. We look at their track record of filling similar projects in similar markets. We conduct our own due diligence to get comfortable with the project.

Peck: How many projects do you fund in a year?

Matt: We complete approximately 200 financings a year. The sponsors run the gamut from a small mom-and-pop operator to a large operating company. The projects vary as well, including refinance, construction, sub rehab, and advisory services, among others.

Peck: Can you describe how Lancaster Pollard works with the Agencies?

Matt: Lancaster Pollard is an FHA/GNMA-, FNMA- and USDA-approved lender. In regards to FHA, we have been the #1 HUD Lean lender cumulatively since FY 2010, recently surpassing the $5 billion mark in total par amount over that time span. A couple of years ago, we invested in our FNMA production with the hires of industry veterans Casey Moore and Doug Harper, and as a result our market share with that agency has been steadily increasing. In fact, when looking at all agency transactions combined, we did almost $1.2 billion in our fiscal year 2017.

Peck: How healthy is the agency lending market?

Matt: It’s a very healthy lending environment reflective of the fact that interest rates are still low and amount of capital in the space is still strong.

Peck: How do you decide between agency financing versus balance sheet lending?

Matt: All of our balance sheet lending through Lancaster Pollard Finance Company is geared toward a permanent agency takeout. Therefore, the two are intertwined.

There are different structural criteria between opportunities that are immediately eligible for agency financing versus those that will be eligible in the near term, with the latter staying on the balance sheet for up to three years. But in all cases, the ultimate goal is permanent, long-term financing via an agency takeout.

Peck: Do you provide financing for the operations of the business or the cash flow businesses as well?

Matt: No. Everything we do is real estate based.

Peck: Can you tell us about the Propero Seniors Housing Equity Fund?

Matt: Propero is a private equity fund established by Lancaster Pollard to invest in seniors housing properties across the continuum including independent living, assisted living, memory care and skilled nursing.

The fund seeks to be the sole owner of each property and utilizes a triple-net lease structure. We look to partner with best-in-class operators of any scale to fund the new development as well as the acquisition of these property types.

One of the key differentiating features of Propero is the ability to incorporate near-term purchase options in the lease agreement, which can provide significant value to our operator clients. Our goal is not to be the long-term owner, but to be bought out of a construction project after stabilization, assumed to be an average between 36 and 42 months. We just recently launched our Propero Fund III and, when looked at cumulatively with Funds I & II, we have raised in excess of $150 million in committed capital.

Peck: When do you turn down an opportunity? Are there any immediate red flags?

Matt: A red flag for us is a deal without a well-heeled and experienced operator. Seniors housing and care is an operating model to create value in the real estate. We are not interested in a deal without an operator vested in the success of the project.

Peck: Where is pricing headed? Will valuations be affected by a higher interest rate environment?

Matt: Overall, our view of the current M&A environment is that it is somewhat surprisingly robust. The REITs are doing big deals and the private REITs, private equity and the owner/operators make up enough of a buyer universe (those that are active) to support M&A processes that are attracting significant activity.

Peck: Is there further room for cap rate compression? Where will cap rates be in 12 months?

Matt: Cap rates have a natural ebb and flow, and we have seen them bounce off the low point, leveling out at its current healthy state. Cap rates generally lag behind interest rate moves, and, despite the recent activity, overall long-term rates are generally below historical averages. This leads us to expect cap rates in the near term will maintain current ranges. Cap rates for seniors housing range from 7% to 8.5% and for skilled nursing range from 12% to 13%.

Peck: Any worries that keep you up at night?

Matt: If you would have asked me this question 18 months ago, I would have said finding a partner to help fuel and accelerate the growth of our company and to support our clients’ strategic initiatives would have been my main concern. We had previously been majority owned by a private equity fund facing the expiration of its stated investment period. This is not a concern anymore, however, as we were acquired by ORIX Corporation USA last fall.

ORIX USA is a division of leading international financial services group ORIX Corporation. ORIX USA is headquartered in Dallas and also owns RED Capital and Boston Financial, a tax credit syndicator. We have maintained our focus on seniors housing and care and we’re thrilled with the confidence that one of the largest global financial services companies has shown in our platform and employees, and together we are positioned for a new chapter in our company’s history, focused on innovation and growth.

Peck: Any other thoughts you would like to share?

Matt: As far as the senior living industry in general, we couldn’t be more bullish on the direction it’s headed and the great work our clients are doing—from providers who are combatting ageism by redefining what senior living should look like, to those expanding their services to ensure every senior receives top-notch care, regardless of acuity level. We look forward to continuing to evolve our platform so we can be a trusted capital partner and advisor to our clients as they strategize for a better tomorrow.

Thoughts From NIC’s Chief Economist

Beth Mace

Welcome to the second-longest postwar job expansion period. In April, the duration of this economic recovery reached 107 months, exceeding the 106-month expansion of the 1960s, but still falling short of the record 120-month job growth period enjoyed in the 1990s. The economy continues to move forward at a good clip by most measures. Through the first three months of the year, job gains averaged 208,000, stronger than the monthly pace of 182,000 in 2017. Strong employer demand for labor, in turn, has pushed the unemployment rate lower, and in April it fell to 3.9%—its lowest level in 18 years. Only two other times in postwar history has the unemployment rate been lower (1953 and 1969).

Today’s unemployment rate is below what generally is believed to be the “natural rate of unemployment” of 4.5%, which strongly suggests that there will be growing upward pressure on wage rates. While elusive for some time, there is beginning to be greater evidence that this is starting to take place. Over the past 12 months, average hourly earnings have increased by 2.6%, while the employment cost index, another measure of wage pressure, rose by 2.7% from year-earlier levels in the first quarter, faster than the 2.4% pace in the comparable prior year period.

The Federal Reserve is carefully watching the economy for signs of other inflationary pressures, such as tariffs and the resulting impact on higher import prices, as well as rising commodity prices around the globe. In anticipation of further wage pressures and in reaction to a strengthening economy, the Fed has raised interest rates six times since 2015 after having kept them near zero for seven years. Most recently, the Fed increased the fed funds rate 25 basis points at its March 20/21st FOMC meeting to a range between 1.50% and 1.75%. Most analysts expect there to be another 25-basis point increase announced by the Fed at its June FOMC meeting, followed by a few more later in the year.

Seniors Housing Inventory Growth. Switching gears to senior housing market fundamentals, first quarter data showed continued downward pressure on occupancy rates, with assisted living occupancy falling to its lowest level on record. The occupancy rate for all of seniors housing (independent and assisted living) for the 99 markets tracked by the NIC MAP® Data Service, showed an occupancy rate of 88.1% in the first quarter, its lowest level since mid-2011 and down from 90.0% as recently as Q4 2015. During the nine quarters since then, seniors housing inventory growth (70,000 units) has exceeded the increase in demand, as measured by net absorption (47,000 units), by 23,000 units.

Based on these data, the occupied penetration rate for seniors housing in the 99 markets was 9.9% in the first quarter, defined as occupied units divided by the number of households over 75 in the 99 markets. If the occupied penetration rate increased by 20 basis points to 10.1%, the occupancy rate would be 90.0% based on first quarter inventory levels. For this to happen, an additional 17,000 units would need to be absorbed, a number very achievable since more than this number of units were absorbed on a net basis in the past four quarters.

For another perspective on the magnitude of these numbers, it may be helpful to look at the multifamily sector, where completions (inventory growth) as a share of total inventory equaled 1.8% in 2017 according to estimates by CBRE, the equivalent of 266,000 units. For seniors housing, inventory grew by 30,000 units from year-earlier levels in the first quarter for the 99 markets. While seemingly small on the surface, for seniors housing, this equals a 3.3% increase in inventory. A comparable estimated increase for the nation would be roughly 45,000 units if we assume that the 99 markets represent approximately two-thirds of the national inventory which is the 99-market share of households 75 year and older relative to the nation. And, a comparable increase of 3.3% in apartment stock would translate into 490,000 units or 41,000 units per month. The sizeable disparities of course are due to orders of magnitudes of differences in the stock of multifamily units versus seniors housing. Indeed, the multifamily sector is significantly larger than seniors housing (14.7 million units versus an estimated 1.4 million seniors housing units at the national level or 927,000 for the 99 markets).

Another way to gain perspective is to compare the estimated 45,000 units of new supply delivered in the past year against the demographic growth in the number of Americans in the age 83 plus year cohort for the comparable period. The selection of age 83 plus may be viewed as a proxy for those individuals that could be potential residents in seniors housing. Based on recently updated estimates from the Census Bureau, in 2017 this equated to 8.5 million individuals. In 2018, an additional 138,000 people are projected to age into the 83 plus cohort, and by 2025, the Census Bureau estimates that there will be 10.2 million people in this cohort, equating to an increase of 1.6 million people over the eight-year period from 2017 to 2025. With a penetration rate of roughly 10%, this suggests the need for 164,000 additional units of seniors housing supply over this eight-year period. If we assume that the national annual run rate of 45,000 units of stock added in the past 12 months continues, then 164,000 units would be added in 3.7 years, outpacing the potential eight-year demand requirement. There are two ways by which to prevent this imbalance, both of which could be done in whole or in part. Assuming a static penetration rate going forward, the first approach would be to slow the rate of new supply delivery to below today’s pace. The second approach, assuming that the current pace of inventory growth is sustained going forward, would be to boost demand by growing the penetration rate toward the high-teens from roughly 10% today.

As always, I welcome your feedback, thoughts, and comments. Let’s keep the discussion going.

Beth

NIC Launches Skilled Nursing Quality Metrics

New Challenges

NIC is expanding and enhancing its core NIC MAP® product to include quality metrics data for the Skilled Nursing sector. This major product enhancement is made possible through a strategic relationship with PointRight®, a leading provider of quality metrics data and predictive analytics.

Being in network and having visibility into healthcare outcomes is becoming increasingly important among skilled nursing providers in a value-based world. To this end, investors seek to have a sense as to how their skilled properties benchmark within their respective markets.

CMS and its Five-Star rating system, while not the only source of quality measures, is an important source of data for determining eligibility for certain referrals. In addition to CMS, pioneering companies are accessing publicly-available data sets and applying their own proprietary algorithms to estimate various additional outcome metrics.

New Solutions

Quality metrics, while always important to the sector, have become more important than ever, as a result of recent changes in the healthcare delivery system. Some of the benchmarking that this data makes possible is not available anywhere else. It will enable operators and investors to better understand the performance of properties and markets when underwriting new deals, managing portfolios, developing strategies, competitive benchmarking, and gathering market intelligence.

NIC MAP clients will now have access to a suite of quality metrics data and analytics from PointRight, which is now available through the NIC MAP client portal. NIC MAP users will now be able to include quality metrics data in their analysis, alongside NIC MAP data, such as market performance data, demographics, wage and employment data, hospital locations, and more.

The following Quality Metrics reports are now available, according to subscription level, at both the metropolitan market and property levels:

- PointRight Pro 30® Adjusted Rehospitalization Rate

- PointRight®Pro Long Stay™ Adjusted Hospitalization Rate

- CMS Overall Five-Star Rating

- CMS Survey Deficiencies (Property level only)

Why PointRight?

PointRight is an industry leader in analytics for post-acute and long-term care, specializing in data-driven quality metrics solutions. The PointRight Pro 30® scores are certified by the National Quality Forum, which means they have undergone considerable examination by a panel of experts. Furthermore, the metrics are endorsed by the American Health Care Association (AHCA).

Serving over 8,000 skilled nursing facilities, PointRight data provides investors, operators and payors the data they need to understand these facilities in terms of quality and performance. Data such as rehospitalization rates, CMS quality measures, resident-level risk scales, professional liability risk, and CMS Five-Star ratings, will now be seamlessly integrated into our NIC MAP product.

Accessing the Data

To learn more about how your organization can benefit from this initiative, please email us at sales@nic.org or call 410-267-0504.

2018 Health Datapalooza: NIC Presentation

Bill Kauffman

NIC recently participated in Academy Health’s Health Datapalooza conference on April 27, which was the first time that NIC was part of the event. Health Datapalooza is an annual event that convenes a diverse group of strategic thinkers and problem solvers who share a mission to deliberate on and consider new ways to use data to improve health and healthcare policy and practice. It is an event which prides itself on sitting at the nexus of ideas, evidence, and execution.

Representing NIC was Bill Kauffman, Senior Principal in the Outreach Group, who provided a presentation to the conference attendees. The presentation allowed NIC to connect with the broader healthcare audience and, specifically, provided a discussion on the growing relevance of seniors housing and care within the broader context of healthcare. NIC consistently seeks to deliver on its mission of enabling access and choice in seniors housing and care by attracting and educating private sector capital, especially institutional capital (primarily pension funds and endowments), about the demand for and investment opportunities in seniors housing and care. This event further allowed NIC to deliver on its mission. Indeed, as healthcare transformation progresses, data and analytics are becoming critically important to provide insights to all stakeholders within the continuum of care including seniors housing and care.

NIC’s Datapalooza presentation showed how reliable data is addressing the needed transparency that allows capital to flow into the seniors housing and care sector. Essential to this effort has been the provision of data that delivers transparency of operational, financial, and investment performance comparable to other commercial real estate sectors. The result of these and other initiatives is that the seniors housing and care property sector is now an established investment category that attracts significant capital from institutional investors.

Seniors Housing Middle Market

In a new effort, NIC is focusing additional attention on the middle market or middle-income senior population. Our goal initially is to generate interest from investors, researchers, and policymakers regarding the size of this opportunity. The middle market is defined as the population of seniors who are too wealthy to qualify for government-supported housing and care (primarily Medicaid), but who often cannot afford today’s private pay housing and care options.

NIC’s middle-market study will include quantitative research that measures current and future demographic, socio-economic, health and care need characteristics of middle-income seniors. This data will help attract and educate private sector capital, thereby creating the investment case for middle-market seniors housing. The research will be based on data from the Health and Retirement Survey (HRS), and is being conducted by NORC at the University of Chicago.

This study is very important and timely since the housing setting is emerging as the platform to manage and coordinate the delivery of health services. Indeed, there is a growing recognition of the crucial role played by housing—including seniors housing—to health outcomes. This study is expected to be completed by year-end 2018, with results shared at a 2019 Policy Summit in Washington D.C. and at an Investment Summit in New York City.

Skilled Nursing Data Initiatives

In addition, NIC’s Datapalooza presentation highlighted the need for timely, accurate and consistent data for the skilled nursing sector. There is a significant need for capital in the sector which is undergoing tremendous change. Not only does the sector need capital for continued real estate infrastructure improvements, but also for operational enhancements and innovations.

However, institutional investment capital requires timely data. Many sources have plentiful data points, including government data sources, but the data is old and with a sector changing so rapidly, many investors do not find much utility in such data. At the conference, NIC presented highlights of the monthly data it collects including the managed Medicare data which is vital to operational and investment decisions given the growth of Medicare Advantage.

Lastly, and consistent with data and collaboration, NIC discussed the importance of quality metrics and its recently announced partnership with PointRight. Through NIC’s partnership with PointRight, NIC MAP® Data Service subscribers will have access to the following PointRight reports at both the metro and property levels:

- PointRight Pro 30® Adjusted Rehospitalization Rate

- PointRight®Pro Long Stay™ Adjusted Hospitalization Rate

- CMS Overall Five-Star Rating

- CMS Survey Deficiencies (Property level only)

For more information about 2018 Health Datapalooza, you can visit: http://www.academyhealth.org/events/site/2018-health-datapalooza

PDPM: Skilled Nursing Industry Continues Trend Towards Value-Based Reimbursement

Ryan Chase

Brandi Healey

In this article, NIC Future Leaders Council Members Ryan Chase, managing director at Blueprint Health Care Real Estate Advisors, and Brandi Healey, vice president, asset management at Sabra Health Care REIT, discuss the benefits of the new CMS Patient Driven Payment Model methodology for the skilled nursing industry.

In April 2018, the Centers for Medicare and Medicaid Services (CMS) released its proposal to systemically redesign the Medicare Part A skilled nursing facility payment structure. Effective October 2019, the current reimbursement system, RUG-IV, will be replaced by a new methodology, known as the Patient Driven Payment Model, or ‘PDPM’. This is a “generational” transition that, if implemented, will have widespread implications for skilled nursing operations in the years to come. Statistically, the PDPM is an improvement to the RUG-IV system and should produce a net benefit to the industry, as it enhances payment accuracy and reduces administrative costs imposed by regulation.

The shift from RUG-IV to PDPM reflects a change in the incentives that drive reimbursement. In its simplest form, RUG-IV is primarily driven by volume, specifically therapy minutes. PDPM reflects the resident’s clinical condition. This is the latest iteration in a sequence designed to better align reimbursement to care and outcomes. Consistent with the tenets of Accountable Care Organizations, Medicare Advantage, skilled nursing Value-Based Purchasing and alternative payment models such as Bundled Payments for Care Improvement, the healthcare industry continues to transition towards value-based care and targeted, patient-specific reimbursement.

So, what’s the Patient Driven Payment Model?

The PDPM is a refinement of CMS’ recent effort to establish a new payment system, one focused on rewarding providers through metrics other than care volume and utilization. Prior to the announcement of PDPM on April 27, 2018, CMS introduced reimbursement reform last year through the Resident Classification System (‘RCS-I’). The PDPM incorporates feedback from providers and industry experts who expressed concern about the system’s complexity, composition and administrative burden. Rick Matros, CEO of Sabra Health Care REIT, noted in their latest earnings release that, “We’ve never really seen this level of collaboration between CMS and the industry before, so that’s greatly appreciated.”

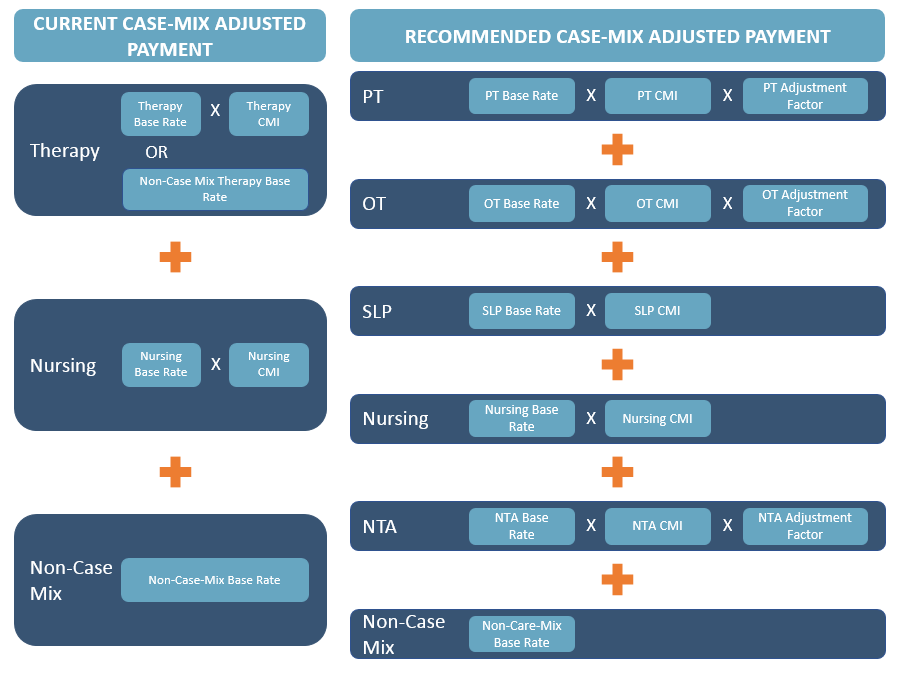

The PDPM is a budget-neutral refinement to the current RUG-IV system that improves payment accuracy by strengthening the relationship between reimbursement and clinical needs of residents. The PDPM accomplishes this in a few ways. First, therapy minutes are no longer tied to reimbursement; whereas, under RUG-IV, the number of therapy minutes provided was a key determinant of the per diem rate. The design of PDPM adjusts this central incentive. Second, the model stratifies the therapy component of RUG-IV into three groups, each assigned individual case-mix indices. Third, it creates a case-mix adjusted component for non-therapy ancillary services (‘NTA’), whereas the current RUG-IV model lacks such sensitivity. In total, there will be five case-mix adjusted components in PDPM, which include: physical therapy, occupational therapy, speech & language pathology, nursing and non-therapy ancillary services. By linking reimbursement to resident characteristics as opposed to care volume, a more robust range of clinical needs can be rewarded in a skilled nursing setting. See below for visual graphic that outlines the two systems.

What does this mean for operators and investors?

Skilled nursing providers have been preparing for value-based reimbursement for several years by increasing their clinical competencies and improving quality. According to Marc Zimmet, CEO of Zimmet Healthcare Services, “PDPM is not a funding change – it’s a reweighting of the revenue-delivery system. By definition, there will be winners and losers; but because CMS can only model a new system based on previous experience, transitions of this magnitude create a short window wherein providers modify behavior and capitalize on mispriced services.” A similar situation occurred in 2010 when CMS proposed a budget neutral change to the RUG-IV system. Providers experienced significantly higher Medicare payments than CMS had intended so CMS readjusted rates downward in 2011.

Operators will be more incentivized for treating medically complex patients and should experience increased rates for nursing care, despite possibly decreased therapy revenues. Reimbursement accuracy for nursing services will increase as therapy minutes will not supersede clinical characteristics of Medicare A residents. PDPM also permits providers to deliver limited concurrent and group therapy, thus reducing overall therapy costs and increasing efficiency to both the provider and the patient. Reimbursement focused on resident conditions, as opposed to the number of therapy minutes delivered, should reduce the number of issues and costs to providers in disputing fraudulent billing claims and Office of Inspector General investigations, saving valuable time and resources. Further, obligatory resident assessments are reduced to only require assessments for a five-day admission and discharge assessment, and a special assessment to reflect changing care needs, estimated to save the industry $2 billion in administrative costs.

While the potential positive outcomes outweigh the negatives in this reform, they do come with uncertainty of how to maximize the benefits. The new system requires providers to develop a strategy to understand and implement the required changes within their organizations and systems. These changes could also unintentionally impact payors other than Medicare. For example, would managed care organizations or Medicare Advantage plans revise reimbursement rates to reflect the PDPM changes? While the proposed changes appear significant, especially the decreased focus on reimbursement based on therapy minutes, providers can thrive under the new system. Matros noted that “operators always follow the incentives so expect to see significant changes in behavior on the part of operators as they start emphasizing nursing patients and not just solely rehab patients.” It’s critical for investors to understand how their operating partners plan to proactively address the new changes.

Asked what operators can do to end up with a net win in the new system, Zimmet offered this advice, “PDPM represents a major philosophical shift in skilled nursing reimbursement. The system holds opportunity for nearly all industry stakeholders, but the initial transition will prove challenging for the unprepared. While much has been made about enhancing clinical capabilities for PDPM, most skilled nursing facilities care for a relatively sick population today. The key is appropriately documenting the care already being provided (such as respiratory therapy) to support reimbursement capture – that’s the behavior change that moves a provider into the ‘win’ column.”

The Caregiver Crisis: A Conversation With Glenn Barclay of Blake Management Group

Jenny Zhao

In this article, NIC Future Leaders Council member, Jenny Zhao, assistant vice president and associate analyst at AEW Capital Management, L.P. talks with Glenn Barclay, co-founder of the Blake Management Group about his experiences in successfully navigating labor challenges in the senior housing and care industry.

We are at the cusp of a major demographic shift. The U.S. population is aging, and rapidly. The oldest Baby Boomers (born between 1946 and 1964) are just turning 72 years old. While the bulk of this cohort remains the adult-child decision-maker for today’s seniors housing and care resident, the Baby Boomer cohort will eventually find themselves the receivers of care.

Given the sheer size of this cohort (at an estimated 76 million Americans) and the declining birth rates that followed the Baby Boomer generation, these trends will lead to fewer adult children caregivers available to support seniors. Current forecasts estimate that the ratio of caregivers (defined as 45-64 year olds) to those over 80 will shrink from 7:1 today to 4:1 by 2030.

The future shortage of caregivers will have huge operational, economic, and social implications for the sector, our economy and our society. Layered on top of this, and as a more immediate challenge, is the state of today’s labor market. The jobless rate is at a record low, while other data show that the U.S. economy is now in the second longest job expansion in post-war history (at 107 months), and job openings continue to exceed hirings.

As the co-founder of a premier seniors housing operator, Glenn Barclay understands first-hand the challenging environment our sector finds itself in. It has become increasingly difficult to hire and retain the ideal staff at all levels of the organization, from frontline staff working directly with residents to the leadership at a community to management in the home/regional office. Future Leaders Council (“FLC”) member Jenny Zhao recently spoke with Barclay about the state of the caregiver crisis and what strategies operators are using to mitigate this. Here is a recap of their conversation.

Zhao: Could you please tell us about the Blake Management Group (“BMG”) and your role there?

Barclay: Blake Management Group (“BMG”) is an industry leading seniors housing operator with communities throughout the South and Gulf Coast. I am co-founder and an advisory board member at BMG. While I served as COO until 2016, I now am solely focused on pre-opening operations, building development and design, while supporting all aspects of operations for BMG. We strive to provide the aging population with a better lifestyle at competitive prices.

When my mother-in-law was aging, my wife and I couldn’t find any seniors housing option that provided enough socialization, care, or supervision to provide us with peace of mind. This personal dissatisfaction was a major catalyst for us to create our brand. Our company and properties are named after my son, Blake, who had a very special relationship with his grandmother, and we took a lot of aspects that were important to us, my son, and his grandmother, and built them into our brand’s foundation and culture. And so, we are proud to say that our communities are the nicest in our markets and include innovative amenities that really go above and beyond what the typical seniors housing community would offer.

Glenn and Blake Barclay

Zhao: How long has BMG been investing in the seniors housing and care sector, and what sets you apart from your competitors?

Barclay: BMG was founded in 2006. We opened our first community in Gulf Breeze, Florida in 2008. Since then, we have expanded and currently operate 14 communities spanning eight states. We continue to grow but remain strategic as we keep our vision and culture a priority. We will have a total of 18 operating communities by the end of the year, and we are very excited about the 12 new developments in our pipeline (delivering in 2019-20) and being able to provide seniors housing to these communities.

The idea of aging in place is very important to us. When a resident moves into one of our communities, we want it to be the last move they make. We want our community to be their home, and we have built our operating model to fully support a philosophy of aging in place. Indeed, we intentionally overstaff our communities with robust wellness and clinical programs that allows for a continuum of care. This means all BMG communities are equipped with 24-hour nursing care, outpatient therapy and a primary care practice that are available to our residents on-site.

Zhao: Given the current demographic and labor market backdrop, do you think there is a caregiver crisis? If so, has BMG experienced higher turnover and/or difficulty finding staff?

Barclay: Without a doubt, the biggest challenge in our sector is recruiting and retaining new staff. We see it across all departments and levels, from entry to executive level positions. Overall, it has become a challenge to find the right people with the right skillset and the right heart to do what we do every day. And increasingly, we are finding that the skillset required is getting harder to meet as our industry matures. For example, an executive director at one of our communities needs to have a strong background not only in multi-department operations, but also in healthcare, management, sales, and hospitality. There are unfortunately few programs available that fully train someone for this position.

With regards to turnover, we make it one of BMG’s top initiatives, and as a result, we have been able to reduce our turnover and increase retention. We review turnover percentages by property and as an organization at least every month. We have 10-12 focus areas within the broader turnover issue that we are constantly looking to improve. Specifically in our frontline staff, the day shift remains relatively stable, while the afternoon and night shift employees tend to exhibit higher turnover as these team members usually have less interaction with the rest of the team. As a way to mitigate this, we have all staff start their training during the day shift. We also plan regular breakfasts and other engaging opportunities for our overnight staff to help them stay connected with other departments and the leadership team.

Zhao: When BMG is looking at developments, how long in advance do you start recruiting new staff? Have you ever walked away from an opportunity due to labor force conditions?

Barclay: For all new developments, we start recruiting 17-18 months prior to opening, well before we even break ground. We have never walked away from an opportunity due to the labor environment simply because it’s never gotten that far. We are very market driven and target markets, not land sites. We know that a connection to the community is not only crucial to support sales, but also to recruit the right people. We do hands on, grass roots networking, which includes cultivating relationships with local churches, civic organizations, social services agencies, and participating in local fundraisers and events.

We also talk to local colleges to see if they have nursing programs or other study programs that we can form relationships with. In the past, we have partnered with local colleges to have student nurses do their long-term care clinicals at our communities. We use this to not only educate future generations about the career opportunities within our sector, but also introduce them to life at BMG and show them a realistic career path. Further, we produce videos with Heart Legacy and other media production agencies that are uploaded to our website and social media platforms. These videos help us communicate BMG’s philosophy and core values of accountability, compassion, integrity, joy, fun, and leadership. When you visit our website (please see https://bmgseniorliving.com/), the first thing you see is a video designed to inspire and connect to the heart of the viewer. We use these videos to relay our brand and mission, and as a recruiting tool to attract people with similar core values who are a good, cultural fit.

While we use traditional career finding services, we find that our retention rate is higher through our grass roots networking. And we know it works! We have one Blake community where nearly the entire legacy leadership team remains intact three years since opening, which is very rare. This team remains passionate about what they do, engaged in our mission, and loyal to our organization.

Zhao: What strategies do you use to recruit and retain talent? What kind of training do you provide new hires, and in what format does this take place?

Barclay: From our own experience and what we know about the industry, we know the biggest reasons we lose people are from lack of engagement and lack of training. So our commitment to retention really begins during the interview process where we highlight the opportunities for growth and advancement. I, myself, began my career in healthcare as an entry-level rehab tech at The Well Mill Rehabilitation Agency and Disability Services of the Southwest, where I ultimately grew to become the president of the company and president of the board of directors during my tenure. This personal journey of mine is one of the reasons why we encourage growing and promoting from within. Furthermore, all applicants will watch a day-in-the-life video and conduct a peer interview. This allows candidates to really learn about their roles and ask questions in a more casual environment.

We also have a learning management system that guides new hires through a very structured onboarding program where the leadership team is very engaged from the start. All BMG new hires go through a mentoring program where they are paired with a “champion” at their particular community and sister communities. These champions not only excel at their jobs, but also help convey our message and live and breathe our culture. Further, our goal for all new hires is to have lunch with their executive director within the first two weeks on the job, which further helps us see how new hires are progressing in their development. The first 90 days of employment is critical to ensure our new team members are getting comfortable and competent in their new job role. When new hires have passed their competency program and the formal onboarding process is complete, they continue to have regular checkpoints with their department leader and executive director.

We find it important to recognize and reward our staff for their achievements. Our Champions Program is one of the ways we do this. We have champions across all positions and levels within our organization that we are grooming for growth. We have had frontline staff who moved up the ranks to director level positions, and we love to see that!

Zhao: And how has recruiting for talent changed from 10 years ago?

Barclay: While our sector will always have a strong care component, we do see the hospitality and customer service aspects of the business growing. We are ultimately selling a lifestyle to our residents and we need people who understand that. To this end, we have grown more open to recruiting candidates outside our sector with a non-traditional background.

Zhao: Does BMG implement any new technology related to staffing? If so, how has technology helped to increase efficiencies and address the caregiver crisis?

Barclay: Yes, our communities are equipped with the most updated technology. First, we have our learning management system that I touched on already, which provides online development to all our staff. We also have state-of-the-art nurse call and point of service systems, both of which increase efficiencies and make the jobs of our staff easier, which directly helps retention. Our nurse call system includes motion detectors in select memory care units. This helps our care team track specific activities that our residents make and allows our team to better respond to the needs of our residents. Meanwhile, our point of service system allows servers to take orders on a handheld device, which directly sends orders to the kitchen. Servers are then able to mingle with residents in the dining area until they are alerted when the order is ready for pick up.

Zhao: What other challenges do you see for the sector, near-term and long-term? Any that we have missed in this discussion? Are there broad solutions that are not being implemented?

Barclay: Moving forward, one of the biggest challenges will be expense control. We see wages increasing across all levels and positions in response to other sectors raising their wages, but rents can only go up so much to stay competitive.

And related to this, another big issue will continue to be turnover and employee engagement. We really see seniors housing as the “adolescent” of healthcare in that it is the newest product to come into the industry and is constantly evolving and maturing. And with that, we still have a lot to learn. I think we will start seeing more and more players looking at success stories outside our industry to help us address our internal challenges.