Welcome to the August edition of the NIC Insider Newsletter.

Gain insight from VIUM’s Steve Kennedy and Kass Matt on underwriting standards, the impact of the regulatory environment, opportunities for the sector, and more in their interview with NIC Principal Bill Kauffman. Trever Sweeney features the drivers and foundational concepts behind active ownership of senior housing real estate that help position portfolios and partnerships for success. Dig deeper into senior housing supply and demand. NIC Principal Omar Zahraoui presents a new metric called the absorption-to-inventory velocity, which indicates the effectiveness of market absorption of inventory. The 2023 NIC Fall Conference is coming up in October, and the article titled, Accelerating Change with the NIC Fall Conference provides a preview of what you can expect by attending. Hint – yes, plenty of networking, and also managing your consumer, investments, and operations will be explored through actionable insights. But that’s not all. NIC Talks are back! Bob Kramer says the industry is at an inflection point and shares the big industry trends that will be discussed to help propel the industry forward.

VIUM: Building a Brand Name A Conversation with Steve Kennedy and Kass Matt

VIUM Capital is making a name for itself. In fact, the name VIUM is related to the word “life”—a good description of what drives the relatively young healthcare lender and its early success.

VIUM Capital is making a name for itself. In fact, the name VIUM is related to the word “life”—a good description of what drives the relatively young healthcare lender and its early success.

Led by industry veterans Steve Kennedy and Kass Matt, VIUM has already achieved a solid track record. The Columbus, Ohio-based firm has closed nearly $4 billion of financings in its first three plus years and was HUD’s second most active healthcare lender in fiscal year 2022.

NIC Senior Principal Bill Kauffman recently talked with Kennedy and Matt, both executive managing directors at VIUM. Here is a recap of their conversation.

Kauffman:Can you tell us about your professional backgrounds?

Matt: After 10 years in corporate banking, I joined healthcare lender Lancaster Pollard in 2006 and spent 14 years there. That’s where I met Steve. We helped to grow the company to the largest provider of HUD-insured healthcare loans nine out of ten years. Following the sale of Lancaster Pollard in 2017, we left in 2019 and started VIUM in 2020. Our team has spent the past almost two decades exclusively financing healthcare and seniors housing. VIUM means “to revive or give life to a partnership.” That partnership, with our VIUM team, our clients, and the alignment with Merchants Capital, has proven to be a special combination in the success we have had in the past three plus years.

Kennedy: I started at Lancaster Pollard as a college intern and spent my career there until we started. Kass and I learned a lot from Tom Green and Brian Pollard, the sole owners of Lancaster Pollard until Stone Point Capital’s investment in 2013. We gained valuable insights into how to construct a finance company for the senior housing and care sector.

Kauffman: What’s different about VIUM?

Kennedy: Lancaster Pollard was not a balance sheet lender. That didn’t matter much 15 years ago. But now it matters to have proprietary control over short-term capital in order to execute permanent loans with HUD, Fannie Mae, and Freddie Mac. We are fortunate to have Merchants Capital as a minority partner. They have a 30 % stake in what we do. Merchants has skilled leadership, a unique bank balance sheet, and is a good fit for us for many reasons. Additionally, we acquired Armstrong Mortgage Company in order to have our own HUD/GNMA license, as well as the skillset of Armstrong’s servicing head, Rima Herd. During our time at Lancaster Pollard, we developed meaningful relationships with Merchants, Armstrong, Bellwether (with whom we partner for GSE loans), and other organizations and personnel that turned out to be valuable. These relationships were the important building blocks of VIUM. But we are a flat organization. We have four additional minority partners (in Chris Blanda, Scott Blount, Brendan Healy, and Tony Ruberg) who are more than just proven top-tier bankers and excellent managers; they are leaders of VIUM and owners. We are all aligned and work closely to collectively guide our firm’s growth.

Kauffman: What is the size of VIUM’s portfolio of loans to senior housing and skilled nursing?

Matt: We currently have $2.6 billion in bridge loans in our portfolio. We have originated and executed a little over $3 billion in bridge loans. Our ability to underwrite bridge loans to a permanent takeout, primarily to HUD, is coming to fruition today. While volume this year has normalized relative to last year’s record levels, we have a tremendous pipeline. Our portfolio mix is approximately 75% skilled and 25% seniors housing, however virtually all of our portfolio is licensed.

Matt: looking for properties with strong operators, reasonable leverage and generally some form of recourse. While cost of capital and credit spreads has evolved, our approach to structuring credit has remained consistent.

Kauffman: How has the rapid rise in interest rates impacted the business in 2023?

Kennedy: It has not impacted our approach. But it has absolutely impacted the industry since other capital providers have paused their lending programs, tightened loan-to-value requirements and added more covenants. We want VIUM Capital to be thought of as always being there. Our parameters are consistent. We are covenant light. We allow earn outs so borrowers can recoup some or all of the equity they have put into a project. We want to be there for sponsors and operators in tough times.

Matt: Certainly volatility and the rapid rise in interest rates has made deals more challenging to structure. On the other hand, we are underwriting all our bridge deals to the permanent markets. With the inversion of the yield curve and floating rate bridge pricing higher than long term fixed rates, we are seeing loan duration compress and a desire to get to permanent markets faster. Lastly, we are using interest rate derivatives (primarily in-the-money interest rate caps) to help offset higher bridge pricing.

Kauffman: There’s much discussion about the tightening of underwriting standards from debt providers. Is that true for VIUM? How so, and what is the expectation going forward?

Kennedy: I don’t think our underwriting standards have really tightened up that much. But it’s important to remember what we do and what we don’t do. Our goal is a clear line of sight to permanent financing. We are not doing direct, new construction financing, or deep turnarounds. We fund acquisitions and recapitalizations that meet coverage ratios on day one. We work with proven, well capitalized sponsors who are regional experts. That’s our niche. Our loan-to-value ratio is upwards of 80%, which is solid for this sector.

Kauffman: How are you underwriting properties?

Kennedy: We are underwriting skilled nursing facilities with cap rates that have held up in the 12% range. Though interest rates have risen, we have the capacity to absorb that coverage. That’s a strength of ours. We make sure our bridge loans will obtain permanent financing. We are locking up rates for borrowers in the 5% to 6% range with a 35-year non-recourse mortgage from HUD.

Matt: Senior housing is a bigger challenge. With cap rates generally lower than interest rates, it’s more challenging to make the numbers work. So, that part of the market has slowed.

Kauffman: How will that play out with so much senior housing debt coming due?

Matt: There are good owner/operators with solid banking relationships that will be able to restructure or extend loans but, in some cases, may require an additional equity contribution. We saw senior housing providers push through significant rent increases, but that has largely run its course. Now the industry has to continue to stabilize, improve occupancies, and keep cost structure in check. The lack of new supply in the near term is a good thing.

Kauffman: Has the regulatory environment had any impact on you or your borrowers?

Matt: We have been in the space for a long time having been through a number of regulatory cycles. On the positive side, several states are approving Medicaid reimbursement enhancements meant to get reimbursement in line with today’s cost.

Kennedy: Scott Tittle joined us two years ago. He was the head of the National Center for Assisted Living (NCAL), which along with its parent, the American Health Care Association (AHCA), represents assisted living and skilled nursing providers. He worked closely with AHCA President and CEO Mark Parkinson for six years. Prior to leading NCAL, Scott was head of the Indiana Health Care Association for five years; that’s where we got to know each other. Being an advocate alongside our clients is really important and a competitive advantage of ours. We are not just providing capital but standing arm-in-arm with them. The big regulatory challenge out there right now is the minimum staffing ratio requirement. We don’t know what the ruling will be, but Mark Parkinson has helped coalesce the industry. The Biden Administration is trying to ensure appropriate care, and that is something we all want. But putting in a minimum staffing ratio is likely to have the opposite effect. We all know there are not enough LPNs and RNs, and it’s not realistic or helpful to mandate staffing ratios. We are hoping when the ruling comes out that it will at least take into consideration how to fund the mandate and set realistic ratios over some period of time. Scott Tittle reminds us that divided government is probably good for our industry to make sure everyone has a seat at the table during policy discussions.

Kauffman: Have you heard anything about the timing of ruling on staffing?

Kennedy: We hear that it will be announced this year, but it keeps getting pushed

back.

Kauffman: What is your outlook for the rest of the year?

Kennedy: Looking at the market globally, we see two trends ahead. The skilled nursing merger and acquisition market is about to come back at a significant level. The primary driver is the improvement in Medicaid reimbursements. Once we have three to six months of trailing cash flow at those higher rates, seller and buyer activity will be triggered as well as refinancings and restructurings. So, for us as a lender, we view Q423 to be the beginning of a relatively strong merger and acquisition market. We also forecast that next year will hopefully be the beginning of a more typical senior housing market. Operators cannot keep raising rates 10% to 12%. Inflation is normalizing. Occupancy has increased to 83.4%, up from its low. But it’s still 300-400 basis points below pre pandemic levels. With the passage of time without external pressures, we think we will see the beginning of a more normal senior housing market.

Matt: The continued seasoning of our portfolio, improvement in Medicaid reimbursement, and the inverted yield curve are driving permanent loan opportunities. We have about $500 million of loans in active stages with HUD. We think HUD volume next fiscal year will be very strong. We are growing our underwriting, analytical, and asset management team to support the volume.

Kauffman: What opportunities do you see for the sector?

Kennedy: The need for affordable assisted living is so great. We’ve seen success in Illinois’ Supportive Living Program which uses tax credits, Medicaid, and private pay sources. This creative capital structure has led to an asset class with over 95% average occupancy. Other states are looking at affordable assisted living programs which is a big opportunity. VIUM is uniquely positioned as a HUD lender to engage as a public private partnership to meet a critical social need.

Matt: NIC’s study on the “Forgotten Middle” highlighted the importance of the issue. We need to figure out how to provide an attractive product at an affordable price that generates a return for owner/operators.

Kennedy: I’d like to add that VIUM is a licensed municipal advisor. We understand the bond world. Also, our partner Merchants is a large affordable multi-family lender. These unique attributes positively position us to serve the affordable seniors housing need. But above everything at VIUM, our most competitive advantage is our culture. We believe we have the best culture of any company in Columbus, Ohio, and of any seniors housing and healthcare lender in the country. We are focused on our clients and our community in a very authentic way with an absolutely great team.

NIC Talks Returns to Main Stage at 2023 NIC Fall Conference; Speakers offer Insights into the Future

Ice hockey star Wayne Gretzky famously said, “I skate to where the puck is going, not where it has been.” It’s a well-known quote that sums up the idea behind the thought-provoking and popular NIC Talks series which returns live this year to the 2023 NIC Fall Conference. Four experts will give 12-minute TED-style talks on cutting edge ideas that will impact the senior housing and care industry.

“NIC Talks is back,” said Bob Kramer, NIC co-founder/strategic advisor and founder at Nexus Insights, who is curating the session. “It’s never been more important to hear what the future holds for senior living.”

As the industry’s thought leader, NIC debuted NIC Talks in 2015. It quickly became an attendee favorite by provoking discussion at a national level with speakers from both inside and outside of the industry.

After a 2021-2022 hiatus, NIC Talks will once again give Fall Conference attendees a preview of what’s next for senior living. “The timing is right for a NIC Talks reboot,” said Kramer. “The industry is at an inflection point.”

The pandemic has obviously had a seismic impact on the industry, compounded by the continuing workforce crisis. A rapid rise in interest rates has led to turbulence in the capital markets. At the same time, the industry is preparing for a new customer, the baby boomers, with their own take on how they want to live.

The speakers will offer forward-looking visions on how to prepare for this new environment. “Join us,” said Kramer. “Come to NIC Talks to be inspired to change, rather than to be scared to change.”

The 2023 NIC Fall Conference will be held October 23-25 at the Sheraton Grand Chicago Riverwalk. NIC Talks will be a featured session on that Tuesday, October 24.

Kramer expects this year’s speakers to offer prescient insights just as past presenters have accurately anticipated big industry trends.

For example, John Cochrane, president and CEO at HumanGood, speaking at NIC Talks in 2016 said, “We need to move from retirement to reengagement and from reactionary healthcare to proactive lifestyle management.” The pandemic highlighted the critical role of senior housing in keeping residents out of the hospital, and that residents want and need engagement.

In 2017, Dan Buettner, author of The Blue Zones, which identifies places where people age well, spoke about finding purpose, eating well, moving naturally, and the importance of place. What he was describing were the social determinants of health—critical factors for a successful senior housing community.

In 2018, Chinwe Onyeagoro, then president at Great Place to Work U.S., gave a talk about the importance of making the staff feel like they belong and that they can trust their managers. The pandemic proved her right, said Kramer, adding, “Companies that took care of their staff were able to pay it forward to keep the residents safe.”

Timely Topics

This year, NIC Talks will focus on themes that echo many of the objectives of NIC’s new five-year strategic plan: partnering for health; the needs of the middle market; age technology; and the new customer.

Here’s what attendees can expect to learn:

- The importance of the integration of housing and healthcare. “For too long, there has been an artificial divide between housing and healthcare,” said Kramer. “Now we realize both are critical to wellness and longevity.”

- The value of a “customer first” approach, using the hospitality model as a template for success.

- How to use a problem-solving mindset to find the best technology solutions to increase staff efficiency and resident satisfaction.

- The impact of artificial intelligence on senior housing and care. What does it mean for residents and staff? How can providers keep up with the rapid pace of radical change?

Like great hockey players, the presenters at NIC Talks sense where things are going. “They’re ahead of their time,” said Kramer.

What follows are more examples of previous NIC Talks that predicted market trends. Click here to watch from our archives.

Lynne Katzmann, Juniper Communities, 2015. “Senior living is bought as a default because we are associated with the negative aspects of aging. Boomers want independence, privacy, and choice. The problem is they don’t think we can deliver.”

Tom Grape, Benchmark Senior Living, 2019. “We no longer think of ourselves as a senior living company. We are now a human connection company.” The next generation of residents is looking for a sense of community.

Lisa Ryerson, AARP Foundation, 2018. “Let’s reimagine the role of activities director into a purpose matchmaker. It’s not about coming up with activities but about connecting people to give them a sense of purpose and belonging.”

Dwayne Clark, Aegis Living, 2018. “Employees need to trust that managers will have their back. It’s a real relationship, not a transaction.” Treating employees like people who have lives that matter outside the workplace helps reduce turnover.

Joseph Coughlin, MIT AgeLab, 2016. Technology that enables people to stay in their homes six months longer represents a $34 billion shortfall to the industry. Develop relationships through technology that enable you to go beyond your fences and partner or white label—a practice that became much more common during the pandemic.

Dan Cinelli, Perkins Eastman, 2020. Connect people by their interests not the level of their frailty. The importance of connection is one reason why investors are

so excited about the emerging active adult segment.

Jo Ann Jenkins, AARP, 2020. “A lack of integration between housing and healthcare not only increase costs, but also puts the independence of older people at risk.”

Susan Dentzer, PBS analyst on health policy, 2018. The emergence of the hospital at home movement is changing where healthcare services are delivered. Senior living residents want to receive healthcare where they live. The pandemic brought this trend to the forefront.

Jacquelyn Kung, Activated Insights, 2015. It’s important to engage with the staff. Retention hinges on employees knowing someone cares about them and their growth.

Register now to attend the 2023 NIC Fall Conference and NIC Talks.

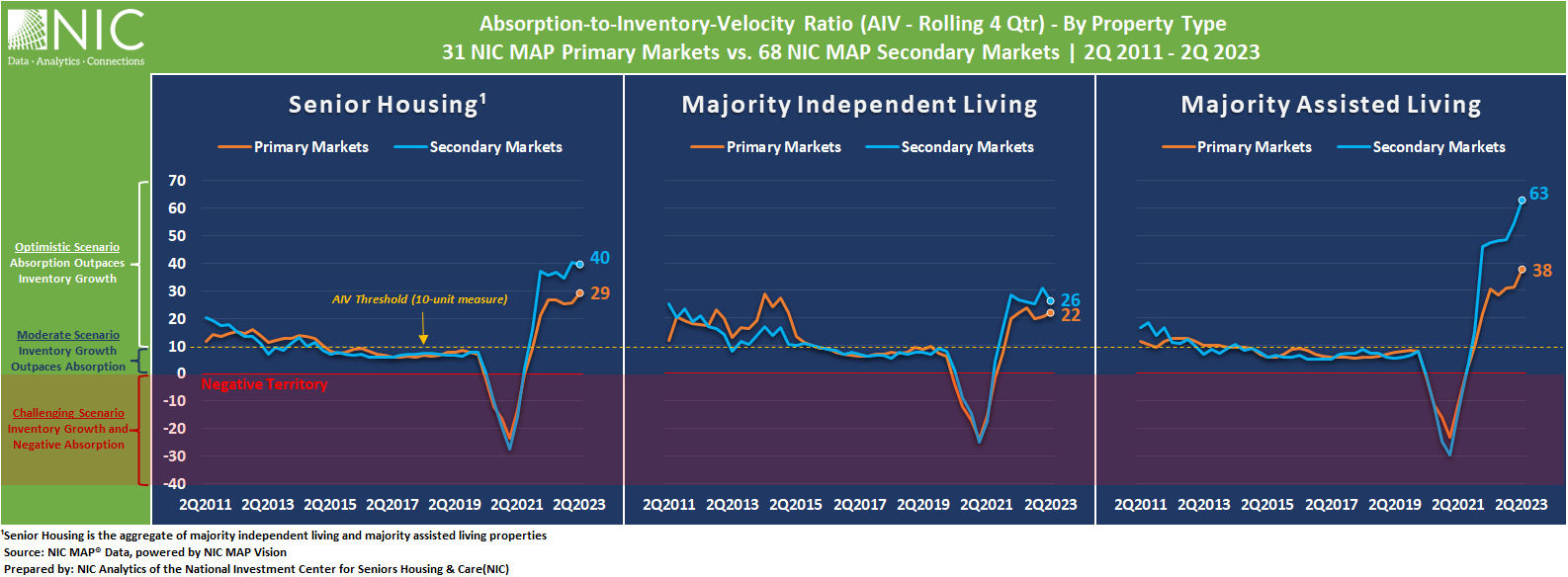

An In-Depth Analysis of Absorption-to-Inventory Velocity (AIV) in Senior Housing

By Omar Zahraoui, Principal, NIC

To add perspective on senior housing demand and supply dynamics, NIC Analytics has created a new ratio for consideration. This new measure offers a nuanced perspective on the balance between demand and supply. Called the absorptionto- inventory velocity (AIV), this metric is calculated by dividing the number of newly occupied units within a given time by the number of new units added to the market inventory during the same period. The ratio serves as an indicator of how effectively the market absorbs or leases the newly supplied units on a net basis.

In this article, NIC Analytics explores the various scenarios associated with the AIV ratio and examines the ratio’s patterns over distinct phases: the pre-pandemic period, the pandemic peak, and the recovery phase, with a particular focus on senior housing property types (i.e., majority independent living and majority assisted living) and NIC MAP market aggregates (i.e., the 31 NIC MAP Primary Markets and the 68 NIC MAP Secondary Markets). In next month’s NIC Insider, a second article will dive yet deeper into the ratio’s trends across the U.S. regions.

Understanding the AIV Ratio: Scenario Breakdown and Interpretation

NIC Analytics is using a 10-unit measurement as the AIV threshold, which serves as a benchmark to interpret the ratio. When the AIV ratio is above or below the 10-unit threshold, it provides a sense of whether absorption, as measured by the change of occupied units, is outpacing or being outpaced by inventory growth, allowing for a better understanding of market dynamics based on these supply and demand conditions. In essence, it allows us to understand that, for every set of 10 units added to the market, the number of units which have been absorbed over a specified time period.

NIC Analytics identified three scenarios defined by the AIV ratio:

Scenario One: A higher positive ratio (above the AIV threshold of 10 units) with stronger absorption relative to the inventory velocity, indicating a healthier balanced market, and resulting in an increase in occupancy. This optimistic scenario is currently unfolding in the senior housing sector during its recovery phase.

Scenario Two: a lower positive ratio (below the AIV threshold of 10 units) with slower absorption of newly added units, potentially signaling an oversupplied market or weaker demand. This moderate scenario is marked by a decline in occupancy and occurred in senior housing during the five years preceding the pandemic.

Scenario Three: a negative ratio (below zero) with negative absorption and continued inventory velocity. In this scenario, the AIV enters negative territory. For senior housing, this challenging scenario occurred in just six quarters. During the history of the time series which began in 2005, this occurred in the first quarter of 2009, the first quarter of 2015, and four consecutive quarters during the pandemic from the second quarter of 2020 to the first quarter of 2021.

AIV Ratios Across Property Types and Market Aggregates: A Comparative Analysis

The exhibit below illustrates the fluctuations in the AIV ratio, tracked on a rolling four-quarter basis since 2011. This is categorized by majority property type for both the 31 NIC MAP Primary Markets and the 68 NIC MAP Secondary Markets.

This analysis examines the fluctuations in the AIV ratio over recent market periods. From a prolonged phase during the teens of occupancy declines – a consequence of inventory growth outpacing absorption – to the heights of the pandemic that was marked by negative absorption and continued inventory growth, and finally, a resurgence of positive absorption amidst a a market with an overhang of supply during the recovery phase. The shifts differ among property types, with assisted living with its higher acuity trend and registering an all-time high AIV ratio.

Given the historical trend pattern and barring any significant disruptions similar to the pandemic, it appears unlikely that the AIV ratio for majority assisted living will dip below the AIV threshold in the near future, and thereby causing prolonged occupancy declines. This is because new inventory growth is likely to remain constrained in the near term due to capital market challenges and the need-based nature of demand for assisted living. It is important for senior housing constituents to stay informed about these trends to navigate effectively through this dynamic but generally improving market.

AIV during the pre-pandemic period.

In the five years preceding the pandemic, the AIV ratio (on a rolling 4-quarter basis) for both NIC MAP market aggregates (NIC MAP Primary Markets as well as NIC MAP Secondary Markets) moved in tandem but was below the AIV threshold, referred to as the moderate scenario. This indicates that inventory growth was surpassing absorption, which resulted in a prolonged phase of declining occupancy before the pandemic struck. This trend was evident in both majority independent living and majority assisted living property types, but was most pronounced in assisted living where new supply increased at an unsustainable pace.

AIV during the pandemic peak.

The AIV ratio (rolling 4-qtr) for both NIC MAP market aggregates plunged into negative territory during the pandemic (challenging scenario), with the Secondary Markets experiencing a slightly sharper decline. Specifically, over the four-quarter pandemic peak ending in 1Q 2021, the AIV ratio for senior housing plummeted to -23:10 for the Primary Markets and -28:10 for the Secondary markets. This means that for every 10 new senior housing units added in each of the Primary and Secondary Markets aggregates, there was a negative absorption of 28 and 30 units, respectively. Hence, supply continued to be added to the market at a time when demand was also very weak. The capital market conditions that were in place prior to the pandemic supported inventory growth during the pandemic period despite concurrent weak demand associated with the pandemic health crisis. This not only shows the magnitude of the challenge faced by senior housing during the pandemic but also reveals how negative absorption amplified the growth occurring in inventory.

AIV during the recovery phase.

Since 2Q 2021, the senior housing market has witnessed nine consecutive quarters of positive absorption. The AIV ratio (rolling 4-qtr) for both NIC MAP market aggregates exceeded the AIV threshold during this period (optimistic scenario), particularly in the Secondary Markets. Over the four-quarter period ending in 2Q 2023, the AIV ratio for senior housing surged to 29:10 for the Primary Markets and 40:10 for the Secondary Markets, which implies that for every 10 newly added units, 29 and 40 units were absorbed, respectively.

As for property types and over the same period, the AIV ratio for majority independent living was 22:10 for the Primary Markets and 26:10 for the Secondary Markets. This indicates that for every 10 new units introduced in each of the NIC MAP market aggregates, 22 and 26 units were positively absorbed, respectively. However, these AIV ratio levels were not the highest on record for majority independent living. Both the Primary and Secondary Markets experienced slightly higher AIV ratios before 2015.

During the same period, the AIV ratio for majority assisted living was 38:10 for the Primary Markets and 66:10 for the Secondary Markets. This means that for every 10 new units added, there was positive absorption of 38 and 66 units in the Primary Markets and Secondary Markets, respectively. These AIV ratios for majority assisted living properties reached an all-time high, far exceeding any level recorded since NIC MAP Vision began reporting data in 2005, suggesting an ongoing trend of high acuity demand in the senior housing market. Notably, assisted living occupancy for the Secondary Markets was 83.6% in 2Q 2023, and was only 0.6pps below its first quarter 2020 levels (84.2%).

Despite the notable improvements, however, a substantial number of senior housing units remain unoccupied in both the Primary Markets and Secondary Markets – 113,348 and 53,854 units respectively. Additionally, there are 34,401 and 15,057 units under construction in these respective markets. Given these figures, the senior housing market still has a significant supply capacity to absorb the inventory growth experienced during the pandemic, a situation that was further exacerbated by negative absorption during that period. The AIV ratio measurements suggest that the market’s recovery will likely be sustained during the near-term given current supply and demand conditions.

Accelerating Change With the NIC Fall Conference

The senior housing and care industry is at an inflection point. Increased costs are affecting operations, lending and securing capital is both challenging and expensive, and consumer preferences continue to shift as baby boomers get closer to entering the doors of senior housing communities. This period of change requires industry leaders to be nimble, innovative, and collaborative. It also requires strong connections, which lead to sharing of ideas, solutions, and capital.

NIC knows that today’s leaders need concrete, actionable insights that will help propel their business forward. The 2023 NIC Fall Conference is the accelerant to ignite change.

In addition to the best-in-class networking opportunities and unmatched insights, this year’s program is designed for action. Attendees will learn what works and what doesn’t directly from fellow operators, investors, lenders, association leaders, and more—those who are already innovating to meet the new customer where they are and grow their businesses amid market and operational challenges.

Here is a preview of the Main Stage program at the 2023 NIC Fall Conference to help you take action:

Managing Your Investments

It’s no secret that dealmaking has been constrained due to the fluctuating economy and capital markets. Higher interest rates and tightening credit markets make it significantly more expensive and difficult to borrow money. Senior housing and care leaders are carefully and closely monitoring market trends and the economic climate to navigate the best path forward. The 2023 NIC Fall Conference will paint the picture of the current landscape and share ideas with leaders for how to not just survive but thrive.

The economic keynote has become a NIC Conference staple and will once again lay out the current risk environment and how potential policy decisions could affect the industry. Additionally, a panel of lenders will detail current underwriting criteria and financing terms while explaining the circumstances that led to current debt market challenges.

In the valuations session, industry insiders will discuss how valuations are being determined amid the currently challenging capital markets. They’ll also share the inside scoop on how investors are rethinking their strategies as they look to opportunistically deploy capital. These sessions will speak to current investment trends and the market outlook for 2024.

Managing Your Consumer

For years, the industry has discussed the coming wave of baby boomers. Now, with this generation on the doorstep, we know more about their health status, housing needs, and preferences. Forward-thinking industry leaders who want to attract this consumer must prepare products with the characteristics sought by this consumer, and especially at a price point they can afford.

Fall Conference speakers will chart future consumers across various segments, from active adult rental properties to full service senior living to middle market. Speakers will outline consumers’ characteristics, housing preferences, finances, and more, and how community design, programming and operations should adapt to attract them. They’ll also touch on emerging trends, best practices, and new technologies that can shift boomers’ perceptions of senior living by prioritizing socialization and wellness.

As older adults age, memory care will become more necessary, even for traditional independent living operators who are seeing higher acuity residents. There have been major developments in memory care research in recent years. A representative from the Alzheimer’s Association will discuss the latest data and how senior housing and care operators can use it to prepare and care for the coming wave of older adults.

Managing Your Operations

The combined shock of the pandemic and the disruption in the capital markets provide an opportunity for operators and capital providers to rethink their business models. The CEOs of Ventas and Welltower will share how they are reshaping their companies for long-term sector growth, along with the strategies they’re using to proactively manage their portfolios and strengthen operator relationships. Another panel will discuss the evolution of management companies and their associated challenges and opportunities.

Finally, one of the biggest factors influencing the success of any senior living property, and ultimately the health of residents, is its staff. The senior housing and care industry is just one profession being challenged to attract and retain frontline workers, yet we know that a satisfied, reliable staff means better care for residents. Operators speaking at the 2023 NIC Fall Conference will share key research findings related to staff turnover (HINT: it’s not only due to pay—it’s culture and inclusion, too). The executive panel will discuss how to provide advancement opportunities for staff and what investment is needed to fund such programs, so attendees can ramp up their own retention programs.

This industry is no stranger to challenge and change. It faced the financial crisis of 2008, and again in 2020 with the COVID pandemic. Weathering today’s turbulent economy and capital markets to serve older adults requires transparency, collaboration, and adaptation. The NIC Fall Conference brings together industry experts at the forefront of accelerating change so they can share their biggest ideas and most effective solutions exclusively with NIC attendees.

Will you join us in Chicago this October?

Active Ownership: Understanding Drivers and Foundational Concepts

By Trever Sweeney, Vice President, Senior Living Asset Management, Ventas, Inc.

By Trever Sweeney, Vice President, Senior Living Asset Management, Ventas, Inc.

The senior housing sector has experienced significant growth coming out of the pandemic and is poised for continued success over the coming years, driven by strong industry fundamentals and underpinned by a rapidly aging population. Owners of senior housing real estate can capitalize on the opportunities in this evolving landscape by positioning their portfolios and partnerships for the greatest chance of success and embracing a paradigm of active ownership that has become increasingly crucial.

Active ownership in its simplest form refers to the hands-on engagement by senior housing real estate owners. The active ownership approach relies on a cycle of high-touch relationship management, developing a deep understanding of senior housing operations, and taking modern, proactive, value-add steps for the success of a portfolio. This article discusses the industry landscape and dynamics driving active ownership as well as highlighting the foundational concepts comprising an active ownership approach.

1. Evolution of REIT Ownership Structures

Over time as the senior housing industry has evolved, NNN-lease structures, where an owner receives a predictable rent stream and an operator has full access to upside harvesting in exchange for full downside risk (plus a credit backing), have fallen out of favor. The industry has so few of the players for the NNN game, with many operators being thinly capitalized. But that aside, the operational intensity of the senior housing business requires a structure that lends itself to operator and owner alignment, not impasse.

Management contracts have clearly gained favor with the two largest healthcare REITs. Ventas and Welltower now own over 1,500 communities subject to management contracts, a three-fold increase over the last ten years, and against a horizon that started with both REITs being majority NNN-leased in their senior housing businesses. Many owners have seen this massive portfolio shift as communities either moved from NNN to management contracts during the last decade or were newly built during the post-GFC and pre-pandemic senior housing supply boom when many new partnerships were struck.

The bottom-line exposure of management contracts, relative to the implied certainty of a NNN lease, requires a far different approach to management and therefore changes the dynamic of the owner-operator partnership. The shift has led owners to needing to better understand the intricacies of the business, assess operational efficiency, and actively contribute to strategic decision-making. Sustained active ownership has become essential to achieve the desired financial

results of investors.

2. The Best Partners Understand the Operations

An active owner needs to be in the field, collaboratively ideating new strategies and problem solving with regional operational leaders. Participating owners need to arrive on-site with good data and enthusiasm and be prepared to facilitate discussion, as the days of a templated owner inspection have gone by. The field is where process improvements or flaws incubate and can be a forum to identify leading indicators of significant issues and prompt swift action. This is just one of the process flows of turning insights into action, a key to effective active ownership.

An excellent partner-owner will have open lines of communication with operators, fostering transparency and trust. The cadence of meetings and level of engagement needs to be higher than it’s ever been. A good owner has both alignment with operating executives and engagement with the regional team supporting their communities. This insight-sharing engagement involves information pulls and pushes – and getting that balance right is critical. In a successful engagement, the owner supplements existing data flows to operational decision-makers, and the value provided by pushing new insights to those close to the field outweighs the effort of the required to get the data. There needs to be a unified approach towards achieving success.

On occasion, consulting resources have to be called in for certain specific addressable issues. Perhaps the tour-to-move-in ratio at a certain community or specific operator is below what you would expect for the community size, reputation, care type and current occupancy, and incremental sales consulting or training resources would help resolve. In other cases, it’s back-office and billing related that requires incremental support. Turnover happens in the field and owners and operators alike should be judicious about identifying when external resources are needed to bolster capabilities. They’re admittedly not cheap, but if you know who to call and when, the return always hits.

3. Leveraging Data and Analytics

In today’s data-driven world, the effective use of data and analytics is a vital component of active ownership. Senior housing owners must develop their own analytics platforms to intake and access: (1) real-time data on sales activity to spot leading indicators and accurately assess the health of the sales pipeline, (2) resident care levels, satisfaction, and move-out reasons and (3) expense detail in its individual components, including wages and hours for staffing. This information, if properly organized and mined, empowers owners to make data-backed recommendations, identify trends and issues, and proactively address potential challenges. Our team at Ventas often calls this use of data and analytics “issue spotting,” a shorthand terminology for a robust process that starts with the data and insights and flows through the critical step of pushing those actionable insights back out to our operating partners in senior housing, with follow-up accountability.

Effective owners in senior housing should complement and become a resource for operating partners, who often are unlikely to have the resources or technical expertise to make a meaningful investment in a robust data platform. The onus is on the owner to build the platform, intake the data, spot the issues, and push learnings, recommendations, and insights back to operating partners. A data-driven approach ensures that owners and operators can make informed decisions based on objective metrics rather than relying solely on subjective evaluations.

4. Proliferation of Operator Transitions

Operator transitions have been occurring at an unprecedented frequency coming out of the pandemic, as many communities fail to meet owners’ performance expectations. The change of scenery can be a value-creating action, but the match of operator and community requires meticulous consideration. A change in management, when not done thoughtfully, can disrupt a critical consistency in care that residents expect.

Operating companies are not commodities, but no owner should expect perfection. The critical threshold question for an owner is understanding their own needs and that of their portfolio. Market familiarity and local relationships are widely acknowledged as considerations pre-transition, but it can be a tough decision to weigh the cultural benefit of a team that’s small and local that may be accompanied by a potential lack of understanding owner data-reporting needs that come from more large-scale experiences.

Few operators carry the requisite corporate overhead necessary to dedicate a resource to the seamless project management of an onboarding. Owners should avail themselves and their talent to significant transition involvement. An excellent transition program ensures that both outgoing and incoming managers are collaborating, issues are quickly resolved, and owners are flagging potential issues based on their past experiences. The idea that transitions are disruptions and materially destructive to cash flows for up to a year is simply not accurate. With an active owner, an eager incoming manager, and an appropriately incentivized and cooperative outgoing manager, value can be preserved with limited diminution of census and cash flow at the community level.

By providing comprehensive onboarding and ongoing support, owners can minimize disruptions and facilitate a smooth transition for both residents and employees. This proactive involvement helps in maintaining the reputation and stability of the senior housing community, thereby safeguarding the long-term value of the investment.

5. Aligned Incentives through Management Contracts

Management contracts between operators and owners play a crucial role in aligning incentives and fostering successful partnerships. Contracts outline roles and responsibilities and establish standard operating procedures for an owner-to-manager relationship, ensuring that both parties work towards a common goal. The best contracts will align financial incentives, incentivizing operators to optimize not only top-line revenue but operational efficiency, resident satisfaction, high quality care, and financial performance.

Aligned incentives of a properly structured contract will create a win-win scenario, where operators are motivated to deliver exceptional care and operational results, while owners benefit from increased property value and sustainable returns. Active ownership in the context of management contracts includes ongoing monitoring of operator performance, providing guidance and support when needed and facilitating continuous improvement initiatives. This active engagement drives operational excellence and promotes long-term success.

Conclusion

Active ownership has become indispensable in the senior housing sector, positioning REIT owners to understand operations, be valuable partners to operators, leverage data and analytics, navigate operator transitions, and foster aligned incentives through management contracts. By actively engaging with operators and leveraging their expertise, owners can enhance the overall quality of senior housing communities, improve financial performance, and ensure long-term value creation. With the aging population continuing to grow at record rates, active ownership will remain a key driver of success in the senior housing sector.