Financing Powerhouse Rebrands Itself as Lument: A Conversation with Aaron Becker

Rebranding a company after several mergers makes sense. It gives the new entity a single purpose and direction. ORIX Real Estate Capital rebranded itself last October as Lument.

Rebranding a company after several mergers makes sense. It gives the new entity a single purpose and direction. ORIX Real Estate Capital rebranded itself last October as Lument.

Lument includes three legacy brands well known in commercial real estate and seniors housing and care finance: Red Capital Group, Lancaster Pollard, and Hunt Real Estate Capital.

NIC Chief Economist Beth Mace recently spoke with Aaron Becker, senior managing director at Lument. They discussed the new name and the direction of the company. They also talked about Lument’s response to the pandemic and what’s ahead for the industry.

Here’s a recap of their conversation.

Mace: Lument is a new name for your organization. Can you tell us about the new entity and the name change?

Becker: Lument is the result of the merging of three industry leaders in the multifamily, affordable housing, seniors housing and healthcare space: Lancaster Pollard, Red Capital, and Hunt. We are bringing these three entities together to share our financial resources, human capital, and talent to support our clients with a wide variety of financing products and services across critical commercial real estate segments. With our combined expertise, knowledge, servicing background, and financial products, we can provide more solutions and options for clients.

Mace: What’s unique about the company?

Becker: Lument is a subsidiary of ORIX Corporation USA, an investment capital and asset management services group in the real estate space. ORIX acquired Red Capital in 2010, and Lancaster Pollard was purchased in 2017. They have complementary skill sets on the seniors housing side. Lancaster Pollard has been the top FHA/HUD senior living lender over the past 10 years, and RED is active in multifamily and affordable housing. Hunt has a phenomenal leadership team. These three companies are the best in their class.

Mace: How did you pick the new name?

Becker: We wanted a fresh start from a branding perspective, as we are all moving forward together. The name Lument comes from the word lumen, meaning light and energy. We want to bring light and energy to our clients. That effort and focus will propel our clients forward as we provide solutions to their capital needs.

Mace: What else does ORIX do?

Becker: ORIX Corporation USA is part of ORIX Corporation, an international conglomerate, headquartered in Japan. It is a broadly diversified financial services group with many real estate interests.

Mace: What is your specific role? Can you tell us about your team?

Becker: I’m the head of production for our seniors housing practice. I manage our seniors housing production team and work with the underwriters. We have more than 20 loan originators across the country. Part of my job is finding new products and services that we can offer our clients, as well as helping our production team serve their clients.

Mace: What types of financing options does Lument offer that are specific to the seniors housing and care sector?

Becker: Together, over the last 10 years, we have been the top HUD lender in the seniors housing space. We are authorized to underwrite, close, and deliver Fannie Mae and Freddie Mac loans. We offer balance sheet lending, debt syndication, bond financing, advisory services, and transaction execution. Our Propero seniors housing equity funds invest in projects; we are now on our third fund and contemplating a fourth. The last fund put $250 million of debt and equity to work, and the next one will be larger. The first two funds were privately invested by employees. Now we are bringing in outside investors.

Mace: How big is your loan portfolio?

Becker: Last year, we originated close to $800 million in HUD and agency loans. When you include HUD note modifications, that total is more than $1.5 billion. Our servicing portfolio, for seniors housing and care specifically, is approaching $8 billion, while our total servicing portfolio as a firm is over $47 billion. The relationship with the borrower begins for us at closing. It’s important for clients to know that we are with them in the years ahead.

Mace: What impact has the pandemic had on your activity and business?

Becker: The year started out strongly. Then, when the pandemic hit, a number of deals were put on hold. Operators just didn’t have the time to focus on financing, and we’re sensitive to that. Even though interest rates are at historic lows, our business slowed. Capital moved to the sidelines until it figured out what was going on. Fortunately, the Federal Reserve stepped in with significant programs to get the financial markets moving again. Good operators learned how to manage and adapt in a new environment. Even with this most recent wave of infections, I feel operators are much better prepared. We are getting deals done, and we are getting busy again. More deals will get done as the situation improves.

Mace: How will the vaccine impact business? How quick might we get back to pre-pandemic levels of activity?

Becker: An effective vaccine bodes well for our industry. Our customers and residents are the most at risk to the virus and should get vaccinated first. We’ll see a turnaround in skilled nursing and assisted living. I think people will be more comfortable with elective surgeries followed by transitional nursing care, which will help boost occupancy. On the assisted living side, occupancy is in the low 70% range. People are sticking it out at home another year. They don’t want to want to go into a facility where they have to quarantine for 14 days, and risk getting sick. They don’t want to move to a building where their family can’t visit them. People who have the options to stay home are doing that. I hope with the vaccine people will feel that assisted living is a safe place to move to. Long-term care and memory care haven’t been impacted as much because staying at home is not an option. Those residents need care.

Mace: How do you underwrite deals in a period of uncertainty?

Becker: It’s a fluid situation and will continue to change. The federal government has stepped up big to help this industry. It should do more for seniors housing, but it has done a phenomenal job for skilled nursing. In terms of underwriting, we cannot include money from the government as revenue because it is non-recurring. But that money is on the balance sheet, so it mitigates the risk for us. The cash is there to support debt service if necessary. The expense side has been more fluid, and we can make some adjustments there. Expenses are starting to stabilize. Hero pay and other programs are unwinding. Lenders are adapting.

Mace: Should workers be offered vaccine pay to take the vaccine?

Becker: It makes sense to do that and rebuild confidence in a community. If people feel it’s a safe place, they’ll go back but it will take time. There may be an initial pop in occupancy. But I don’t think we will be back to pre-COVID levels immediately. Strong operators who have weathered the storm will be well positioned.

Mace: What is your view of the current state of the capital market?

Becker: There’s plenty of capital. Some is on the sidelines, but more is being deployed. I think interest rates will be attractive for a year or two. Pricing on long-term loans, where we are active, has moved up about 30 basis points in last few months. But rates will be attractive for a period of time. The Federal Reserve can buy longer dated bonds to bring down yields.

Mace: What is your perspective on new players in the market?

Becker: We are very wary of new players. You have to have a strong operating partner. This is not the kind of industry that you can jump in and out of. Private equity will keep moving into the space. They need to be in the market. They have capital they have to put to work. When the vaccine is more widely deployed, there will be a strong move by capital to come into the market. FHA, Fannie Mae, and Freddie Mac have kept their doors open. Underwriting has changed and is more difficult. But defaults are low, and our portfolio is holding up well.

Mace: What about the public REITs? Are they coming in or out of the market?

Becker: We work with a lot of REITs in our advisory practice on the sell side. We are looking at bringing deals to market in the months ahead. There’s a lot of interest in those deals, and the cost of financing is low.

Mace: Where is pricing today? Has the risk premium for seniors housing widened?

Becker: Cap rates spiked early on, moving up 25-50 basis points. Part of that is low interest rates. Operators are better equipped to handle infection control. They know a lot more about the disease now and how to treat it. Cap rates have not moved up as much as initially feared because operations are stabilizing, and interest rates remain low.

Mace: How does the integration of healthcare into seniors housing affect your underwriting? Are deals more complicated?

Becker: We think about that every day. One thing we’ve noticed is that assisted living does what nursing homes were doing 25 years ago. We look at acuity levels and services. We do a deeper dive on operations and the kind of care that is being provided. It’s tougher today because we can’t walk a building and see what care is being provided. Fortunately, technology allows us to see things virtually. But there is no doubt that understanding the operational piece has become a big piece of underwriting. We want to know what policies are in place for infection control; how people are brought into the building; and how the operator has performed during the COVID outbreak. A review of operations is a significant part of underwriting, and that will continue going forward.

Mace: Is there a property type you prefer, either independent or assisted living? Or a continuum of care? What about skilled nursing?

Becker: We do it all. We never want to say we’re staying away from a certain segment and believe in all aspects of the continuum. We’re bullish on the sector long term. With the baby boomers aging, we like where we are. Each part of the continuum has its own risks, and we want to make sure we understand how each segment operates. But every deal stands on its own. We feel comfortable moving forward as long as the deal meets our underwriting criteria.

Mace: In your crystal ball, what are you optimistic about? Pessimistic about?

Becker: We love the seniors housing space. The vaccine is here, and the demographics going forward are quite strong for the industry. We love the business we’re in. But I think we have a road ahead from a recovery standpoint. Occupancy isn’t going to jump to 90% overnight. We will get there, but it’s going to take some time, patience, and fortitude.

Mace: Anything else you’d like our readers to know?

Becker: This year, we’ve really deepened our relationship with our clients because we were able to help them in a time of need. It goes back to the Lument philosophy that the relationship starts at closing. We feel fortunate that clients are comfortable coming to us for help, and we love being able to provide solutions for them. When we get past this, we’ll be able to look back and say we were there for them and our partnerships have been strengthened.

Executive Survey Insights Wave 17: November 30 to December 13, 2020

By Lana Peck, Senior Principal, NIC

“The pace of move-ins continued to be sluggish in Wave 17, with more survey respondents reporting declines in occupancy rates than increases in occupancy for each of the four care segments. Fewer organizations cited stronger resident demand as a factor influencing the pace of move-ins. Comments by survey respondents added color to the key survey findings: several leaders of their organizations cited rising COVID-19 cases among residents and staff in some properties resulting in stress with containing outbreaks and maintaining staffing levels amid wage growth and hazard pay challenges. While some operators were eagerly anticipating arrival of the vaccine, others expressed frustration with new slowdowns in the turnaround times for receiving COVID-19 lab test results.”

“The pace of move-ins continued to be sluggish in Wave 17, with more survey respondents reporting declines in occupancy rates than increases in occupancy for each of the four care segments. Fewer organizations cited stronger resident demand as a factor influencing the pace of move-ins. Comments by survey respondents added color to the key survey findings: several leaders of their organizations cited rising COVID-19 cases among residents and staff in some properties resulting in stress with containing outbreaks and maintaining staffing levels amid wage growth and hazard pay challenges. While some operators were eagerly anticipating arrival of the vaccine, others expressed frustration with new slowdowns in the turnaround times for receiving COVID-19 lab test results.”

—Lana Peck, Senior Principal, NIC

NIC’s Executive Survey of operators in seniors housing and skilled nursing is designed to deliver transparency into market fundamentals in the seniors housing and care space at a time when market conditions continue to change. This Wave 17 survey includes responses collected November 30 to December 13, 2020 from owners and executives of 80 seniors housing and skilled nursing operators from across the nation. Detailed reports for each “wave” of the survey and a PDF of the report charts can be found on the NIC COVID-19 Resource Center webpage under Executive Survey Insights.

Wave 17 Summary of Insights and Findings

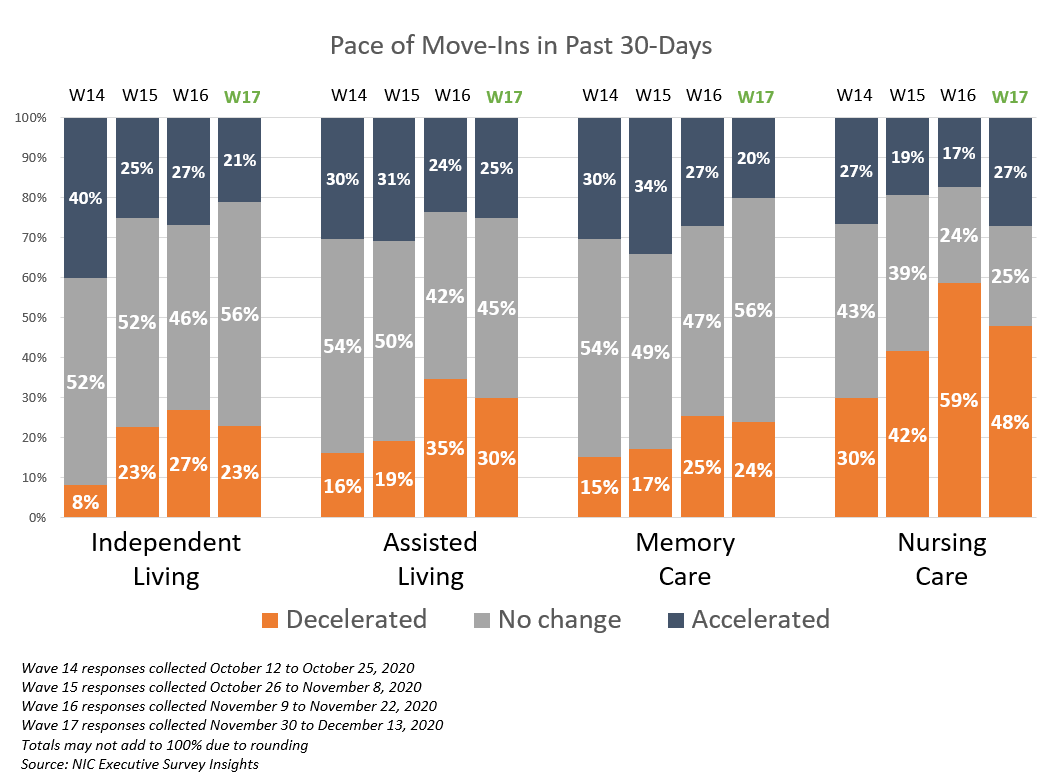

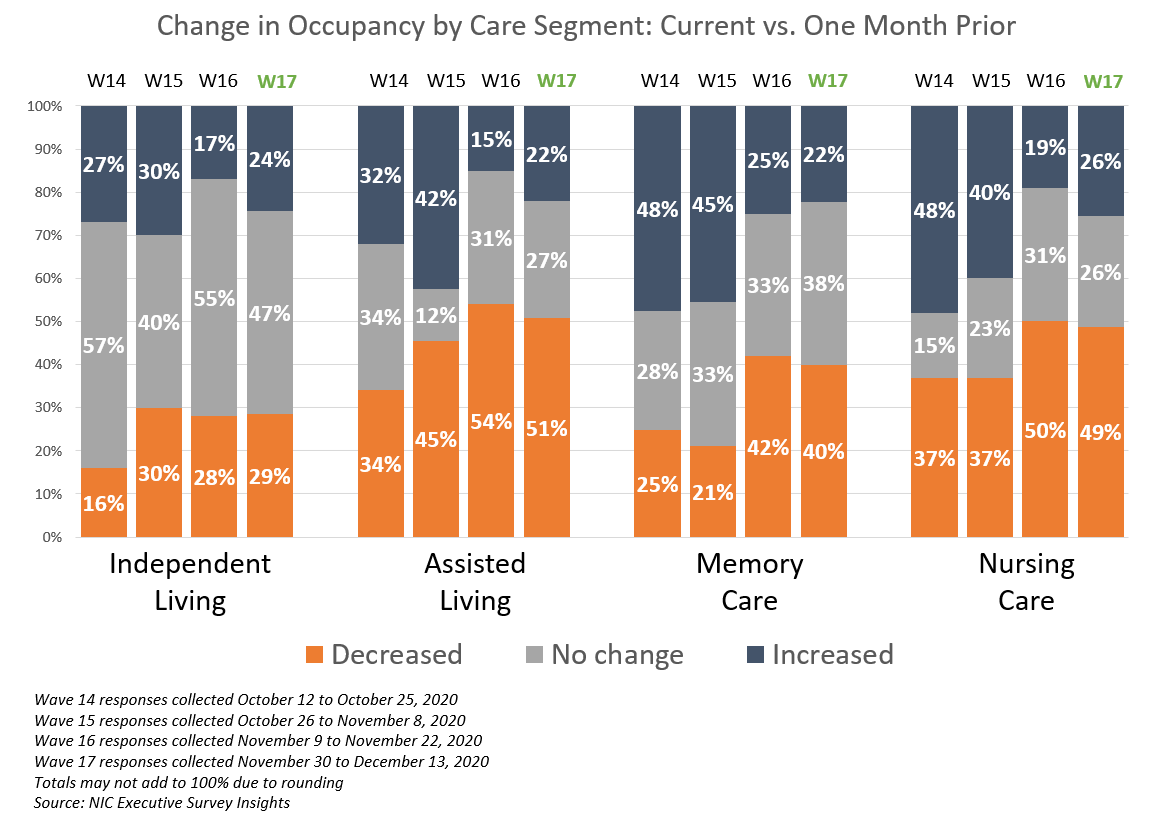

- In Wave 17, reports of decelerations in the pace of move-ins slightly outpaced accelerations within independent living, assisted living, and memory care, and continued to significantly outpace accelerations in move-ins in the nursing care segment since Wave 14 surveyed in mid-October. The shares of organizations reporting an acceleration in the pace of move-ins in the past 30-days for the independent living, assisted living, and memory care segments remained at or around their lowest levels since Wave 8 (surveyed late-May to early-June).

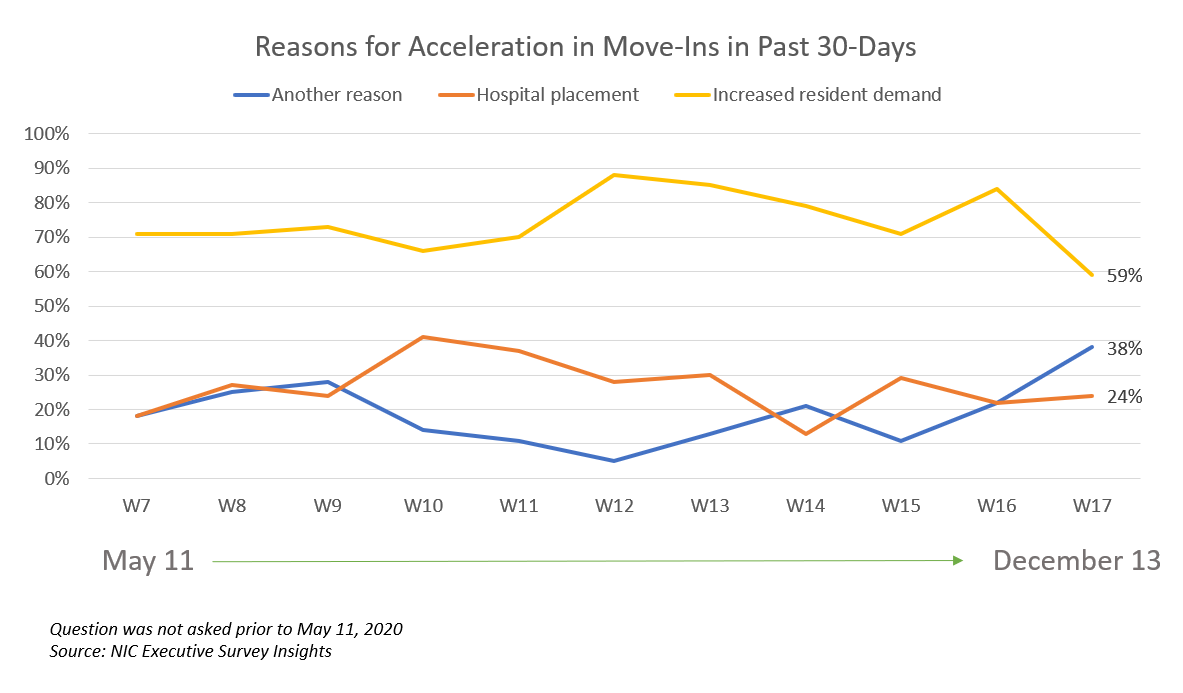

- The shares of organizations citing increased resident demand as a reason for acceleration in the pace of move-ins (59%) was at the lowest level in the survey time series, falling from a recent high of 84% in Wave 16. Hospital placement cited as a reason for acceleration in the pace of move-ins (24%) continued to lag the survey time series high of 41% reached in Wave 10, surveyed in late July. The percentage of respondents citing “another reason” for acceleration in the pace of move-ins has risen to 38%. Comments from respondents included reasons such as rent concessions and incentives, residents transferring from different levels of care, more needs-based admissions, and residents and families becoming comfortable with COVID-19 infection mitigation and visitation protocols.

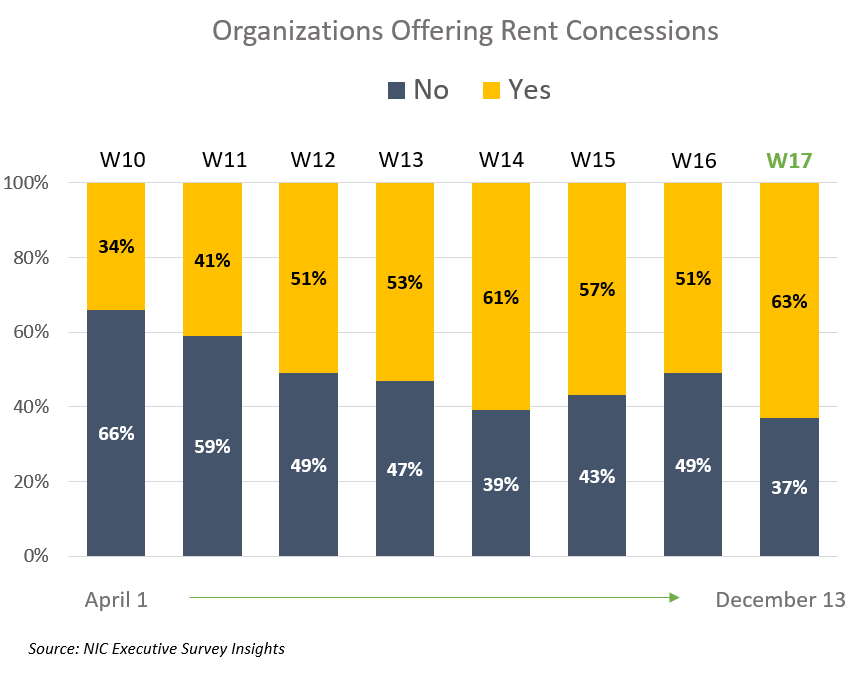

- NOI is continuing to be pressured as more organizations in the Wave 17 survey sample were offering rent concessions, paying staff overtime hours, and using agency or temp staff to backfill staffing shortages. Organizations offering rent concessions (63%) is up from 51% in Wave 16, and nine out of ten organizations (87%) were paying overtime wages. Staffing is a growing challenge. One survey respondent noted that with the surge of recent COVID-19 cases and the resulting second wave of infections, their organization is experiencing distress in finding labor at “double-time wages.” Others addressed the issue of financial tension in the context of occupancy challenges indicating that fewer move-ins coupled with attrition and transfers to higher levels of care is putting pressure on business operations.

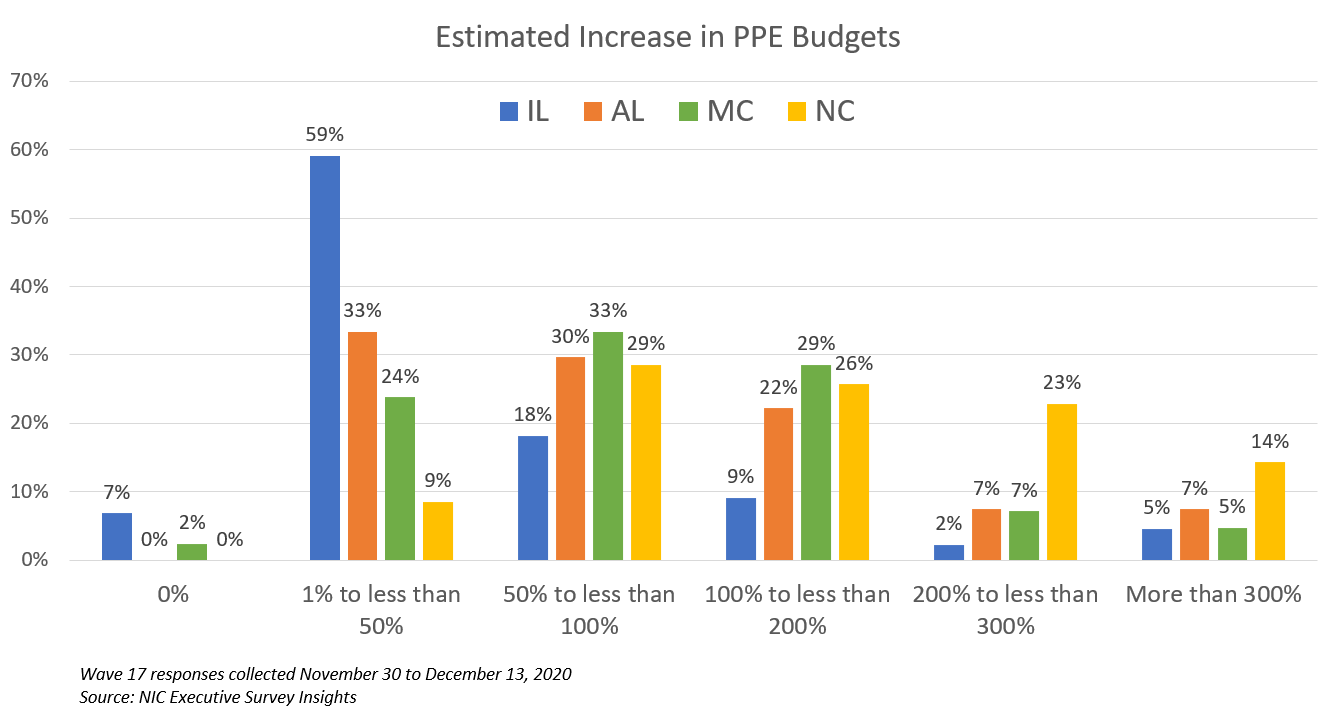

- About two-thirds of organizations (65%) noted they are experiencing challenges obtaining PPE due to high demand/competition (36%) and/or restrictions on allocation (29%). One-third (33%) reported budgetary constraints in paying for PPE.

- The higher-level care segments (assisted living, memory care and nursing care) reported increases in PPE budgets commensurate with growing levels of care. Additionally, organizations with the largest portfolios of properties were more likely to report significantly higher PPE budget increases than single-site operators.

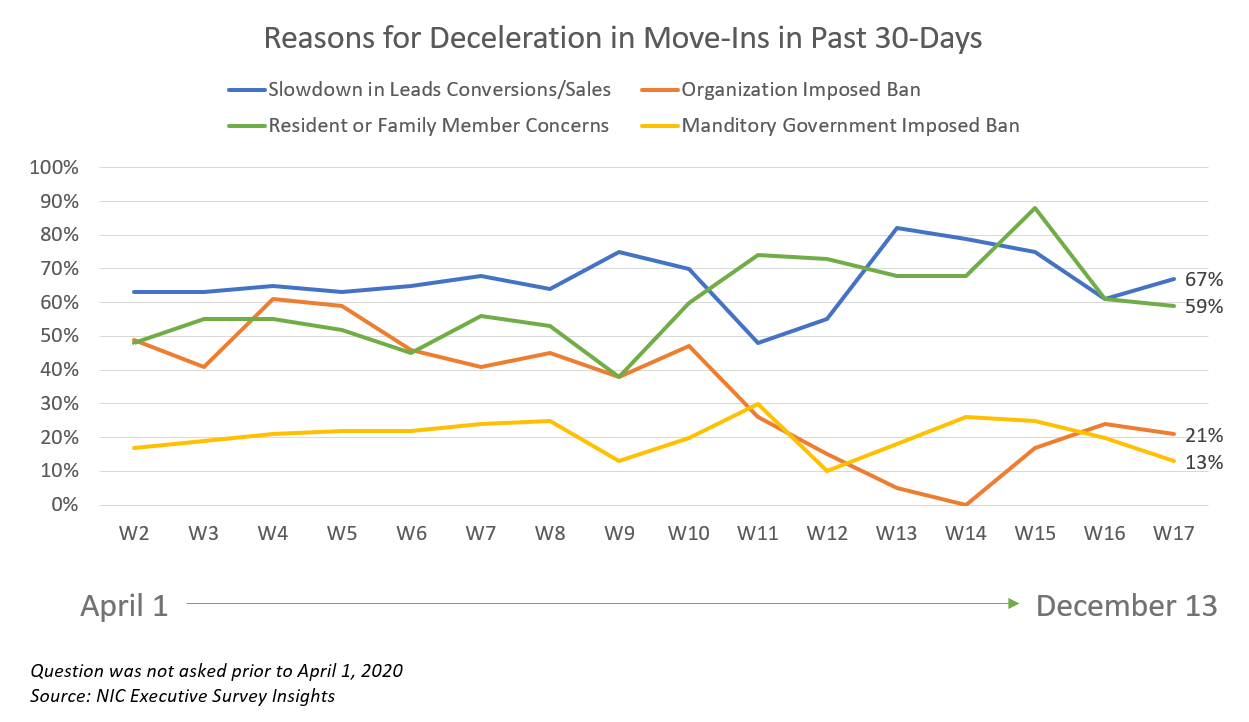

- Despite surging COVID-19 cases across the country, only about one in five organizations (21%) reported a self-imposed ban as a reason for deceleration in the pace of move-ins in Wave 17. At this point in the pandemic, two-thirds of organizations were neither increasing nor easing move-in restrictions in some or all geographies. The share of organizations increasing move-in restrictions in Wave 17 (22%) rose slightly since Wave 15 surveyed in late October (19%).

- Among reasons cited for deceleration in the pace of move-ins during the past 30 days, slowdown in leads conversions/sales and/or resident or family member concerns were either up or down slightly from Wave 16 (67% and 59%, respectively).

- Approximately one-quarter of respondents (26%) indicated that their organizations had a backlog of residents waiting to move-in. This is down from a high of 34% reached in Wave 16 and similar to levels last observed in Waves 12 through 15 surveyed mid-September to early November.

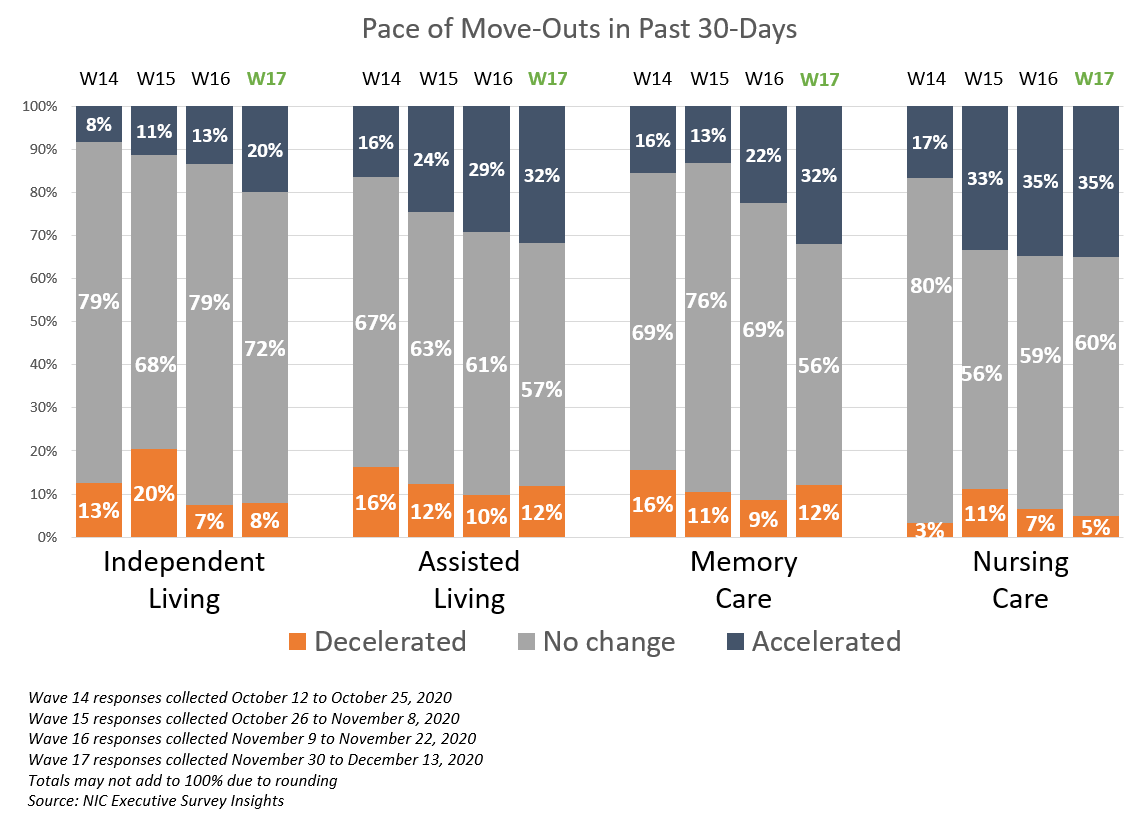

- A growing share of those organizations that responded to the Wave 17 survey reported an acceleration in the pace of move-outs for each of the care segments except nursing care—which remains at levels last seen in the surveys from the month of April (Waves 2-5). Notably, the shares of organizations with assisted living and/or memory care units reporting acceleration in the pace of move-outs during the past 30-days is at the highest levels reported in the survey time series (32%, respectively).

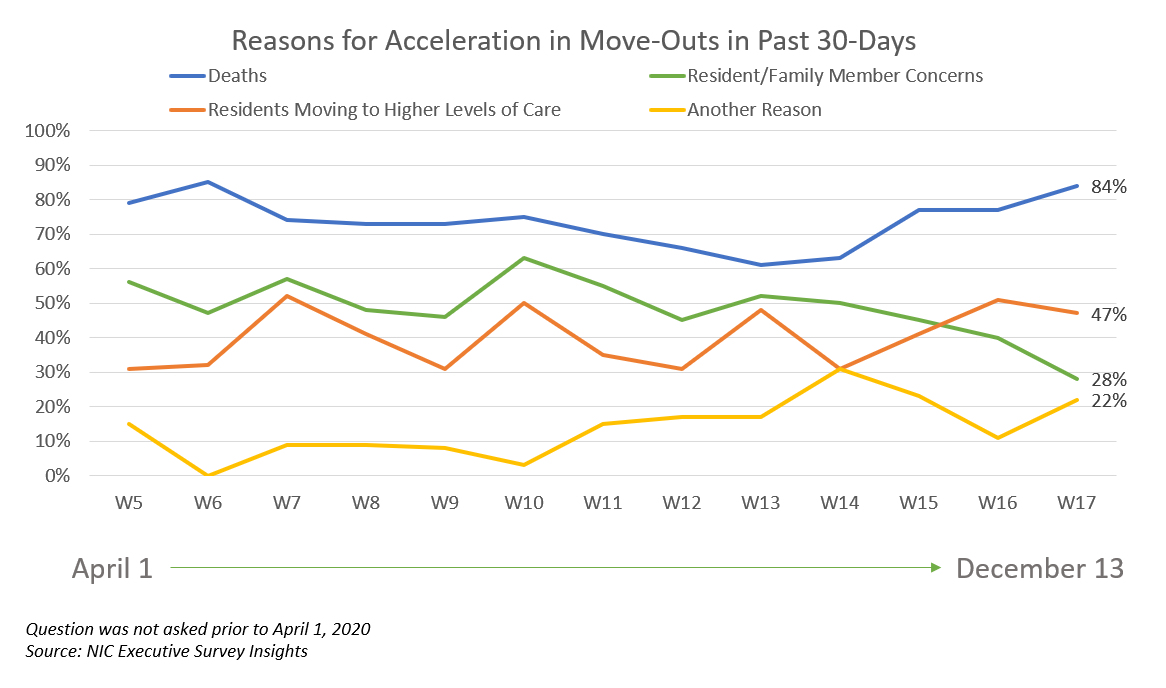

- As shown in the chart below, resident deaths (unspecified reason) continued to be cited most frequently as a reason for acceleration in the pace of move-outs in the last 30-days (84%). This is up from 61% in Wave 13 and similar to the peak of 85% reached in Wave 6 surveyed in early-May. Comments by respondents citing “another reason,” included COVID-19 (unspecified), COVID-19 deaths, and residents transferring to other levels of care.

- Presumably, as a result of better and safer visitation protocols and more acceptance, resident or family member concerns cited as a reason for acceleration in the pace of move-outs (28%) was down from 40% in Wave 16 and is at the lowest level in the survey time series.

- For each of the care segments, the shares of organizations reporting downward changes in occupancy in the past 30-days outpaced those reporting upward changes. One survey respondent mentioned that November was the first month in which their organization saw a net occupancy increase since February—but the last week of November and the first week of December also had the highest positive COVID-19 tests among residents and associates in their communities. Compared to Wave 16, the percentage of organizations reporting month-over-month declines in occupancy rates remained at similar levels. Between 40% and 51% of organizations with assisted living units, memory care units, and/or nursing care beds reported downward changes in occupancy during the past 30-days.

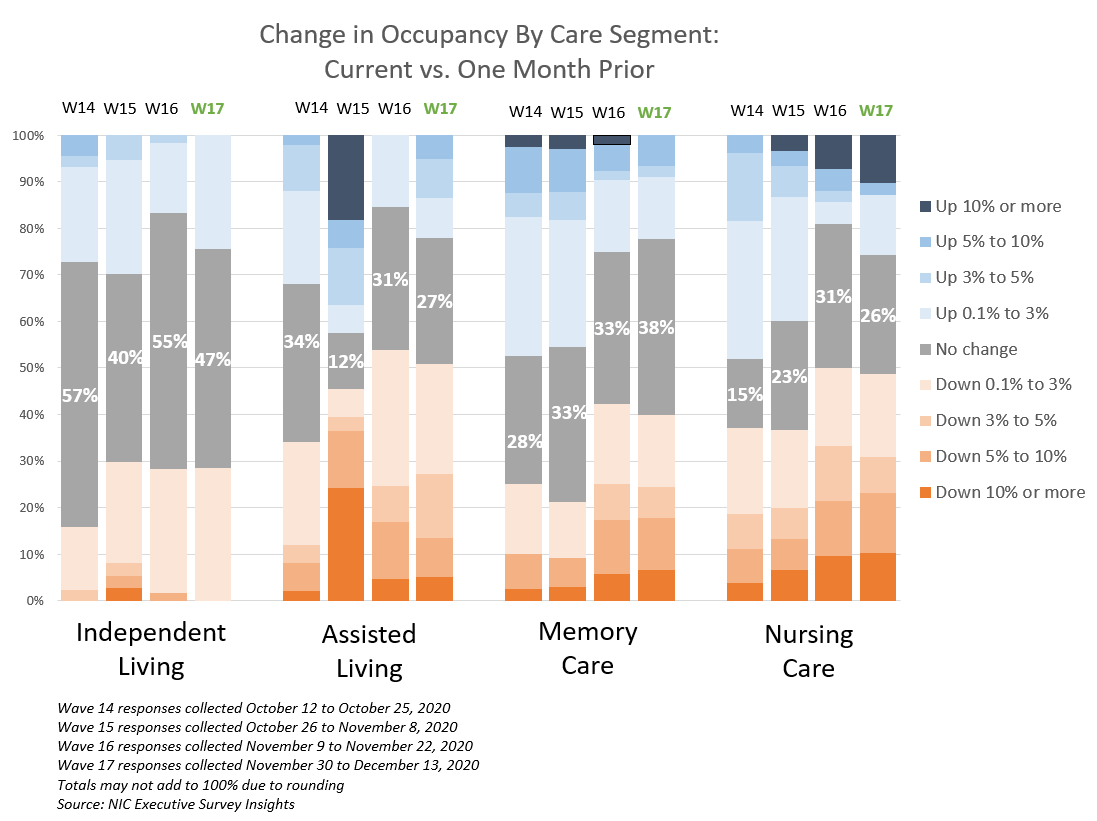

- The chart below illustrates that In Wave 17, 51% of operators with assisted living units noted declines in occupancy rates. The following chart describes the degree of those occupancy rate changes. The blue and orange-hued stacked bars correspond to the solid bars in the chart above indicating the degree of change by the saturation of color. For the assisted living care segment, one in four organizations (27%) reported occupancy drops of more than three percentage points, while another one in four (24%) reported occupancy declines between 0.1 and 3.0 percentage points.

- The independent living segment saw the least occupancy rate change: just under one-third (29%) reported a decline in occupancy of less than three percentage points, and one-quarter (24%) reported an increase of no more than three percentage points.

- The nursing care segment saw the largest (downward and upward) changes in occupancy rates—ten percentage points or more, respectively. One half (49%) reported a decline in occupancy in Wave 17.

- Consistent with the findings of the Wave 16 survey, organizations with nursing care and/or memory care segments reported more week-over-week occupancy declines than those organizations with other care segments (31% and 29%, respectively). However, nursing care also saw the highest week-over-week increase in occupancy rates in recent waves of the survey (28%).

- In Wave 17, one-half of respondents received their COVID-19 test results within two days, however it is taking three or more days to receive test results for the other half of respondents (48%). Although frustration with turnaround times was expressed in comments, with some fearing the impact of delays could result in difficulty mitigating infection control before effective isolation can be accomplished in light of the swell in coronavirus cases across the country, these findings were relatively unchanged since Wave 14 surveyed mid-October.

- Nearly nine out of ten respondents (87%) indicated their organizations have increased the use of telehealth/virtual appointments since the beginning of the pandemic.

Wave 17 Survey Demographics

- Responses were collected November 30 to December 13, 2020 from owners and executives of 80 seniors housing and skilled nursing operators from across the nation. Just under half of respondents are exclusively for-profit or nonprofit providers (46% and 44%, respectively), and 10% operate both for-profit and nonprofit seniors housing and care organizations.

- Owner/operators with 1 to 10 properties comprise 64% of the sample. Operators with 11 to 25 properties make up 20% of the sample, while operators with 26 properties or more make up 16% of the sample.

- Many respondents in the sample report operating combinations of property types. Across their entire portfolios of properties, 78% of the organizations operate seniors housing properties (IL, AL, MC), 35% operate nursing care properties, and 38% operate CCRCs (aka Life Plan Communities).

Owners and C-suite executives of seniors housing and care properties, we’re asking for your input! By providing real-time insights to the longest running pulse of the industry survey you can help ensure the narrative on the seniors housing and care sector is accurate. By demonstrating transparency, you can help build trust.

“…a closely watched Covid-19-related weekly survey of [ ] operators conducted by the National Investment Center for Seniors Housing & Care…”

Wall Street Journal | June 30, 2020

If you are an owner or C-suite executive of seniors housing and care and have not received an email invitation to take the survey, please click this link or send a message to insight@nic.org to be added to the email distribution list.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and transparency into market fundamentals in the seniors housing and care space at a time where trends are continuing to change.

Thoughts from NIC’s Chief Economist

By Beth Burnham Mace, Chief Economist

It’s with a collective sigh of relief that we have turned the calendar page on 2020 and gladly welcome 2021. And with it comes new hope as COVID-19 vaccines are beginning to be distributed, with residents and staff of senior living and nursing care properties among the first to receive the vaccines. The primary challenge will be the implementation and distribution of vaccines to residents and staff. While this is principally a logistics challenge, it will also be difficult to get full buy-in of all residents and staff to be inoculated.

It’s with a collective sigh of relief that we have turned the calendar page on 2020 and gladly welcome 2021. And with it comes new hope as COVID-19 vaccines are beginning to be distributed, with residents and staff of senior living and nursing care properties among the first to receive the vaccines. The primary challenge will be the implementation and distribution of vaccines to residents and staff. While this is principally a logistics challenge, it will also be difficult to get full buy-in of all residents and staff to be inoculated.

At some point, this will be behind us, thankfully. A huge amount of gratitude goes to those scientists that have worked to rapidly develop the vaccines in an unprecedented short time frame. And a huge amount of gratitude goes to those workers, health care professionals, and management teams on the front line of our properties who continue to care for our elders. The seniors housing and care industry is one that is based upon caring for seniors, and the physical and emotional toll of the pandemic has been and continues to be enormous. Every person has a story and a family behind them, many of whom many have incurred significant sacrifices and insufferable losses.

Bottom Lines Are Being Squeezed. In addition to the very real emotional toll on residents, staff, and family members, there’s been the financial impact to operators that has hurt their bottom lines as rising costs associated with staffing, PPE, and testing, and shrinking revenues, associated with weaker occupancy rates, have created a double negative financial shock wave. The uncertainty associated with these changes, along with the unknown timeline and endpoints, have resulted in many traditional capital providers pulling back from looking for new business, and instead focusing on helping their operator partners best address the pandemic.

That said, activity is starting to pick up, and the transactions market is beginning to re-awaken, with more deals being socialized and presented. Up until now, few sellers were willing to list their properties, because there was limited incentive to actively list properties for sale when a seller knew the pricing would be weak due to limited buyer interest. As a result, the bid/ask spreads have been wide, and transaction volumes have been low. Real Capital Analytics (RCA) reports that seniors housing sales volumes totaled $1.1 billion in the third quarter, 69% below year-earlier levels. Notably, only 2% of these sales were classified as distress—good news, at least thus far into this real estate cycle, and a significantly smaller share than for the retail or hospitality sectors.

And What’s Ahead?

The impact of the coronavirus on the seniors housing industry has been significant and will be long lasting. The pandemic accelerated a trend NIC has been focusing on for years, including at the educational sessions at our conferences—the intersection of healthcare and housing for older Americans. When appropriate, bringing healthcare to seniors instead of bringing seniors to healthcare is an advantage for seniors, health insurers, and operators. The ability to explain to potential residents and their adult children how healthcare is provided within a community will be a competitive advantage.

Additionally, technology adoption within senior living has taken a huge leap forward, largely out of necessity. Telehealth is one example. Social connectivity with family and other residents without interfering with social distancing protocols is another example. While technology doesn’t replace face-to-face experiences, it can support social well-being. Many of these technology-related experiences will remain even after the pandemic is over.

Infection control will likely remain top of mind for both potential residents and their decision-influencing adult children. A recent American Seniors Housing Association (ASHA) survey indicates that infection control mitigation efforts need to be both obvious and effective. Unfortunately, there will be other contagious viruses, and there’s an opportunity now to have seniors housing and skilled nursing be appreciated and recognized as a safe space for older adults.

Finally, the messaging about the benefits of living in seniors housing needs to better articulated, boldly stated, and widely marketed. Negative press headlines in the past nine months about the impact of the pandemic in congregate settings have been and will continue to be a challenge in 2021. The impact of COVID-19 has been different for nursing care operators than for operators of independent living, for instance, and this difference needs to be highlighted. NIC has funded via a grant the first phase of a study by NORC at the University of Chicago that is examining the facts on the incidence and fatality rate of the coronavirus by care setting in the context of what was known about the virus at the time. The second phase of the study will compare that experience to that of a similarly frail population in the general public. The study’s first phase results will be available in Spring 2021.

Also, the value proposition of seniors housing remains intact. The bottom line is that seniors housing offers its residents socialization and hospitality, healthcare support and medical care plan adherence, educational experiences, nutrition and exercise opportunities, safety, and generally a healthy, nurturing, and engaging lifestyle. It supports a sense of purpose and provides a community in which to age while thriving. Taken in its entirety, the future of seniors housing is bright and will continue to serve seniors as it provides care, housing, and socialization.

Lastly, as always, I appreciate and welcome your comments, thoughts, and feedback. And of course, Happy New Year to each of you!

“Future Consumers Won’t Buy What We’re Selling” 2020 NIC Talks, Part Two

The 2020 NIC Fall Conference featured much of the content that attendees have come to expect and value over the years, despite being delivered for the first time on a virtual platform. NIC Talks, which are modeled on TED-x-style presentations, continued a tradition of delivering brief but powerful thought-leadership from beyond the seniors housing and care sector. This brief review of the second day of presentations follows last month’s NIC Insider article “’It Is Not Perfect… But We Are Not Going Back’ – 2020 NIC Talks, Part One,” which covered Day One. All NIC Talks, from this and prior years, can be viewed on NIC’s YouTube channel.

Day Two was no less impactful and relevant for industry leaders considering strategies to move forward and plan for a post-COVID-19 ‘new normal.’ In his opening remarks, NIC Co-Founder and Strategic Advisor Bob Kramer reminded attendees of the importance of innovative thinking and fresh perspectives, during a time of rapid industry disruption. He said, “We started NIC Talks, in our 2015 Fall Conference, as a way to stimulate conversation, innovation, and future thinking for NIC participants, as we know our industry is facing major changes, with the coming of the baby boomers. And with COVID-19 hitting our industry incredibly hard, this year it’s more important than ever to be thinking about how to deal with disruption amidst what could be the creative destruction of some traditional operating models in seniors housing and care.”

Dr. Louise Aronson, Professor, UCSF Division of Geriatrics, and New York Times bestselling author of Elderhood: Redefining Aging, Transforming Medicine, Reimagining Life, kicked off the schedule with a talk titled “Ageism and COVID-19: Opportunities to Create a Better Future.” Of her title, Aronson quipped, “You might have noticed from my title that it has two bummers in it: ageism and COVID. What I’m hoping to do in this next little bit is convince you that both of those and, in fact, the two together offer an opportunity.”

Aronson discussed how outdated views of aging, and widespread misunderstanding of seniors’ housing and care options, are impacting not only the quality of life of seniors, but the potential for success in the seniors housing and care industry. When it comes to the realities of aging and seniors housing, the public is poorly informed. Aronson said, “Many people believe that all seniors housing is nursing homes. They have no idea of all the different things that are available.” This and other misinformation, exacerbated by largely negative media coverage through the COVID-19 pandemic, contributes to ageism. “The nursing home coverage in the popular press reinforced those notions of old as singularly frail,” observed Aronson. Combined with shifting consumer demands, largely driven by baby boomers, ageism, and ignorance is presenting a growing challenge to industry leaders, particularly when the public is asked to make sacrifices or accommodations for older Americans.

The opportunity, according to Aronson, is to rethink what the industry offers in the future, while becoming better advocates for seniors. “If we all start thinking about what we’d like to see, and working towards it, we’re more likely to have an industry that does well for everyone; for residents, for staff, for families, for owners, for everyone.” She advocates for several changes, beginning with combating ageism and misinformation on aging. Instead of isolating residents, Aronson believes society should prioritize high-risk elders for PPE and testing. To achieve this, she observes, seniors housing settings must become part of a continuum of care, partnering with the healthcare system.

Aronson closed her talk with specific suggestions for the industry. Pointing to what she sees as a loss of physicians’ control in the healthcare industry, and resulting declines in quality of outcomes and satisfaction, Aronson warned the seniors housing industry to police itself, saying, “If you don’t control your industry, other people will.”

She also pointed to major advances in technology as an area of opportunity, suggesting partnerships with “elder-friendly tech” companies, as they test new software and devices. She said, “you get the stuff for free, they get to try out their tech. It’s a win-win.” Aronson discussed the potential for the industry to create smaller, more “family-like” units, in which people can cohort, retaining safety protocols while remaining socially connected. Finally, she asked attendees whether they’d want to move into their properties, saying, “Now is your opportunity to make the changes, to create the future in which you hope to live in terms of both ageism and seniors housing.”

Dan Cinelli, Principal, Perkins Eastman, brought the perspective of a leading seniors housing architect to the table. Like Aronson, he pointed out that, in addition to major disruptive influences such as COVID-19, the baby boomers will continue to drive change in the industry. He asked, “Will your current real estate products continue to be marketable for the future boomer consumer? I’m here to inform you that the majority of those future consumers won’t buy what we’re selling.”

Cinelli explained that his company had been studying predictive trends, in an effort to understand what boomers will want from the seniors housing industry beginning in 2023. Cinelli presented three scenarios based on this data.

The first scenario, “vertical main street,” envisions the conversion of under-utilized retail town centers and shopping malls into the most age-friendly, walkable communities in America. He envisions partnerships in which, “You could build a new mid-rise residential building inserted into the closed Lord & Taylor footprint, which is surrounded by a variety of community amenities.” The space could host rent-by-day co-working offices, maker spaces, a post office, a public library, and, he suggested, a teaching kitchen/restaurant. The kitchen, pharmacy, outpatient clinic, pop-up surgery center, and other amenities might be developed in partnership with a local technical or medical college. In the end, Cinelli’s vision is of an intersection of seniors housing and the broader community, “a place for all members of the community to gather together.”

Termed, “life pod homes,” the second scenario would enable aging boomers to install a high-tech dwelling unit on their existing property. Each unit comes with a membership to the nearby converted mall, which is now an age-friendly community, offering services such as a driverless car service, which enable even dementia patients to stay in their homes longer. Once in need of more care, these residents will be likely to move to the community they’ve been enjoying and are already familiar with.

Cinelli called his final scenario, “new applications for empowering the new consumer.” While not a brick-and-mortar idea, the concept is to connect with seniors far earlier than they would typically begin to look at seniors housing and care options. Cinelli imagines an online presence that attracts entrepreneurial “thriver” boomers and connects them to advances and innovations within local communities. By offering a chance to test, evaluate, and provide feedback on new products and services, “Your imminent boomer consumer links to your senior living brand, as a visionary business, 15-20 years before they show up on your assisted living doorstep.”

Linking seniors, via web-based applications, to a variety of senior living entities, seniors would be able to connect to other like-minded consumers. Cinelli termed this idea, “bed, match, and beyond,” saying it would enable older adults to connect with each other. Users would explore real estate options, eventually creating intentional communities. It could become, as Cinelli imagines, “your new main marketing tool.”

In his introduction of Jo Ann Jenkins, the CEO of AARP, Bob Kramer made it clear that she would likely be in agreement with Cinelli and Aronson regarding the importance of redefining how society views aging. Kramer referred to Jenkins’ best-selling book, Disrupt Aging: A Bold New Path to Living Your Best Life at Every Age, as a “rallying cry for revolutionizing society’s views on aging.” He explained that he’d asked Jenkins to focus in particular on the changing needs, wants, and expectations of the boomer consumer.

Saying, “People today don’t want to age the same way their parents did. They want new and better solutions to help them age with independence, dignity, and purpose,” Jenkins reinforced the argument that boomers in particular will indeed expect new models from the seniors housing and care sector. She also made the point that seniors spend far more on housing than they do on healthcare. She said, “All of this points to the need for innovation in both housing and long-term care, that puts housing and health together to support quality of life.”

Jenkins pointed to the need for new, age-appropriate housing models, saying, “The simple fact is that a vast majority of the US population does not live in or have access to housing that will meet their needs as they age. There are two primary reasons for this: good, age-friendly housing options are beyond many people’s financial means, and the design of most housing has never really taken into consideration what most people need and want.”

Jenkins argued that the market is shifting towards more affordable options. Referring to NIC’s recent middle market “Forgotten Middle” study, which AARP helped sponsor, Jenkins pointed to the growing need to lower seniors housing costs, saying, “The challenge is to come up with creative solutions that reduce the cost of housing while supporting engagement and the long-term well-being of people of all income levels, not just the wealthy.”

Another challenge which Jenkins addressed is poor public perception of the industry. “When people think of your industry, they think immediately of nursing homes and frail elderly. They don’t think of seniors housing as a place where people can come and become less isolated, make new friends, continue to grow and thrive, while having many of their needs met. In other words, they don’t see the total breadth of your industry and the choices you make available. And this challenge has only become more difficult as a result of COVID-19.”

To meet this and other challenges, Jenkins encouraged industry leaders to take a fresh look at their models and develop what boomers of all income levels will want and be able to afford. Referring to AARP’s own struggles to change public perceptions on its value proposition and brand, Jenkins said, “How do you gain people’s trust and win them back? How do you connect with consumers long before they ever think about moving into one of your communities? You do it by providing housing that people actually want and can afford. You do it by providing not just a home but a community where people can choose to lead as full lives as possible, regardless of their health or condition.”

A library of all NIC Talks presentations, including those from previous years, can be accessed on NIC’s YouTube Channel.

FLC Alumni Spotlight: A Chat with FLC Oversight Committee Member, Lawrence “Lory” Brin, Head of Healthcare Real Estate, MidCap Financial

Current NIC Future Leaders Council (FLC) member and Vice Chair, Kari Onweller, caught up with Lory Brin to hear about his career in the seniors housing and care industry, MidCap’s current portfolio and future outlook, and some fun reminiscing on his time as a member of the FLC. A recap of the conversation is below.

Current NIC Future Leaders Council (FLC) member and Vice Chair, Kari Onweller, caught up with Lory Brin to hear about his career in the seniors housing and care industry, MidCap’s current portfolio and future outlook, and some fun reminiscing on his time as a member of the FLC. A recap of the conversation is below.

Onweller: Can you tell me a little bit about yourself, your background, how you ended up at MidCap and your promotion to become the Head of Healthcare Finance in early 2019?

Brin: I began my career as an attorney in New York focused on corporate finance and M&A. Practicing law at a Wall Street firm was a fantastic formative experience that provided tremendous exposure to the transactional world. I interacted with very smart and driven individuals and worked on deals related to Fortune 500 companies. I learned through my experience at the firm that I found it more fulfilling to work on projects related to something tangible (like purchasing a fleet of aircraft) than something abstract (like a corporate bond offering). I also developed a preference for working on transactions in a broader capacity in which I could use a variety of skill sets and shepherd a process from start to completion.

After a few years, my wife and I moved to DC to be closer to family. At that time, I transitioned from law into a business role. I found that real estate finance was a great intersection where I could capitalize on my expertise as a corporate attorney and exercise a broader skill set in the context of something I could actually see in person. In 2007, I had the great fortune to join the healthcare real estate team of Merrill Lynch Capital. Kevin McMeen led the real estate business for that platform, and he and the senior management team cultivated an excellent business coupled with extraordinary culture. It is one of the fortuitous circumstances of my career that I ended up in the healthcare real estate space.

In 2008, the senior management team of Merrill Lynch Capital’s healthcare group, including Kevin, started MidCap Financial, and I was fortunate to be one of the thirty founding members of that platform. It was an incredible experience to help scale MidCap from a start-up company to the largest specialty finance company focused on healthcare. At the end of 2013, MidCap’s original equity investors had a successful exit from their investment, and MidCap became an affiliate of Apollo Global Management. The affiliation with Apollo enabled MidCap to raise substantial equity for our balance sheet and broaden our product offerings outside the healthcare sector. In the spirit of expanding our market, I spearheaded our medical office lending business, while maintaining my presence in the seniors housing and long-term care sectors.

By 2019, our real estate business had evolved sufficiently that our non-healthcare commercial real estate activity was as active as our healthcare real estate activity. Moreover, we were pursuing more business opportunities attributable to our relationship with Apollo. Those factors, combined with my experience on both the credit and business development sides of our business, created an opportunity for me to assume more leadership over the healthcare real estate platform. I also benefited greatly from the support provided to me by Kevin McMeen and Steve Curwin (MidCap’s CEO) for the opportunity for continued professional growth.

Onweller: Can you highlight the different debt offerings that MidCap provides and your current portfolio make-up?

Brin: MidCap is a diversified middle market specialty finance company with over $27 billion of commitments. We have six business lines: leveraged finance and financial sponsors; asset-based lending; real estate lending; life sciences and technology lending; lender finance; and franchise finance.

Our real estate lending business focuses on bridge lending to transitional properties and other scenarios for which conventional capital is suboptimal. We also have an active HUD business that provides permanent financing for transactions that we have financed on a bridge basis, as well as other properties on a direct basis.

Our core offering in our healthcare real estate balance sheet business is a two-to-five-year floating rate product that is generally presented on a nonrecourse basis. As an unregulated lender with deep sector expertise, we have the latitude to approach deals differently and to structure creatively. What makes our real estate business unique, especially relative to other nonbank lenders, is that we hold all of our real estate deals on balance sheet and service all of our deals in house. Many of our non-bank competitors are debt funds who raise pools of capital for their loans and eventually sell those loans in collateralized loan obligation (CLO) securitizations. By contrast, our strategy enables MidCap to exercise control over our loans, which leads to better execution with respect to unfunded commitments (such as draws for capital expenditures or interest shortfalls) and more constructive flexibility for when performance deviates from underwriting.

Onweller: What growth plans does MidCap have currently, and how has the short-term and/or long-term outlook on the industry changed as a result of the COVID-19 pandemic over the last nine months?

Brin: In the wake of the dislocation caused by the COVID pandemic, MidCap’s healthcare real estate business is well situated to add value in the seniors housing capital markets. Our deep expertise in the sector combined with our capital structure enables us to approach transactions creatively and tailor structure in a bespoke manner. We expect the next 12 to 24 months to be turbulent, and there will be many strong operators and communities that will need capital solutions to enable them to navigate through the disruption. There will also be compelling acquisition opportunities that will be best complimented by flexible capital that understands the investment thesis.

MidCap has weathered the fallout from COVID well. Our portfolio has shown strong resilience, and our business has significant liquidity. Our healthcare real estate business has been quite active since the summer. Relative to the past few years, we are seeing opportunities with more institutional caliber equity sponsors and more moderate leverage requests. We understand that the COVID pandemic has uniquely affected the long-term care sectors but believe that the future of seniors housing is bright. We are focused upon the importance of maintaining alignment with investors and operators, and ensuring projects are sufficiently capitalized to weather potential disruptions. Sophisticated investors and operators seem to be adopting the same perspective. We anticipate a very robust amount of activity in the coming year.

Onweller: What do you think are the biggest opportunities and challenges for the seniors housing industry as we head into 2021?

Brin: There is the obvious fallout from the COVID pandemic, which has materially affected seniors housing and long-term care. It has caused dislocation in the assets themselves as well as the related capital markets. It has also led to a reassessment of the operating model for seniors housing, forcing market participants to reconsider where the asset class stands relative to its focus on healthcare, on the one hand, and lifestyle on the other.

In addition to COVID, the sector was already struggling with how to absorb the significant amount of new development that delivered in the past five years. Moreover, seniors housing has seen a recent realignment of care types, with new concepts such as active adult entering the landscape. There is a looming issue of affordability for a large portion of the market that the industry needs to solve in the coming years. And there are exogenous players such as managed care providers that will affect the future of seniors housing. Finally, and not least significantly, the sector is finally getting close to the time when the baby boomer generation will begin to utilize seniors housing, which will require a rethinking of the product offerings to account for their preferences.

Given the broad reset that the market is experiencing, there are significant opportunities and challenges for the sector. One thing that seems clear is that the industry will not simply revert to the way things were a year or two ago.

Onweller: Turning to a little bit more of a fun topic, especially for me as someone currently on the FLC, when were you part of the FLC, and do you have any favorite memories of your time on the FLC that you would be willing to share?

Brin: I was on the FLC from 2011 to 2014, which I believe was the third FLC class.

I have a number of fond memories from my time as a member of FLC. A few things that stand out for me are each of the semiannual retreats I attended; serving on the planning committee for the NIC Spring Conference; planning and moderating a panel at that Spring Conference; and all of the various dinners and cocktail events I attended with my FLC colleagues during my term.

The semiannual retreats in particular were amazing opportunities to spend a concentrated amount of time with other FLC members as well as NIC leaders. They afforded a forum for individuals to discuss pressing issues in seniors housing and long-term care from the perspectives of the various stakeholders in the industry—operators, investors, balance sheet lenders, advisors, GSEs, and service providers. They were also a lot of fun. My class got to spend a day at Churchill Downs in Louisville and a few days at an outdoor retreat in Georgia where we even got to try some skeet shooting.

I remember when I began my FLC term, we had a joint session with the outgoing class of FLC members, which happened to be the inaugural group. I recall distinctly that many of those members advised us that as a member of FLC, you essentially get out of the experience what you put into it. I think that advice was spot on—members who proactively engage have the best experience. Members who attend the regional meetings, actively participate in their projects, and avail themselves of the networking opportunities find that the FLC can be a watershed experience in their careers. I attribute a significant amount of my understanding of NIC, visibility in the seniors housing industry, and business network to the time I was fortunate to be a member of the FLC, and to my continuing involvement in FLC initiatives following that time. It is very gratifying for me to now be a member of the FLC Oversight Committee.

Onweller: What advice do you have for someone that may be new to the seniors housing and care industry and is looking to embark on a long-term career within the space?

Brin: It is an exciting time to enter the space, which is now at a moment of inflection for all the reasons I outlined previously. The current dislocation in the market and coupled with the challenges it needs to address in the future, creates an environment ripe with opportunity.

My advice would be to learn about the various players in the ecosystem and how they interact with one another. While seniors housing has evolved meaningfully during the past twenty years, it is still a relatively small sector that is approachable. Cultivating relationships with other industry participants is important. NIC, ASHA, Argentum and other similar trade groups offer excellent opportunities to meet peers in the sector. Seniors housing is also a property type that demands substantive expertise regarding the operating model. There are several industry periodicals and virtual webinars today which provide good insight into various facets of seniors housing. Finally, maintain perspective regarding the fundamental issues regarding public health, housing, and social wellness that seniors housing will affect in the coming decades.