Seniors Housing Occupancy Stable, While Demand for Independent Living Grows at a Rapid Rate

The Five Takeaways from NIC’s Third-Quarter Seniors Housing Data Release

NIC MAP® Data Service clients attended a webinar earlier this month on the key seniors housing data trends during the third quarter of 2016. Five key takeaways emerged:

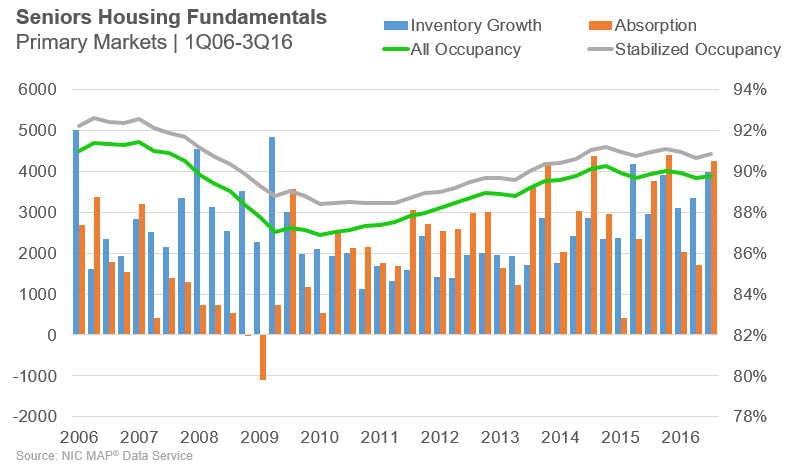

- Third-quarter occupancy equaled its three-year average rate of 89.8%, around which seniors housing occupancy has oscillated since 2013.

- Independent living occupancy reached a near seven-year high given record absorption amid strong inventory growth.

- Assisted living construction starts increased after having slowed during the first half of the year.

- Seniors housing annual rent growth was its highest since 2007.

- Finally, property sales transaction volumes continued to slow. (See the transactions article of this edition of the Insider for more information on transaction volume in the third quarter.)

Let’s take a closer look at some of these trends.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Occupancy Rates Oscillating

The all occupancy rate for seniors housing, which includes properties still in lease up, was 89.8% in the third quarter. This was equivalent to the average occupancy rate for the past three years. It was 290 basis points above its cyclical low of 86.9% during the first quarter of 2010 and 50 basis points below its most recent high of 90.3% in the fourth quarter of 2014.

Occupancy rose 10 basis points from the second quarter, as the pace of absorption picked up after a weak first half of the year. Inventory continued to expand as well, but at a lesser pace than absorption during the quarter. For the past year, inventory has increased on average by roughly 3,600 units per quarter.

By property type, it was a very active quarter for independent living. Nearly 2,500 units were absorbed on a net basis, the most in a single quarter since NIC’s data collection began in 2006. Inventory grew at a lesser 2,158 units and below the record pace of 3,268 units in early 2008. As a result, occupancy improved to 91.1%, up 0.2 percentage point from the prior quarter. Occupancy for independent living was unchanged from year-earlier levels and down 0.1 percentage point from its seven-year high of 91.2% in the fourth quarter of 2015.

For assisted living, inventory growth exceeded absorption for the fourth consecutive quarter. Occupancy remained stable at 88.0%, but was down 20 basis points from year-earlier levels.

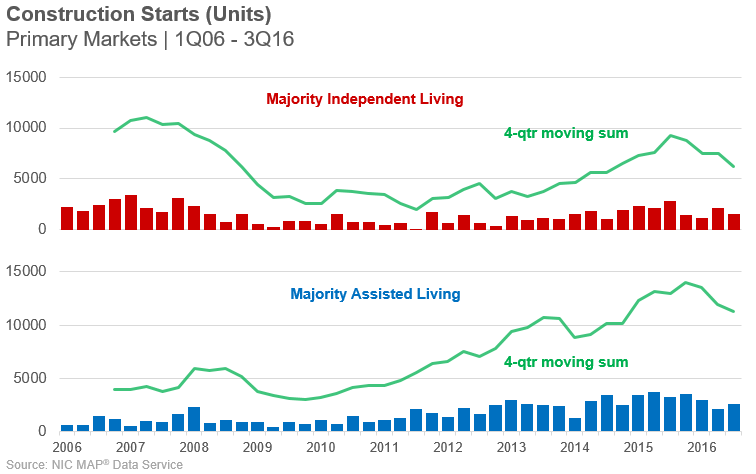

Construction Starts Slowing

Construction starts are a good indicator of future inventory growth, and generally a start converts into a completed unit within six to eight quarters. On a four-quarter aggregate basis, the pace of independent living starts was the weakest since late 2014. By this measure, starts of assisted living units also slowed. On a quarter-to-quarter basis, starts for assisted living edged higher in the third quarter, after three consecutive quarters of slowing activity.

Starts may be slowing due to well-publicized concerns about oversupply in a limited number of markets. Additionally, slower starts activity may be tied to tightening credit for development activity. Anecdotally, NIC’s data collection team has observed that a number of projects in planning stages have been on hold due to lack of funding. Some projects have changed ownership. Sometimes, when projects change ownership, we see plans and delivery dates altered or projects delayed because paperwork was not submitted correctly or planning boards did not grant certain permissions. Recently one community pulled the plug on a new property after discovering there was another property scheduled to break ground in the third quarter very near the site of the first.

Starts data also are often reported by the developers with a lag, so revisions are not unusual. For the four quarters ending in the second quarter, assisted living starts were initially reported at 7,009 units as of June. Data revisions now show that assisted living starts tallied in at 7,525 units, a difference of 516 units or 7% more than initially estimated. For independent living starts, this figure is 929 units or 8%. There were a total of 11,942 starts for independent living units for the year ending in June.

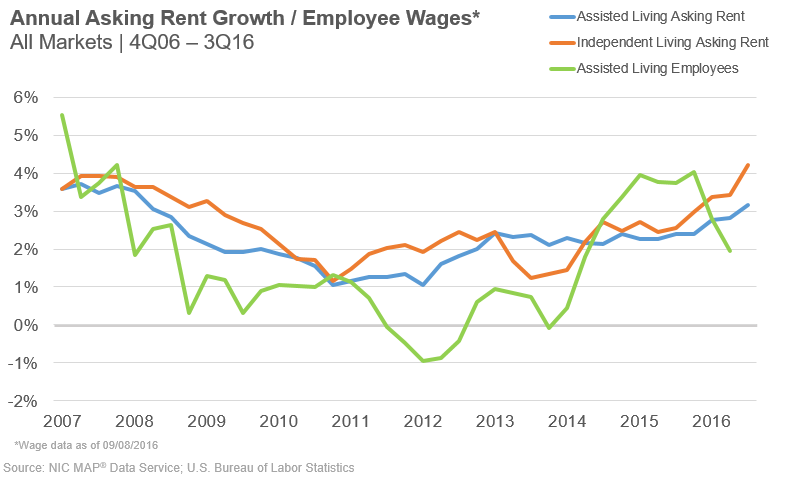

Asking Rent Growth Strong

At 3.8%, annual asking rent growth for seniors housing accelerated to its highest level since 2007. Asking rent growth for assisted living (blue line) was 3.2% for the third quarter and, for independent living (orange line), it was 4.2%. There is wide variation in rent growth, however, with San Diego and San Antonio experiencing gains of 1.2% in seniors housing asking rents from year-earlier levels, while San Francisco and San Jose saw gains of more than 6%.

Looking Ahead

Over the next 12 months, NIC expects the occupancy rate for assisted living properties to stay close to today’s levels of 88.0%. Since late 2010, occupancy has stayed in the range of 87.5% to 89%, and our expectation is that this will remain the case for the next four quarters. For independent living properties, occupancy is also projected to remain fairly flat near its 91%, as demand and supply largely match each other.

[/expand] [cresta-social-share]

Property Sales Transactions and Pricing Decline

What the Third-Quarter Data Reveals about Transaction Volume

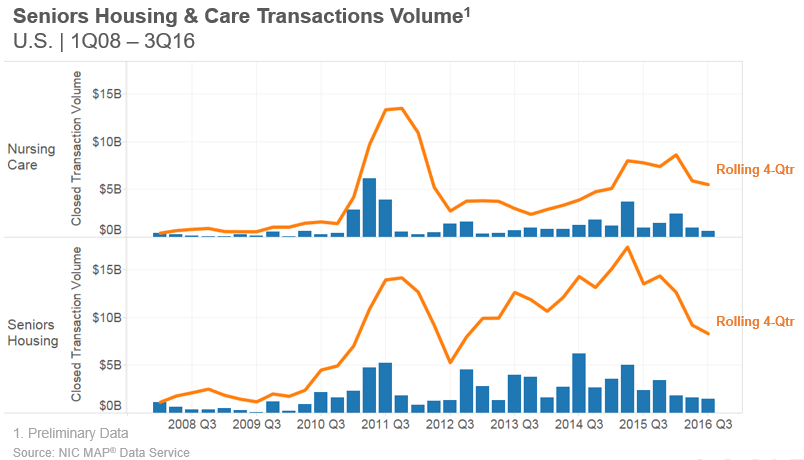

There has been much discussion about the current seniors housing and care transactions market. Both dollar volume and the number of deals that were closed decreased significantly over the past two quarters, and NIC’s preliminary look at third-quarter 2016 data shows a continuation of the slowdown in deals.

But the picture isn’t entirely dim. While it’s true that public buyers (public REITs especially) have slowed down because their cost of capital increased and they’re finding fewer deals to suit their strategies, the private buyers, represented by private REITs and private owners/partnerships, have continued to stay relatively active.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

The Third-Quarter Data

Transaction volume for seniors housing and care in the third quarter registered $2.0 billion, which is the lowest since the second quarter of 2013. The current $2 billion included $1.4 billion in seniors housing and $600 million in nursing care. The total volume was down 21% from the previous quarter’s $2.6 billion and down 39% from the third quarter of 2015, when volume came in at $3.4 billion.

The third quarter marked the fifth quarter in a row with less than $5 billion in total volume, a trend we haven’t seen since 2013, when the cost of capital increased significantly for the public REITs, who have been the primary drivers of large transaction volumes throughout this current cycle. At the start of the third quarter, public REITs’ cost of capital improved, but toward the end of the quarter and continuing into the start of the fourth quarter, their cost of capital increased again as interest rates rose. Most likely, the Welltower announcement of the $1.15 billion deal with Vintage Senior Living took advantage of lower costs of capital at the start of the third quarter.

The rolling four-quarter total volume for seniors housing and care was down 9% from the prior quarter, from $15.1 billion to the present $13.8 billion.

Digging deeper, we see that the volume was down in both nursing care and seniors housing. Nursing care volume was down 40% compared to the prior quarter (from $1 billion to $600 million) and seniors housing was down 9% (from $1.6 billion to $1.4 billion). Compared to the third quarter of 2015, nursing care volume was down 39% and seniors housing was down 38%.

The rolling four-quarter volume in nursing care decreased from $5.9 billion to $5.5 billion, and seniors housing decreased from $9.2 billion to $8.3 billion.

To put these figures in context, last year in the third quarter, the rolling four-quarter volume was $7.8 billion for nursing care and $13.5 billion for seniors housing. In short, this year’s activity is noticeably down.

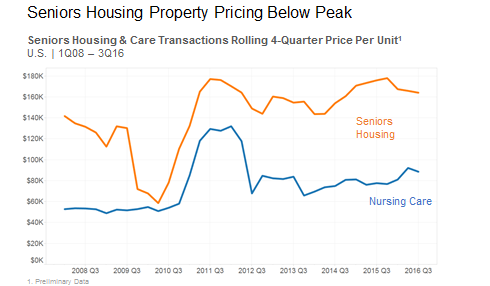

Seniors Housing and Nursing Care Price Per Unit Down

The price per unit for seniors housing continued to slide in the third quarter, dropping 1% to $164,000 from the prior quarter and 7% year-over-year. This price has now dropped for three quarters in a row.

The rolling four-quarter price per unit for nursing care fell after two quarters of gains. The price per unit fell 4% in the third quarter of 2016, to $88,500 quarter-over-quarter. However, the price per unit is up 14% from last year, when it registered $77,500.

The divergence in price per unit trends for seniors housing and nursing care properties over the past year can be attributed to some high prices trading for nursing care. Several new nursing care properties are designed for higher acuity, which is different than the traditional nursing care model and, therefore, offers the potential for more cash flow per bed. In addition, there have been some turnaround buyers paying top dollar for the cash flow a property could potentially experience based on changing its mix of patients. Some of these properties are not receiving as many Medicare patients as their perceived market potential indicates, so buyers are betting that the operators will implement a strategy to increase the amount they receive from Medicare to make the properties more profitable. , the overall effect of lower interest rates has allowed buyers to pay higher prices.

Source: NIC MAP® Data Service

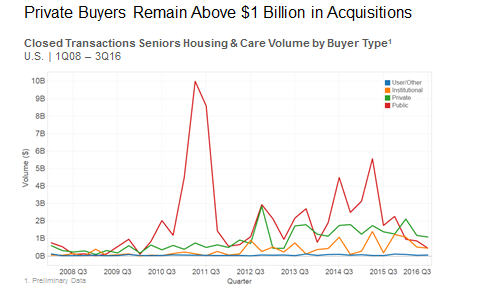

Private Buyers Acquire over $1 Billion

Private REITs and smaller private entities remained steady buyers in the third quarter, with an aggregate acquisitions volume over $1 billion for the 13th straight quarter. Although the overall volume from all buyer types fell quarter-over-quarter, the private buyer fell the least, with a 7% decline from $1.2 billion to $1.1 billion. The majority of these deals are not of the magnitude that we see on the public buyer side, but the private buyer represents a relatively consistent flow of deal-making.

Private buyers’ resiliency most likely can be attributed to several factors. First, there is a large amount of private capital searching for yield within this environment of low interest rates, so commercial real estate—including seniors housing and care—has attracted its fair share of buyers to the market. And compared with other commercial property types, seniors housing and, especially, skilled nursing have a larger cap-rate spread (in other words, higher expected investment returns), which is a welcome opportunity for many private REITs, hedge funds, and other partnerships.

Second, there are many smaller transactions representing strategic buying and selling. These transactions may include buyers looking to position themselves to gain market share or reposition a property, or a seller looking to shed some non-core assets, such as a smaller portfolio or a one-off property sale.

On the public side, buyer volume, which is usually dominated by the public REITs, continued to decrease in the third quarter. It registered a 48% decline quarter-over-quarter to only $448 million from $866 million, and an even more significant 74% decline year-over-year. In comparison, volume from private buyers decreased a much smaller 21% year-over-year.

The institutional buyer volume only decreased 12% quarter-over-quarter and actually registered more volume in the third quarter than the public buyer.

Source: NIC MAP® Data Service

Less than 100 Transactions

The number of transactions decreased along with dollar volume in the third quarter. Preliminary figures show that less than 100 deals closed, although NIC usually sees some adjustments to these figures as smaller transactions are reported to the NIC MAP® Data Service after the close of the quarter. The current transactions count shows a drop-off in transactions from last quarter and also from the third quarter of 2015. There is talk of volume being slower because of the lack of large portfolio sales, but the transactions count seems to be holding up. Although we are not seeing the 130–150 transactions closing per quarter as we did over the last couple of years, closing about 100 transactions per quarter is still fairly robust activity.

Out of the 96 closed in the third quarter, 72 transactions were for single properties, and 24 were portfolio transactions. Single-property transactions dropped 18% from the prior quarter, when 88 closed. The number of portfolio transactions dropped 14%, from 28 to 24.

Over the past couple of years, an average of 105 single property deals and 29 portfolio deals closed per quarter.

When we look at transaction size, we did not see larger transactions of $1 billion or more during the third quarter. One exception was a large portfolio transaction from Welltower that was announced but did not close in the third quarter. In fact, the last time a transaction closed with $1 billion or more in seniors housing and care properties was in the fourth quarter of 2015, with the Griffin/NHI Trilogy deal. Also thin during the past two quarters have been deals in the range of $500 million to $1 billion.

[/expand] [cresta-social-share]

In 2015, Wages Rose for Some, Stagnated for Others in Long-Term Care

For seniors housing and care providers, employee wages make up a significant share of overall expenses. In states with rising minimum wages, that slice of the expenses pie has the potential to widen further. This is especially true in the skilled nursing sector, where providers typically employ a greater number of higher-skilled medical workers and certified nursing assistants. Indeed, as NIC’s Chief Economist Beth Mace alluded to in the last NICMAP® Webinar, data from the U.S. Bureau of Labor Statistics indicates that overall nursing home employee average hourly earnings rose faster than inflation at a pace of 3.2% from June 2015 to June 2016.

But rising wages are not the leading labor headline in some areas. Two recently published labor studies indicate that many ground-level employees in long-term care did not see their wages grow in 2015, which may be counterintuitive to some considering the perception that the minimum wage is now on the rise. The research indicates that lower-skilled employees in skilled nursing did not realize the growth in wages that were realized by the sector’s higher-level employees (e.g., administrators and managers) in 2015.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Nursing Home Administrator Wages on the Rise . . .

A study from the Hospital and Healthcare Compensation Service shows that nursing home administrators earned an average 3.8% salary increase from 2015 to 2016, compared to the 2.5% increase reported the prior year, according to McKnight’s Long-Term Care News. Registered nurses and directors of nursing also received wage increases. Positions at the administrator level earned the highest percent increase. Wage growth for this job category may make this type of employment more attractive to young people just beginning their careers or established professionals looking to move to a new sector.

Seniors housing and care providers report difficulties in attracting and retaining qualified employees at all levels, including the administrator level. Leaders in the industry are taking notice, and groups like AHCA/NCAL, Argentum, ASHA, Leading Age, and NIC are highlighting the need to grow the pool of educated professionals who have the skills to run seniors housing and care properties in order to meet the growing demand of a rapidly aging population. For example, NIC’s Future Leaders Council has identified workforce recruitment as a priority issue and instituted initiatives to bring seniors housing and care to the attention of undergraduate and graduate students. In addition, Argentum hosted a one-day symposium on workforce development in Washington, D.C., in October 2016. Capital providers, too, will need to boost the number of qualified workers in the sector. Right now, the worker pools across seniors housing and care are relatively small compared to what the sector will need as the baby boomers age into seniors housing properties in the coming decade.

But Wages Didn’t Grow for Nursing Assistant Employment

Operators may experience wage pressures from increased labor competition across all industry groups, minimum wage increases in states and municipalities, and the new overtime law that will go into effect at the end of 2016. Despite the upward pressures on wage rates felt by operators, a study from the Paraprofessional Healthcare Institute (PHI) indicated that nursing assistants made an average of just under $12 per hour in 2015; the median annual salary was $19,000. Ten years ago, nursing assistants made just over $12 per hour (adjusting for inflation), meaning wages for this group have declined over the past decade when inflation is taken into account. The combination of relatively low wages and high workplace injury rates makes the task of attracting and keeping nursing assistants difficult for many providers. High turnover is an additional and expensive challenge for providers as well, because wage competition and employee satisfaction potentially incentivize employees to change jobs for small wage gains.

In looking at recent data, it is important to keep in mind that some of this data excludes minimum wage hikes implemented after the data collection period. The new overtime rule will certainly impact this group of workers as well, but is not taken into consideration here. A future comparison of this study and newer iterations of it will prove to be a useful resource in understanding the true impact of new labor regulations.

Wage Rates Aren’t the Only Challenge in Employing Nursing Assistants

According to PHI, over 90% of nursing assistants, who make up nearly 40% of nursing home employees, are women, and 20% were born outside of the United States. Many of those female and foreign-born workers fall in the 45-to-65 age cohort. One challenge for skilled nursing is finding new workers to fill positions as today’s caregivers retire. The nursing home sector also will be challenged to fill new positions that will be needed to accommodate growing demand from aging Baby Boomers.

But younger workers today may not be easily attracted to skilled nursing. Evidence suggests that social, educational, and professional changes over the last two decades have resulted in fewer women seeking careers typically considered “female,” such as nursing, meaning there may be fewer workers to replace today’s nursing assistants as they retire.

Today’s 20% foreign-born long-term care workers will also need to be replaced at some point. That replacement rate could be complicated, especially if immigration policy makes it harder for current workers to stay in the United States or for new workers to enter the U.S. Foreign workers are hard to replace with domestic workers, because Americans are less typically likely to accept the lower wages the positions pay.

Nursing assistants help nurses with some clinical tasks and are mostly responsible for assisting residents with activities of daily living tasks (ADLs). These tasks often involve lifting residents, which has resulted in this employee group having a workforce injury rate over three times the national average. For skilled nursing providers, workforce injury costs have become a major expense in addition to general labor costs. Adding to these costs, only about 20% of nursing assistants have health insurance, and another 20% receive their healthcare coverage through Medicaid and Medicare.

Quality Labor Is a Public Health Issue

Because almost all nursing homes rely on Medicare and Medicaid for revenue streams, states and the federal government have some mechanisms to increase wages for nursing assistants. In Massachusetts, Governor Charlie Baker is instituting a raise for nursing home workers, including nursing assistants, the Boston Globe reported. One possible outcome of Governor Baker’s move is that the public will gain greater insight into the labor pressures facing those who provide key services to our country’s frail seniors.

Providing quality care requires a qualified workforce (individuals who are educated, dedicated, and trained appropriately). High staff turnover in skilled nursing properties can result in more opportunities for mistakes, because research has shown that patients are most vulnerable and most likely to experience an adverse effect during transitions in care, such as a handoff from former to new employee. High turnover also could mean that nursing assistants have less opportunity to hone their craft. Institutional knowledge and compounded experience can be critical in creating a highly effective workforce capable of delivering on the services for aging residents struggling with chronic and terminal conditions and disabilities.

Takeaway for Providers

Making conscientious investments in labor and workforce development now could reduce the challenges providers will face in the near-future to attract and retain employees. Providers who invest in high-quality labor now could also benefit from demonstrating quality care to payors and partners, which could offer the additional benefits of costs savings and stronger revenue streams. As government initiatives move the industry toward value-based payment, risk sharing, and strategic partnerships, high-quality labor is certain to be a major component of value propositions of the providers.

[/expand] [cresta-social-share]

Home. Risk. Value.

A First Look at the 2017 NIC Spring Investment Forum

Setting business strategies for an unclear future continues to challenge many in seniors housing and care. It’s an issue that multiple sessions at the 2017 NIC Spring Investment Forum, March 22–24 in San Diego, CA, will address.

“It begins to sound like a broken record, but for years we’ve been anticipating this vast tidal wave of aging seniors,” said NIC CEO Bob Kramer. “That tidal wave is now nearly here, and time’s running out for everyone in seniors housing and care to put in place strategies to care for them efficiently, effectively, and profitably.”

Understanding the full value the industry has to offer seniors and stakeholders alike will be critical for operational success in the future, he said. “There’s additional value to be unlocked.”

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Breaking Down Silos

Seniors housing and care is a strong platform for managing the most expensive lives in healthcare. But for decades, operators have infrequently ventured outside their four walls. Going forward, Kramer said, “policy changes, new partners, and even consumers will demand that assisted living and skilled nursing providers demonstrate capabilities they don’t possess today.” Many discussions at the Forum will focus on how operators can begin to identify partners, tools, and strategies that will allow them to deliver and demonstrate the value they offer to partners and payors.

The tidal wave of seniors is also bringing a surge of new technologies, products, and services aimed at making their lives better. The enablers of these offerings will be looking to partner with seniors housing and care operators, who care for large numbers of the frail seniors they’re seeking to serve. “Both sides have value the other needs,” said Kramer.

Today’s Markets and Tomorrow’s Strategies

The Forum’s programming in March 2017 will feature a good mix of sessions for both providers of capital and care to begin thinking about their short-term and long-term strategies. Some highlights include:

- Capital Connections, a networking opportunity to meet select capital providers in a relaxed environment and discuss various financing options.

- Conference Luncheon with former Senator Tom Daschle (D-South Dakota) and former Senator Bill Frist (R-Tennessee), who will discuss the impact of a new president and a new Congress on health care and long-term care policy, entitlement reform, and tax policy.

- Capital and economic sessions, including valuations, economic trends, supply and demand trends by product type, and the most recent data from NIC.

- Sessions on unlocking value, which will include examples and case studies of what providers in the industry are doing.

Registration Opens in December

Registration for the 2017 NIC Spring Investment Forum will open in December. Sign up to receive a notification once registration opens.

[/expand] [cresta-social-share]

Seniors Housing & Care Industry Calendar

October – November 2016:

30-2 LeadingAge: 2016 Annual Meeting and EXPO, Indianapolis, IN

15-17 REITWorld: NAREIT’s Annual Convention, Phoenix, AZ

NIC Partners

We gratefully acknowledge our following partners: