M&T Bank Expands Healthcare Lending Platform: A Conversation with M&T’s Christopher Callaghan

Christopher Callaghan

With a long track record in seniors housing and care lending, M&T Bank continues to see the sector as a driver of new business. NIC’s senior principal Bill Kauffman recently spoke with Christopher Callaghan, head of Healthcare Banking at M&T Bank. They discussed today’s lending environment and M&T’s plans for growth in the sector. Here’s a recap of their conversation:

Kauffman: Can you give us some background on your professional career and how you became head of Healthcare Banking at M&T Bank?

Callaghan: I started my banking career at a trust company in Boston. Then I became a commercial lender at the First National Bank of Maryland, joining the healthcare team in 1999 with a focus on acute care relationships. After M&T acquired First National Bank of Maryland/Allfirst, I had several roles in the Healthcare Banking Group, eventually being selected to lead the team in 2012.

Kauffman: How long has M&T Bank been lending to the seniors housing and skilled nursing sectors?

Callaghan: M&T formed its Healthcare Banking Group in 1988. M&T provided mortgages to skilled nursing facilities dating back to the 1960s, and we financed our first CCRC in 1978. M&T thought then, as we do today, that our clients want to work with a team that has an understanding of their business.

Kauffman: What is the focus at M&T Bank today and what is the growth plan overall for the bank?

Callaghan: Our healthcare lenders have historically called on all healthcare service providers in specific geographies. The same banker calls on the hospital, skilled nursing facility, physician practice, and seniors housing in a given market. This allows our bankers to learn from different parts of the continuum, and we think our clients like having bankers with a fairly broad view. M&T has a strong track record as a community bank in each of the regions it serves. We are looking at ways to continually enhance our community relationships and develop new opportunities. We have several initiatives looking outside of our traditional regions to provide incremental growth. Healthcare is a big part of that.

Kauffman: How about your organization’s plans for growth in financing seniors housing and skilled nursing properties?

Callaghan: Healthcare is focused on four initiatives. We’ve started a national bridge platform for HUD/FNMA placement in M&T Realty Capital and added seniors housing financing in the Pacific Northwest where we have a successful commercial real estate lending practice. We’re adding healthcare lending in Florida as we expand our commercial efforts in that market and we are dedicating resources to building healthcare relationships on a national basis.

Kauffman: Do you lend to independent living, assisted living, memory care, skilled nursing, and CCRCs?

Callaghan: M&T is generally comfortable with commercial and specialty real estate and we continue to have a strong appetite for construction financing. We have a long track record of lending to seniors housing, CCRCs, and skilled nursing, and expect it to continue to be a driver of new business at the bank. From a credit appetite, we are active across all of the above. M&T continues to lend on balance sheet to provide flexible commercial bank execution for properties pre-stabilized or recently acquired. Additionally, we can provide a full suite of services, including municipal bond underwriting (tax exempt bonds) to the CCRC community, as well as permanent market execution across Fannie Mae, Freddie Mac, FHA/HUD, and life companies.

Kauffman: How has that changed over the last few years?

Callaghan: We have really seen the pace of seniors housing development increase in the past several years. But more than just development, it seems that market participants have changed. There are two key drivers from our perspective: more institutional money and better data. We’re partnering with sophisticated investors who are contributing significant equity into development. In comparison to other cycles, today’s capital stack is so much stronger with the higher levels of equity. New equity and enhanced transparency to the sector—as NIC’s mission has been fulfilled—has in turn accelerated the pace of development in a more conservative way than we might have seen in the last cycle. Also, the use of data and technology has created innovation around quality of care and resident needs, which enhances the patient and resident experience, and also improves day-to-day management, strategic thinking and problem resolution. Particularly in the skilled nursing environment, innovative providers are creating advantages in a competitive market.

Kauffman: What are the greatest challenges for growing your business in seniors housing and skilled nursing?

Callaghan: The differences in each sector drive how we look at challenges. For the skilled sector, we tend to focus on quality of care, the reimbursement environment, and regional staffing issues. For seniors housing development, we’re looking at a market’s demographics (including labor), competitive product offerings, and the operator’s portfolio. In each case, there are multiple alternatives from other banks, to HUD or agency placement. The capital markets seem to be as competitive as ever. We play pretty well in construction/acquisition loans on the balance sheet side and with our long-tenured relationships on the agency side.

Kauffman: What types of terms and rates does M&T Bank offer its borrowers?

Callaghan: In the development market, the loan tenure is generally tied to the stabilization schedule. While we are usually linked to an expected liquidity event, with acquisition or refinancing situations, we tend to prefer floating rate debt with synthetic fixed rates. The market is pretty transparent, so we are usually in the range of market rates.

Kauffman: How do you compete with other lenders?

Callaghan: We have a long track record as an active participant in the healthcare sector. We often find that we’re competing on advance rates and loan structures where we think we can offer creative solutions.

Kauffman: What are the advantages of borrowing from M&T Bank?

Callaghan: We are a knowledgeable long-term lender in this market. We grew through the last down cycle using the same discipline and focus we use in the upturns.

Kauffman: When do you turn an opportunity down?

Callaghan: M&T tends to be less competitive in markets we don’t know well or that we are concerned about. We can usually get our hands around structure or pricing issues, but we struggle when we don’t have faith in a particular market or location.

Kauffman: What do you look for in a good borrower?

Callaghan: Partnership. We like to share information, contacts, and referrals. We feel that we can really add value in a situation but can only be there when we share information and ideas through an effective partnership. We’re seeing an increase in that activity, making referrals to investors looking for operators, or operators looking for real estate. This is a small industry, and we tend to form deep relationships that we think help us out a lot.

Kauffman: What do you see as the most significant opportunities and risks in private pay seniors housing right now?

Callaghan: Demographics signal continued growth in the sector. We’re seeing certain metrics showing supply may be outpacing demand. There are changing senior needs and tastes, and aging inventory, so we feel there is still a lot of runway for targeted seniors housing development. We’re curious about development with lower price points; there is likely another untapped market there. The biggest risk is overdevelopment in certain locations or projects that don’t meet changing needs. Looking forward, we are expecting innovation in care and delivery channels and how they meet the changing needs of the senior population.

Kauffman: How about skilled nursing—opportunities and risks?

Callaghan: We see continued consolidation with well managed regional operators acquiring portfolios from national providers and the few remaining mom-and-pops. We like this market and see continued opportunity. The biggest risks remain reimbursement stream, payment models, and staffing issues.

Kauffman: And how do you see the short-term playing out when the Patient-Driven Payment Model (PDPM) goes live next year?

Callaghan: PDPM will largely have facility-specific impacts. Some of our clients expect to do quite well under PDPM and have a business mix that will benefit from the shift. There are others that may not fare as well. The best operators will adapt to the model and move on.

Kauffman: How can operators and investors mitigate these risks now?

Callaghan: Ultimately, providing great care to residents and attracting the best caregivers tends to produce above market results over the long run. We worry about borrowers who might have taken on too much leverage, either debt, or operational leverage (staffing), which can strain operations when there are unforeseen bumps in the business plan.

Kauffman: What about the future, say, five to ten years out? What risks do you see and how should investors and operators prepare?

Callaghan: In the out years, I’d expect higher acuity across the sectors. Residents in assisted living will likely be getting significant therapy hours. Are we building today for that contingency? How do we staff a more intensive skilled nursing facility? How does IT and data fit in?

Kauffman: In terms of deal flow, how is the environment today?

Callaghan: We are seeing significant opportunities in seniors housing development and skilled nursing acquisitions.

Kauffman: Is it very competitive for deals?

Callaghan: Seniors housing and skilled nursing are very strong asset classes. We are seeing more institutional money and more banks entering the market, so, yes, it is very competitive.

Kauffman: What is your view on pricing/valuations right now in both seniors housing and skilled nursing?

Callaghan: There was a period where skilled bed prices seemed to skyrocket in certain markets. Through performance, the value has been proven out, but at the same time, valuations today seem more rational. On the seniors housing side, we are seeing more upscale facilities in high cost locations, so the valuations are varied but seem appropriate given the individual markets. Newer facilities are commanding higher rates. The older properties that may have suffered some occupancy challenges are seeing small increases in rents.

Kauffman: There has been much discussion about the private debt funds in the market place recently. What are your thoughts about this? Are they filling a necessary void since banks cannot take as much risk as they did prior to the financial crisis?

Callaghan: They are definitely showing up on our radar and we’ve seen them do a few deals. I think it speaks more to the performance of the sector than it does to fallout from the downturn, because we’re seeing new banks entering the competitive set.

Kauffman: It sounds like there are many deals being done with “covenant-lite” structures, or no covenants at all? What are your thoughts on that?

Callaghan: We generally see a need for prudent controls as we encounter construction, stabilization, or turnaround risk. We’ll work with our borrowers to create reasonable structures that work for both of us and balances both of our needs. Covenant-lite is more appropriate in the permanent market. We are there for those transactions, but agency placement often seems to be a better choice in many of these situations.

Navigating Change – Programming for the 2019 NIC Spring Conference

NIC conferences are characterized by senior decision-makers focused on networking, thought-leader speakers and insightful educational programs. The 2019 NIC Spring Conference program will not disappoint. Once again, an exciting, leading-edge mix of sessions is on offer throughout the event. The conference’s program provides industry-leading insights and strategies that focus on today’s real-estate based investment landscape, while addressing the challenges and opportunities of adapting to a value-based world.

As the seniors housing and care sector prepares to adapt to numerous fundamental changes, there is a lot to consider for anyone hoping to navigate the coming years. Our healthcare system is moving to a value-based system. Providers are taking on risk and finding ways to share rewards when outcomes improve at a lower total cost of care. A new generation of seniors will live longer and demand more from the sector. Workforce challenges persist, as does the adoption of new technologies. Meanwhile, healthcare players are beginning to take an active interest in the sector.

Focused on navigating these changes while continuing to deliver value for every attendee, this year’s schedule of breakout sessions is divided into two focus areas: “Investing and Valuations” and “Value Creation, Partnerships & Risk.” “Investing and Valuations” is aimed squarely at addressing issues of interest primarily to capital providers. Over a variety of formats, these sessions look at market trends, capital flows into the sector, valuations, home healthcare and home care investment, and the impact of workforce issues, in addition to providing the very latest data and analysis that this audience has come to expect from NIC.

The “Value Creation, Partnerships & Risk” program tackles many of the challenges and opportunities facing owners, operators and providers today, particularly as they plan for the future. Attendees will gain insight, in a variety of settings, on how to achieve care coordination, win managed care business, form upstream and downstream healthcare partnerships, create a high-performance network, and approach the challenges and opportunities of taking on risk. These sessions will offer a range of perspectives, presenting real-world answers to key questions such as: why are these initiatives important? What exactly is changing now? Who will pay for it, and how will it all come together for businesses moving forward?

In addition to general sessions, including a luncheon keynote talk to be delivered by bestselling author, consultant and futurist Ian Morrison, the conference offers a variety of session formats. Traditional breakout sessions of 60 and 75 minutes each will feature thought-leader presentations and panel discussions. In addition, specialty programming offers creative new formats designed to increase engagement, deliver ideas and solutions more efficiently, and encourage discussions in more intimate settings. An engaging new “Hackathon” session will encourage attendees to select and solve an industry-related issue through an interactive experience. Small group discussions round out the program with intimate group conversations lead by industry experts.

Taken as a whole, this year’s program reflects an industry that is growing, attracting capital, and working hard to overcome the everyday issues it has been facing for years while simultaneously looking ahead to a period of significant new challenges and exciting new opportunities. More information on the 2019 NIC Spring Conference, to be held in San Diego, California, February 20-22, as well as conference registration, can be found here.

A Tale of Two Cities…and Many Markets

Beth Mace

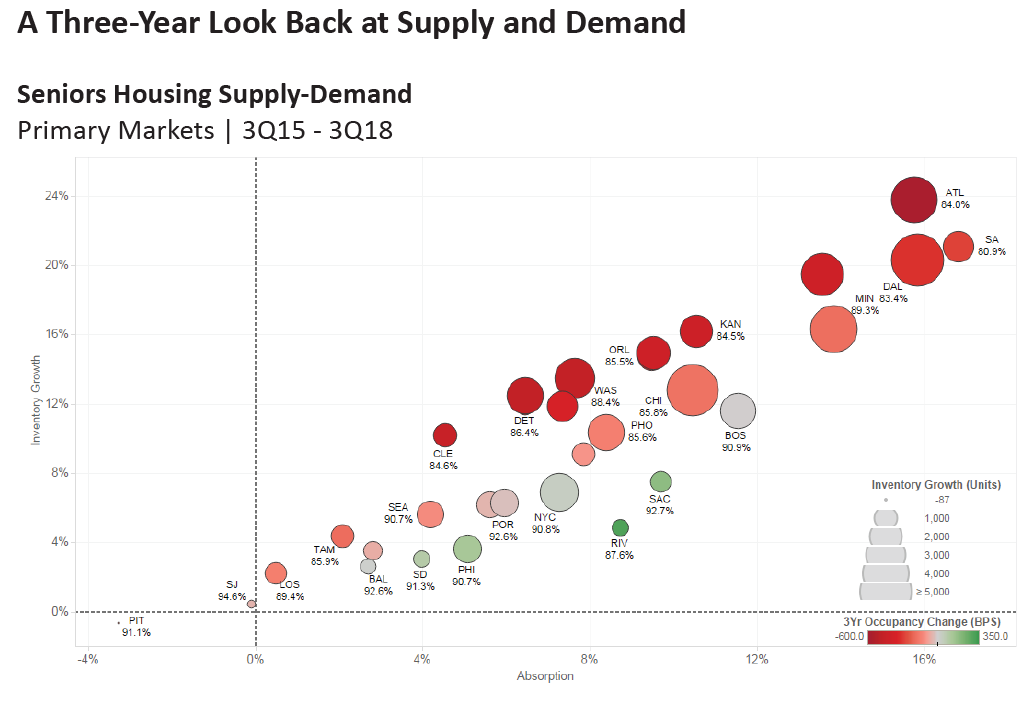

The seniors housing occupancy rate remained at a six-year low rate of 87.9% in the third quarter as inventory growth continued to broadly exceed net demand at the aggregate national level. However, it’s a tale of two, three and ultimately many markets that are each performing differently as unique conditions and factors contribute to disparate development and demand patterns at the local and metropolitan market level. This is evident in the very wide disparity between the best and poorest performing markets with a 13.8 percentage point variance between the most occupied market (San Jose: 94.6%) and the least occupied market (Houston: 80.8%) in the third quarter.

The chart below provides details of the supply and demand dynamics for the NIC MAP 31 Primary Markets in the past three years. The vertical axis shows annual inventory growth in percentage terms, while the horizontal axis shows annual net absorption growth for the past three years. The color of the circle depicts the movement of the occupancy rate over the past year: red for a deteriorating occupancy rate and green for an improving occupancy rate. The size of the circle shows how many absolute units were added to inventory in the past three years.

In the past three years, Houston, Atlanta, San Antonio and Dallas have all seen inventory grow by 20%, while Minneapolis, Kansas City, Denver and Orlando have seen a 15% increase in stock. In all these metropolitan markets, occupancy has fallen between two and six percentage points as the pace of new inventory growth has exceeded that of demand.

The flip side is metropolitan areas that have not seen very much inventory growth and have seen occupancy rate improvement in the past three years. This includes Riverside, Sacramento, Philadelphia, Baltimore, San Diego and New York.

The strongest net absorption occurred in many of the markets that experienced the fastest growth in inventory. In the chart, this can be identified by the markets furthest to the right. This includes San Antonio, Dallas, Atlanta, Minneapolis, Houston and Kansas City. The fact that these circles are also red, however, shows that occupancy declined in these markets over the past three years and that, while demand was strong, it simply was not “strong enough.” However, there is a good chance that demand will start to catch up in some of these markets because projects currently under construction have declined significantly. This is particularly the case in San Antonio, which had less than 100 units under construction as of the third quarter.

In terms of absolute unit growth over the past three years, the most unit inventory gains occurred in Dallas, Chicago, Minneapolis, Atlanta and Houston–those markets with the largest red circles in the chart. These five geographies accounted for 40% of the 54,000 units of inventory growth in the NIC MAP Primary Markets in the past three years. Behind this top five group are Washington DC, New York City, Detroit, Phoenix, and Boston. The top 10 markets for inventory growth accounted for 63% of inventory growth in the past three years. Offsetting these trends are markets with relatively little inventory growth over the past three years which include San Jose, Baltimore, Las Vegas, San Diego, Riverside, and Pittsburgh.

Taken together, this analysis supports the maxim that all real estate is local and that broad aggregate trends can obscure opportunities. It would appear that the much-ballyhooed supply story of San Antonio has been paid heed and units under construction currently have slowed dramatically, providing a pause in inventory growth to allow demand to catch up and occupancy to rise above 81%. Meanwhile, Phoenix currently has the most absolute number of units under construction at 3,524 units or 13.9% of its inventory, dwarfing the 2,368 units completed in the past three years. Eight other markets have greater amounts of units under construction today than what was completed in the past three years. Other than Phoenix, this includes Baltimore, San Diego, Riverside, Sacramento, Los Angeles, Philadelphia, New York, and Miami. These markets bear watching and deserve further examination to determine if demand in these markets will in fact be “strong enough.”

NIC Future Leaders Council Celebrates its 10th Year

Sara Veit

In this article, Sara Veit, Managing Director, Omega Healthcare Investors, Inc. recognizes new and alumni Future Leaders Council members.

The Future Leaders Council (FLC) was established by NIC in 2009. The idea for the NIC Future Leaders Council was the result of input from current and past chairs of NIC’s Board of Directors. Their goal was to provide FLC’s members with a unique opportunity to help advance NIC’s mission by contributing to the work of NIC committees and task forces on board-directed priorities and initiatives, and through its own initiatives.

Another goal for FLC members was to develop leadership skills and meaningful professional relationships with the current industry leaders through the experience, networking, and informational mentoring that resulted from these contributions–and through leadership training.

The current FLC is comprised of 26 professional members who were nominated and selected to serve a three-year term. Each member was nominated by a NIC volunteer leader and was ultimately selected among the numerous nominations by the FLC Oversight Committee to serve on the FLC.

At the most recent NIC conference held in Chicago, NIC welcomed the newest incoming FLC Class of 2021, which includes the following members:

- Jay Leo, The Springs Living LLC

- Alex Massopust, New Perspectives Senior Living

- Tom Mathisen, Life Care Services

- Lucas McCurdy, Coastal Reconstruction Group

- Dennis Murphy, Benchmark Senior Living

- Courtney Nickels, Artemis Real Estate Partners

- Dana Scheppmann, Capital One Healthcare

- Spencer Smith, Sentio Investments LLC

- Julie Stande, Nixon Peabody

As a current member of FLC, I was tasked with interviewing the class of 2021. My first question was: “What motivated you to seek membership in the FLC?”

“NIC has done so much to propel the seniors housing and care industry forward, and there is so much more to do as we look to carry out the mission of NIC. The NIC FLC will be a major component and contributor to the efforts of NIC moving forward, and I’m excited to be a part of that. I am also keenly aware of the high quality of individuals that comprise the NIC FLC, and I wanted to serve in a group that was highly thought-provoking and innovative.”

– Tom Mathisen, VP of Life Care Services

This year FLC is chaired by Andrew Smith, Brookdale Senior Living with co-chairs Brandi Healey, Sabra Healthcare REIT, and Sarah Peerson, Wells Fargo Bank. The leadership team is currently finalizing our 2019 Work Plan which designates committees and task forces for current members to get involved. The Class of 2021 looks forward to their assignments.

“Whether it is in planning work retreats, contributing to the NIC Insider Newsletter, the NIC Investment Guide, or serving on targeted committees,

I am committed to volunteering time in and out of the office where I am best-suited or needed most.”

— Courtney Nickels, VP of Artemis Real Estate Partners

One of the greatest accomplishments of the FLC was identifying the need for an educational workshop for new professionals entering the industry. This past fall, FLC designed, marketed and hosted the third annual and expanded four-hour Seniors Housing Boot Camp. Over 70 professionals registered for the sold-out event. FLC plans to continue to spearhead this recurring event in the future through the leadership of Richard Wang, Belmont Village (FLC Class of 2019); Ryan Chase, Blueprint Healthcare (Class of 2020); and Fritz Kieckhefer, CIBC (Class of 2020).

This year, FLC’s goals are focused on the following areas: educate the NIC community; develop a strong and sustainable FLC community; promote workforce participation in seniors housing and care; and “expanding the tent” of senior housing.

“I am eager to identify ways to grow outside of an individual company level to positively influence the future of senior living.”

— Jay Leo, COO of The Springs Living, LLC

The work being done by FLC provides its members the unique chance to continue to develop their volunteer leadership skills and, at the same time, broaden their professional network. NIC’s goal is to continue to attract emerging leaders with energy, drive, and passion for the benefit of the seniors housing and care industry.

The FLC’s past 10 years have been a huge success, but it is even more exciting to think of what else might come from this group of emerging leaders. Thanks to NIC for your unwavering support and resources, and to the FLC alumni community for paving the way for this one-of-a-kind opportunity to impact our industry.

“Together we should be able to tackle some of seniors housing’s biggest obstacles and make a real noticeable difference in the market.”

— Dennis Murphy, director of Benchmark Senior Living

“I am excited about being on a platform on the front lines of aging around the best leaders in the industry where my passion, work ethic, and desire for impact can be fully realized.”

— Lucas McCurdy, senior vice president of Coastal Reconstruction Group

This is the listing for FLC alumni.

FLC current class members (2019, 2020 and 2021) are listed here.

If you have interest in applying for the class of 2022, visit this page. Nomination applications are due in May 2019.

Granger Cobb Institute Moves Forward at Washington State University

A recently launched Washington State University institute named in honor of industry pioneer Granger Cobb has already raised $1.8 million in donations as it prepares to offer an undergraduate major in senior living operations within the next few years.

The Granger Cobb Institute for Senior Living was approved last May by Washington State University (WSU), Pullman. The Institute grew from a course in senior living offered by WSU–an idea generated by a handful of senior living industry leaders including Cobb, who passed away in 2015.

“Granger was one of the truly creative early CEOs in our industry,” said Bill Pettit, president of R.D. Merrill Co., who also helped create the first senior living course at WSU. “He was all about operations.”

Cobb had a long career in the senior living industry. He founded assisted living company Cobbco and served as president and CEO of Summerville Senior Living. He was president and CEO of Emeritus Senior Living and became a board member of Brookdale Senior Living when Emeritus merged with Brookdale. Cobb was also a former chairman of Argentum, the senior living industry association.

Pettit, along with Chris Hyatt of New Perspective Senior Living, announced plans for The Granger Cobb Institute at the Argentum Conference in Nashville last year.

The Granger Cobb Institute for Senior Living is part of the School of Hospitality Business Management at WSU’s Carson College of Business. Nancy Swanger, director of the School of Hospitality, has spearheaded the effort to take the original senior living course and set the stage for it to become a full major, said Pettit. “She has been incredibly productive in getting the University to focus on this opportunity.”

Over the past three years, WSU has expanded its senior living management curriculum. It covers everything from marketing, lifestyle and dining, and financial management to the delivery of care.

While a number of universities offer important programs in gerontology, the new senior living major at WSU is the only program of its kind in the nation to focus on operations. “We are excited about WSU’s commitment to offer a full major in senior living,” said Pettit. A program dedicated to operations is important because of the complexity of senior living and how it differs from the hospitality business, noted Pettit. Senior living includes a high degree of government regulation as well as the delivery of care. “The Granger Cobb Institute will be turning out grads with the type of education and training that aligns perfectly with the needs of our industry,” said Pettit.

The Institute is already working on research in the field of senior living, according to Scott Eckstein, a clinical assistant professor and senior living executive in residence at WSU.

An online non-credit certificate program will be offered in 2019. The program will include seven courses that cover all aspects of senior living management. The course is open to those interested in working in the senior living industry.