Learning with Earnings: A Conversation with Cindat’s Allan He

Allan He

Though the countries have their differences, the U.S. and China have something important in common: an aging population. China has more than 200 million people over age 65. The U.S. is catching up with its older population projected to double to more than 98 million by 2060.

This shared perspective explains in part why Cindat Capital Management, a large private investment firm based in Beijing, is focused on seniors housing and care properties in the U.S. According to Allan He, senior partner at Cindat, it’s a way to learn about the industry and apply those lessons to China while generating good returns.

NIC chief economist Beth Mace recently talked with He about Cindat’s evolving strategy and where it’s headed. Here’s a recap of their conversation.

Mace: Tell us about yourself.

He: I am a senior partner at Cindat Capital Management, a fund management platform based in China. I was educated as a civil engineer and have more than 20 years of experience in construction, real estate development and investment. Our mandate at Cindat is to invest on behalf of institutions and investors from China, or originally from China, in offshore platforms. I started with the company when it was a new venture four years ago. I am responsible for Cindat’s healthcare and senior living investment business.

Mace: Are your seniors housing investments global in scope?

He: We are global in scope. Our investor base is mainly made up of large institutional investors. Most of them are insurance companies or public investment companies with large amounts of capital to be deployed on a routine basis. Two years ago, we were looking for investment opportunities and seniors housing came up on our radar screen. We first started in the U.S., but we have recently closed a transaction in the U.K. We also invest in senior care in China. We’re building out our global seniors housing and care platform.

Mace: What was it about seniors housing and care in the U.S. that attracted Cindat to the sector?

He: Two major factors: first, we were looking for stable cash flow assets; and second, after initial study, we realized that the sector has a lot of synergies with our home market in China. We can locate investments in the U.S. with stable cash flow and we can gradually bring this expertise back to China where seniors housing is just getting started.

Mace: How did Cindat get started in the U.S.?

He: We started looking at portfolios because we needed sizable transactions since our investors are primarily institutions. Two years ago, the major U.S. REITs were facing the challenge of increasing interest rates as well as some changes on the regulation side. When the REITs started selling portfolios, we looked at the sector. Our initial strategy was to collaborate with the major REITs since we were starting from scratch. We like to take the time to understand the sector. If you look at our $930 million joint-venture transaction with Welltower, the portfolio covers 11 states and nearly 40 assets. For us, the size of the transaction matters as we learn about the asset type.

Mace: How much equity has Cindat invested in seniors housing and care in the U.S. and globally?

He: We have invested $250 million of equity in U.S. properties. There are some new deals in the pipeline. In the U.K., we invested £100 million. In China, we are closing some deals which are more of an operating platform with equity there close to US$50 million. We have deployed about US$400 million equity in total worldwide, and we have a strong pipeline of potential transactions.

Mace: Are there any government restrictions on where or what Cindat can invest in?

He: That’s a big subject. A lot of people know about the recent controls established by the Chinese government to cool down investment in overseas real estate. Chinese investors have made a lot of money in real estate which has been booming for the past 15 years. Institutions and individuals tend to think real estate prices will keep rising and they have applied that same mentality to investments overseas. But overpriced transactions can hurt the public. So the government is cooling down the market with legitimate controls. In a way, that’s good because it makes the sector healthier. We have an advantage because Cindat is an established and professional firm with a proven track record.

Also, seniors housing is different from other real estate. China has strong synergies with the U.S. seniors housing market. One of our objectives is to locate investments in the U.S. and gain operations expertise for the asset model. This benefits the Chinese market, and so we do not see the government discouraging investment in seniors housing similar to the way it might for trophy real estate asset types like prime office or hotel properties.

Mace: Are Cindat’s seniors housing investments part of a dedicated fund or part of a bigger pool of money?

He: We have a committed pool of investors behind us. Cindat typically assembles multiple investors for each deal. We are in the process of aggregating a discretionary global fund for healthcare and seniors housing.

Mace: Are most of Cindat’s capital sources institutions?

He: Most of our investors are public companies listed in China or Hong Kong with a mandate to invest offshore. So far, we don’t have any wealth management type capital in senior housing investment, and we don’t have any funds directly from government. Some sovereign Chinese funds have a mandate to invest overseas, and we are in discussions with them.

Mace: What is Cindat’s targeted rate of return for seniors housing?

He: So far, we have mainly invested in properties with simple triple net lease arrangements. We are looking for stable cash flow. We expect a cash-on-cash return of 8-10%, but we do not have a specific return requirement. It depends on the deal, and the risk profile and asset type.

Mace: The U.S. public REITs provide a large platform. When Cindat chooses partners, do you prefer larger operators or capital sources?

He: It depends on the timing. We are in the learning stage, so we tend to engage with a local partner with good credit and a strong local base. In the long run, we will also be looking at smaller players and opportunity-type transactions. Our transactions will be more diverse as we evolve.

Mace: From an operator’s point of view, why would I want to use Cindat rather than another source of equity capital?

He: We are a complementary fit for those seeking institutional funds as well as for those seeking international investors. In the coming three to five years, we will rely heavily on local partners. That is a strong reason for operators, asset managers or REITs to work with us. Another reason is that we don’t have a lot of restrictions like the ones that frustrate public companies in U.S. We are more flexible and have a mid- to long-term outlook. For example, investors might try to avoid skilled nursing. But we are comfortable with the sector in the long run. It is not going to disappear. There is a lot of fundamental demand from aging seniors. We just need to figure out how to operate those facilities in a more sustainable fashion. That is our difference and our advantage.

Mace: Are there any risks for a U.S.-based operator to use Cindat’s funds, such as a currency or tax risk?

He: No. We haven’t run into any situation where a REIT or operator faces more risk by joining us. As international investors, we can be more flexible than other types of partners.

Mace: When would you turn down an opportunity?

He: There are some situations where the property is overpriced, and we would easily pass on that. The reason we have partnered with REITs is that they have already screened opportunities.

Mace: Does Cindat invest in independent living, assisted living, and skilled nursing properties?

He: We got into this sector with the premise that it is an operating asset. We don’t have a narrow agenda or geographic restrictions. We have not done any truly independent living properties. When we do skilled nursing, we tend to stay in the certificate-of-need states. As international investors, we avoid areas with less regulation and less transparency. We are interested in development with good operators with development expertise and where there is an opportunity to earn a good margin if the assets have the right format from the beginning. We would probably not do small individual developments.

Mace: Cindat provides equity capital for existing properties, restructurings and refinancing. What about construction financing?

He: With construction, we prefer a local third-party financing source.

Mace: Does Cindat provide capital for operations or only bricks-and-mortar?

He: We started with triple-net-lease arrangements. But that is not our long-term goal. We would like to set up RIDEA structures or invest in operators. We are looking at that. We would like to get into operations to benefit our assets and earn a good return.

Mace: Pricing, cap rates, and valuations in the U.S. could get hurt if interest rates rise. Any sense where pricing is headed?

He: We agree that pricing is a little hot at this point, and interest rates are rising. Healthcare regulations and tax policies create a lot of uncertainty. We are a bit cautious, so we are looking at opportunities in the U.K. and Europe. But we believe this is an interim stage in the U.S., and that in two years there will be a big pick up in the aging population and more demand. We have a seniors housing team in the U.S. headed by John Stasinos, who previously led HCP’s international portfolio.

Mace: Anything else that makes you worry or something else you’d like to share?

He: The operators in our portfolio are in the process of sorting things out. Investors get nervous, but we are still comfortable. We stay alert to operating issues and the covenants in leases. We also watch the political climate, especially related to the changes in the tax law and how that impacts our investors. We have an annual business plan and acquisition targets. We feel optimistic, and we are bullish on this sector. One of our advantages is our global strategy, which helps offset some of these local issues.

Will Pressure on Skilled Nursing Fundamentals Continue?

Bill Kaufman

The latest trends provide insights into the way forward

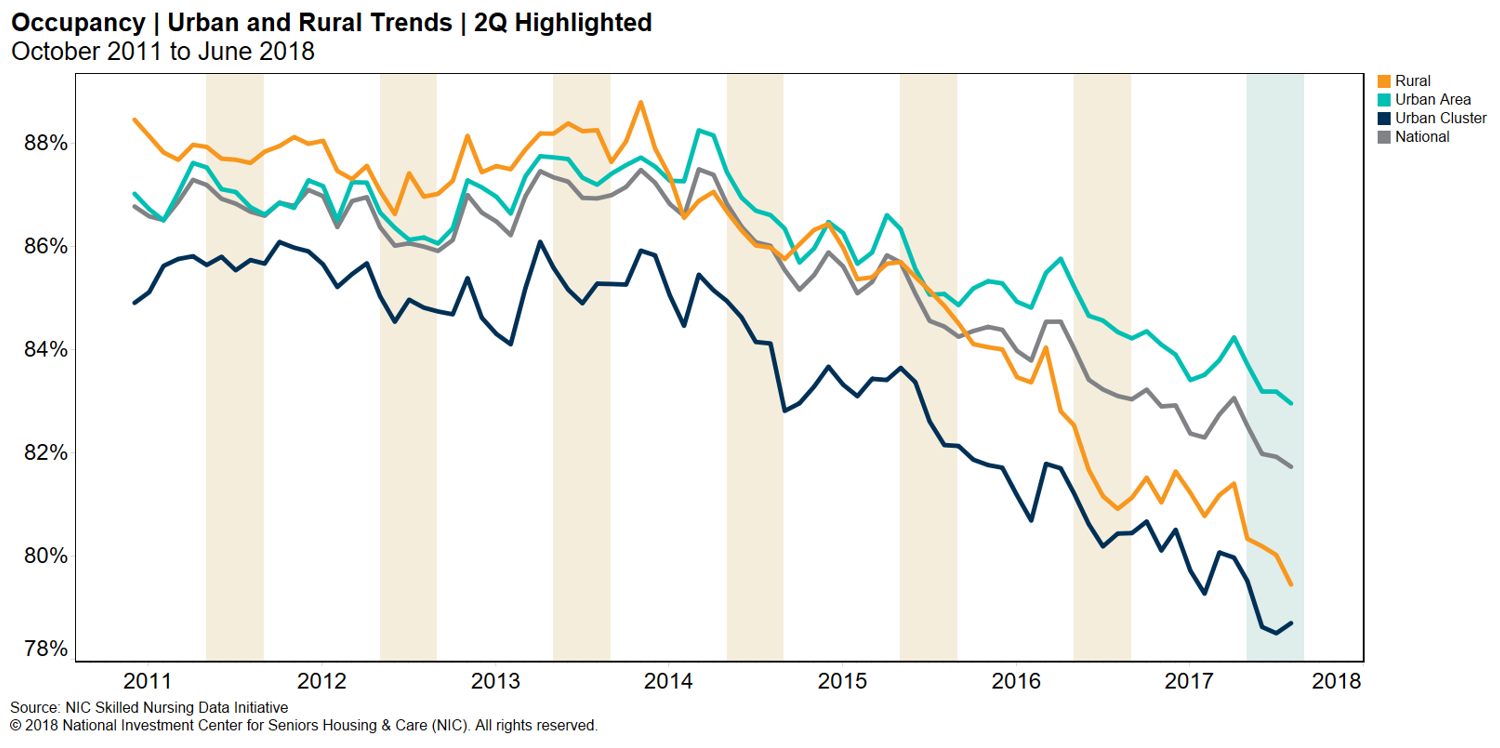

One of the reasons NIC started the Skilled Nursing Data Initiative is to provide timely, accurate and consistent data. The timeliness aspect of the data is very important, especially in a world today where the skilled nursing sector is ever changing, so the latest quarterly trends are interesting to note. For example, let’s consider how occupancy continues to be pressured, as it is down quarter-over-quarter as of June 2018, and down from a year ago when compared to June 2017.

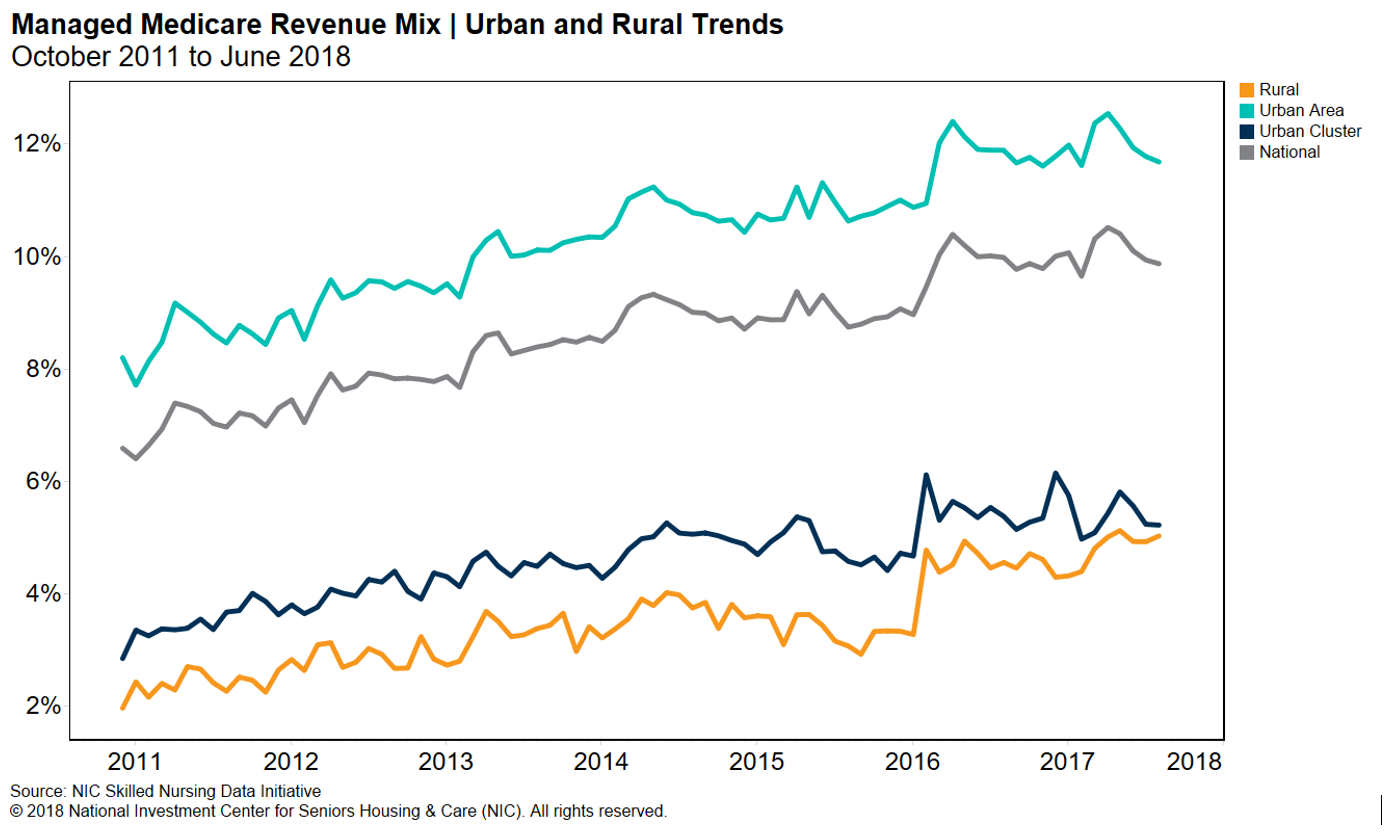

Another factor to consider is how the fundamentals of different geographic areas change over time and exhibit different trends. For example, take a look at the urban versus rural managed Medicare revenue mix trends exhibit below. You’ll notice how the urban area has trended up to the 12% range over the last few years, but the rural area has only reached to around 4%. Of course, Medicare Advantage has not penetrated as deep into rural areas, hence the 4% revenue mix level, but the point is that the economics of the business can be very different in certain areas/locations. Less managed Medicare penetration into rural areas is one of the reasons why the weighted average reimbursement rate among the four main payer types in rural areas has been essentially flat. That is much different than the 3.73% decline in urban areas.

All that said, it is also essential to take a step back and think about the big picture and the long-term trends. And the big picture right now is that given the pressures on the sector in general (keep in mind all local markets can vary), from policy changes and the changing dynamics of a continued move to a value-based healthcare system, we have seen a supply and demand imbalance in terms of patient days. In other words, the sector over the last few years has had an oversupply of patient days available when compared to the demand for those days. And most of that oversupply has been on the Medicare side of the business. Until the supply and demand come back into balance you could see continued pressure in the short-term before an increase in occupancy occurs. Now when will that happen? Hard to tell because of all the moving pieces, and now you have another dynamic coming into play with a new payment model from Centers for Medicare and Medicaid Services (CMS), the Patient Driven Payment Model (PDPM), starting October 1, 2019. However, one could argue this model may be positive for the industry because of aspects like new rules for group therapy and even potential consolidation as smaller operators may elect to sell instead of going through another CMS payment transformation.

And just another note on occupancy, the occupancy metric in the skilled nursing sector is not the “be-all and end-all” of measures. It is important, but one has to consider the full picture when evaluating the business, especially with individual properties and/or markets. For example, it may be very possible to run a property at 80% occupancy if you have mostly skilled mix with higher reimbursement rates and a good operator in place. It may be another story if you are running at 85% Medicaid patient day mix.

So what will the future hold?

Let’s be very clear that there are numerous pressures on the skilled nursing sector. However, if history is any guide, the future in 10 years will look much different than today. When drilling down on the supply- and-demand big picture conversation, one cannot exclude the aging demographics and the need in the future to care for a massive elderly population. The headwinds with demand may turn into tailwinds as the population needing care in skilled nursing properties expands. This population, which is a subset of the aging demographic, will be very sick and unable to live in their primary residence because of the complexity of care needed and no matter how much advanced technology comes into play.

Any way you look at it, the growing higher-acuity population will have to go somewhere for long-term care, and maybe it is not the skilled nursing property, but it certainly could be. As of today, there will continue to be a significant number of elders who will not have the ability to pay for long-term care and will be too sick to stay in their current homes. In addition, there is a segment of the population that won’t even have a home to where they could bring in-home care, and no family to help them. Then add in the factor of medical advances that could help most sick people live longer, but who would still need long-term care and maybe for a very long time. Where are they going to be cared for?

Not to mention, relative to the demand side, a shift by operators to care for higher-acuity patients could take market share from the long-term acute care hospitals. That might also be a positive.

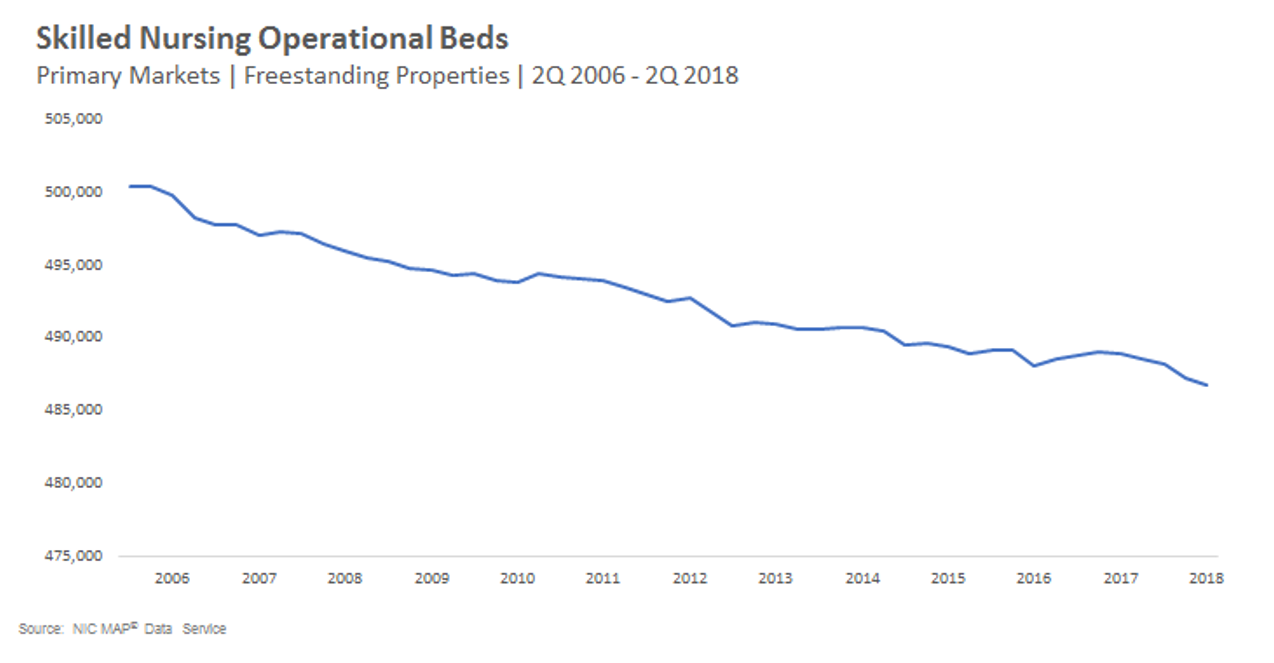

On the supply side of the equation, which is rarely discussed these days, there continues to be an interesting story playing out. Total operational beds continue to decline. If you look at the line graph below you will see an example of this in the primary markets over many years.

Given the supply-side equation, one could argue that this is another positive for the sector in the long term resulting from the decline in operational beds and the fact that there are high barriers to entry in most markets and states throughout the country, due to certificate of need (CON) and bed moratorium regulations.

Looking ahead, there are plenty of risks from the operator’s and investor’s perspectives. But there are certainly ways to mitigate the risks of future failure, whether it is increasing your ability for care collaboration across the continuum, including running your own managed care program, or venturing and/or expanding into ancillary services. One of the most likely routes to future success is making sure you are the best operator in your markets, in terms of delivering quality care at a lower cost and having the ability to handle lower lengths of stay, especially if you are moving toward a majority skilled mix business model.

The NIC Skilled Nursing Data Report is available here. There is no charge for this report.

The report provides aggregate data at the national level from a sampling of skilled nursing operators with multiple properties in the U.S. NIC continues to grow its database of participating operators in order to provide data at localized levels in the future. Operators who are interested in participating can complete a participation form. NIC maintains strict confidentiality of all data it receives.

Featured Article in Upcoming Seniors Housing & Care Journal 2018 Focuses on Partners in Care in Assisted Living

Relations between family and staff can be strained and conflictual rather than cooperative in elder care communities, leading to stress for both groups. To date, few programs have addressed the need for improved communication between staff members and relatives of residents in assisted living communities. Partners in Care in Assisted Living (PICAL) is a novel intervention designed to improve communication and cooperation among families and staff, with the goal of making them better “partners in care” for assisted living residents.

This program is the subject of the article selected as the outstanding research article by the editors of the Seniors Housing & Care Journal 2018, which will be released Wednesday, October 17 at the 2018 NIC Fall Conference. The research article, Partners in Care in Assisted Living: Fostering Cooperative Communication Between Families and Staff, authored by Pillemer, Schultz, Cope, Meador, & Henderson, describes an intervention to improve communication between families of assisted living residents and staff. The program, Partners in Care in Assisted Living (PICAL), provides training in communication, including active listening skills, types of feedback, and guidelines for handling disagreements. A randomized controlled trial showed that for staff, frequency of conflicts with family members and scores on burnout and depression scales declined among those in the intervention group.

The 2018 Seniors Housing & Care Journal offers peer-reviewed research articles and commentaries with a strong focus on applied research and best practices in the fields of seniors housing and long-term care. The Journal continues to feature topics most relevant for seniors housing providers and investors, with emphases on asset transparency, leadership development and talent selection, availability and affordability of seniors housing, and quality outcomes.

A second article, Employee Total Motivation (ToMo), by Paris, Howell, & Smith, was awarded special recognition by the Journal’s editors. The authors examine the relationship between employee motivation, employee satisfaction, and resident satisfaction, finding a positive correlation between all three. Moreover, employees with the highest total motivation scores are more likely to recommend their community and are more likely to be satisfied with their working conditions and jobs overall. The study further suggests that communities with the most motivated employees have the most satisfied residents. These findings underscore how important it is for owners and operators to understand and encourage factors motivating staff.

In addition to the seven research articles in the 2018 edition of the Journal, five commentaries offer new insights into important issues in seniors housing and care. If you would like to submit a proposal for an article for publication in next year’s 2019 edition of the Journal, please direct your e-mail to Associate Managing Editor Dugan O’Connor.

2018 NIC Talks: How Am I Changing the Future of Aging?

Fall Conference NIC Talks Speakers

At the 2018 NIC Fall Conference, the highly popular NIC Talks series returns with eight speakers, representing outside experts and an industry leader, who will all address the theme of “How am I Changing the Future of Aging?” These 12-minute TED-style talks are designed to be insightful as well as thought provoking and perhaps challenge people’s perspectives on the future of aging. Over August and September, we highlighted six of this year’s speakers in the NIC Insider. This month, we introduce you to the remaining two upcoming NIC Talks speakers. Next month, of course, you’ll be able to attend NIC Talks in person at the 2018 NIC Fall Conference in Chicago.

Bret Kinsella

The Power of Voice

Hundreds of millions of consumers are accessing voice technology through smart phones, PCs, and household appliances. Driven by advances in artificial intelligence and computing power as well as demand, the voice era is already upon us. Bret Kinsella, founder, editor, and research director of Voicebot.ai, which has become the central source of voice industry data, research reports, and expert commentary, is uniquely qualified to understand this new technology–and where it is headed. He will share his insights on the rise of voice in our culture and discuss how emerging devices and use cases will impact all of us, with a special focus on elder lifestyles.

Yoky Matsuoka

Thoughtful Technology and How it can Build Homes That Take Care of People

Yoky Matsuoka, chief technology officer at Nest Labs and a thought leader in smart technology, shares what the integrated home of the near-future will look and feel like. She’ll talk about the challenges of building technology that seamlessly blends into people’s lives, and how ongoing research into usage helps her company continue to provide products that improve aging in place.

To learn more about the NIC Talks scheduled for the NIC Fall Conference, visit the website.

Peer-to-Peer Salons: Facilitated Discussion to Engage, Enlighten, and Inform

by Jessica Pearce, Program and Professional Development Manager, NIC

Outside of the stellar networking opportunities provided by the NIC Fall Conference, the event also provides impactful educational opportunities for attendees. We encourage you to review the session lineup for the 2018 Fall Conference, and we invite you to attend the breakout sessions on timely topics presented by industry thought leaders and including the latest trends identified by NIC MAP® data. Premiering at this conference are the Peer-to-Peer Salons. These salons provide a forum for an exchange of ideas to address specific current hot topics with your fellow industry practitioners.

Why Peer-to-Peer Salons?

Engaging learning experiences for participants are an important component of the 2018 NIC Fall Conference. While panel dialogues provide a wealth of information, the peer discussion salons allow participants to communicate with fellow industry professionals who face similar issues. Exchanging shared experiences and exploring prospective solutions with peers offer salon participants the opportunity to discover best practices that they could deploy in their own businesses.

Timely topics and sharing experiences

These timely topical discussions will be facilitated by Lisa Spinali, a professional facilitator who helps build cross-sector solutions to ensure the discussion will prove enlightening for participants. This unique learning forum allows participants to share and potentially debate their own viewpoints with fellow participants to give shape and color to the discussion topics.

This year, we are addressing three major topics impacting the industry: the labor market, penetration rates, and market underwriting.

The question we are presenting during the salon on the labor market will be: How can we navigate the challenges of the tight labor market? During this facilitated discussion, participants are encouraged to share insights with fellow peers to gain perspective on how labor challenges are being managed by senior living housing operators and investors. This discussion will take place on Thursday, October 18 from 9:45 am to 11:00 am.

Our second salon topic on Thursday will focus on penetration rates. The question presented will be: What opportunities exist to increase penetration rates across senior care properties? The discussion will brainstorm possibilities on how senior living properties and the sector as a whole can attract a larger share of the targeted senior population as residents. It’s hoped that participants will leave this salon with a better understanding of what products and services can be offered to appeal to prospective residents and what can distinguish individual properties’ product offering from the competition. This discussion will take place from 11:15 am to 12:30 pm that same Thursday.

The final salon will focus on market underwriting. The question to engage its attendees will be: Given current market conditions, how do we underwrite markets for investment? Participants will exchange viewpoints on factors that are used to assess market demand and supply potential. This discussion will take place from 2:30 pm to 3:45 pm that Thursday afternoon.

Overall, the Peer-to-Peer Salons are designed to engage participants for their expertise and insights in order that they learn from each other. Participating in these innovative sessions will provide perspectives on how fellow industry professionals are tackling critical issues in today’s marketplace. We hope that these sessions will provide ideas, prospective solutions, and discussion topics that can be carried back to your respective businesses.

To learn more about the Peer-to-Peer Salons, please visit the NIC Fall Conference website.

Why There’s a NIC Spring Conference – and Why You Should Go

When the first NIC conference took place back in 1991, it was to serve the same mission NIC has today: to improve housing and care access and choice for America’s seniors. The event was designed to bring together capital providers and operators, some of whom didn’t yet understand why they should be talking to each other. NIC saw then, as it does now, that to make a real difference, it would have to inform investors and facilitate the business relationships that drive growth.

Over the years, the NIC Fall Conference has not only served to grow businesses but has become a focal point for the industry, a means to share hard-earned insights and shed light on the new ideas that will continue to move the sector forward. Today it is a must-go pilgrimage for many of the industry’s key players, consistently delivering the most efficient and effective means for capital and operators to connect. Last year’s Fall Conference drew over 3,000 senior decision-makers from across the sector.

But the sector is about to weather major disruption.

Several factors are acting on seniors housing and care today, all of which will likely drive monumental change in the near future. Our healthcare system is moving from a fee-for-service payment and delivery model to a value-based system. Policy is shifting to place risk on providers and to reward improved outcomes achieved at lower total cost of care. A new generation of seniors is living longer, will need and demand more effective and coordinated care delivery, and has a different view of what it means to live well as they age. Workforce challenges will help to drive adoption of revolutionary new technologies, many of which are finding a place in housing and care settings already. Players in other healthcare silos and payors, some of whom may not have been interested in sitting down with our sector before, are beginning to take an active interest in settings where several million frail seniors with multiple chronic conditions and functional needs live. There is a lot to consider for anyone who hopes to navigate the challenges and opportunities presented by these and other changes at play today.

New partnerships emerging

Navigating disruptive change, therefore, is the focus of NIC’s Spring Conference. It has been carefully designed to facilitate the new kinds of partnerships that will break down old silos, create new efficiencies, and improve outcomes, as well as to shed light on the innovations and solutions that will propel the industry into the future. What really sets the event apart is that NIC is actively encouraging conference attendance over time by health systems, physician-led organizations, and managed care plans and payors, as well as home health, home care and hospice companies, together with their investors, who have an active interest in understanding the opportunities in senior care collaboration–but may never have done so before. In addition to high quality networking, the event will focus on the collaborations that are being formed right now, as well as on financial, operational, and technological innovations that are already making a difference.

Along with challenges, there are also opportunities to thrive. Last year’s Spring Forum raised awareness of new ways to come to the table, often with new partners, in a move towards vertical integration, sharing of risk and savings, growing revenue streams, solidifying market position and more. New technologies were discussed, including new approaches to value-based care, and new ways of thinking about workforce retention and staffing challenges. It has become clear that to succeed the sector will need to collaborate with partners providing a range of healthcare services. To remove any doubt about the event’s focus, we’ve renamed it this year: 2019 NIC Spring Conference: Investing in Seniors Housing and Healthcare Collaboration.

Whether you are an investor, owner, operator, provider, or other stakeholder, business as usual is no longer an option. This goes for the rest of the healthcare system as well. One key role of the NIC Spring Conference is to connect seniors housing and care decision-makers to potential partners in a variety of healthcare sectors, both upstream and downstream. Post-acute, home health, physician groups, hospital systems, managed care plans, and a host of other players are interested in partnering for mutual success – and to achieve the laudable goal of delivering improved outcomes at a lower cost of care.

In broad terms, providers and payors are already moving towards a model in which healthcare comes to the seniors where they live, rather than the reverse. A “heads in beds” view, in which operators’ financial well-being depends chiefly on occupancy within a disconnected silo, will be disrupted by a system in which healthcare outcomes are measured, evaluated, and factored into payment for players across the system–including seniors housing and care providers.

Investors, debt providers, payors, and upstream partners will want to know where the seniors housing and care sector is heading, with whom they’re partnering, and how they are addressing the coming challenges. They will value the insights and innovations that will differentiate one operator from the next. Anyone with a stake should pay attention to how industry leaders are shaping their businesses, in order to anticipate valuations, strategic partnerships, acquisition strategies, and other factors that will affect investment risk and returns.

Continued growth demands change

NIC has never lost track of the mission that it serves. Our leadership recognized early on that perhaps the greatest challenge for us to overcome, if we were to achieve greater access and choice for our seniors, was the sector’s lack of transparency. Without the data and metrics that characterize top investment classes, seniors housing and care was deemed a significant risk by investors. Capital was expensive and hard to come by. Addressing that obstacle would take a major effort, involving years of data collection, millions of dollars in investment, and the focused efforts of a dedicated staff of analysts and researchers here at NIC.

The Fall Conference, while always a valuable asset for the industry, is also a means for NIC to win support, encourage operators to trust us with their data, and, not incidentally, to help fund the research and educational activities we know the sector needs. Today, seniors housing and care is viewed as an attractive commercial property type by institutional investors–an achievement that would have been impossible without years of time-series data, analysis, and the kind of trust in delivering results that can only be built over time. Ultimately, our seniors benefit from greater choice in housing and care as a result.

Armed today with decades of research and data, long-standing and trusted relationships within the industry, and the perspective of having lived through major shifts in the industry, NIC believes the sector is about to weather disruption that cannot be ignored. Our reaction today, as it was in 1991, is both to provide a forum for the industry to form the partnerships it needs and to work hard in the background to build the data that is so crucial to the availability and affordability of the capital that continued growth will demand.

The depth of change that is approaching is likely to generate winners and losers. The seniors housing and care sector has weathered many changes, resulting in a wide range of outcomes, from bankruptcies to attracting global institutional investment and outperforming other major commercial property types consistently over the last decade. The Spring Conference is designed to help it adapt to the disruptive changes that are coming and to better serve America’s elders both in terms of choice and access in the years ahead. We look forward to seeing you there.

The 2019 NIC Spring Conference: Investing in Seniors Housing and Healthcare Collaboration will occur in San Diego, California, February 20-22, 2019. Look for information and booking details on our website, in emails, and online in the coming weeks.

Rising Labor Costs Impact Income, Valuations

Andrew Lavinder

by Andrew Lavinder, Vice President, Real Estate, MidCap Financial Services, LLC.

The rising cost of labor for caregivers is primarily driven by the strength of the economy and pressure from state and federal legislatures to increase the minimum wage. There have been more job openings than hires since 2015 according to data from the Bureau of Labor Statistics. This has caused the unemployment rate to shrink to 3.9% as of August and put upward pressure on wage rates. Additionally, the number of “quits,” which can serve as a measure of workers’ willingness or ability to leave their jobs, has passed pre-recession highs and appears to be at an all-time high.

The seniors housing industry is not the only industry feeling the pressures of the tight labor market. Many companies throughout the U.S. economy have increased hourly wages to attract new workers. Target, for example, said last week that it plans to hire 120,000 seasonal workers, 20% more than last year, and pay a starting wage of $12 an hour. The increase is part of Target’s plan to raise its minimum hourly wage to $15 by 2020. Other companies, such as Wal-Mart, Walgreen’s, and FedEx, have followed suit, as they compete for workers in a tight labor market. In FedEx’s most recent earnings release, it said higher hourly wages had a $170 million impact on results or $0.48 per diluted share.

In addition to market forces, there is growing pressure from state and federal lawmakers to increase the minimum wage. The drive to prop up the minimum wage is most prominent in coastal states and major cities such Los Angeles, San Francisco, Chicago, and New York. In California, for example, the minimum wage is set to increase by $1/hour in each of the next five years, going from $11/hour on January 1, 2019 to $15/hour by January 1, 2023. The increase will likely have a direct impact on the cost of caregivers given the average hourly rate of CNAs in California is about $14 per hour and the work is demanding. However, an increase in the minimum wage not only increases wages for workers below the minimum wage, but it also increases wages for workers slightly above the minimum wage. The larger impact being known as the ripple effect.

It is important for market participants to understand the dynamics affecting the cost of labor given that labor-related expenses comprise the largest component of expenses for senior care communities. On average, labor costs at independent living facilities represent 35%-45% of operating expenses, whereas labor costs at assisted living facilities represent 53%-57% of operating expenses.1 Moreover, caregivers typically comprise a majority of the labor costs and can account for 50+% of all labor-related costs depending on the acuity of residents in the building.

According to the NIC MAP® Data Service and the Bureau of Labor Statistics, the average hourly earnings of an assisted living worker is increasing over 5% per year, while same store rent growth is only increasing 2.5% per year. That trend does not bode well for future profit margins. As a hypothetical example, consider a 100-bed assisted living facility that employs an average of 10 CNAs per hour. If the average hourly wage of caregivers increases by $1/hr per year (~7% of a $14/hr CNA wage), it would decrease NOI by about $90K per year, all else being equal. That would equate to a reduction in value of around $1.1 million assuming a cap rate of 8.0%. As can be seen in the example, rising labor costs can quickly change the economics of a transaction if rent or occupancy growth doesn’t keep pace.

The current oversupply of properties in some markets further exacerbates the issue as many properties do not have the pricing power needed to pass thru cost increases. Moreover, the abundance of new supply makes it harder for existing facilities to retain staff as new facilities often offer higher wages to recruit staff from other properties. Buildings that compete on price may be more vulnerable to the effects of higher labor costs, given it is harder for these properties to raise rates and they often run at lower starting margins. Whereas properties that compete on value may be better suited to pass price increases through to their residents. The good news is that wage and labor pressures are typically indicative of a robust economy that can absorb higher prices. However, that is not always the case, and market participants should strongly consider the effect of rising caregiver costs and labor-related expenses when making investment decisions.

1 ASHA/ALFA (Argentum)/LeadingAge/NCAL/NIC, The State of Seniors Housing 2017. This report provides data on financial and performance measures, including operating expenses and other key financial performance metrics. The data is pulled from the 2017 edition, which summarizes data for 2016.