How a Big Equity Investor Navigates a Tricky Market: A Conversation with Samira Madhany of The Carlyle Group

Samira Madhany

Samira Madhany is clear and direct in her appraisal of the opportunities and challenges that lie ahead for the seniors housing industry. As Principal at The Carlyle Group, Madhany seeks out new properties for investment across the country from the equity giant’s headquarters in Washington, D.C.

Listen to Madhany speak and it’s apparent that her keen insights of the sector are based on her experience with a large portfolio over a number of business cycles. That experience also guides today’s investment decisions.

NIC Chief Economist Beth Mace recently spoke with Madhany who detailed Carlyle’s strategy and offered her observations on the next stage for seniors housing. Here are some excerpts of their conversation.

Mace: Tell us about The Carlyle Group and your role there.

Madhany: The Carlyle Group is a global alternative asset manager with $195 billion of assets under management. I joined Carlyle’s U.S. Real Estate team in August 2006. We’re focused on opportunistic and core-plus investments in major metro markets in the residential, hotel, industrial, office and retail sectors. I began working on our senior housing investments in 2007, and today I’m responsible for sourcing new opportunities to invest in across the country.

Mace: How long has Carlyle been investing in the seniors housing and care sector?

Madhany: We have been investing in seniors housing for more than 15 years, and we have acquired or developed 16,000 units in 100 communities with a total capitalization of about $4 billion. Our seniors housing properties are held in our opportunity fund and our core-plus fund. We don’t have a standalone seniors housing fund. We are currently investing our eighth opportunity fund and an open-ended core plus fund.

Mace: Why did Carlyle enter the sector? What changes have you seen in the sector over the last decade?

Madhany: When we first entered the sector, we spent a considerable amount of time researching the landscape and the fundamentals of seniors housing. At that time, the fundamentals were quite strong. We had positive demographic trends in a targeted age cohort; new supply was decelerating from its peak in the late ’90s; demand was expected to exceed supply by a factor of two to three times; and occupancy was projected to reach 90 percent.

The industry was then and continues today to be highly fragmented. The top 50 owners control less than 35 percent of the units. And historically, the sector has attracted local developers, and owners and operators. Many of these owner/operators were not well capitalized to be able to continuously reinvest in communities and enhance the residents’ experience. We saw an opportunity to invest in a sector where: 1) fundamentals were moving in the right direction, 2) more institutional capital was needed to provide a more high quality experience for residents in a best-in-class community, 3) there was a unique resilience compared to other real estate types given its combination of real estate, hospitality and needs-driven services.

Fast forward to today, and the long-term fundamentals in seniors housing are quite strong. The age 65-plus population is expected to grow from 40 million to 72 million by 2030—an impressive 80 percent cumulative growth in that age cohort. Product acceptance, renters by choice, and penetration rates are continuing to increase, and the sector is still relatively fragmented and undercapitalized. So many of the reasons why we entered the sector still apply 15 years later.

Mace: What challenges do you see for the sector, both in the near- and long-term?

Madhany: We believe there is still an opportunity to invest in the sector, which has positive long-term fundamentals. We can create something unique both in the way of the quality of the product and the level of service we offer to our residents to allow them to age in place with comfort, dignity and respect. We could not do this without the partnerships we create with our operators.

On the flip side, seniors housing at its core is an operating business and with that comes the day-to-day challenges of providing exceptional care and services to our older generation. When we are caring for people, we have found that our greatest assets are the individuals that provide the touch points day in and day out.

Wage pressures and employee retention issues make it more difficult to keep the best talent. We have to think outside the box to maintain that edge in order to focus on the resident experience.

We have all seen the headlines. There has been a tremendous amount of development in the assisted living and memory care sectors. That new supply has and will continue to impact occupancies and rates, especially over the next two to three years as demand remains temporarily tepid until baby boomers seek out traditional needs-based senior housing.

Long term, affordability will need to be addressed, and groups that can figure out that equation will have an advantage over others.

Mace: What property types do you invest in?

Madhany: Carlyle will acquire or develop everything from a community that offers housing to a resident who is age 55 or over to one that offers services and care, including assisted living, independent living, and memory care. We like to provide the full continuum of care so residents can age in place. For this reason, we have not invested in stand-alone memory care communities. While we are national in scope, we do seek opportunities in markets with positive demographic trends and limited supply coming online. We do not invest in skilled nursing or entrance fee continuing care communities.

Mace: Do you provide equity for repositionings, expansions, acquisitions, and new development?

Madhany: Yes, we provide equity for all of the above.

Mace: What do you look for in a property?

Madhany: When we look at a community, we ask ourselves several questions: What are the supply/demand fundamentals of the market, and more specifically, of the primary market area? Are there any limitations to the physical plant that would render it obsolete or make it challenging to lease and operate? Can we align ourselves with a best-in-class operator to improve resident experience and optimize the unit mix?

Mace: What about ground up development?

Madhany: Every market has pockets of growth, and we continue to do ground up development in these submarkets. But we develop selectively and pay close attention to the fundamentals, developer, operator, and the physical design of the building. We think it is important to have the right number of units, the right unit mix, and a “Class A” design.

Mace: How does Carlyle find operators? Why should an operator work with Carlyle?

Madhany: Finding a best-in-class regional operator is a challenge we continue to face. Today we have relationships with more than 10 different operators on our existing portfolio and have worked with several others in the past. Selecting a regional operator that can develop and execute our vision for a community is based on the location of the asset, the unit mix, and the business plan.

Our operators and joint venture partners are critical in executing our business plan. This is a business made of people, and it is the people that determine resident and family satisfaction at every community. We have worked with both small and large organizations. We continue to seek out new partners and operators to work with and look for organizations that have strong leadership with breadth and depth of experience in the sector and a passion to truly care for and provide a community for residents and their families.

Mace: What’s the advantage for an operator to work with Carlyle?

Madhany: Our team holds itself accountable for the quality of the community and service we deliver to our residents and their families. We are collaborative, flexible and hands on, and we try to be creative. Operators take comfort in knowing we are alongside them as they make decisions that impact the community. We do more than simply check in periodically on the performance of a community. We also have the benefit of relying on our operating history and portfolio of assets to be able to say this is what has worked at other communities and here’s what might work at another property.

Mace: When do you turn down a deal? What are the red flags?

Madhany: It’s difficult for us to get comfortable with primary markets that have weak fundamentals, where occupancy is low and concessions are prevalent, and there’s little year-over-year rent growth. Other red flags are physical limitations that can’t be changed or are cost prohibitive to change. Also, too many units in the community can impact the level and quality of service. Large units can impact affordability. Finally, I cannot emphasize enough the value of our team and the partnership we create with our operator. If we cannot garner the support of an experienced team, we would likely pass on the deal.

Debriefing the 2018 NIC Spring Investment Forum Planning Committee Co-Chairs Highlight Key Moments

Torey Riso

James Thompson

NIC’s recent Spring Investment Forum was a success, drawing a record attendance of 1,800 industry stakeholders. They had the opportunity to network, explore partnership opportunities and attend 17 different educational sessions to bring them up to date on the latest industry trends.

The Forum would not have been possible without NIC’s volunteer leadership. A Planning Committee met for the better part of a year to determine the most relevant programming for seniors housing and care investors, owners, operators and service providers.

Special thanks goes to the Planning Committee Co-Chairs, Torey Riso, President and CEO of Blueprint Healthcare Real Estate Advisors; and James Thompson, Senior Director-Senior Housing and Healthcare Lending, Synovus Bank.

Both Riso and Thompson have donated a great deal of time, effort and expertise as long-time members of the planning process. Each brings a special perspective to the task. Riso’s experience is primarily on the investment side of the seniors housing business, while Thompson is a lender that focuses on the skilled nursing sector.

NIC recently talked to the co-chairs to get their takeaways from the Forum. Here is a recap of their impressions.

NIC: What is it like serving as co-chairs of the Spring Investment Forum Planning Committee?

Thompson: NIC has a unique process of combining a strong and committed staff with industry leaders and volunteers to plan and execute the conferences. As co-chairs, we help ensure that the general content is appropriate and that the committee make-up is highly competent and consistent with the ongoing Forum theme as it evolves. The volunteer chairs also help to prioritize session ideas and help ensure that the session leaders, speakers, and specific session content support the theme. The opportunity to discuss emerging trends that will impact our industry has been a rewarding experience.

Riso: There was one particularly important moment for me during my second year on the committee. I recall being one of approximately 25 committee members in a meeting thinking to myself: “Wow, this is a unique collection of extraordinarily smart and engaged people from across our space of seniors housing and care, and well beyond.” I saw people representing investors, banks/lenders, advisors, owners, operators, home health, technology, non-real estate based providers, for-profit and not-for-profit entities. For a moment, I felt like I had gone back in time to a hypothetical job on the planning committee meeting of the long-distance telephone communications business in the 1980s asking about how they should change their rate plans. What that group may not have realized was that the entire system would soon be turned on its head and long-distance rate plans would soon not exist.

Unlike my hypothetical long-distance planning committee, the NIC group knew that big changes were ahead. While they didn’t know exactly what the changes would be or how quickly they would arrive, we all knew change “is a comin’.”

Being on the Forum Planning Committee invites us to ask relevant questions of stakeholders in a number of impacted sectors about the unknown, listen to the ideas generated, and then shape helpful future questions, and, along the way, seek a few answers.

NIC: Can you share your perspective on what NIC Forum Planning Committee members get from the experience?

Riso: As I mentioned, our participation provides an opportunity for an exchange of ideas among people from the seniors housing and care space with those of related sectors that haven’t traditionally engaged with each other. The ideas discussed and exchanged will be at the forefront of the industry as it changes over the next many years. As an added plus, it provides the ability for industry leaders to form lasting relationships among similarly situated thought leaders.

Thompson: The Planning Committee is a diverse group of highly competent, experienced individuals who work in a variety of post-acute organizations, including private pay seniors housing. As our Forum content has expanded well beyond the traditional real estate owner/operator/capital provider, so has our committee. Almost without exception, the participants say that they value the discussions that occur during the planning process as well as the relationships that begin or expand as a result of committee participation.

NIC: What are your three main takeaways from the 2018 Spring Investment Forum?

Riso:

- The seniors housing and care industry as it is, and has been, is changing.

- Changes are going to impact my business and my sector.

- There are ways to prepare for and get ahead of it. Just waking up and doing what you’ve done for the past 25 years is not enough.

Thompson:

- Skilled nursing providers can see a path to profitably meeting the care needs of their patients even though the industry is currently facing both operational challenges as well as headline risk.

- The industry has a sense—as investor Arnie Whitman put it during the opening plenary session—that it is time for the industry to leave the “kid’s table.” The industry has a prominent and cost-effective role to play in healthcare delivery to seniors.

- Given the large numbers of frail elderly in private pay seniors housing, providers are beginning to understand that they have a significant role to play in supporting, indirectly and directly, the health of their residents. The initial benefits will be improved length of stay or higher census derived from market differentiation and, later, by directly receiving payment for chronic care management or care coordination.

NIC: What was the Forum’s biggest success?

Riso: In my opinion, the biggest successes are having different groups come together to get educated and share ideas; providing an environment conducive to deal making; and allowing thought leaders from different sectors to forge deep and long lasting relationships.

Thompson: Networking has always been an important part of the NIC experience. Personally, I see the greatest success in the value that session attendees are realizing by learning about new trends coupled with strong traditional programming, both of which are leading to year-over-year growth in attendance.

NIC: What themes emerged during the Forum that will have a big impact on the industry? Any comment on the news that CMS may allow Medicare Advantage plans to cover “daily maintenance” types of care? NIC Blog

Riso: The potential changes that CMS may allow Medicare Advantage to cover certain types of care are consistent with the NIC’s hunch about the future of our industry. They brought people together to ask questions and lead the dialogue and that conversation continues today more than ever.

Thompson: CMS’ movement to allow MA plans to provide for preventive and early intervention services will allow skilled nursing and seniors housing operators to get paid directly for many of the things they are already doing to improve outcomes and coordinate care transitions. A common complaint from skilled nursing operators over the last few years has been that they are not getting paid for success in value-based care.

NIC: Following up on the previous question, NIC seems to be ahead of the curve in addressing important new trends. Can you comment on the strategic thought leadership at NIC? What makes NIC different?

Riso: More important than trying to understand how we continue the success of our industry based on a backward look is to understand what possibilities lie ahead. That involves disruption to the status quo and the adoption of new ideas and processes. NIC has always wanted to foster those conversations among the best and brightest the industry has to offer. I applaud its resolve to make that happen.

Thompson: The direction and theme of the Forum over the last couple of years has come from the NIC Board. However, both the staff and Planning Committee are dedicated to providing great content and want the Forum to be “the place” to come to stay abreast of the new trends.

NIC: What themes do you expect to emerge at the 2019 Forum? How do these themes “continue the conversation” of the 2018 Forum?

Thompson: We are early in the planning process, but we will continue to reach out beyond the traditional capital provider/operator panel members. For example, the 2019 committee includes a prominent health system executive. Mostly, the programming will reflect an extension of the 2017/2018 theme because it is relevant. I would not be surprised to see new care models begin to emerge in response to payment methodology changes, technology, and, hopefully, a significant growth in skilled nursing and senior housing operators taking on risk. We plan to showcase more concrete examples of the variety of ways that skilled nursing and seniors housing can get reimbursed for the services they have been providing for the last several years.

Five Things Real Estate Owners and Investors Should Know about Healthcare That Will Impact the Bottom Line

A highlight of the 2018 NIC Spring Investment Forum in Dallas was a session that explained key changes in the healthcare system and why they are so important to traditional real estate investors.

The management of healthcare for elder residents and the payment process is a complex and quickly changing arena—one of the reasons it’s easy to let someone else handle the details. But session panelists provided a quick roadmap of the trends investors need to navigate to generate higher returns.

Here are five takeaways from the session.

- All residents served by your properties are covered by Medicare and possibly Medicaid—and this matters. Panel moderator Anne Tumlinson, of Anne Tumlinson Innovations, presented some eye-opening statistics. Medicare is a $600 billion program. About $120 billion of the Medicaid program is earmarked for elders who receive care in nursing homes, or through home and community-based services. Rising program costs are a big concern to the government, which is focused on getting more value for the dollars spent and slowing the growth of utilization. Also, 10 percent of Medicare beneficiaries account for 60 percent of the program dollars spent. Tumlinson cited research that shows that those 10 percent of beneficiaries have chronic conditions and also need help with the activities of daily living. “Elders living in your buildings are the most expensive part of the population,” said Tumlinson. Another important fact is that Medicare Advantage—insurance plans offered by private companies and approved by Medicare—is growing quickly. (Separately, the Centers for Medicare & Medicaid Services recently announced that it is considering allowing Medicare Advantage plans to pay for services related to the “daily maintenance” of residents.) Privately managed Medicaid programs are also growing quickly. These programs are impacting seniors housing and care residents, said Tumlinson.

- New payment models are emerging to help reduce healthcare costs which are already impacting the industry. Panelist Brian Fuller, of Great Lakes Caring and a national expert on value-based care, detailed the list of government programs and experiments underway to cut costs. There are many confusing terms and acronyms for these programs and the organizations that administer them. The critical thing to know is that these programs generally bundle payments to cover an episode of care and shift risk to the care provider, creating an incentive to seek low-cost care delivery settings. Why is that important? “Your buildings can be in the driver’s seat to coordinate services,” said Fuller.

- Building owners may have an opportunity to get paid for services they already provide but are not presently being paid for. Panelist Michael Monson, of Centene Corporation, a large private insurer that manages healthcare plans, including state Medicaid programs, discussed how building owners can help reduce costs by keeping residents out of the hospital. The building and the insurer would assume the risk for the care of the resident by being paid a set amount for care. If the resident is kept healthy and out of the hospital, the savings would be shared by the insurer and the building. Though these arrangements are still somewhat experimental, Monson said they are becoming more widely used. “You need to have an appetite and willingness to bear risk,” he said. “That’s the way it is going to go.”

- Seniors housing is the solution. Society has a problem, noted panelist Lynne Katzmann, president and CEO of Juniper Communities. Healthcare costs are growing rapidly, especially for the part of the population that resides in seniors housing. Katzmann was encouraged to hear that companies like Centene want to partner with operators. “It’s here,” she said. “They get it.” Juniper’s Connect4Life program is a good example. The high-tech, high-touch program integrates care for residents by providing primary care on site, offering ancillary services such as hospice, and assigning a medical navigator to each resident. Providers are connected by electronic health records. The program has increased the length of stay of residents by 12 percent. New care charges have helped to double daily rates in three years. The incidence of hospital readmissions was 80 percent lower than that of similar residents who live in the outside community. “If you were an insurance plan, you would want to work with us,” said Katzmann.

- Care coordination is the key. Commonwealth Senior Living, a regional provider in Virginia, set out to differentiate itself from other providers. The company had two goals, said panelist Richard Brewer, president and CEO at Commonwealth. The first goal was to work with local hospital systems to lower costs and avoid rehospitalizations of elders being discharged from the hospital. They achieved this by moving the patient into assisted living instead of sending them home or to a nursing home. The second goal was to educate the professional community about the benefits of senior living. “The challenge is getting the hospitals and health systems to understand what you are doing,” said Brewer. Commonwealth established a program that brings an elder discharged from the hospital to an assisted living setting for 15 days. Home health provides medical care. “We are not providing more care,” said Brewer. “But we are doing a better job of coordinating care.”

Here is a link to an audio recording of the entire session, “What Seniors Housing and Care Investors Need to Know about Healthcare and Why It’s Important.”

Senior Living – Welcome to the Major Leagues of Post-Acute

Allison Pendroy

In the words of Babe Ruth, “Yesterday’s home runs don’t win today’s game.” Certainly, that statement defines today’s evolving healthcare landscape, as long gone are the days of post-acute as an afterthought. To the contrary, today’s senior living providers find themselves in the midst of spring training, undergoing a redefinition of business practices to warm up for the opening of the season.

The Rules of the Game

Today’s value-based payment model is truly transforming the healthcare industry, all with a major goal of shoring up the long-term sustainability of the Medicare program. Given almost half of Medicare patients use post-acute care in some way following hospital discharge, the government has been gradually adjusting provider reimbursement for the cost and quality of services that occur beyond the inpatient setting. Health systems are held financially responsible for care delivered outside the acute setting—a change that cuts deep, and is modifying behaviors. In response, hospitals are on a quest for cost and quality improvement and seeking partners on the continuum of care chain that are reliable and dependable. Shorter stays and limited readmission rates improve the batting average for any player.

Drafting the Team Roster

Today’s value-based payment model is as much about what is happening outside hospital walls as it is about what’s taking place within the acute environs. Acute providers cannot do this alone and have begun drafting their teams. As such, seniors housing providers now can join the post-acute major leagues with a defined role to play—effectively providing a portal for healthcare entry from independent living, assisted living, memory care or skilled nursing.

As seniors housing now finds itself part of the line-up, business is changing, and providers need to be increasingly agile and capable of adapting to the rising acuity of residents who are coming our way. This will require attracting and retaining the right workforce equipped with the appropriate training and engagement, an understanding of how to analyze and apply data, marketing savvy, the development of expert relationship networking skills, and the establishment of “triage” mechanisms onsite to drive quality outcomes and avoid a return to hospital episodes.

Winning Strategies

Much like baseball teams spend time pre-game and in-game crafting pitching and fielding tactics, it is critical that a senior living provider develop and execute a conscious post-acute strategic plan. The first place to start is for an organization to assess its capabilities, determining what they do well and where competencies currently fall short. From there, it is important to identify necessary enhancements to address any shortcomings. At the same time, senior living providers need to be able to anticipate the needs of acute providers in their marketplace. Accessing area market data provides an understanding of the pain points of an acute organization, enabling an astute senior living provider to customize a specialty program (e.g., cardiac, orthopedic) that may help address acute provider problem spots. This approach can positively position the senior living community for ongoing active referrals and continued occupancy flow to the community. In this way, each senior living community is essentially like that batter on home plate, self-aware of his/her strengths and weaknesses, while assessing the likely form the pitch will take from the acute provider—all to make the right connection with the ball and land a home run.

Keeping Score

Data shouldn’t only be used to determine pain points, but data will also serve as the record for final runs from the game. Just as statistics are critical to the sport of baseball, data is everything when hospitals evaluate good partners. Senior living providers shouldn’t only seek routine access to marketplace discharge and readmission data, but also must be willing to analyze it, using it to align clinical practices and foster improved results. Use of data isn’t one and done. Instead, it should be put to work via an iterative process, consistently embraced as part of a continuous improvement loop.

A senior living community’s individual outcomes data should be overlaid against the hospital’s data to speak toward the value proposition. This data can be packaged into a robust marketing strategy capable of addressing multiple platforms for stakeholders including hospitals, managed care health plans, physician groups, and home health agencies.

Forming the Line Up

Building relationships takes time and persistence. It takes hard work, commitment, and active management. Is your organization prepared to go for the extra inning? Senior living providers cannot wait to be approached by acute providers but need to take the initiative to walk out onto the field and step up to home plate. While relationships can take many forms, becoming part of a post-acute alliance starts with building the right relationships with hospitals and health plans. Senior living providers must be deliberate in seeking the right introductions and take the compelling market message to the home turf of the hospital or health system. It is incumbent upon senior living providers to demonstrate with confidence something unique in their player abilities, along with special competitive advantages that the coach can’t find elsewhere and then campaign to join the post-acute continuum. Also, this cohesive marketing message should be consistently deployed across all platforms beyond the hospital, also including other occupancy referral sources and allies, such as managed care and physician practices.

The beneficiaries of continued resident referral flow will be those senior living providers best able to articulate the ability to meet the healthcare needs of the acute and managed care providers, along with demonstrated experience in mitigating risk and driving the right outcomes. Those who exude confidence in their abilities coupled with strong data that tells a positive story will get the most playing time. Blake Gillman, vice president/director post-acute services at LCS, sums it up best, “It’s very important to acute providers they seek patient placement where there is the least amount of risk and highest degree of the outcome, which will contribute to the most confidence they have in their post-acute partners.”

Let’s Play Ball

As senior living providers, let’s take advantage of the warm-up the spring training season provides to improve our skills and capabilities. We’ve been called up to the major leagues, and the healthcare game will never be the same. Just as baseball is a team sport, the present and future of post-acute care will require forming strong teams comprised of skilled players. Let’s play ball!

Five Key Takeaways From NIC MAP’s First-Quarter Seniors Housing Data Release

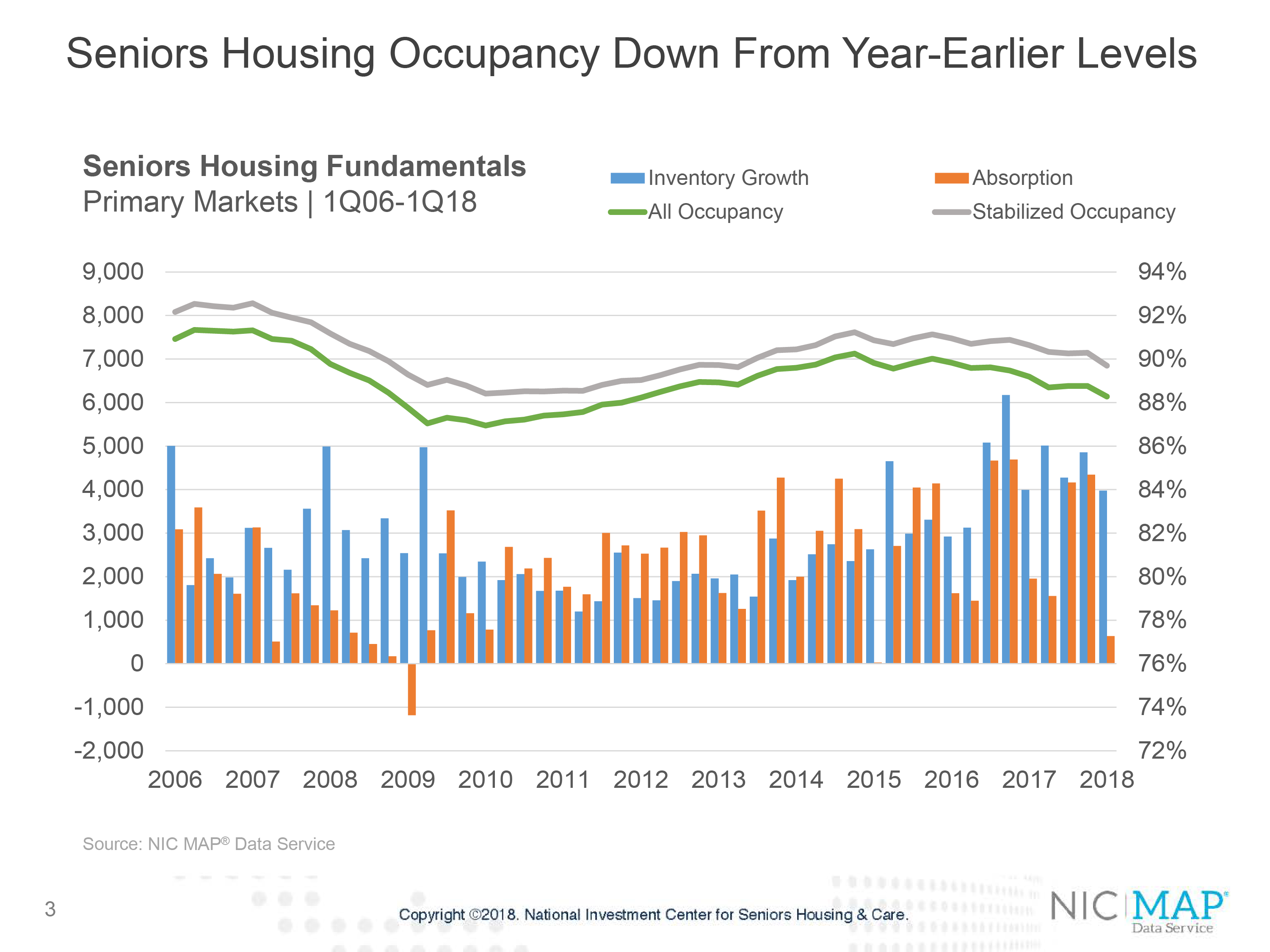

Seniors Housing Occupancy Declines, While Same-Store Rent Growth Decelerated in the First Quarter

NIC MAP® Data Service clients attended a webinar in mid-April on the key seniors housing data trends during the first quarter of 2018. Five key takeaways emerged:

- Seniors housing occupancy fell to a six-year low of 88.3%, while assisted living occupancy dropped to its lowest rate since NIC began reporting the data in 2006.

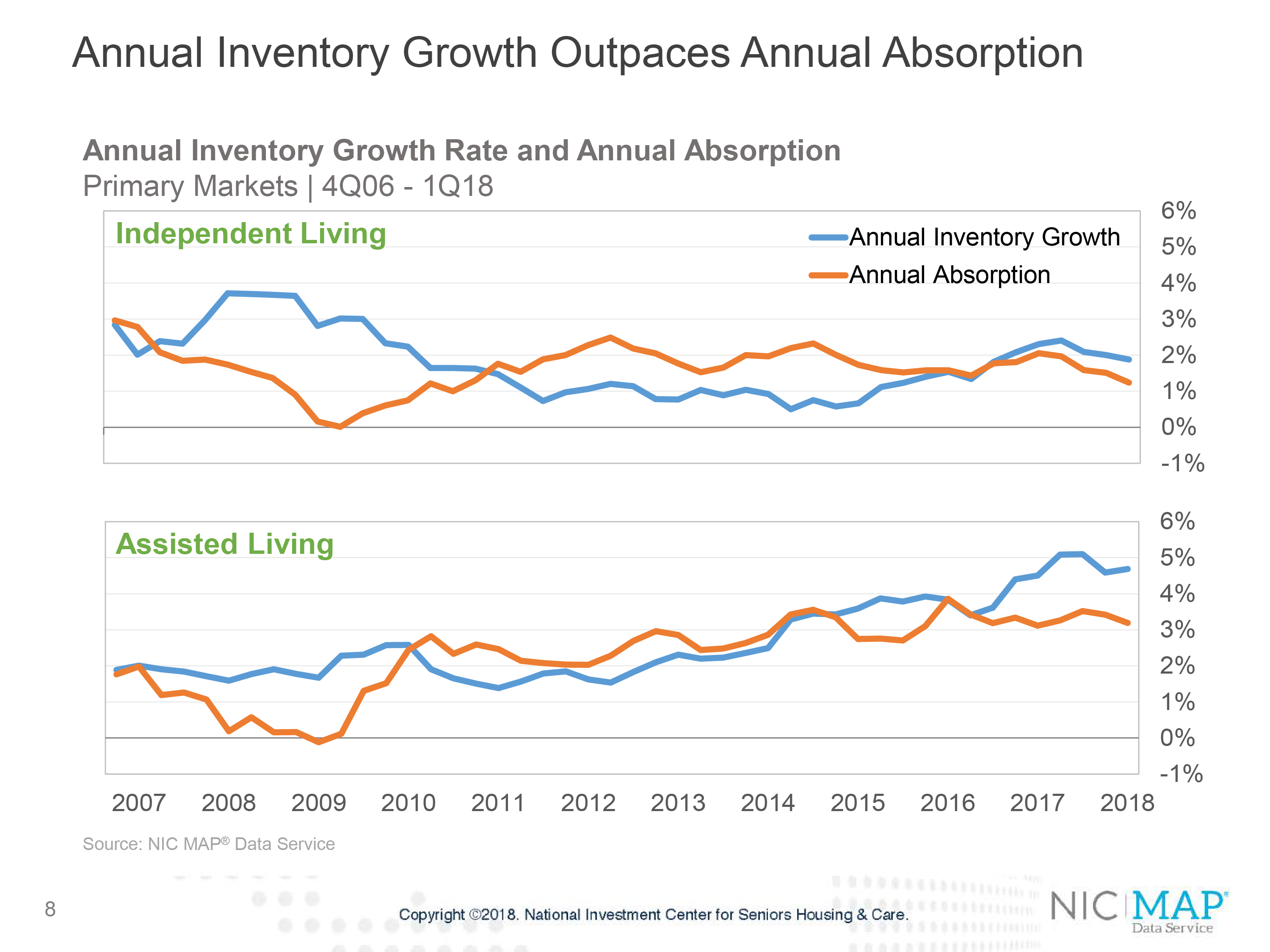

- Annual inventory growth outpaced annual absorption for both assisted living and independent living.

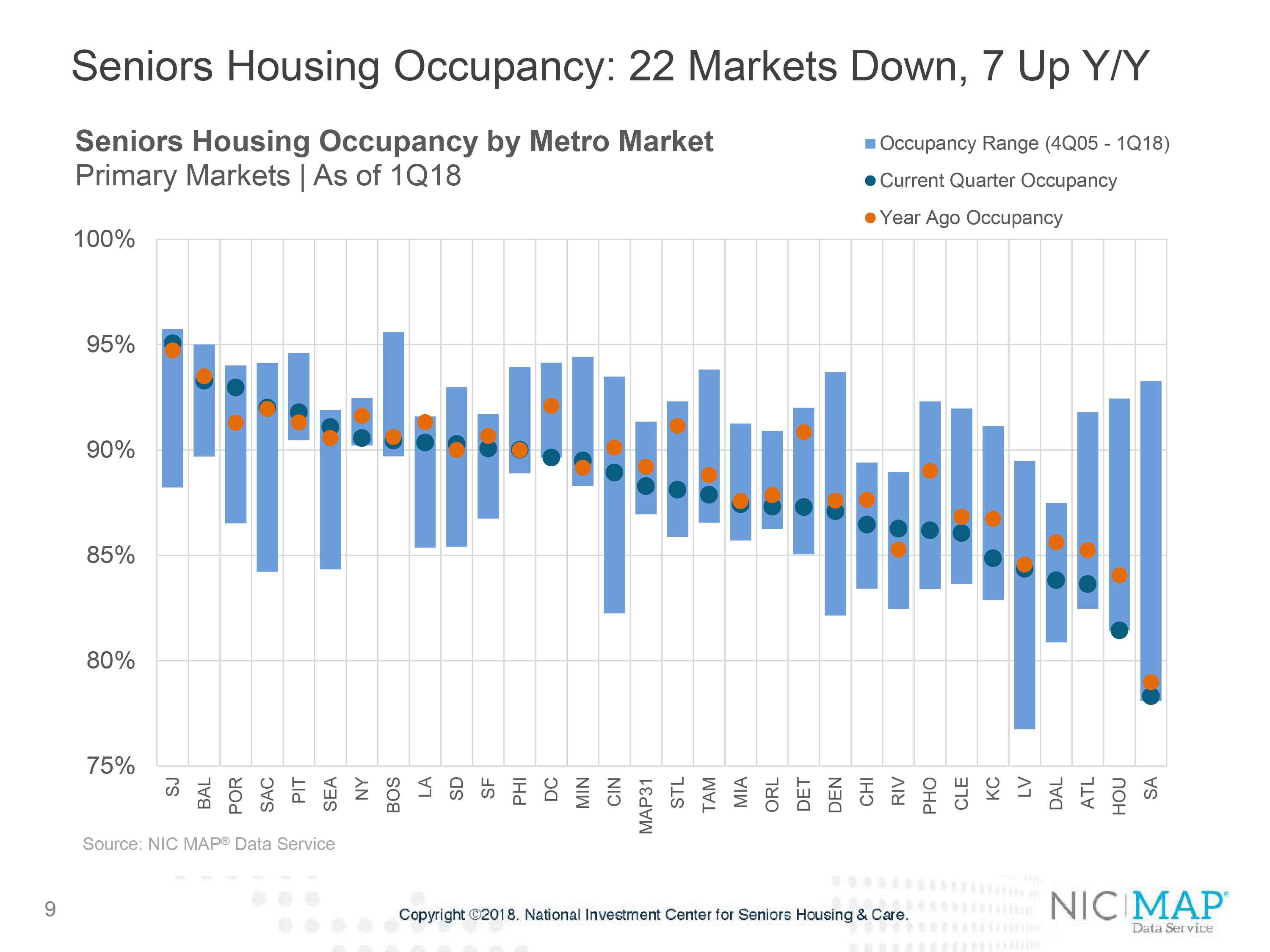

- Of the 31 Primary Markets, 22 metropolitan markets experienced lower occupancy rates compared with a year earlier, while 7 metropolitan markets saw higher rates and 2 were unchanged.

- Same-store rent growth decelerated.

- Closed transaction volume slowed in first quarter.

Let’s take a closer look at some of these trends.

Beth Mace

Seniors housing occupancy fell to 88.3%

The all occupancy rate for seniors housing, which includes properties still in lease up, was 88.3% in the first quarter, down 90 basis points from 89.2% in the first quarter of 2016 and down 50 basis points from the fourth quarter. This was the lowest occupancy rate in six years. This also placed occupancy 1.3 percentage points above its cyclical low of 87.0% reached during the first quarter of 2010 and 2.0 percentage point below its most recent high of 90.2% in the fourth quarter of 2014.

Assisted living occupancy fell to a record low rate of 85.7% in the first quarter. Net absorption totaled only 420 units, which was the fewest units absorbed on a net basis since the first quarter of 2015, while inventory growth slipped to 2,500 units, which was the weakest pace since the first quarter of 2016.

The quarterly decline in the overall occupancy rate stemmed from a marked slowdown in first quarter absorption as well as less inventory growth. Winter weather typically causes a slowdown in both inventory growth and demand in the first quarter. This year a particularly harsh flu season may have also slowed leasing activity as many properties lost marketing days due to flu-related property-level quarantines.

Annual inventory growth outpaced annual absorption for both assisted living and independent living

- Assisted living inventory growth has been ramping up for a longer period than independent living in the Primary Markets. In mid-2012, the occupancy rate of independent living was the same as for assisted living at 88.8%. Since that time, there has been a clear divergence in occupancy performance reflecting the differences in supply growth and demand for the two property types.

- For majority independent living properties, inventory growth exceeded absorption by 70 basis points in the first quarter—1.9% versus 1.2%. The occupancy rate for majority independent living properties was 90.3% in the fourth quarter.

- Annual inventory growth for majority assisted living properties was 4.7%, up a bit from the fourth quarter. Annual absorption slipped back to a pace of 3.2%.

Seniors housing occupancy: twenty-two markets down, seven up year over year

The following chart shows a comparison of occupancy rates among the Primary Markets. The blue dot shows the current occupancy rate, and the orange dot shows the year-ago occupancy rate. The top of the blue bar shows the all-time highest occupancy rate by market, and the bottom of the blue line shows the all-time low.

Fifteen markets had occupancy rates higher than the Primary Market average. Starting on the left is the market with the highest first-quarter occupancy rate: San Jose, at 95.1%. After San Jose, the highest occupancy levels are in Baltimore, Portland, Sacramento, Pittsburgh and Seattle, all markets with occupancy rates above 91%. At the other end of the spectrum are San Antonio, with an occupancy of 78.3%, followed by Houston, Atlanta, Dallas, Las Vegas and Kansas City, all with occupancy rates below 85.0%.

Twenty-two of the thirty-one markets had occupancy rates lower than year-earlier levels, while seven markets had higher occupancy rates than one year ago and two were unchanged (Sacramento and Philadelphia). The most significant deterioration occurred in Detroit (down 360 basis points to 87.3%), St. Louis (down 3 full percentage points from 91.1% to 88.1%), Phoenix, Houston and Washington DC. The most improvement occurred in Portland Oregon, where occupancy increased by 1.7 percentage points to 93.0%, while Riverside was up 1.0 percentage points to 86.3%.

Same-store rent growth decelerates

Same-store asking rent growth for seniors housing decelerated in the first quarter, with year-over-year growth of 2.3%. This was down from 3.7% in the fourth quarter of 2016, when it reached a cyclical peak and the smallest increase since early 2014. Asking rent growth for assisted living was 2.9% for the first quarter, up 20 basis points from the fourth quarter. For independent living, rent growth slipped back to 2.0%, half the 4.1% pace it achieved in the third quarter of 2016, when rent growth reached its highest pace since NIC began collecting this data.

According to the U.S. Bureau of Labor Statistics, average hourly earnings were up 5.0% for assisted living employees as of Q4 2017. Together, these lines show the pressure operators may be having as expense growth has been pressured higher, while rent growth has been easing. For many operators, labor expenses amount to 60% of their expenses.

Closed seniors housing and care dollar volume: $2.3Bn for first quarter

Seniors housing and care transactions volume totaled $2.3 billion in the first quarter based on preliminary estimates. That includes $1.5 billion for seniors housing and $800 million in nursing care transactions. The total volume was down 17% from the previous quarter’s $2.8 billion and down 50% from the first quarter of 2017, when volume came in at $4.7 billion. The first quarter of the year is usually one of the weakest quarters in volume, due to the usual rush to close deals at the end of the year, leaving the pipeline a bit empty flowing into the first quarter. There were some other dynamics at play as well toward the end of last year with tax reform, but the first quarter of 2018 was relatively quiet overall, even with these preliminary figures.

A few relatively notable transactions in the first quarter were:

Invesque (Toronto-based group) bought 40 properties from Care Investment Trust including mostly seniors housing units but some skilled nursing beds to total over 3,300 units /beds for over $400 million, and

Cascade/KKR JV bought 18 seniors housing properties from Welltower for a little over $300 million including over 1,400 units.