Carespring's Patient-First Approach to Skilled Care: A conversation with David Eppers

David Eppers

While many of those who work in the industry are driven by a deep personal mission to help others, David Eppers was initially inspired by his mother, Marcy. She cared for seniors in a small Wisconsin town, mostly through her own personal relationships and through her church.

During his 28-year career in long-term care, Eppers has enjoyed the gratification of working with the frail elderly—something his mother taught him by being a role model for him for his whole life.

Today, Eppers continues to carry that legacy forward as owner and chief financial officer of Carespring Health Care Management, Loveland, Ohio.

NIC’s Senior Principal Bill Kauffman recently spoke with Eppers about the future of the skilled nursing industry and what’s ahead for Carespring.

What follows are excerpts from the conversation.

Kauffman: Would you provide an overview of the Carespring portfolio?

Eppers: Carespring has 10 skilled nursing facilities and one retirement center in the market that covers Southwest Ohio and Northern Kentucky. We are also building an additional skilled nursing facility scheduled to open in the fall of 2018 in Northern Kentucky.

Kauffman: Do you own all your real estate? If not, what are your thoughts about owning vs. leasing?

Eppers: Although we build our own facilities, they are currently financed through REIT relationships, but we operate our facilities as if we own the real estate. This includes renovations and updates that meet the changing needs of our patients. We also incorporate functional improvements into our building designs. Recently, we’ve added more therapy gyms and converted semi-private rooms to private suites that share a bathroom and closet.

The biggest challenge with leasing is the annual lease escalator. Our lease cost is steadily increasing while our revenue stream may not. Additionally, lease agreements don’t provide an adjustment if interest rates drop.

Kauffman: How did Carespring get to where it is today?

Eppers: Barry Bortz founded Carespring with the construction of a single facility in 1986. His focus has always been to simply provide the best care possible within a warm and progressive environment. People visit our facilities and comment on the beautiful design and innovative floor plan and ask where it came from. It truly comes from a patient-first mentality. We see what the patient wants and the best way to deliver it, and design our buildings accordingly. It’s rewarding to us when one of our seniors says, “This is the nicest place I’ve ever lived.”

Our caregivers are the most important part of Carespring. We can only be effective with a patient-first mentality by promoting our caregivers. That includes a well-supported nursing function and in-house therapy. Barry Bortz created a culture to continue to innovate and improve upon the way we provide care. He passed away in September 2016 from a health challenge he dealt with for the previous six years. I truly miss him as a friend. As for Carespring, however, Barry left behind an incredible legacy and a solid management team to continue on with his vision.

Kauffman: What is your growth plan for the next few years?

Eppers: We’ve always grown through construction of one or two facilities at a time. That will continue as a baseline. We have some plans in the works to accelerate that growth plan. I can’t get into the details here, but we are looking to take advantage of some of the tremendous opportunities within this industry.

Kauffman: Have ACOs and/or bundled payments affected your portfolio’s performance? Are there any other payment model initiatives in your markets, and how are they playing out?

Eppers: A few physician groups are managing voluntary bundles in our markets. These bundle projects have required direct face-to-face meetings to ensure we are both meeting the objectives of the bundle—great care at a lower cost. That has been a boost to our census.

In our markets, hospitals systems are looking at outcomes despite not directly engaging in an overall ACO model. All of them have initiated a process to narrow their networks and have attempted to align with the best providers. Each of the seven systems in our market is progressing at their own speed with some just beginning the data tracking component, while others are having outcome meetings with aligned partners. We are included in the narrowed markets, but we haven’t seen a dramatic cause-and-effect relationship in our census.

Some of the managed care providers are creating their own narrowed networks and are aligning with partners that provide lower-cost-per-episode outcomes and lower rehospitalization rates. We participate in some of those networks, and one has a “floor-to-skilled nursing” program to expedite the transfer from the hospital to our lower cost setting.

Kauffman: How does Carespring respond to the changing payment models and value-based purchasing? Is that payment model here to stay?

Eppers: Third-party payment methodologies have had many significant changes since I joined this industry in 1989, and I expect that to continue. The one thing I’ve learned is that we have to be flexible in our processes so we can effectively handle what comes our way and still provide excellent care. Value-based purchasing conceptually is fine. We should get what we pay for. However, the measurements of performance often times aren’t accurate. We’ll see what happens.

Kauffman: We have seen plenty of occupancy challenges within the skilled nursing sector over the last few years. What’s driving these challenges?

Eppers: There has been much more volatility in skilled days on a month-to-month basis as well as overall census challenges. Our industry is trying to determine the right provider for particular care needs. For some, home may be the best environment, for others a skilled nursing facility is needed. Some may benefit from a longer (or shorter) hospital stay. Our occupancy challenges will continue until we get this worked out.

Kauffman: Have you felt occupancy pressures like many in the sector? If so, how are you addressing it?

Eppers: We’ve felt it, absolutely. Our approach is simple. We need to provide excellent care. We work on that every day. We identify and meet our patient needs. The other important piece is to stay engaged with the hospital systems within our communities. We are all part of the patients’ care experience.

Kauffman: Aging demographics should play a positive demand factor for the skilled nursing sector in the future. What are your thoughts on that and how do you plan to capitalize on this demand?

Eppers: As the senior population grows, demand across the continuum will grow. But the types of services required will change. We need to continue to develop progressive environments to meet the changing needs, systems that are efficient and effective at providing and documenting care, and a means to draw staff into the industry and to continue to develop them as caregivers.

We believe we do this very well through our staff, systems, and facilities. For that reason, we also need to expand into other markets.

Kauffman: How do you see the skilled nursing sector evolving/changing over the next decade?

Eppers: Our patients will want more comforts and amenities, more private rooms, and likely will have more clinical needs than before. Providers of the future will meet those needs. I also expect to see payment sources change to support more effective and cost efficient incentives such as eliminating hospital stay requirements and promoting concurrent therapy for a fair rate. Eventually systems come around to what makes sense.

Kauffman: Is staffing a challenge in your market? What about wage pressure? Do you have programs in place to address these challenges?

Eppers: Staffing continues to be a challenge from a wage and retention standpoint. We make every attempt to engage and develop our staff. Retention is our focus. Our program promotes engagement. Staff-to-resident engagement as well as staff-to-staff engagement programs are in place. These programs measure and encourage these behaviors in a fun way. The first program, the “Bee Program,” started in one of our facilities and resulted in vastly improved outcomes, staff retention, and census. The Bee Program promotes and tracks engagement. It allows staff and patients to give staff awards, or “Bees,” in recognition for basically everything positive that they do. Staff can accumulate Bees and receive additional recognition and rewards. It’s now spread to all facilities.

Kauffman: Do you view acquisitions as a viable growth plan?

Eppers: Yes, definitely if the right market comes along that allows us to install our systems and processes, we can grow through acquisitions.

Kauffman: What do you see as the greatest opportunity and the greatest risk for skilled nursing operators in the next 10 years?

Eppers: Great skilled nursing providers have the opportunity to take advantage of being the lowest cost inpatient setting, compared to an inpatient rehabilitation facility (IRF) and a long term acute care hospital (LTACH). To do so, we must meet changing care needs while continuing to be cost effective and continue to grow the clinical capabilities of our nursing staff.

The greatest risk is that skilled nursing is becoming a much more complex business. Providers who can’t manage significant change will struggle mightily. A provider must be nimble and adjust to the ever changing needs of the residents (especially the baby boomers), regulatory environment demands, hospitals and third-party payer systems.

The other big challenge is the imbalance in our payment systems. We need to continue to serve our seniors who otherwise can’t afford care through our state Medicaid programs. For Carespring, Medicaid recipients represent over half of our patient population. The payment system, however, pays $40 to $60 per day less than it costs to provide care. That’s an imbalance that must be resolved as payment systems try to reduce the cost of skilled services.

How to Unlock Value in Senior Care Collaboration A preview of the 2018 NIC Spring Investment Forum

The lines continue to blur between senior living and the services seniors need to better their lives. Assisted and independent living communities increasingly provide wellness and other health-related services to their residents. Skilled nursing facilities are becoming more specialized, providing care for conditions which might have previously been treated in a hospital.

The breakdown of the silos between the traditional real estate aspect of seniors housing and care and the services seniors need to thrive—while providing the best care in the lowest cost setting—will be explored at the upcoming 2018 NIC Spring Investment Forum.

The theme of the 2018 NIC Spring Investment Forum is: “Unlocking New Value Through Senior Care Collaboration.” It highlights how owners, operators, service providers, and investors can benefit by identifying opportunities to better today’s residents.

“We, as an industry, want to foster the connection points between traditional real estate investment and non-real estate investments in services and care,” said Torey Riso, co-chair of the Forum’s planning committee, and CEO at Care Investment Trust, New York. “ It’s important for traditional real estate investors and owners to explore the other side of the care delivery equation, Riso emphasized. Technology is changing the way services are delivered. Home care and home health are becoming important components of the care delivery system in senior living communities, he noted.

“There is a reshuffling of services and how these services can be provided in a more efficient way, and in a different setting,” said Riso. “The Forum will explore these opportunities.”

This is the second year the NIC Spring Investment Forum has focused on the theme of “Unlocking New Value Through Senior Care Collaboration,” said Jim Thompson, Forum co-chair, and senior director—senior housing lending, Synovus Bank, Birmingham, Ala. “The sessions will dig deeper into many of the topics we introduced at last year’s Forum.”

Attendees will gain insights into how to position their companies to benefit as the fee-for-service health system migrates to one that rewards integrated care, good clinical outcomes and a lower cost. “Seniors housing and skilled nursing facilities care for a lot of frail elderly” said Thompson. “We have a significant role to play as the healthcare delivery and payment systems change.”

The NIC Spring Forum will spotlight specific issues currently facing the industry, said Thompson. These include a look at which provider partnerships are most valuable, how to adjust to the reality of a shorter length of stay in skilled nursing and narrowed health system networks, what investors need to know about the changes in the industry, and labor issues which have emerged as a big concern for operators and owners.

“We need to think outside of the four walls of our buildings,” said Thompson.

Conference Highlights

Focused on practical solutions, NIC’s Spring Investment Forum attracts more than 1,500 leaders in healthcare, seniors housing, home care, finance and care coordination. The Forum includes networking opportunities as well as educational sessions. Some topic highlights include:

Seniors Housing & Care. Discussions will include a deep dive into local markets with the latest data from NIC. Sessions will address capital flows into the sector, investing in skilled nursing, valuations, care quality and profit margins.

Home. How is home defined? What are the social determinants of health? What is the customer experience? What are the customers’ expectations?

Value. Questions will be addressed on how to leverage scale, emerging payment models, and how to become a care manager or coordinator.

Partnerships. The role of primary care and home care for frail elders and how partnerships can be used as a value driver.

Risk. Programming will cover the need for, and the role of data and predictive analytics; financial returns of innovative care models; the financial results of not taking on risk vs. taking on risk; becoming a Medicare Advantage Plan; and whether care delivery is enough to achieve the desired financial returns.

Looking ahead to the Forum, Riso said: “I’m excited to be on the planning committee for NIC’s Spring Investment Forum because of its cutting-edge nature. We’ll be asking questions about how to bring together seniors housing, skilled nursing and innovative services. It’s a fascinating place to be because we’ll continue to identify the relevant questions, and begin to define the possible answers that will shape the future of the industry.”

Sign up to receive a notification once registration opens in mid-November. As a preview, here’s a link to highlights from NIC’s 2017 Spring Investment Forum.

How to Benefit from the Program of All-Inclusive Care for the Elderly ("PACE")

The Program of All-Inclusive Care for the Elderly (PACE) which integrates care delivery can benefit many seniors housing providers. What follows is the second part of a two-part series that explains the program and why partnerships with PACE providers are worthy of consideration. Part I appeared in the Sept. 2017 issue of the NIC Insider. It covered the benefits of the PACE program and how it works. Part II discusses which senior living operators should consider PACE along with insights for the investor. This series was compiled by the following members of the NIC Future Leaders Council, along with input from the national PACE organization: Susannah Myerson, Vice President of Senior Housing Finance, Wells Fargo Bank; Andrew Smith, Director of Strategy & Innovation, Brookdale Senior Living; Derek Zeller, Director, BMO Harris Bank; Morgin Morris, Vice President of Mortgage Banking, KeyBank Real Estate Capital

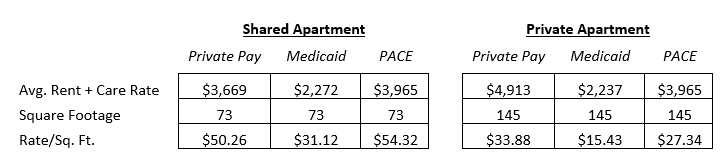

Determining whether relationships with PACE providers should be a priority for an operator depends on the type of senior housing operator. Specifically, it depends on the Medicaid penetration at the community. A high-end, private pay community would likely not have much reason to partner with PACE providers. However, relationships with PACE providers may make sense for an operator with a substantial Medicaid population. Residents participating in a PACE program can be financially preferable to pure Medicaid residents and can also receive additional oversight and care through their participation in PACE. Further, residents participating in PACE programs and living in shared apartments can often generate a rate per square foot that is competitive with a private pay resident in a private apartment.

Case Study: Comparing Rent + Care Rates in 60-unit Memory Care community in Colorado.

Lender or equity investor considerations

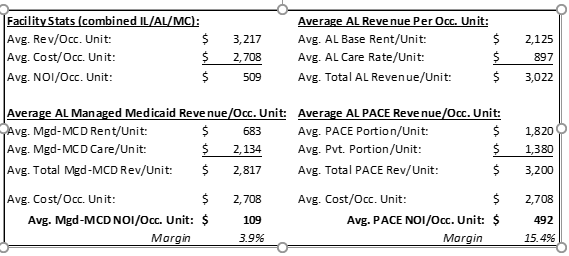

Capital providers will typically base the amount of debt and/or equity allocatable to a care facility on their assessment of the facility’s value. As the value assessment typically comes from a derivative of NOI, the effect that PACE has on a facility’s income statement will unavoidably impact its ability to attract capital. See the following example showing the program’s financial impact on an assisted living-focused facility in Northeast Ohio as compared to the State’s Managed Medicaid payor:

As the comparison above shows, a typical PACE payor at this facility provides for a per-occupied-unit margin of 15.4% – 11.5% greater than that of the average Managed Medicaid payor. At face value, one could conclude that the PACE eligible facility would be more attractive to capital providers given this added revenue and NOI margin. Although this may be the case, there are a number of other factors the investor should contemplate that may temper the assessed income differential. In particular, the capital provider should consider how sustainable the PACE program is in the current governmental reimbursement environment, and further, what the downside scenario should be from an underwriting perspective. The Managed Medicaid model is a likely landing spot for investors considering the downside scenario, so a discount to the discrepancy in average NOI per occupied unit is likely to be applied by most investors. Ultimately, the different capital providers will need to take their individual risk appetites into account when determining how to view Pace Program participants.

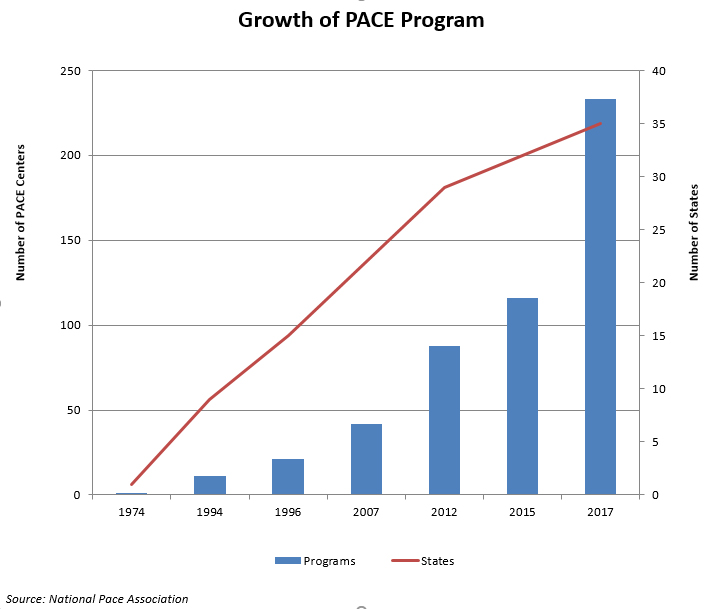

Future & potential growth

Source: National PACE Association

With an estimated 9 million “dual eligible beneficiaries” in the United States in 2017, and that number projected to increase substantially over the next 10 years, PACE providers (and potential providers) are taking note. PACE programs have seen an exponential growth since 2015 when the program allowed for-profit providers to enter the space.

One company that is aggressively expanding its PACE programs is InnovAge, a Denver-based provider that currently operates nine PACE centers in California, Colorado, New Mexico and Virginia. In May of 2016, the company received $196 million in venture capital backing from the private equity firm Welsh, Carson, Anderson & Stowe. InnovAge notes that nationwide PACE programs reached fewer than 4% of eligible seniors in 2015, and InnovAge is committed to expanding its reach into additional markets and marketing the PACE program to all seniors.

Seniors Housing Occupancy Unchanged, While Growth in Inventory and Demand for Assisted Living Accelerate

Beth Mace

Five Key Takeaways from NIC MAP’s Third-Quarter Seniors Housing Data Release

NIC MAP® Data Service clients attended a webinar in mid-October on the key seniors housing data trends during the third quarter of 2017. Five key takeaways emerged:

- Seniors housing occupancy remained unchanged at 88.8%

- Annual growth rates for both assisted living inventory and absorption reached record highs in third quarter

- Eleven markets saw annual gains in inventory of more than 10%

- Same-store rent growth decelerated

- Closed property sale transaction volume accelerated in third quarter

Let’s take a closer look at some of these trends.

Seniors housing occupancy unchanged at 88.8%

The total occupancy rate for seniors housing, which includes properties still in lease up was 88.8% in the third quarter, unchanged from the second quarter. This placed occupancy 1.9 percentage points above its cyclical low of 86.9%, reached during the first quarter of 2010, and 1.4 percentage points below its most recent high of 90.2% in the fourth quarter of 2014. For the four quarters ending in the third quarter, more than 23,000 units were added to inventory, versus 16,000 units absorbed. As a result, occupancy fell 60 basis points from the third quarter of 2016.

Stabilized occupancy for all seniors housing properties (defined by NIC as properties that have been open for at least two years or, if open for less than two years with an occupancy level of 95%) was higher than total occupancy and stood at 90.3% in the third quarter, also unchanged from last quarter and down 60 basis points from year-earlier levels. It is notable that the difference between total occupancy and stabilized occupancy was 140 basis points, down from 160 basis points the prior quarter but still quite significant. The size of this gap reflects the large number of properties recently opened and still in lease up.

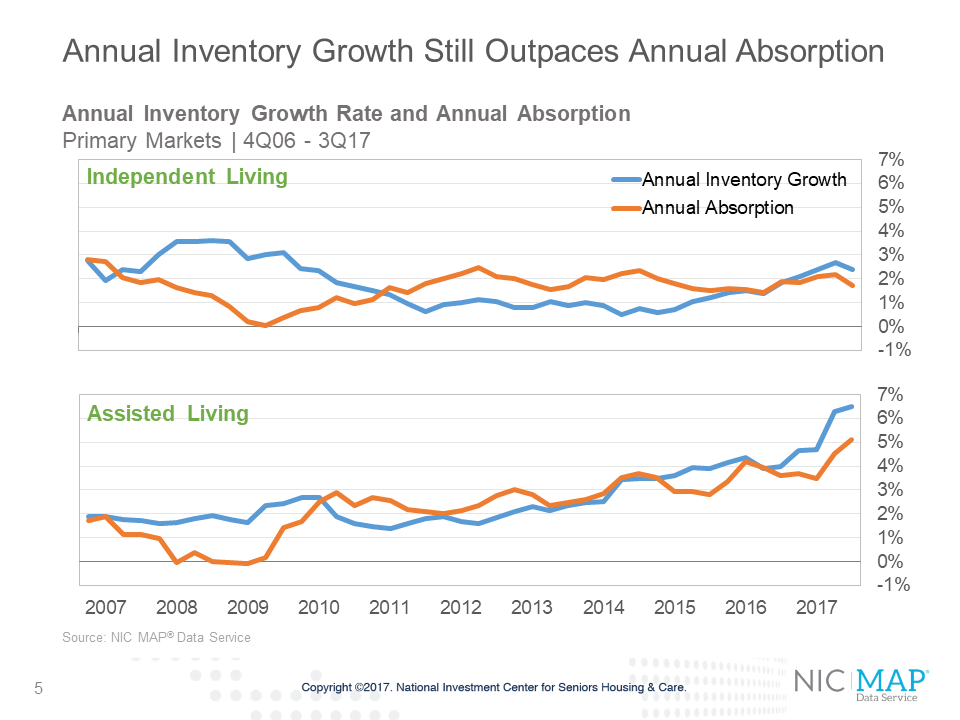

Annual growth rates for both assisted living inventory and absorption reached record highs in third quarter

- Assisted living inventory growth has been ramping up for a longer period than independent living, and as of the third quarter, annual inventory growth for majority assisted living properties in the primary markets reached its highest level since NIC began reporting the data in 2006—6.5%. This has put significant downward pressure on occupancy which stood at 86.6% in the third quarter. Annual absorption also accelerated in the third quarter and came in at a pace of 5.1%. This puts annual absorption also at the highest rate since NIC began reporting the data.

- For majority independent living properties in the primary markets, inventory growth exceeded absorption by 70 basis points in the third quarter—2.4% versus 1.7%. The third quarter pace of year-over-year inventory growth was a bit weaker than in the second quarter when it posted a 2.7% gain, the strongest pace since mid-2009. The occupancy rate for majority independent living properties was 90.5% in the third quarter.

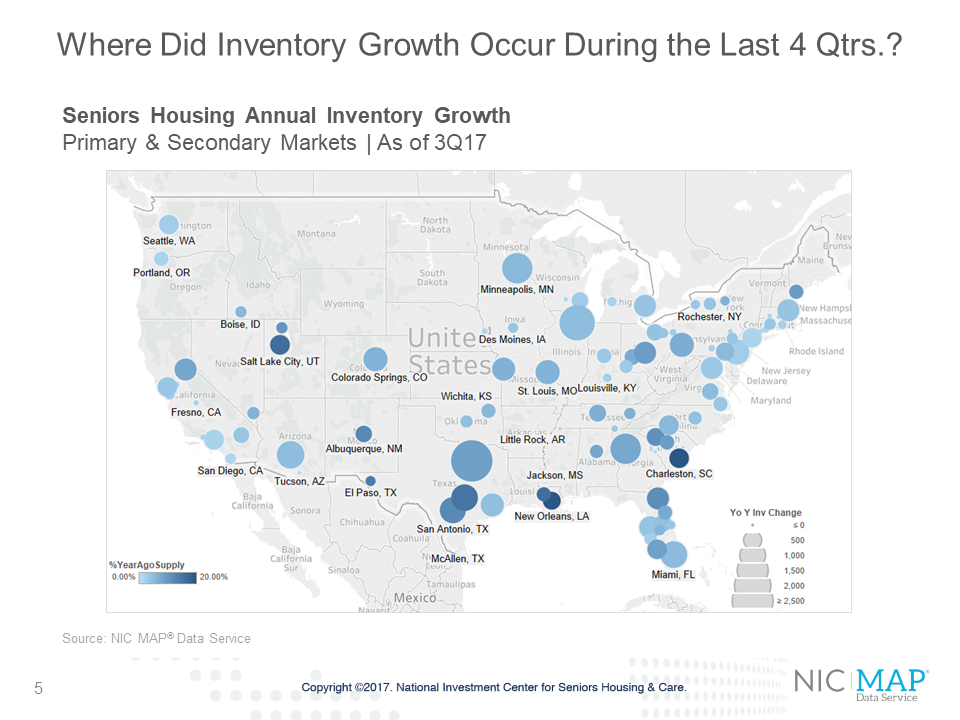

Eleven markets saw annual gains in inventory of more than 10%

During the past year, nearly 38,000 units have been added to the stock of seniors housing inventory among the primary and secondary markets. Roughly one quarter of this growth occurred in seven metropolitan markets: Dallas, Chicago, Minneapolis, Atlanta, Phoenix, Austin and Miami. Dallas alone accounted for 7% of all new seniors housing inventory in the past 12 months.

Relative to each metropolitan markets own inventory, there were 11 geographies that experienced gains in inventory of more than 10% over the course of the year. They include New Orleans, Charleston, Baton Rouge, Salt Lake City, Austin, El Paso, Albuquerque, San Antonio, Jacksonville, Greenville and Ogden, and are depicted by the darker shades of blue circles on the following map.

Same-store rent growth decelerates

Same-store asking rent growth for seniors housing slowed in the third quarter, with year-over-year growth of 2.7%. This was down from 3.4% in the first half of this year, and was near the 2.6% average pace experienced since late 2006.

Asking rent growth for majority assisted living properties was 2.4% for the third quarter, down 70 basis points from the second quarter. For majority independent living, rent growth decelerated to 2.5% from 3.7% in the second quarter and down from 4.2% in the third quarter 2016, when rent growth reached its highest pace since NIC began collecting this data.

There is wide variation in rent growth. Los Angeles rents increased by 4.7% from year-earlier levels, while San Jose was up by 5.4%. At the other end or the spectrum was Kansas City, which saw rents fall by 0.2%.

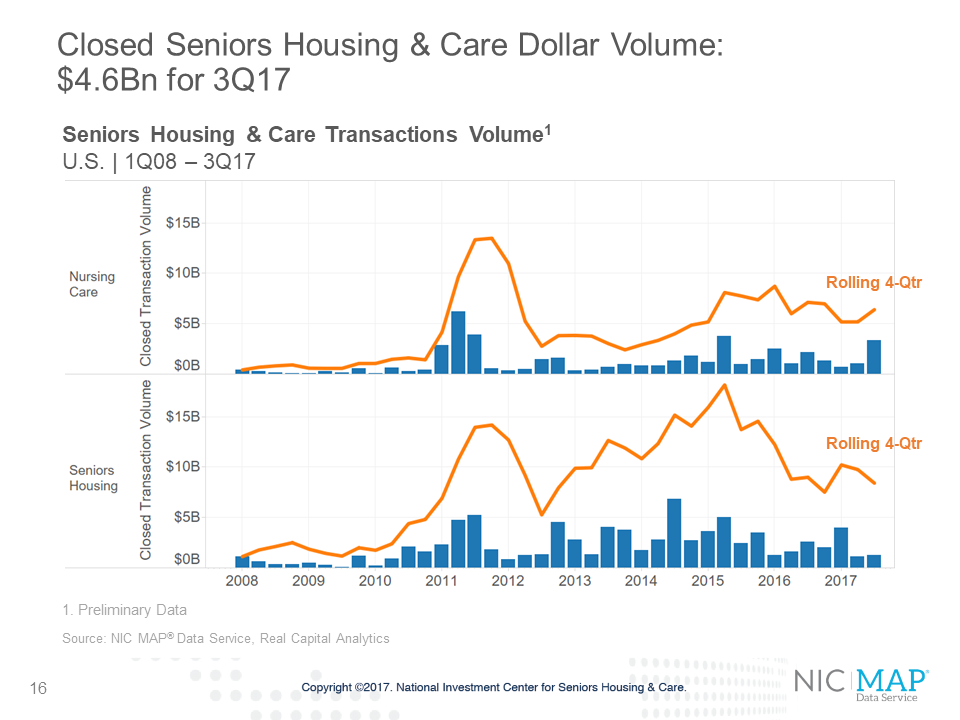

Closed transaction volume picked up in third quarter

The third quarter saw a significant uptick in closed transaction volume. Seniors housing and care transaction volume totaled a preliminary $4.6 billion in the third quarter, which is comprised of $1.3 billion in seniors housing sales and $3.3 billion in nursing care. The total volume was up 113% from the previous quarter’s $2.2 billion.

At $15 billion, the rolling four-quarter total seniors housing and care volume was flat compared with the second quarter

In Case You Missed It: NIC Talks “Tell Me Something I Don’t Already Know About Aging”

Disruptive change is just over the horizon as the senior living industry prepares to care for the Baby Boomers. Are you ready?

Returning to the stage for the third year at the 2017 NIC Fall Conference, the provocative speakers forum NIC Talks featured nine thought leaders who challenged the conventional thinking about senior living. The speakers were asked to address the theme: “Tell Me Something I Don’t Already Know About Aging.”

Inspired by the popular TED Talks format, the fast-paced and compelling NIC Talks touched on trends, research, and areas for innovation and collaboration. The featured speakers—including fresh perspectives from outside the industry—explored topics such as ageism, longevity, and the emerging role of artificial intelligence in healthcare.

If you missed NIC Talks at the conference, the video links are here – http://www.nic.org/events/nictalks-boomers-envisioning-aging-revolution/nic-talks-videos-1/. Find out what the experts are saying about the future of aging and aging services, and get ready.