Straight Talk from a Lending Pro: A Conversation with Matt Huber of People’s United Bank

Matt Huber doesn’t mince words. He tells it like it is. What he expects from borrowers, and what they can expect from him.

Matt Huber doesn’t mince words. He tells it like it is. What he expects from borrowers, and what they can expect from him.

Throughout his career, Matt Huber has launched de novo, or entirely new, healthcare finance divisions for different banks. It’s what he likes to do: put together the business plan, write the credit policy, and hire staff. He’s learned what it takes to build a successful seniors housing and care loan portfolio as markets seesaw back and forth. And he’s not afraid to share his insights.

NIC Chief Economist Beth Mace recently talked with Huber about his role as market manager of Healthcare Financial Services at People’s United Bank. Here’s a recap of their conversation on what borrowers need to know in today’s uncertain market and what’s ahead for the industry.

Mace: People’s United ranks among the largest 50 full-service banks in the nation. Where does seniors housing and skilled nursing fit into the organization and its goals? How long has People’s United been lending to the seniors housing and care sector?

Huber: We started a dedicated healthcare finance group when I was hired in July of 2017. I came on board to develop a de novo group dedicated to seniors housing and care with a deep understanding of the business and a goal to expand it. I have experience in nonprofit healthcare and the hospital sector, but my real forte is in for-profit seniors housing.

Mace: Where did your seniors housing background come from?

Huber: For the past 21 years, I have been a dedicated healthcare banker. I started in 1999 at M&T Bank in Syracuse when they launched a healthcare group. In 2004, I moved over to Key Bank which had a much larger healthcare platform and, after two years, moved to Cleveland to manage Key’s Midwest and Northeast markets. In 2009, First Niagara reached out and asked me to start a de novo healthcare group back in upstate New York. It was a dream job for me. I put the business plan together, wrote the credit policy, and hired the people. In about seven years, we built a $2.5 billion portfolio. I’m proud of that. First Niagara was then acquired by Key Bank, and I stayed another year to help them transition their hospital portfolio to a more consistently delivered business strategy across their national footprint. I knew Jeff Carpenter, executive vice president, Commercial, People’s United Bank, through NIC conferences. He asked me to come over to the bank and start a de novo healthcare group. I’ve been here almost four years now. The bank has grown to over $65 billion in assets with retail locations from New York City to Maine. Our seniors housing and care business covers the Northeast as well as the Mid-Atlantic states.

Mace: What is your role, and how has it changed during your tenure at the bank?

Huber: My role as healthcare market manager at People’s United has expanded since I joined in 2017. Our bank has a large presence in New Hampshire, Vermont, and Maine. Those relationships continue to be managed by middle market bankers in those states. But I provide oversight on those credits, along with our healthcare credit officer. Four dedicated healthcare relationship managers report to me, focusing on Massachusetts to Virginia. I also wrote the credit and commercial policy for the healthcare group at People’s United Bank. As of December 2020, our healthcare portfolio totaled $2.4 billion, of which about $1.1 billion is seniors housing and care. Seniors housing represents approximately 25% of the bank’s portfolio, and 26% is skilled nursing. When I joined the bank, my group accounted for $450 million in loans. We’ve grown by $800 million in three and a half years.

Mace: How has COVID-19 impacted your portfolio?

Huber: Cases are going down, hopefully because of the vaccine. But we haven’t seen an uptick yet in occupancies and cash flows from nursing homes where most of the cases have occurred. The COVID-19 impact on these facilities was terrible after the holidays, which we’ll see reflected in their year-end and first quarter numbers. Our approach to skilled nursing and memory care will be measured and careful going forward. We’re not out of the woods yet. At the end of last year, we called our top 15 customers to ask about 2021. All of them said the first half of the year would be challenging and then occupancy would be rebuilt through the second half of 2021 and into 2022. I think that’s largely true.

Mace: Are you expecting that borrowers will have problems in terms of covering debt service?

Huber: With funds from the CARES Act, we had incentives in 2020 to restructure loans through 2021 without classifying them as a total debt restructure (TDR). The Office of the Comptroller of the Currency (OCC) said industries gravely impacted by COVID-19 should be supported. We had the ability to give two 90-day payment deferrals without classifying the loans as a TDR. Most of our borrowers are regional players and have been through hard times. And they’re doing the right things. So, fortunately, we had very limited number of payment deferrals or need for restructures from our borrowers. Our goal is to get the borrower back to full payment and a stabilized facility. Their win is our win. We are not quick to throw loans into a workout.

Mace: What should a borrower do to prevent a workout situation?

Huber: The more transparent a borrower is with the bank, the sooner and the better we can help them. Think about this from both sides. Borrowers own these assets and operate them. They don’t want to lose them. The lender doesn’t want to take possession of the facility. It’s not in the best interest of residents to have a bank-owned asset either.

Mace: Do you lend for new development?

Huber: We only loan to those who know how to construct facilities and fill them. We have never and will never provide construction financing to a borrower that hasn’t done this before. We are not going to be your first construction loan ever. We work with major regional operators who’ve done their homework, using NIC MAP®, of course.

Mace: What is your appetite for lending?

Huber: For 2021, our business plan continues to call for growth in loans, commercial bank services, and adding new customers and supporting existing ones. But we will be a bit more conservative in our approach to ensure we are lending to those who have weathered challenges in the past and have the wherewithal to manage through this cycle.

Mace: What do you look for in a good sponsor?

Huber: We have a very similar business plan to the one we had at First Niagara coming out of the Great Recession. When other banks were sitting on the sidelines, we did development loans with very experienced sponsors with deep pockets. When there is a lot of money flowing, it’s easy to get construction capital; but in times like this, it’s a little harder, and that’s where relationships are built. If you support good sponsors in tough times, hopefully that relationship continues when times are good. That’s where experience comes in, you know which partners to pick.

Mace: How do you measure the quality of an operator?

Huber: The less care they provide, the harder it is to find public information. The more care they provide and the more regulated they are, the more public information is available from the Centers for Medicare & Medicaid Services (CMS). Information on assisted living varies from state to state. We track occupancy and payor mix, and where residents are coming from. The biggest factor is whether the facility has been able to maintain long-term occupancy, compared to competitors. We also look at the turnover rate in the executive director position and among the unit managers. Before COVID-19, we always liked to visit the facility and chat with the activity director or the director of nursing. Are they calling their residents by their names? How do residents respond? We also like to see the places the public doesn’t see, like the kitchen and basement.

Mace: When do you turn a lending opportunity down? Are there any immediate red flags?

Huber: An immediate red flag is high leverage. We’ve had potential borrowers ask for a 90% percent loan to cost. Anything above 80% is a problem for us. If we’re doing a bridge loan to an agency, we like the sponsor to earn into that higher leverage with some stability. If we extend 65% or 70% leverage at first, we might provide a pathway to get to 80% to 85% leverage. We don’t do non-recourse construction lending. We need a secondary source of repayment if the deal goes sideways. If the borrower is taking over a special focus facility under the CMS program for properties with serious quality issues, we want to see a path to resolve that. I’d also be cautious about a sponsor in my geography that I don’t already know, or if this is the sponsor’s first or second facility.

Mace: Any advantage to me as a borrower if you are focused on the Northeast and Mid-Atlantic?

Huber: As a bank, we are deeply invested in the community. We have 6,500 employees that live in and use the healthcare systems in their communities. We have a philanthropic arm and foundation to support the community. A regional bank like ours is more apt to listen to the borrower’s story because we are all a part of the local community. We are relationship driven. We know the local markets. We’ve turned down some development projects because we knew nearby buildings with good operators were only 80% occupied. That’s not for us.

Mace: Do you believe that seniors housing is as an operating business in a real estate setting? If so, how do you evaluate the operating business? How do you evaluate the real estate?

Huber: About 75% of our loans are commercial real estate mortgages. The remainder are operating lines of credit. The federal government classifies seniors housing as a form of real estate, and we are required to code loans based on the regulator’s rules. From an underwriting viewpoint, we always analyze core operations to see how we are getting paid. If a REIT asks for a loan, we spend most of our time scrutinizing the operator. And the more care they provide, the more we are focused on the operator. Independent living is more of a tenant situation. I think investors have come into this industry and put real estate folks into a healthcare group viewing the facilities more as real estate. But you can have a nursing facility that was built in 1972, 100% occupied, and the quality of care is amazing. Then you can have a nice, new building with bad care. It’s still an operating business.

Mace: What are the opportunities as well as the challenges you see for the seniors housing and care sector? In both the near and long-term?

Huber: The challenges are well known. COVID-19 has poked some holes in our systems. Part of the reason facilities have not been able to get their occupancy up is that the adult children are concerned that they may not be able to see their folks. But I think there are some opportunities in telehealth and short-term rehab as people search for other solutions. Keeping up the residents’ faith in the product during a pandemic is an opportunity. We may not have seen the last pandemic. I think the seniors housing and care industry could be a haven for people and will continue to be a major component of the healthcare system. And, as boomers get older, there won’t be enough services and housing available. It just comes down to whom comes up with the next creative idea to get us there. I’m bullish on the industry, but I’m going to be careful until the pandemic is more under control.

Thoughts from NIC’s Chief Economist

By Beth Burnham Mace, Chief Economist

Good news at long last. New U.S. COVID-19 infections, hospitalizations, and death rates are on the decline. A combination of factors is contributing to this trend. Foremost among them are vaccinations which are well underway, especially for America’s elders in congregate settings. More broadly, the U.S. is now administering 1.6 million vaccine doses each day (as of mid-February), and the pace is likely to hasten. The vaccines are highly effective at preventing infection. Importantly, they are also successful in reducing symptoms for those already affected. A reduction in symptoms, in turn, lowers long-term hospitalizations and ultimately fatalities. With over 500,000 deaths in the United States from COVID-19, this is good news indeed.

Good news at long last. New U.S. COVID-19 infections, hospitalizations, and death rates are on the decline. A combination of factors is contributing to this trend. Foremost among them are vaccinations which are well underway, especially for America’s elders in congregate settings. More broadly, the U.S. is now administering 1.6 million vaccine doses each day (as of mid-February), and the pace is likely to hasten. The vaccines are highly effective at preventing infection. Importantly, they are also successful in reducing symptoms for those already affected. A reduction in symptoms, in turn, lowers long-term hospitalizations and ultimately fatalities. With over 500,000 deaths in the United States from COVID-19, this is good news indeed.

Other factors have also come into play. One of these is behavior modification with the message of social distancing and mask wearing finally seeming to stick (at least better than it had been). People are staying home more. Mobility data from Google for mid-February show mobility trends for places like public transportation hubs, such as subway, bus, and train stations, were 45% below baseline levels of early 2020, for example.

Battling COVID-19

Another reason for the declines may be that many Americans have already been infected by COVID. Indeed, as of February 22, there were 28 million cases of COVID reported in the U.S. according to the Johns Hopkins Coronavirus Resource Center. This represents nearly 9% of the U.S. population. If infection means immunological protection, then there may simply be fewer Americans still susceptible to the virus, or at least the original virus.

Further good news specific to the skilled nursing sector is that weekly data from CMS shows that new COVID-19 confirmed cases within skilled nursing properties have been falling at a faster pace compared with U.S. overall new cases. Notably, as NIC’s Skilled Nursing COVID-19 Tracker shows, new confirmed cases within skilled nursing properties were down 89% from 32,570 on December 20 to 3,424 on February 14, while U.S. new reported cases were down 59% over the same period. While similar precise data does not exist for seniors housing, it’s likely that the same or similar trends are occurring since seniors housing residents and skilled nursing patients were both given high vaccination priority.

It’s a game changer for seniors housing and care and should launch improvements in move-ins, visitations, property tours, occupancy rates, and overall interaction and socialization. Many operators are now talking about post-COVID-19 property-specific protocols that should be established. State and local guidance on quarantines is also easing, especially after second vaccinations have taken place.

A significant offset to this optimism is the lack of staff enthusiasm for getting vaccinated, however. Four out of five organizations in Waves 20 and 21 of NIC’s Executive Survey Insights indicated that educating and motivating staff to take the vaccine is a challenge. Further concern of course is the rise of new variants of the novel coronavirus being introduced into the U.S. from the U.K., South Africa, and other places.

Reductions in cases and fatalities are easing the herculean pressure placed on our nation’s healthcare systems in the past several months. Hospitals and ICU beds were approaching or at capacity in several instances and this pressure has now eased.

While all of this suggests that we are entering the beginning of the end of this pandemic, it is still important to realize that we cannot let our guard down. We need vaccinations in combination with other interventions, including frequent testing, continued emphasis on physical distancing, and adherence to masking guidelines. These interventions continue to be an effective and vital weapon against the rate of mutation of the virus and the spread of current virus strain until vaccines are widely accepted and distributed and herd immunity is achieved. Herd immunity—with three-fourths of the population having been vaccinated or infected and thus presumably with some immunity to the virus—looks possible by the summer or fall of this year.

Economic Recovery Outlook

If this pace of improvement continues, the economy will start to shift into a fuller recovery as service businesses, such as restaurants, entertainment venues, and travel-related activities, spring back to life. Pent-up demand should jump start a burst in activity once the “coast is clear.” Middle- and high-income households have plenty to spend as evidenced by the nation’s personal savings rate climbing to the equivalent of 7% of GDP. Of course, this does not consider the millions of households who have struggled as service-related jobs have been lost, but this is where many of the dollars of the fiscal programs being endorsed by the Biden administration will focus.

The economy will also benefit from the $900 billion relief package passed into law at the end of last year. Further, the likelihood of additional deficit-financed fiscal stimulus will generate more economic growth as at least portions of President Biden’s $1.9 trillion American Rescue Plan appear headed to passage in the next several weeks. There may also be substantially more spending on various social initiatives as laid out in the Biden administration’s “Build Back Better” agenda. Notably, this spending would be paid for by tax hikes on businesses and high net worth citizens; such efforts will get significant political pushback. With this amount of fiscal stimulus, the economy could return to full employment–an unemployment rate of close to 4% and a labor force participation rate of 62.5%–by early 2023 according to Moody’s Analytics. If this path unfolds, real GDP growth in 2021 alone could exceed 5% or 6%. It’s also likely that interest rates will stay low for the foreseeable future, as Fed Chair Jerome Powell and the FOMC have indicated that this will be the case.

As always, there are plenty of risks to this outlook. Among them is the pandemic itself as new strains of the virus that are more virulent and contagious are showing up across the globe. And regarding the economy, there are growing concerns about surging asset prices for stocks, bonds, single-family housing, and many commodities. Low Treasury yields support high asset valuations. There is also concern among policy analysts that inflation will become undesirably high in the coming years and move beyond the Fed’s stated target of 2% and closer to 3%.

In wrapping up and as always, I appreciate and welcome your comments, thoughts, and feedback.

Legal Basis and Risks of Mandating the COVID-19 Vaccine in Seniors Housing

By Courtney Nickels, Artemis Real Estate Partners

To mandate or not to mandate? It is a very serious question that many employers are facing, and the stakes are especially high for senior living and other healthcare providers. Assuming proper processes are followed, legal experts advise that healthcare employers can mandate that virtually all employees take the COVID-19 vaccine, particularly those employees who have contact with residents/patients and other employees. One thing is clear—there is incomplete federal and state guidance for employers on the ability to mandate. Employers are also weighing many factors, not just legal, in their decision. For healthcare providers, the benefits of mandating the vaccine arguably far outweigh any potential legal risks.

To mandate or not to mandate? It is a very serious question that many employers are facing, and the stakes are especially high for senior living and other healthcare providers. Assuming proper processes are followed, legal experts advise that healthcare employers can mandate that virtually all employees take the COVID-19 vaccine, particularly those employees who have contact with residents/patients and other employees. One thing is clear—there is incomplete federal and state guidance for employers on the ability to mandate. Employers are also weighing many factors, not just legal, in their decision. For healthcare providers, the benefits of mandating the vaccine arguably far outweigh any potential legal risks.

Experts and partners at Arnall Golden Gregory, LLP (AGG) shared their legal view and answered frequently asked questions with members of NIC’s Future Leaders Council (FLC). Both Henry Perlowski, chair of the employment practice, and Hedy Rubinger, chair of the healthcare practice, are advising clients of the firm on how to navigate this issue and its implications in real-time.

The legal basis supporting employer vaccine mandates is twofold. First, the Equal Opportunity Employment Commission (EEOC) issued guidance that the vaccine is not considered a medical exam, which is otherwise prohibited by employers. While COVID-19 remains a declared pandemic by the World Health Organization, an employer can require COVID-19 testing and/or vaccination as long as it is job-related and consistent with business necessity. In customer-facing healthcare roles, these two qualifiers are easily confirmed. Second, the EEOC reiterated that employers must make reasonable accommodations for sincerely held religious beliefs and disabilities under the American Disabilities Act. If the employer has a solid process in place to handle exemptions, mandating the vaccine is legally defensible for healthcare employers. Should an employer elect to mandate vaccination, legal experts highlight the importance of clearly communicating the employer’s expectations, establishing and vetting a process for managing exemptions, and maintaining a consistent team that handles the exemption process with uniformity.

At least two senior housing operators, Atria Senior Living and Juniper Communities, publicly announced in January that the COVID-19 vaccine will be mandated for all employees with some exemptions. Recently, Silverado Senior Living, ALG Senior Living, and Aegis Living also indicated an intent to mandate the vaccine. Many other regional and national operators are considering this path, but most of the industry is following a softer consent-based approach to date. According to NIC’s Executive Survey Insights research through February 7, only 8% of organizations have or will make the COVID-19 vaccine mandatory for staff. The survey results also indicate that employee vaccination rates have ranged from an average of only 40% in the South region to 70% in the Pacific region. Of the respondents, 94% of organizations had completed the first vaccination clinic, and 62% had completed the second clinic.

Efficacy data from skilled nursing facilities is beginning to come in as well, and it shows reductions in COVID-19 cases that could likely be attributable to the vaccine rollout. As reported by AHCA/NCAL, new weekly COVID-19 cases among nursing home residents declined 22% over the three weeks between December 20th and January 10th. The organization’s research division, the Center for Health Policy Evaluation in Long Term Care, also found that COVID-19 cases decreased faster among nursing homes that completed their first vaccine clinic compared to nearby facilities that did not. Expect more data to come as AHCA/NCAL has issued a letter publicly urging the Centers for Disease Control to expedite the evaluation of the vaccine’s effectiveness among the long term care population.

The Biden administration, which is “pro-vaccine,” may issue additional guidance for employers in the near term and as more data becomes available. However, a Democrat-controlled government traditionally has an expectation for greater employee rights, in opposition to a vaccine mandate and potentially creating tension between the administration’s goals. Regardless, the new administration clearly regards that vaccine distribution is in the best interest of the country. In the absence of further federal guidance, employers must consider their priorities and weigh the long-term risks and benefits in determining whether to mandate. The 800-pound gorilla in the room is clearly this question – if employers or the federal government mandates the vaccine for healthcare workers, will there be enough employees to do the job?

For a more detailed legal opinion and support, please see a detailed article co-authored by Perlowski of Arnall Golden Gregory, LLP.

4Q 2020 Care Segment Performance in CCRCs Leads Non-CCRC Properties

By Lana Peck, Senior Principal, NIC

The NIC MAP® Data Service (NIC MAP) tracks occupancy, asking rents, demand, inventory, and construction data for independent living, assisted living, memory care, skilled nursing, and continuing care retirement communities (CCRCs)—also known as life plan communities—for more than 15,000 properties across 140 metropolitan markets. NIC MAP currently tracks 1,208 not-for-profit and for-profit entrance fee and rental CCRCs in these 140 combined markets (1,137 CCRCs in the 99 combined Primary and Secondary Markets).

The NIC MAP® Data Service (NIC MAP) tracks occupancy, asking rents, demand, inventory, and construction data for independent living, assisted living, memory care, skilled nursing, and continuing care retirement communities (CCRCs)—also known as life plan communities—for more than 15,000 properties across 140 metropolitan markets. NIC MAP currently tracks 1,208 not-for-profit and for-profit entrance fee and rental CCRCs in these 140 combined markets (1,137 CCRCs in the 99 combined Primary and Secondary Markets).

The following analysis examines current conditions and year-over-year changes in inventory, occupancy, and same store asking rent growth—by care segments within CCRCs (CCRC segments) compared to those same care segments in non-CCRC properties for both freestanding and combined communities to focus on the relative performance of care segments within CCRCs.

Current CCRC Occupancy by Payment Type and Profit Status

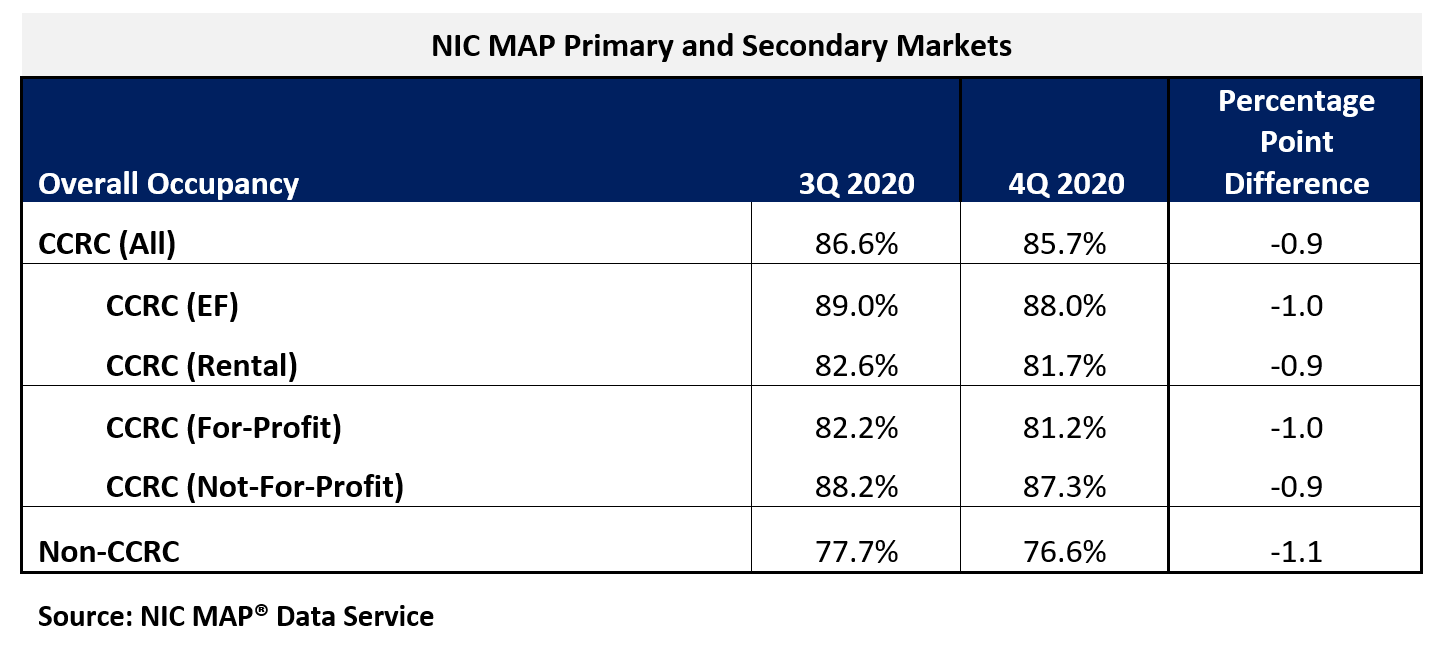

In the fourth quarter of 2020, CCRC occupancy across the Primary and Secondary Markets fell 90 basis points from the third quarter to 85.7%, another new low since NIC MAP began reporting the data in 2006. The cumulative drop in occupancy was 350 basis points since the pandemic began to have an impact on occupancy rates in the second quarter. Prior to the second quarter of 2020, CCRC occupancy had oscillated around 91% for 22 consecutive quarters.

Non-CCRC occupancy averaged 76.6% in fourth-quarter 2020—a very wide 9.1 percentage points lower than CCRC occupancy (85.7%). Entrance fee CCRC occupancy (88.0%) was 6.3 percentage points higher than rental CCRCs (81.7%), and not-for-profit CCRC occupancy (87.3%) was 6.1 percentage points higher than for-profit CCRCs (81.2%).

CCRCs vs. Non-CCRCs: Care Segment Detail

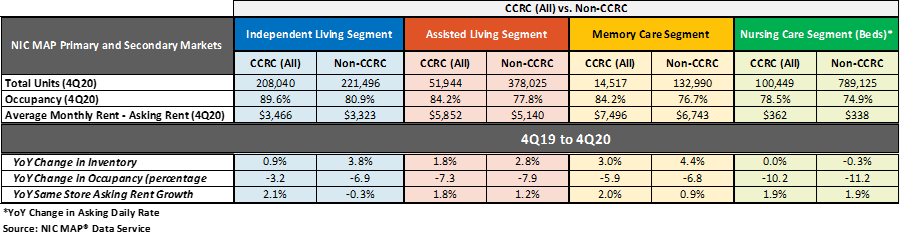

The table below compares each of the care segments—independent living, assisted living, memory care, and nursing care—in the Primary and Secondary Markets. The table shows the fourth quarter 2020 total open units, occupancy, and average monthly asking rent and year-over-year changes for CCRCs and non-CCRCs.

The CCRC independent living care segment (which represents 55.5% of CCRC units) registered the highest occupancy in the fourth quarter of 2020 (89.6%), as well as the least year-over-year drop in occupancy falling 3.2 percentage points. The current nursing care segment occupancy rate in non-CCRCs, which represents 51.9% of non-CCRC units, was much lower at 74.9%, and fell 11.2 percentage points year-over-year.

Higher occupancy at CCRCs

The CCRC independent living care segment had the highest fourth quarter 2020 occupancy (89.6%), followed by CCRC assisted living and memory care (both 84.2%), and CCRC nursing care (78.5%). Among non-CCRCs, the independent living care segment had the highest fourth quarter 2020 occupancy (80.9%), followed by non-CCRC assisted living (77.8%), memory care (76.7%), and nursing care (74.9%).

The difference in 4Q 2020 occupancy between CCRCs and non-CCRCs was the highest for the independent living segment (8.7 percentage points), followed by the memory care segment (7.5 percentage points), the assisted living care segment (6.5 percentage points), and the nursing care segment (3.6 percentage points).

Occupancy declined from year-earlier levels for each of the care segments. However, CCRCs had lesser declines in occupancy than non-CCRCs. Among CCRCs, independent living care segment occupancy declined the least (-3.2 percentage points), followed by memory care (-5.9 percentage points), assisted living (-7.3 percentage points), and the nursing care segment (-10.2 percentage points). Among non-CCRCs, memory care and independent living segment occupancy declined the least (-6.8 and -6.9 percentage points, respectively), followed by assisted living (-7.9 percentage points), and the nursing care segment (-11.2 percentage points).

Higher annual, same-store asking rent growth at CCRCs

Overall, CCRC same-store, year-over-year asking rent growth in the fourth quarter of 2020 was 2.4%, down from the time series high of 4.7% reached in the first quarter of 2019, but slightly higher than the time series low of 2.1% at the end of 2010, the end of 2013, and beginning of 2014. Year-over-year asking rent growth did not vary significantly across the CCRC care segments unlike the non-CCRC care segments; the variation was only 30 basis points for CCRCs but 220 basis points for non-CCRCs. Among CCRCs, the highest year-over-year asking rent growth was 2.1% in the independent living segment; among non-CCRCs, it was highest in the nursing care segment (1.9%). The lowest year-over-year asking rent growth was noted for CCRCs in the assisted living care segment (1.8%); in non-CCRCs, it was noted for the independent living care segment (-0.3%).

Significantly weaker inventory growth at CCRCs

Non-CCRC properties had higher rates of inventory growth (year-over-year change in inventory) by segment than CCRCs, with the exception of the nursing care segment. The highest rates of inventory growth were reported for non-CCRC properties in the memory care and independent living care segments (4.4% and 3.8%); the lowest were reported for both CCRCs and non-CCRCs in the nursing care segment (0.0% and -0.3%, respectively). Negative inventory growth can occur when units/beds that are temporarily or permanently taken offline, or converted to another care segment, outweigh added inventory.

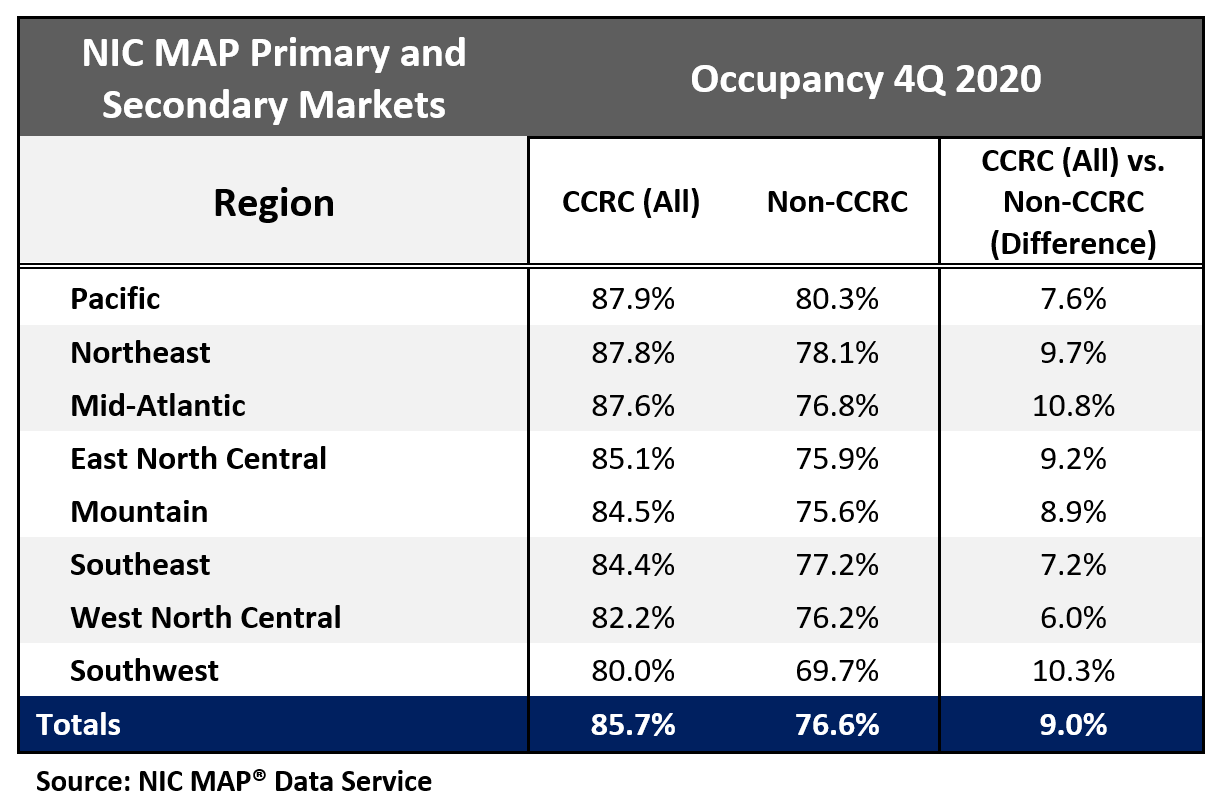

Regional occupancy is highest in the Pacific, Northeast, and Mid-Atlantic

Seniors housing and care communities in the Pacific, Northeast, and Mid-Atlantic regions, which were more significantly impacted earlier in the pandemic than other regions, currently have the strongest CCRC occupancy rates ranging from 87.6% to 87.9%. The weakest CCRC and non-CCRC occupancy is in the Southwest region at 80.0% and 69.7%, respectively. That said, the greatest difference in CCRC and non-CCRC occupancy was in the Mid-Atlantic region—a 10.8 percentage point difference.

Details into the regional performance of entrance fee and rental CCRCs can be found in this NIC Notes blog post.

NIC Boot Camp: Once Again a Hot Ticket

Among all the types of events that NIC offers each year, from NIC MAP® data release webinars, to Leadership Huddles, to the upcoming “NIC Chats” podcast series, the NIC Fall Conference, and many more, one type of event stands out. The latest NIC Boot Camp, slated to kick off in April, sold out within days of opening registration, with the next scheduled for June now open for registration.

These intimate, hands-on learning and networking opportunities are now in their fifth year. They have become so popular that, when registration opens, many of the seats, which are usually limited to around 60 persons, are filled by those wait-listers who had sought to participate in a previous Boot Camp. The workshop, titled “The Art of Assessing a Deal,” has arguably become one of the hottest tickets in the industry, particularly for companies who wish to send professionals new to their roles in seniors housing and care to the best place to get to know the ropes – and begin to network with each other and their distinguished instructors.

NIC Boot Camps are designed to provide these professionals with the opportunity to learn best practices in deal assessment and market analysis from industry practitioners who are experts in their respective subject matter. In pre-COVID times, the Boot Camps were one day affairs, gathering attendees together for eight hours of instruction and small-group work, all in a single conference room. The atmosphere was deliberately intimate and social. This year, NIC has modified the program to suit the needs of professionals accessing it on a virtual platform.

Now spread out over three weeks, the course delivers all eight hours of the in-person Boot Camp, through a combination of both live and self-guided content. In weekly virtual sessions, facilitated discussions enable attendees to analyze real-world scenarios, data, and case-study details, and to collaborate with fellow attendees on that week’s topics. The attendee experience, though virtual, remains a unique opportunity for hands-on learning in an intimate environment, led by seasoned subject matter experts and thought leaders.

NIC is spreading the course out in this way both to minimize its impact on the daily work responsibilities of attendees, and to ensure sufficient opportunities for discussion and interaction with both instructors and peers, but without forcing attendees to sit for a full day on a webcam.

Each Boot Camp also features a keynote presentation given by an eminent industry leader. Former presenters include NIC Co-founder and Strategic Advisor Bob Kramer; John Moore, Chairman and CEO of Atria Senior Living; and, most recently, Principal, RSF Partners, and Chair of the NIC Board of Directors, Kurt Read. Aegis Living CEO Dwayne Clark will keynote the April event.

Seniors housing and skilled nursing Boot Camps are planned as separate events, focusing respectively on their unique qualities and market dynamics. Though separate, each will include a similar series of mini-lectures given by sector leaders with critical experience and practical insights. These deep dives address a wide range of issues facing anyone in the business of assessing seniors housing or skilled nursing investment opportunities.

Presentations cover a lot of ground. Typically, they kick off with an industry overview, featuring the latest NIC MAP® data, presented by a NIC Senior Principal. Other sessions cover case highlights and investment guidance, investment assessment, market assessment, sales and marketing, operational strategy, capitalizing a deal, and valuation modeling.

Each presentation includes opportunities for questions and answers. Just as in the in-person events, attendees are divided into smaller working groups, each carefully balanced to distribute a variety of backgrounds and skill sets, for further discussion – and to team together on the in-depth case study component of the course. Each group will prepare and bid on a property, in a case study based on an actual property. This approach provides not only real facts and figures for attendees to consider, but – after their bids – the benefit of learning what actually occurred and how the resulting deal played out in the real world.

Register now for the June Seniors Housing Boot Camp before it sells out. A Skilled Nursing Boot Camp is planned for September. Those interested in attending future Boot Camp sessions can sign up to be placed on the waitlist to receive further details as they become available.