Lender Fannie Mae Is Open for Business: A Conversation with Roosevelt Davis

In today’s challenging business climate, it helps to partner with reliable institutions staffed by experienced professionals who know the industry.

In today’s challenging business climate, it helps to partner with reliable institutions staffed by experienced professionals who know the industry.

Roosevelt Davis is a good example. He has a deep understanding of seniors housing and care, developed over a long career as a finance professional for the sector. Davis is currently Director, Multifamily Seniors Housing, at Fannie Mae.

Fannie Mae serves the secondary mortgage market as a reliable source of capital for lenders financing multifamily properties, including seniors housing and care properties. Fannie Mae recognizes the critical need to support the financing of housing for the country’s aging population.

Davis joined Fannie Mae in 2008 and previously worked at Freddie Mac on its multifamily and seniors housing team.

NIC Chief Economist Beth Mace recently talked with Davis about Fannie Mae’s role in the industry and its response to the COVID-19 outbreak. What follows is a recap of their conversation.

Mace: What role does Fannie Mae play in financing for the seniors housing market?

Davis: Fannie Mae’s leadership in the seniors housing market spans more than two decades and has long been recognized as a top provider of capital for the industry. We understand seniors housing serves a critical need for our country’s aging population, and that’s why we’ve financed more than $25 billion of seniors housing since 2008.

Our book of business totaled more than $17 billion as of June 30, 2020. Fannie Mae provides secured debt financing for stabilized independent living, assisted living, and memory care properties, and Life Plan or Continuing Care Retirement Communities (CCRCs). We do not provide financing for standalone skilled nursing properties or seniors housing construction loans. We will handle construction take outs, but we do not finance distressed properties.

Mace: What was Fannie Mae’s lending volume in 2019? What share of the seniors housing lending does Fannie represent?

Davis: Our total seniors housing volume in 2019 was $3.05 billion. We don’t have specifics on our share of seniors housing lending, but we have consistently been one of the top seniors housing debt lenders in the country.

Mace: What role do lending partners play in Fannie Mae’s program? Does Fannie Mae do its own underwriting? Who bears the risk?

Davis: Fannie Mae’s Delegated Underwriting and Servicing (DUS®) model is the premiere financing platform in the multifamily market. Because seniors housing transactions are complex, it’s important that we work with DUS lenders who are experienced in financing seniors housing assets. We currently have 17 approved seniors housing lenders in our DUS lender network.

We delegate underwriting and servicing to our DUS lenders. They underwrite, close, and deliver loans to us that meet our requirements. In exchange, they share in the risk on these loans. This offers the borrower certainty of execution, faster decisions, quicker closings, and better pricing. Under the DUS model, Fannie Mae and DUS lenders share in the risk on loans sold to Fannie Mae. We describe this as the Loan We All Own®. It aligns and empowers each of us every step of the way. Approximately one third of the seniors housing credit risk is held by our lenders.

Mace: Do you have your own underwriting team, or do DUS lenders do the underwriting?

Davis: The DUS lenders work on initial underwriting and submit a package to us. The front-end seniors housing production team and credit team review the transaction and gather more input from the DUS lender. We then provide a quote and structure that we’re comfortable with.

Mace: What’s changed from Fannie Mae’s perspective since the COVID-19 outbreak in terms of lending to the seniors housing sector?

Davis: To mitigate risk, we’ve implemented various changes in our credit underwriting stance regarding our analysis of sponsors and operators, properties, and the market outlook. We require reserves of 12 months for principal and interest, with a maximum 60% leverage, and 1.5 minimum debt-service coverage for assisted living and a 1.4 minimum for independent living transactions.

Mace: How have terms changed since the COVID-19 outbreak?

Davis: Prior to COVID-19, we offered 75% loan-to-value and 1.30 coverage for independent living and 1.40 coverage for assisted living. Because of the current uncertainties around cash flow, we now ask for higher debt service coverage and offer lower leverage levels. That helps us mitigate some of the risks of financing seniors housing properties in this challenging environment. Also, we don’t require a 12-month principal and interest reserve escrow for deals with a maximum of 55% leverage and a minimum of 1.7 coverage for assisted living, and 1.6 coverage for independent living.

Mace: Is there a maximum loan size?

Davis: No.

Mace: Has the deal volume dropped since the COVID-19 outbreak?

Davis: We have seen a slowdown for requests for seniors housing loans. In the first quarter of 2020, we financed $608.5 million in seniors housing. In the second quarter of 2020, we financed $250.4 million for a second quarter year-to-date seniors housing total of $858.9 million in volume.

Mace: Is the reduction the result of a slowdown in demand from borrowers or higher standards from the DUS lenders?

Davis: Both. If borrowers don’t need to refinance their properties now, they’re holding back and dealing with what they have to handle at their communities.

Mace: What metrics are you watching?

Davis: We have continued to pay close attention to the operators’ experience and liquidity given that expenses have increased to combat COVID-19. Added expenses include personal protective equipment (PPE) and test kits, sometimes at prices higher than retail due to supply shortages. Other expenses include in-room meal service, cleaning and medical supplies, and premium pay for frontline workers. We want to make sure operators have funds to handle short-term increases in expenses and the slowdown in move-ins.

Mace: Lower occupancies and higher expenses are squeezing net operating income. How are operators addressing that issue?

Davis: Every operator is different; they’re reducing expenses by cutting back on returns to investors, and slashing certain activities and nonessential travel. In some cases, they’re reaching out to their investors for help if a cash infusion is needed. Stakeholders are committed to the industry for the long term and see this as a short-term situation. It’s in everyone’s interest to keep properties operating and keep residents safe.

Mace: What has to happen to get back to “normal?”

Davis: That’s a tough question to answer. The COVID-19 pandemic is unprecedented in our lifetime, and there’s a lot of uncertainty as to its impact.

Mace: What do you like about the seniors housing and care sectors?

Davis: There are several factors that I like about seniors housing and care. First, the long-term demographics—baby boomers are the largest cohort and will need care in the decades to come. Second, the sector is recession resilient. Like all commercial real estate sectors, it has its own business cycle. In past downturns, the demand for seniors housing has been less affected by the rise and fall in unemployment or the expansion or contraction of the economy. But given the unprecedented nature of COVID-19 pandemic, the demand for seniors housing is still uncertain. Third, Fannie Mae plays a key role in providing capital to companies that deliver housing and care to a vulnerable population of society, our elderly.

Mace: What opportunities as well as the challenges do you see ahead for the seniors housing and care sector?

Davis: The slowdown in construction of seniors housing is expected to create some equilibrium in supply and demand in the markets that were overbuilt. Seniors housing also had a labor issue due to low unemployment. I think operators will be able to attract professionals and staff because of the high unemployment rate. The biggest challenge I see is dealing with COVID-19 and its adverse effects on residents, staff, occupancy, expenses, and net operating income. This highlights even more the need for affordable and low-income housing for the elderly.

Mace: Seniors housing has traditionally been viewed as a real estate product. More healthcare is being introduced into the sector because of COVID-19. Does that give you any pause about the further integration of healthcare and housing as we go forward?

Davis: I think it makes the product even more of a needed asset class. People are realizing that their parents and grandparents need that care, and facilities that can provide it are more attractive to them.

Mace: Where is pricing headed? Where will cap rates and valuations be in 12 months?

Davis: It’s hard to know. The lack of seniors housing sales following the onset of the pandemic and the uncertainty of its impact make it difficult to predict cap rates and pricing in the next 12 months.

Mace: Have you considered changing underwriting assumptions on rental growth rates?

Davis: We look at that on a deal-by-deal basis. We conduct an exit analysis on a 10-years basis and make adjustments based on how we think rental rates will be going forward.

Mace: Is Fannie Mae still under conservatorship? What does that mean? Does it affect your operations at all?

Davis: The two government-sponsored enterprises (GSEs), Fannie Mae and Freddie Mac, are still under conservatorship. Our board of directors owes their fiduciary obligations solely to the Federal Housing Finance Agency (FHFA). The GSEs each have a volume cap on multifamily lending of $100 billion from October 1, 2019 through December 31, 2020. The FHFA directs that at least 37.5% of the GSEs’ multifamily business be mission-driven, affordable housing. The volume cap is an important part of how we manage our production. Our paramount goal is to finance a balanced book of business with strong credit quality and meet our mission percentage for affordable housing.

Mace: What else would you like our readers to know and understand about using debt finance through Fannie Mae?

Davis: Despite the challenges the sector faces, Fannie Mae is a reliable source of mortgage capital. The DUS platform for the secondary mortgage market is designed to perform in changing markets. We are in every market, every day.

Thoughts from NIC’s Chief Economist

By Beth Burnham Mace

It’s discouraging and shocking that, as we approach fall, a microscopic virus continues to outsmart us. At the end of July, there were 16.5 million confirmed cases of COVID-19 globally, up from 10.2 million at the time of my last article in late June. And now 149,000 lives have been lost in the U.S., up from 126,000. And sadly, up to one third of those deaths are reportedly in nursing care and seniors housing properties. That said, while the daily number of cases recently being reported is double the previous peak in mid-April, the number of deaths is less than half of its prior peak pace. This may be due to improved treatments and because the average age of those infected is lower than initially.

It’s discouraging and shocking that, as we approach fall, a microscopic virus continues to outsmart us. At the end of July, there were 16.5 million confirmed cases of COVID-19 globally, up from 10.2 million at the time of my last article in late June. And now 149,000 lives have been lost in the U.S., up from 126,000. And sadly, up to one third of those deaths are reportedly in nursing care and seniors housing properties. That said, while the daily number of cases recently being reported is double the previous peak in mid-April, the number of deaths is less than half of its prior peak pace. This may be due to improved treatments and because the average age of those infected is lower than initially.

The only real solution is to find a medical cure and a widely available and replicable vaccine, but the immediacy of that is no sooner than year-end at the earliest. In the meanwhile, we need to implement treatment protocols and therapeutics to try to slow the possibility of death, especially for those most at risk of serious complications. By preventing serious illness at seniors housing and skilled nursing properties, we can slow the need for hospitalizations, freeing up beds for others in crisis. All of us need to follow CDC guidance and common sense by wearing masks and physically distancing. Testing needs to be made more available, and the turnaround time for testing needs to be shortened if it is to be an effective preventative tool. Unfortunately, PPE shortages continue to plague many operators, and contact tracing efforts continue to be nascent. Full attention and diligence toward finding a cure is imperative for the sake of our humanity as well as for the economy.

The Economy. The economy seems to be sputtering after an initial post-lockdown bounce in May and June, when the economy seemingly rebounded, at least to some degree, after the immediate devastation caused by COVID-19 in April. The second consecutive weekly increase in initial jobless claims since late-March in the week ending July 25 has heightened fears that the economy’s recovery has started to go into reverse. Moreover, initial claims have been broadly flat for the past month, at a level more than double the peak seen in the 2008/2009 recession. This suggests that job losses have remained elevated as the initial strong wave of rehiring slows. Moreover, the upsurge in virus cases, especially in the South and the West, presents additional downside risk and could be the underlying cause of the economy’s change in momentum. Statistics from the Federal Reserve Bank of Dallas on mobility and engagement show a flattening in consumer activity in recent weeks. People must feel safe to feel good about the economy and move back toward a business-as-usual behavior. Unfortunately, we are not close to that point.

The way forward is rocky and uncertain and is hostage to the path of the virus and the discovery of a vaccine. Recent re-imposed guidance on mask wearing and physical distancing as well as mandated business closures demonstrate the fragility of the recovery as coronavirus infections continue to climb. In my view, the path forward will take the shape of a “double W” (i.e.,WW), with some sporadic recovery followed by a shallow pause or slowdown, and then further followed by a gradual rebound.

Bifurcated Property Markets. Not all parts of the economy are being equally affected by COVID, and the timing of crises varies across the nation. Similarly, not all properties are performing poorly in the immediate aftermath of COVID. According to the NIC MAP® Data Service, the average occupancy rate for seniors housing in the Primary Markets in the second quarter was 84.9%, down 2.8 percentage points from the first quarter and the lowest level since NIC began reporting the data in 2005. However, the average occupancy masks a lot of detail, including the distribution across individual properties. Indeed, more than one in five properties (22%) in the Primary Markets had an occupancy rate of 95% or higher. Additionally, more than 43% of all properties had occupancy rates higher than 90%. Those properties are more likely to be able to withstand the significant challenges of COVID.

On the other hand, 28% of properties had occupancy rates below 80%, and 40% of properties had occupancy rates less than 85%. These properties will have a more difficult time withstanding the operating stresses associated with COVID, including rising expenses associated with labor and PPE costs as well as slowing revenue streams associated with weaker occupancy rates.

That said, there were fewer properties in the above-95% occupancy category. In the first quarter, a full third of properties were in this cohort; in the second quarter, however, this diminished to 22%. Further, in the first quarter, there were 22% of properties with occupancies below 80%, versus 28% in the second quarter. And, there were 31% of properties with occupancies below 85%, versus 40% in the second quarter. Hence, it is a tale of “multiple property performances,” many of which have deteriorated since COVID struck.

Investment Performance. Like that of many property types, seniors housing investment returns fell in the second quarter of 2020, as the effects of the COVID-19 global pandemic and the utter collapse of the economy took their toll. The total investment return for seniors housing was a negative 1.00% in the second quarter of 2020, according to NCREIF. This was the first negative return since second quarter 2012. The income return remained positive but was the smallest increase on record back to 2003. Meanwhile, the appreciation return was a negative 2.04%, the third consecutive negative return and making the appreciation return a negative 2.43% since fourth quarter 2019. Many investors reduced their appreciation expectations in the first half of the year, as the impact of the coronavirus weighed heavily on their view of the sector.

Comparatively, the total negative return of -1.00% was on par with the NPI, which fell by 0.99%, but was slightly worse than the apartment performance, which dropped by 0.60%. Hotels plunged by a whopping 16.59%, retail by 3.85%, and office by 0.50%. The only sector that did not see declines was industrial, but even there, the appreciation return was negative, albeit slightly (- 0.07%). Note that the performance measurement cited for seniors housing reflects the returns of 123 institutional-quality seniors housing properties, valued at $6.3 billion in the second quarter.

Looking Ahead. At the time of this writing in late July 2020, it is nearly impossible to look ahead with any certainty. The path forward for the pandemic as well as the economy depends upon the path of the virus and the discovery of a replicable vaccine that can be widely distributed across the globe. That said, for seniors housing, strict protocols for visitation, sanitation, and move-ins have been implemented by virtually all institutional investment-grade operators, which has allowed many to begin to open their doors again for new residents. Anecdotal stories suggest that there are waiting lists for many operators, especially for those who operate assisted living. And NIC’s new monthly Intra-Quarterly data suggests that the largest impact on occupancy occurred in the immediate aftermath of the pandemic in the month of April, followed by lesser occupancy declines in May and June. Moreover, NIC’s Executive Surveys indicate that more operators are reporting improvements in both move-ins and occupancy levels.

Nevertheless, revenues, occupancy, and expenses have all taken a toll on margins and NOI and have left many operators challenged. Additionally, costs of borrowing have gone up, insurance premiums have risen, and the threat of re-infections loom large. We are not out of the woods.

Longer term, the general investment thesis for investing in seniors housing remains. This includes the basic need for congregate living settings associated with an aging population, including middle income seniors. Other considerations include the sector’s long-term attractive investment returns (11.79% on ten-year basis compared with 9.70% for the NPI and 9.71% for apartments according to NCREIF data) and portfolio diversification benefits for investors. Additionally, the sector offers compelling and emerging opportunities in both healthcare collaboration and population health management, critical elements to stave off staggering societal healthcare costs. And lastly, there is a better understanding of the sector by institutional capital providers who hold significant amounts of investable and targeted “dry powder” capital.

As always, I appreciate and welcome your comments, thoughts, and feedback.

Virtual Networking Launches at ‘the NIC’

Amidst a historic pandemic, bringing thousands of people together in the fall is not possible. Yet, with a wave of disruption impacting seniors housing and care, it was equally apparent that this year the sector could ill afford to go without the up-to-the-minute data, information-sharing, thought-leadership, and convening power that the event has reliably delivered for decades. NIC, therefore, is executing its upcoming 2020 Fall Conference as a virtual event.

The Essential Virtual Experience

The virtual experience NIC has created offers a number of advantages over traditional in-person events. The schedule is spread over two weeks for convenience, and to minimize conflicts, such as concurrently scheduled educational sessions and the possibility of missing networking opportunities. The focus of the first week will be a full program of educational sessions and thought-leadership. The second will present attendees with opportunities to engage in small group discussions and presentations, focused on building relationships and exchanging information on business and market trends. The event is designed to be spread out and made more convenient for busy executives on tight daily schedules. Because everyone is logging in from home or the office, rather than convening for three jam-packed intense days in person, and because much of the programming will be available on-demand, scheduling can be more relaxed.

Attendees can also expect to be presented with the most efficient and effective networking opportunities in seniors housing and care, even while they attend virtually.

As research, vetting, and careful planning has yielded a clear picture of what attendees expect to gain from an online experience, NIC has developed an efficient platform for seniors housing and care professionals to network and connect. Attendees of the industry’s premier event will be able to seek out opportunities, reconnect with peers, and explore new relationships, particularly during this time of immense challenge and opportunity.

NIC staff have researched available technologies, including the most advanced online meeting and networking platforms, and employed focus groups to help inform a process of developing the most effective and efficient virtual means to deliver quality, substantive opportunities to connect and learn. Virtual work environments are proving to have many advantages, and confidence in the platforms that many now routinely rely upon has quickly grown. This development emboldened NIC to commit to the understanding that, although nothing can replace the experience of in-person networking, it is possible to come close, and even to improve on some aspects of the networking experience, in an online environment.

Welcome to the NIC Community ConnectorTM![]()

The resulting platform is called the “NIC Community Connector,” a proprietary networking tool custom designed to suit the needs of capital providers, owners, operators, service providers, and other stakeholders across the seniors housing and care sector. While launching in parallel with the 2020 NIC Fall Conference, the NIC Community Connector will remain complimentary and accessible to all attendees through the end of the 2020 calendar year. The platform’s subscribers will retain their access to a powerful set of tools that will streamline efforts to identify financing partners, seek property transactions, and build and grow networks.

NIC chief economist Beth Burnham Mace said of the platform, “I view this as a sort of ‘NIC 2.0.’ NIC has been known for connecting people, and this is a means to do so in a virtual environment, which is more and more how people work today and into the future.”

Upon registering for the Fall Conference starting August 5, registrants will be issued usernames and access links to the NIC Community Connector registration form. The information submitted there will be used to create a profile on the platform. NIC Community Connector registrants will then gain access to the platform when it opens on September 9, to search for and message other subscribers as appropriate for their business needs and personal preferences. The secure, carefully populated, and thoughtfully filtered networking tools should provide users with a high degree of confidence and accuracy. Subscribers will be able to access the searchable online database of peers and prospects who have either opted in to being contacted or are identified as being a good match based on their registration profile.

On September 14, NIC will begin weekly downloadable updates of the Conference Attendee Listing, an opt-in list of all attendees registered for the 2020 NIC Fall Conference. The list, which will be available exclusively through the NIC Community Connector platform, will be available to current subscribers until one month after the conference.

NIC plans to add more features post launch, including both public and private groups, which will enable subscribers to communicate beyond messaging. As subscribers engage with the platform, and with each other, NIC staff will closely monitor performance and user feedback. This information will help guide and prioritize further updates and enhancements to the platform. While the NIC Community Connector subscriptions are complimentary for the 2020 NIC Fall Conference attendees through the end of 2020, NIC is planning for paid subscription options, as the platform gains value. Now is a great time to take advantage of the platform at no additional cost, provide feedback via NCCSupport@nic.org, and help shape the future of connecting and growing strategic relationships across the seniors housing and care sector.

Executive Survey Insights

By Lana Peck, Senior Principal, NIC, & Ryan Brooks, Senior Principal, NIC

Designed to deliver transparency into the market fundamentals and gain awareness of COVID-19 incidence among residents and community staff in the seniors housing and care space, the Executive Survey Insights: Market Fundamentals and Executive Survey Insights: COVID-19 are NIC reports developed to provide timely insights from owners and C-suite operators and executives on move-in and move-out rates, changes in occupancy rates, and COVID-19 penetration rates by care segment. Data from these two surveys are collected in alternating two-week periods, and both reports are reported monthly.

- Owners and executives of seniors housing and skilled nursing operators across the nation responded to the surveys. The Wave 9 Market Fundamentals survey sample includes responses collected June 22 to July 5, 2020 from owners and executives of 85 seniors housing and skilled nursing organizations. Wave 2 of the COVID-19 survey includes responses collected July 6 to July 19, 2020 from owners and executives of 52 seniors housing and skilled nursing organizations.

Detailed reports for each “wave” of the survey can be found on the NIC COVID-19 Resource Center webpage under Executive Survey Insights.

Summary of Insights and Findings: Market Fundamentals Survey, Wave 9

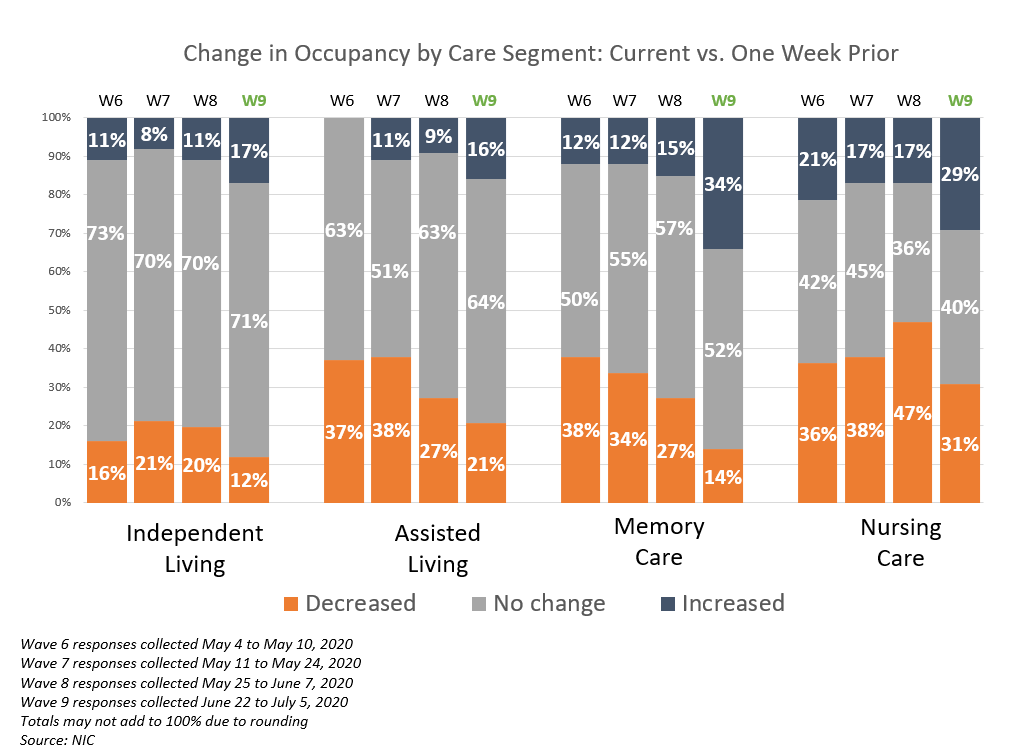

In Wave 9, the shares of organizations reporting an acceleration in move-ins in the past 30-days—across each of the care segments—was the highest in the time series (March 24 to July 5, 2020), while the shares of organizations reporting deceleration in move-ins was the lowest.

- In Wave 9 of the survey, between 36% and 42% of organizations reporting on their independent living, assisted living, memory care, and nursing care segments noted that the pace of move-ins accelerated in the past 30-days. This is the second consecutive wave showing an increase of organizations reporting accelerated move-ins in the past 30-days, and the highest in the time-series, which spans March 24 to July 5. The independent living care segment saw the most growth in the shares of organizations reporting an acceleration in move-ins between Wave 8 and Wave 9 (from 19% to 42%). Comparatively, between 16% to 26% of organizations with independent living, assisted living and/or memory care units, and 33% of organizations with nursing care beds reported that the pace of move-ins decelerated in the past 30-days—the smallest shares reported in the time series to date.

- Reasons cited by survey respondents for either an acceleration or deceleration in move-ins varied. In Wave 9 of the survey—as some state and local governments had lifted COVID-19 contagion spread mitigation measures, prompting some organizations to resume pre-pandemic planned move-ins, just over a third of respondents cited an organization-imposed ban or resident or family member concerns as reasons for slumping move-in rates–the fewest since the survey’s inception.

- As a result, the largest share of Wave 9 survey respondents reported occupancy improvement across all care segments since the survey began. Approximately 80% of organizations with memory care (MC) units, 70% of organizations with independent living (IL) units, approximately 60% of organizations with nursing care (NC) beds, and approximately 45% of organizations with assisted living (AL) units reported an increase or no change in occupancy rates from one-month prior in Wave 9, compared to approximately 50% MC, 45% IL , 40% NC and 50% AL in Wave 8.

- The nursing care segment in Wave 9 shows the highest share of organizations relative to other care segments reporting month-over-month increases in occupancy (42%), presumably caused by elective surgeries having resumed in certain geographies. Furthermore, not shown in the chart, organizations with the highest levels of acuity (memory care and nursing care)—report the most week-over-week occupancy improvement (34% and 29%, respectively).

- About one in ten organizations reported that it is still very difficult to obtain enough PPE/testing kits in most markets. Access to PPE and COVID-19 test kits picked up in Wave 9 compared to Wave 8, however. More than one in three organizations note that access to PPE and COVID-19 test kits improved considerably in Wave 9, compared to approximately one in four organizations responding similarly in Wave 8.

The overall findings of the Wave 9 survey suggest that pent-up demand and the easing of COVID-19 related move-in restrictions freeing up the backlog of pre-pandemic planned move-ins resulted in larger shares of organizations reporting month-over-month and week-over-week improvements in occupancy rates than in all prior waves of the survey. That said, it is important to note that, while most Wave 9 metrics indicate more favorable occupancy trends compared to previous survey waves, the survey data is relative to post-pandemic metrics 30-days ago, not relative to pre-pandemic metrics.

The overall findings of the Wave 9 survey suggest that pent-up demand and the easing of COVID-19 related move-in restrictions freeing up the backlog of pre-pandemic planned move-ins resulted in larger shares of organizations reporting month-over-month and week-over-week improvements in occupancy rates than in all prior waves of the survey. That said, it is important to note that, while most Wave 9 metrics indicate more favorable occupancy trends compared to previous survey waves, the survey data is relative to post-pandemic metrics 30-days ago, not relative to pre-pandemic metrics.

Summary of Insights and Findings: COVID-19 Wave 2

Testing and Current Penetration of COVID-19 by Care Segment

- In Wave 2, the operator average percent of residents tested for COVID-19 (of residents in place on June 30, 2020) for independent living is 18.5%. For assisted living the operator average percent residents tested is 41.7%, and for memory care is 45.7%.

- The operator average percent of confirmed or suspected COVID-19 in independent living is 0.4%. For assisted living the operator average percent is 2.9%, and for memory care is 3.9%.

- In Wave 2, operator average testing penetration for independent living was 18.5%, for assisted living was 41.7%, and for memory care was 45.7%. In both Waves 1 and 2, operator average testing penetration increased as care setting acuity increased.

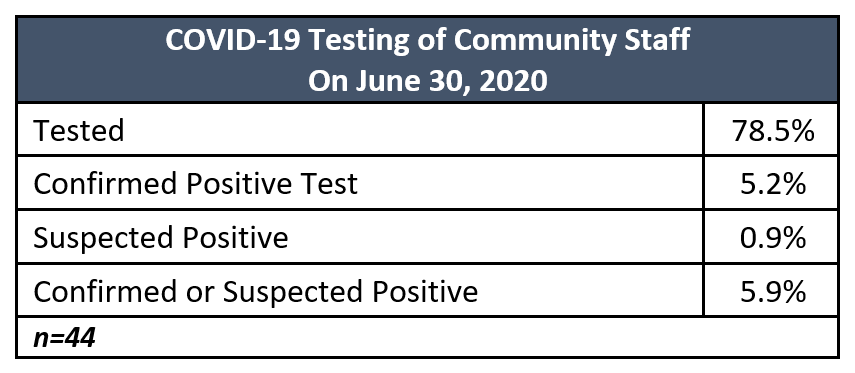

Testing and Current Penetration of COVID-19 Among Community Staff

- The operator average percent of community staff tested for COVID-19 (of staff in place on June 30, 2020) regardless of care setting is 78.5%. Of total staff, the operator average of 5.2% tested positive, and another 0.9% suspected positive, for the community staff operator average penetration rate of 5.9%.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and transparency into the seniors housing and care space at a time where trends are rapidly changing. NIC also thanks to both ASHA and Argentum for their support in encouraging participation in the Executive Survey Insights: COVID-19 survey. The results of our joint efforts to provide timely and informative data to the market in this challenging time have been significant and noteworthy.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and transparency into the seniors housing and care space at a time where trends are rapidly changing. NIC also thanks to both ASHA and Argentum for their support in encouraging participation in the Executive Survey Insights: COVID-19 survey. The results of our joint efforts to provide timely and informative data to the market in this challenging time have been significant and noteworthy.

If you are an owner or C-suite executive of seniors housing and care properties and would like to participate, please click here to access Wave 3 of Executive Survey: COVID-19.

Decline in Skilled Nursing Occupancy Continues in May; Medicare Revenue Per Patient Day Increases

By Bill Kauffman

In response to rapid market changes caused by the COVID-19 pandemic and its impact on the skilled nursing industry, NIC has increased the data release frequency for key performance metrics. NIC will release data on a monthly frequency from its Skilled Nursing Data Initiative. The latest data which was released on July 30, 2020 includes market trends data from January 2012 through May 2020.

In response to rapid market changes caused by the COVID-19 pandemic and its impact on the skilled nursing industry, NIC has increased the data release frequency for key performance metrics. NIC will release data on a monthly frequency from its Skilled Nursing Data Initiative. The latest data which was released on July 30, 2020 includes market trends data from January 2012 through May 2020.

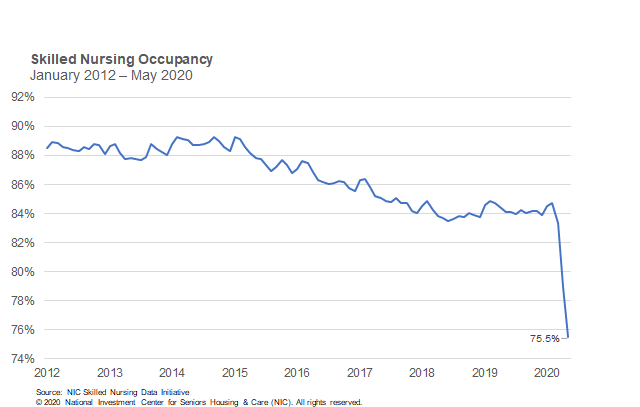

Occupancy

The skilled nursing occupancy rate continued to decline in May due to the impact of the COVID-19 pandemic. Occupancy fell 347 basis points from April to end May at 75.5%. This represents a decline of 784 basis points since March, when occupancy was 83.3%, and is down 921 basis points since February, prior to the pandemic. Year-over-year, the occupancy rate is down 862 basis points from May 2019.

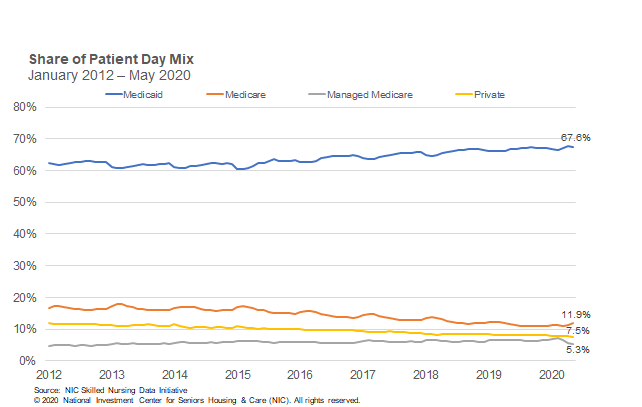

Patient day mix across all four payor types (i.e. Medicare, Managed Medicare, Medicaid and Private) did not see relatively significant movement when compared to the occupancy change from April to May, suggesting admissions decreased across all payor types, except perhaps for Medicare which saw patient day mix uptick slightly.

Medicare

Medicare patient day mix increased 66 basis points from 11.3% in April to 11.9% in May. Since March, it is up 82 basis points. In addition, Medicare revenue mix was relatively steady from April to May, decreasing by only 11 basis points. When compared to overall occupancy, it is likely that the cancellation of elective surgeries continued to have a major impact on Medicare, even as many states have recently started to allow those surgeries to resume. However, Medicare patient days likely did not decrease as much as it would have given that the Centers for Medicare and Medicaid Services (CMS) waived the 3-Day Rule, which waives the requirement for a 3-day inpatient hospital stay prior to a Medicare-covered skilled nursing stay. This enables more patient days to be covered by Medicare, which can have a positive impact on cash flow, all else equal. Meanwhile, Medicare revenue per patient day (RPPD) increased 0.9% from $548.81 in April to $554 in May. Medicare RPPD likely increased because of additional reimbursement due to COVID-19 positive patients requiring isolation, in addition to the temporary suspension of the 2.0% sequestration cuts by CMS, which will be effective from May 1 through December 31, 2020.

Managed Medicare

Managed Medicare admissions are likely still experiencing declines because of COVID-19 even though some states resume elective surgeries, as many may still be hesitant to move forward with surgeries because of the pandemic. Many insurance plan enrollees will also be cared for at home after surgeries, bypassing skilled nursing properties. Managed Medicare revenue mix has declined significantly since February, dropping 307 basis points to 7.3% in May. Since March, it is down 228 basis points. However, Managed Medicare revenue mix held relatively steady from April to May and only declined by 27 basis points. Year over year, it is down 220 basis points from 9.5% in May 2019. Meanwhile, Managed Medicare RPPD increased 0.6% from $453.53 to $456.35 in May. Since March, it has increased by 1.2% suggesting some reimbursement stability from insurance companies during the pandemic. However, year-over-year RPPD is only up 0.4% from May 2019.

Medicaid

Medicaid revenue mix declined 96 basis points from 49.4% in April to 48.5% in May. Medicaid patient days likely decreased as well, due to lower overall admissions in May and some Medicaid patients converted to Medicare given the waiver of the 3-Day Rule. Medicaid revenue mix has declined 240 basis points since March when the mix was 50.9%. Year over year, Medicaid revenue mix decreased 268 basis points from May 2019. Meanwhile, Medicaid RPPD increased 0.4% from $230.30 in April to $231.26 in May. However, there has been an increase of $7.13 RPPD from February, representing a 3.2% increase as states embraced measures to help skilled nursing properties such as increasing reimbursement related to the number of COVD-19 cases at properties. Even with this increase the concern continues to be that current Medicaid RPPD does not cover the actual cost of care in most states.

This analysis and commentary is based off aggregate data from a sample of skilled nursing operators with multiple properties in the United States. NIC continues to grow its database of participating operators in the NIC Skilled Nursing Data Initiative in order to provide data at localized levels in the future. Operators who are interested in participating can complete a participation form here. NIC maintains strict confidentiality of all data it receives.

Forging New Partnerships and Rethinking Operations: Design and Development is Key to the Middle Market Solution: A Conversation with Gaurie Rodman, Director of Strategic Planning and Development Services, Aptura

By Adam Rybka, Vice President, Community Strategy, Longview Seniors Housing Advisors

Gaurie Rodman was a panelist at last year’s NIC Middle Market Investor Summit, sharing her perspective as an operator on successful middle market strategies to date. For more information on NIC’s Middle Market Seniors Housing Study visit here. The following conversation has been edited for clarity.

Gaurie Rodman was a panelist at last year’s NIC Middle Market Investor Summit, sharing her perspective as an operator on successful middle market strategies to date. For more information on NIC’s Middle Market Seniors Housing Study visit here. The following conversation has been edited for clarity.

Rybka: How are you thinking about the middle market from the development side, and are you currently working or involved with any developments or redevelopments aimed toward this cohort?

Rodman: When speaking about the middle market from a developer’s mindset, we need to consider, first and foremost, how we will solve the baseline cost problem. You need to be able to build for about $80K per unit, depending on the market, for the project to pencil out at a middle market rent price point.

In today’s landscape, this is very hard to do given the regulatory environment, construction and land costs. So how do you address that? One way is through creative redevelopment and adaptive use of existing structures.

At Aptura, we are working with our partners on various concepts for the middle market. One of our current projects is the adaptive reuse of a vacant, 1800s schoolhouse into a 60-unit senior living community.

As an industry, we should look to take advantage of Federal, State and Local incentives such as TIFs, opportunity zones, brownfield sites, PILOT programs etc. These sites usually have the added advantage of being located in the vicinity of support services and amenities that can be leveraged for operational efficiencies. Senior Living has traditionally gone to less challenging greenfield sites. As we look to take cost out of development adaptive reuse, brownfield or distressed sites with public incentives to develop can become an important part of the solution.

Rybka: As we look at the industry, it appears that we are still in the early days with various groups trying to figure out the middle market product and slowly putting their theses to work. How is the design for a middle market product different than some of the new properties that have hit the market over the last few years? What needs to occur to hit that per unit development cost?

Rodman: When looking at a true middle market product, you must start by taking all the pieces apart and first start with the unit itself and the unit size, as this ultimately drives the size of our community. We must be far more focused around this basic building block. The apartment still needs to be inspirational for someone to move in, and so as we tighten the footprint from a design aspect, you need to add more amenities at the same time – an example of this is going with a smaller unit size, but then incorporating much larger windows, and perhaps a Juliette balcony, allowing for more natural light and enhancing the space.

Senior living also needs to do a better job of looking at rentable and non-rentable space, much like an office developer, and reduce the overall building size for the middle market product, taking into consideration the potential design and construction savings. My personal theory is that most amenity spaces within the middle market product should be multi-purpose, and we should never have a single-use space. A prime example of this is your typical lobby which can serve as a gathering space and coffee bar in the morning, a grab-and-go bar midday, ice cream parlor in the afternoon, and finally a wine bar and happy hour space in the evening.

A salon, which is expensive to build as it needs proper ventilation, electricity, and plumbing could have an outside entrance generating lease revenue and be utilized throughout the day. Then we also need to give thought to other spaces such as theater rooms, and if they are actually needed in today’s era. Every space needs to be looked at through this creative lens and scrutinized for the middle market product, and all of this starts by evaluating the programming first.

Rybka: We start with design and building configuration, but what else do we need to do as an industry to solve the middle market problem?

Rodman: Affordability is the fundamental problem with the middle market. To solve the problem, we will need a shift in the operational and programming mindset and

seek out partnerships to aid with new operational models that bring select services in from the outside. We also need to rethink where and how we develop, while receiving

support from the regulatory side to ensure that the rules align with the new designs and operational models. The middle market solution is thus not a singular solution. With

the demographic trends, we will continue to face staffing challenges, and part of the equation in the middle market solution also potentially lies around the ability of the

senior resident to be part of the economic and operational structure of the community. Ultimately, the middle market solution cannot be an incremental change; it must be a transformational change.

Rybka: Can you expand on some of those middle market opportunities? What are some of the ways to change the operating model?

Rodman: We know that the middle market will be a large cohort, but how and when they come is yet to be determined. There is an opportunity for creativity, especially with the speed at which we capture and attract people earlier in the life cycle to a congregate living community, versus waiting until the residents are very frail.

Part of the solution is creating a product for a more active adult resident, who can then age in place, adjusting the operating model to provide the needed care throughout the resident’s life cycle. Looking outside the box, that active adult can also potentially become a part of the operational model and serve to provide certain services currently provided by staff members.

With that said, partnerships are going to be very important because operationally we might not be able to be everything for everybody. We need to re-knit senior living into the fabric of our communities, because right now senior living tends to stay in isolation on a five or six acre piece of land that provides everything for itself from care to food services. Instead, we should start thinking about the housing piece separately and partner with a network of vendors to provide some or part of those services or activities, thereby reducing development costs and changing the operational model. To capitalize on this will require taking a hard look at where you are located within a community, and the proximity to the physician’s office, grocery store, restaurant, or salon.

Rybka: You touched on amenity spaces previously. How are you envisioning the dining experience within a middle market product?

Rodman: The senior industry, I believe, should anticipate a higher expectation of variety from our seniors. They will demand more variety, more choices, fresher and more farm-to-table services. Residents will be coming into senior living used to food delivery through vendors such as Uber Eats. What does that mean to an operating model that currently anticipates serving three meals a day within the community?

As I mentioned before, partnerships will be critical to serve the needs of the senior population, and the same applies to leveraging partnerships with local restaurants. Designing more outdoor spaces to provide outside programming is another way, such as allowing a food truck to deliver a portion of the meals to the community and increasing variety at the same time. If you can provide 20% of the meals with a food truck, what does that do to the size of the dining room or the commercial kitchen? We should take a hard look at the kitchen, if it can be shared onsite or offsite with local restaurants, or if it is needed to begin with. By removing part of the kitchen or dining room, or tightening the space, you can ultimately reduce your development cost and significantly impact your operational model. At the same time, however, you now need to think about hiring a community liaison to assist with the planning portion and ensuring you always have a back-up plan.

Rybka: Does COVID change how we think about the middle market product and approach to design?

Rodman: We have looked at this in the context of how operators have responded to the pandemic issue today and how the building design should support operations. We bucket this into three categories that are applicable to a typical senior living and middle market design alike:

- In the case of a pandemic, how can we keep the virus out of the building? With that the entry point becomes the first line of defense. We need to start thinking about features such as automatic doors, automated temperature and health screenings, and areas close to the lobby or entry points where staff and individuals can change their clothes and put on their PPE.

- If an outbreak does occur, how do we deal with it within the building and manage the resident population? Forward thought should be given to the creation of isolation units that can be segregated and self-sustained as needed. One approach within the middle market product is smaller, more efficient multi-purpose ecosystems within each wing in lieu of a larger one-use venue. The use of materials that reduce transmission of bacteria, mechanical and ventilation systems, and other technologies that will allow for healthier environments and provide operational efficiencies also become critical.

- Social engagement, which we know is important to maintain the wellbeing of a frail resident population. How do residents engage with family and each other and circulate throughout the building? As an example, when thinking about unit configurations (smaller but more efficient footprints), designing spaces with a vestibule or bathroom close to the entry point is essential. In this manner, the care aide or home-health worker can wash their hands before walking into the residential portion of the apartment, thereby mitigating infection spread.

Many of the strategies for building reconfiguration in response to this pandemic will have interesting implications for the design of a middle-market product. The ultimate solution will inherently be tied to an operational transformation which will leverage partnerships and technology to create safe environments for purposeful aging. Any proposed new middle market facility location, design and construction will need to adapt to these operational changes.