Building Design in the Age of COVID-19: A Conversation with Architect David Segmiller

Building design takes its cues from market trends, and senior living is no exception. The fallout of the COVID-19 pandemic and its significant penetration amid the older population will impact project design for years to come.

Building design takes its cues from market trends, and senior living is no exception. The fallout of the COVID-19 pandemic and its significant penetration amid the older population will impact project design for years to come.

That’s the view of architect David Segmiller, who recently discussed design trends with NIC Chief Economist Beth Mace. Segmiller directs the senior living practice at Hord Coplan Macht in Charlotte, North Carolina. The firm’s clients include names such as Erickson Living, Life Care Services, and Brightview Senior Living.

Segmiller is an expert in design for an aging population. He has taught and lectured on the topic and has been deeply involved in industry organizations. Segmiller is a former chair and founding member of the Urban Land Institute’s Senior Housing Council.

What follows is an edited version of their conversation.

Mace: David, can you tell us about yourself and your role at Hord Coplan Macht?

Segmiller: I’ve had a long career in senior living design at several different firms. I grew up in the CCRC world when senior living first emerged among nonprofit sponsors. Since then, I’ve worked with for-profit clients as well. I joined Hord Coplan Macht last September. I am back working with a lot of the same professionals I knew when I worked in Baltimore for 20 years.

Mace: You’ve been involved in architecture and design firms for your entire career, with a specialization in seniors housing. What are some of the changes that you’ve seen?

Segmiller: Early on, the industry was mostly CCRCs (now referred to as Life Plan Communities), and the formula was simple. There was independent living and nursing care. Assisted living was becoming another level of care, and we did not yet segregate for memory care. Residents who needed more care had to have home care or move to the nursing home even if they didn’t belong there. The levels of care emerged over time and the housing model changed. The changes have been market driven. We’ve gone from serving the Greatest Generation, which was more formal, to today’s seniors who are more casual. For example, there was a time when communities had one dining room and everyone got dressed up for dinner. Now we have multiple dining venues and more casual options. The industry has changed a lot over the years.

Mace: What other design changes have you seen?

Segmiller: To appeal to the wealthier Silent Generation, apartments have gotten bigger and communities have more amenities. We’ve moved away from staff service areas. We used to have locker rooms, but nobody used them; and now we are thinking about putting them back in because of the COVID-19 outbreak.

Mace: How do you think the pandemic will affect design going forward?

Segmiller: I’ve talked to CCRC leaders, and they’re being flexible about how to use space. They’re taking activity space that isn’t being used and turning it into areas where staff can change into scrubs for work. Another change we’ll probably see is an external living room that allows residents to have visitors without entering the building or being in close physical contact. It’s not a huge cost, and we don’t have to build more rooms; though in the north it might have to be an interior space. The biggest issue for residents and their families is how to deal with isolation. I wrote a white paper about this, and most CEOs do not want to change the social aspects of their communities because that’s a selling point and why people move there.

Mace: What can operators do to retrofit/modify/alter existing building infrastructure in a COVID world?

Segmiller: Besides adapting existing spaces, all visitors should be funneled through one entrance or two at most to control access and conduct screening.

Mace: What about HVAC systems?

Segmiller: Most systems mix tempered inside air with fresh air brought into the building. That’s good. But I don’t think we’ll go as far as hospitals with ventilation systems that control airflow to prevent infection spread. That’s expensive. But we will pay more attention to air exchange especially in skilled nursing and other situations where residents don’t have as much access to fresh air. That is the critical issue. We’ve talked about retrofitting ultra-violet light in ductwork to treat the air. But so far, we have not seen that this virus moves through ductwork. We have a project now that is evaluating things like ultraviolet light and other means of infection control before it starts construction.

Mace: What else can be done?

Segmiller: Surfaces can be treated with antimicrobial coatings. But every day we hear different things about the virus. It may not be transmitted so easily by surfaces. So how much do you spend on antimicrobial surfaces? How far do we have to go, and how much do we have to spend to keep the virus from moving around easily? That’s what we are trying to figure out.

Mace: What about elevators? How do you keep them safe?

Segmiller: We can use antimicrobials coatings and touch-free systems. Voice-activated technology is coming out. It’s not mainstream yet, but its introduction may be accelerated by the pandemic. The problem with elevators is that, for the short term, we might have to limit how many people can be together in one car.

Mace: Elevators tend to be the jam point. Will buildings add more elevators?

Segmiller: Maybe. But adding an elevator is expensive. It could add $50,000 or more per elevator to building costs which ripples through the pro forma forecast and rent rates. We must figure out what makes sense.

Mace: Is there one new design feature that will last after COVID-19?

Segmiller: This virus is way beyond any flu, much worse and more intense. We need plans to deal with a pandemic. We need to design with that in mind from a flexibility standpoint. How can we set up spaces to be multi-use if there is a lockdown? Where do we store personal protective equipment (PPE)? Is it better to add a big room or rent storage space off site? A lot depends on what is mandated, and PPE has a short shelf life. As I mentioned earlier, we also need a way for families to visit without coming inside the building.

Mace: Will projects have isolation wards?

Segmiller: It may be considered for a section of the nursing center. It’s possible to create neighborhoods and designate one as the isolation ward. We do that already for hospice patients. It could be a selling point to be able to isolate people and keep them safe, but it’s a matter of how much to spend. We may create rooms capable of isolation in nursing, or a wing, but not the majority of the building.

Mace: What housing model seems to control infection best?

Segmiller: I recently attended a conference by the Green House Project. It offers a small group home experience as an alternative to the traditional nursing home. The Green House COVID-19 infection rates are low because the small houses don’t have as much staff and residents can be isolated easily in the stand-alone houses. But is the small house model affordable to the vast population who needs it? Is the government going to offer more reimbursement? How do you find a compromise to make that work? Semi-private rooms make more financial sense to serve less affluent markets, but that limits infection control.

Mace: There continues to be a discussion about the social versus the medical model in seniors housing. Now in response to the pandemic, the question of safety and healthcare has been pushed top and center. How do you design to take into account all these considerations?

Segmiller: A lot depends on the housing model. We still expect to see different products, whether it’s stand-alone independent or assisted living, a combination of those with memory care, or a Life Plan Community. Some providers are licensing their entire buildings for assisted living, which is a very popular approach now. These projects are more adaptable in a pandemic. The least adaptable projects are the lower market nursing homes. The virus is hard to control without enough PPE and a lot of staff turnover.

Mace: How will new designs impact costs? Are developers willing and able to manage the costs?

Segmiller: Projects under construction have continued, but the pipeline is shaky. Projects that were on the drawing board are on pause. Equity is willing to commit funds, but lenders are stuck. They’re not willing to dive into a piece of property until they know what COVID-19 will do and how long the project might be tied up. We’re not landing as much work, but that could change on a dime if banks become more willing to lend.

Mace: What about construction costs and labor trends?

Segmiller: We haven’t seen cost of materials come down. It’s too early. Prices are being driven by the cost of commodities which can be hard to get. We probably won’t see construction cost reductions until late summer as the work pipeline slows. There’s also labor risk if workers don’t show up at sites.

Mace: In recent years, there’s been a movement toward locations that are closer to dense urban centers and away from the suburbs. Will this continue?

Segmiller: Most early CCRCs were built by religious organizations on outlying land. Now everyone is looking for urban infill sites because people want to be able to go to a nearby store or restaurant. I can’t imagine people wanting to be isolated. But it depends on how long this health crisis lasts. We’re doing a paper on intergenerational living and that will be an important community component going forward. We’re social animals, and that won’t change.

Mace: Do you have any projects underway now?

Segmiller: We are drawing projects slated to start next year, but some senior living developments are on hold. Our healthcare and school practices are busy. The multifamily sector has been impacted the most amid uncertainty over rents because of mandated tenant protections.

Mace: What advice/insights do you have for operators and developers today?

Segmiller: We already design flexible buildings, and they’ve held up pretty well in the pandemic. We may see more of the small house model for nursing care if we can afford to serve a larger share of the population. The big issue moving forward is how to make our products more affordable to accommodate more seniors. The pandemic has made that harder. We may need more square footage to deal with issues related to PPE, screening, and the needs of the staff.

Mace: Do you think that these changes will affect investor interest in the sector?

Segmiller: Investors haven’t changed their viewpoint on the market. Buildings can’t solve all problems, but they need to be flexible enough to handle whatever comes along, including a pandemic.

Mace: Looking in your crystal ball, where do you see the industry a year from now?

Segmiller: We’ll find a way to deal with this as a society and figure out how to keep each other safe. A lot depends on developing effective therapeutics and a vaccine. I think senior living will get over the recent wave of negative press which has already slowed down some. The growth of the aging population will continue to drive senior living. I’m usually an optimist. A year from now, I think we’ll be back to where we were before the pandemic hit.

Executive Survey Insights: COVID-19

By Ryan Brooks, Senior Principal, NIC

Wave 1, Data Collected 6/9/2020 – 6/21/2020

Wave 1, Data Collected 6/9/2020 – 6/21/2020

A NIC report to provide insight into COVID-19 among current residents and to more clearly understand existing conditions by care setting.

NIC’s monthly COVID-19 Executive Survey of seniors housing and skilled nursing operators is designed to bring awareness to the operators, their capital providers and business partners, and the general public, on the current COVID-19 penetration rates by care segment. Providing data on current penetration rates gives perspective on how the sector has adapted in the five months since COVID-19 was declared a pandemic. Providing data by care segment enables insights into how COVID-19 has impacted the different populations within each care segment, which vary substantially in levels of health.

The initial survey (Wave 1) for data on May 31, 2020 includes responses collected June 9 to June 21, 2020 from owners and executives of 105 seniors housing and skilled nursing operators from across the nation. Detailed reports for this wave, along with other survey findings can be found on the NIC COVID-19 Resource Center webpage under Executive Survey Insights.

Summary of Insights and Findings

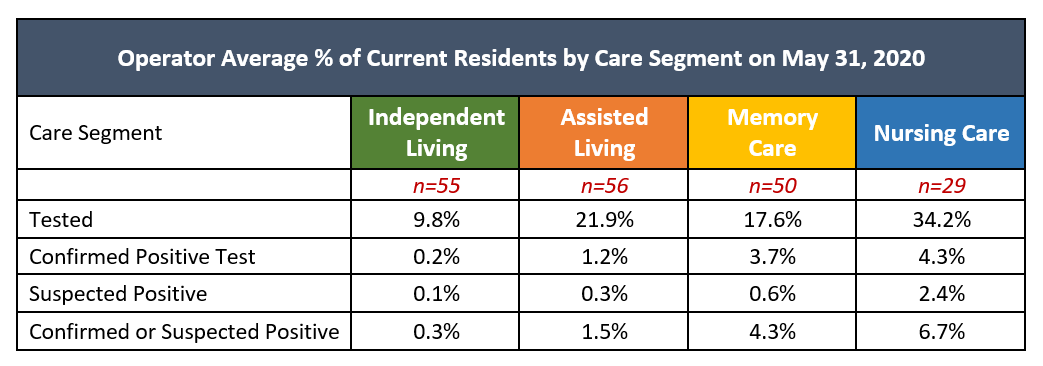

Data collected in a survey of seniors housing and care operators by NIC shows average COVID-19 penetration among current residents varies by care setting, ranging from 0.3% in independent living to 6.7% in nursing care.

Data also shows COVID-19 testing varies by care segment, with an operator average ranging from 9.8% in independent living up to 34.2% in nursing care.

Key Findings

Testing and Current Penetration of COVID-19 by Care Segment Respondents were asked: “Distributed into the following categories, the total number of my organization’s (independent living, assisted living, memory care, nursing care) residents were: 1) Tested for COVID-19 with a PCR test, 2) Laboratory confirmed positive PCR test, and 3) Suspected COVID-19”

- The operator average percent of residents tested for COVID-19 (of residents in place on May 31, 2020) for independent living is 9.8%. For assisted living, the operator average percent residents tested is 21.9%, and for memory care is 17.6%. The care segment with the highest resident testing is nursing care at 34.2%.

- The operator average percent of confirmed or suspected COVID-19 in independent living is 0.3%. For assisted living, the operator average percent is 1.5%, and for memory care is 4.3%. The care segment with the highest average percent of confirmed or suspected COVID-19 is nursing care at 6.7%.

Demographics

- Responses were collected June 9 to June 21, 2020 from owners and executives of 105 seniors housing and skilled nursing operators from across the nation.

- More than one half of respondents were exclusively for-profit providers (62%), 28% of respondents were exclusively nonprofit providers, and 10% operate both for-profit and nonprofit seniors housing and care organizations.

- Owner/operators with 1 to 10 properties comprise 52% of the sample. Operators with 11 to 25 properties make up 22%, while operators with 26 properties or more make up 26% of the sample.

- Many respondents in the sample report operating combinations of property types. Across their entire portfolios of properties, 57% of the organizations operate seniors housing properties (independent living, assisted living and memory care), 21% operate nursing care properties, and 22% operate CCRCs (aka life plan communities).

Methodology

Answering on behalf of their organizations, seniors housing and care owners and executives provided the COVID-19 incidence data as of May 31, 2020 shown above. The data is self-reported, non-validated, and based on a convenience sample.

Data is reported as operator averages to prevent the skewing of data that can be caused by larger-sized operators. Operator averages are obtained by first calculating rates for each operator survey response and then taking an average of those rates across the sample.

Public Data Reporting

Public data for COVID-19 cases in America’s long term care properties, a category consisting of skilled nursing and, in some geographies, assisted living properties, has been largely cumulative, providing a growing number of COVID-19-positive and suspected cases. These data do not include information on independent living nor differentiate between assisted living and memory care settings. The cumulative data does not provide insight into how changes in visitation policies, improved access to PPE and other resources, increased testing, and resolution of early COVID positive tests have impacted current residents.

NIC’s Executive Survey Insights: COVID-19 data provides a “snapshot in time,” capturing benchmark data on residents by care setting on May 31, 2020. NIC collected and analyzed “active case” data among current residents, provided by 105 seniors housing and care operator companies. While the survey, which NIC plans to update monthly, will require a larger number of respondents to achieve a more representative data set, this initial release provides useful insights that complement existing public data.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and transparency into the seniors housing and care space.

If you are an owner or C-suite executive of seniors housing and care properties and have not received an email invitation but would like to participate in the current Executive Survey, please click here for the current online questionnaire.

Thoughts from NIC’s Chief Economist

By Beth Burnham Mace

July. Five months into the pandemic 130,000 lost lives in the U.S. as of July 6, 11.5 million confirmed COVID-19 cases globally. 126,000 lives lost in the U.S. as of June 29, with up to one third of those reportedly in nursing care and seniors housing properties. Recent data collection and analysis from NIC shows that the incidence of confirmed or suspected COVID-19 is higher in nursing care properties than in independent and assisted living properties.

July. Five months into the pandemic 130,000 lost lives in the U.S. as of July 6, 11.5 million confirmed COVID-19 cases globally. 126,000 lives lost in the U.S. as of June 29, with up to one third of those reportedly in nursing care and seniors housing properties. Recent data collection and analysis from NIC shows that the incidence of confirmed or suspected COVID-19 is higher in nursing care properties than in independent and assisted living properties.

Unfortunately, instead of receding, total confirmed cases in the broad U.S. population are on the rise again, led by states that have “re-opened” and the newly vulnerable now include more than just the elderly as younger individuals are also testing positive for the virus. The path forward is ambiguous as the virus seemingly does not succumb to human hopes and desires as evident by the recent upswing in nationwide cases. The only real solution is to find a widely available replicable vaccine and the immediacy of that is no sooner than year-end, at best. The path between now and then will need to be carefully considered by all of us at the individual level as we consciously consider how much exposure risk is acceptable for every single choice we make when we leave our homes.

That said, life does and must go on. This is nowhere more evident than in the seniors housing and care industry which, unlike many other industries, has remained open during the entire pandemic. Containment, safety, and care considerations have been top-of-mind for virtually all operators and their capital partners. Forward momentum now exists for tried, true, and tested protocols that safeguard residents and staff against this pernicious viral enemy. These include suppression, sanitation, and protection protocols such as limiting the number of staff members assigned to any one person, promoting dining and other community activity guidelines that simultaneously support socialization and social distancing, creating outdoor visiting areas and living rooms, introducing robotic sanitation utilization, telehealth, ubiquitous use of iPads and mobile apps, modifying ventilation systems and more. Communications strategies have also become a key mitigant to combating media headline risk and fear—transparent communication to family members, staff and residents about the status and condition of COVID at the property and organization level. Meanwhile, restricted visitation and virtual tours have been imposed at many properties, and PPE is also significantly more available today than in March, although shortages still do exist. As a result of these efforts and lessons learned, our industry is much better prepared for the existing ongoing viral outbreak or even a second wave, should that occur.

Move-ins. Based on NIC’s Executive Survey Insights, operators are gradually opening the doors for new residents as they remove self-imposed closures to new residents. Openings are not casual, however, with well thought out, scripted, and choreographed measures in place to test and quarantine new residents should that be warranted. The incidence and prevalence of the disease has not been uniform, so admission strategies occur at the property level, with attention being paid to negative COVID-19 test results for residents and staff, federal and local government-mandated guidelines related to social distancing, and downward COVID testing trends seen more broadly in the local communities. The inconsistent patchwork of government rules is challenging for operators with properties in many states, however. Hopes for robust contact tracing protocols are also an area of focus but seem more aspirational than reality at this point.

The expectation is that as move-in rates gradually advance, occupancy levels will follow suit. In fact, some operators may experience a nice pop in occupancy rates as they open to new customers and as many operators are reporting expanding waitlists. However, the recovery rates may not be fast enough for all operators since many properties had low occupancy rates going into the pandemic. According to the NIC MAP® Data Service, 22% of all properties within the NIC MAP Primary Markets in the first quarter of 2020 had occupancy rates below 80%. These properties likely have been challenged by the combination of rising expenses associated with labor and PPE costs and slowing revenue streams associated with declining occupancy rates. On the other hand, 50% of properties had occupancies greater than 90% in the first quarter and 33% of properties had occupancy rates higher than 95%. Operators of these more fully occupied properties likely have been better able to withstand the NOI pressures associated with COVID-19.

The Economy. COVID-19 has been a direct assault on operators of senior housing and care properties, taking immediate and initial aim at vulnerable seniors. However, the virus has also assaulted the economy. Indeed, the economic impact of the pandemic has been unprecedented with whole industries and economies shattered, massive numbers of workers laid off, and the thousands of businesses teetering on the edge of bankruptcy and failure. The jobless rate surged to 14.7% in April in the immediate aftermath of the pandemic from 3.5% in February (subsequently, it slipped back to 11.1% in June, while first quarter GDP contracted by 5.0%, with expectations of a further drop of 30% or more at an annual rate in the second quarter.

The way forward is rocky and uncertain and is hostage to the path of the virus and the discovery of a vaccine. Government actions to date—both fiscal and monetary—have been successful in taking the sting away for many, but the lasting toll of the economic shock will be extreme for many persons and businesses for years to come.

The shape of the recovery has been a discussion point for many analysts. However, the much-preferred V-shape recovery path, which represents a severe drop in economic activity followed by an equally quick rebound in economic activity is rapidly fading from view as the virus rears its head across many states that had been initially minimally infected. In my view, the shape of the recovery is elongated and gradually rising like the Nike swoosh logo or an elongated W-shape, with an initial pop in economic activity to be followed by a slowdown as the benefits of extended unemployment insurance (currently scheduled to expire at the end of July) and the one-time $1,200 government stimulus check dissipate. Fed Chair Jerome Powell continues to reiterate that the Federal Reserve remains committed to using all its tools to support the economy, but, in recent testimony, he noted that: “The path forward will also depend on the policy actions taken at all levels of government to provide relief and to support the recovery for as long as needed.” This is a direct plea for additional fiscal support. The Fed continues to indicate that there is great uncertainty surrounding the economic outlook, traceable to federal government activity, and the coronavirus itself.

Wrapping Up. In summary, the double whammy of the direct effects of the coronavirus on seniors combined with the effects of a historic contraction in economic activity pose unprecedented challenges to the seniors housing and care industry. Revenues, occupancy, and expenses have all taken a toll on margins and NOI. However, capital is not stepping away and has been hand in hand with operators as they strive to protect and support residents and staff. In the near-term, there will be openings for opportunistic and value-add investors who either purchase, recapitalize or reposition troubled properties. With continual assurance from the Federal Reserve that interest rates will remain low for the foreseeable future, the cost of capital will also be attractive and support growing transaction volumes. As investors make choices on how to build and grow accretive portfolios, seniors housing stands out with its underlying favorable demographics, especially in comparison to COVID-related uncertainty associated with office, hotel, and retail commercial real estate properties.

As always, I appreciate and welcome your comments, thoughts, and feedback.

NIC Fall Conference Goes Virtual

The Premier Event Offers Convenience, Thought-Leadership, and Connections—Online

For thousands of senior decision-makers across seniors housing and care the annual NIC Fall Conference is the “go-to” event worthy of booking flights, traveling, a hotel stay, and three days of intense networking, meetings, breakout sessions, and deal-making. The conference routinely receives high marks from attendees, particularly when they are asked about its impact on their businesses. In short, “the NIC,” as it has become known by many returning attendees, is the industry’s premier event. Amid the global COVID-19 pandemic, however, times have swiftly changed, rendering an in-person gathering of thousands not possible this fall. But the good news is that the quality and business value of the 2020 NIC Fall Conference, subtitled “the essential virtual experience,” promises to remain as compelling and impactful as ever, if not more so.

For thousands of senior decision-makers across seniors housing and care the annual NIC Fall Conference is the “go-to” event worthy of booking flights, traveling, a hotel stay, and three days of intense networking, meetings, breakout sessions, and deal-making. The conference routinely receives high marks from attendees, particularly when they are asked about its impact on their businesses. In short, “the NIC,” as it has become known by many returning attendees, is the industry’s premier event. Amid the global COVID-19 pandemic, however, times have swiftly changed, rendering an in-person gathering of thousands not possible this fall. But the good news is that the quality and business value of the 2020 NIC Fall Conference, subtitled “the essential virtual experience,” promises to remain as compelling and impactful as ever, if not more so.

Registrants will immediately observe that many aspects of the conference remain the same. As in previous years, Main Stage sessions feature prominent national figures and Washington insiders, discussing issues of the highest relevance to the industry. With an important national election only weeks away, confirmed speakers for the 2020 NIC Fall Conference include the host of “Matter of Fact,” Soledad O’Brien; political pundit, author, and New York Times columnist, David Brooks; and political commentator, and author, David Gergen. Andy Slavitt, senior advisor for The Bipartisan Policy Center and former Acting Administrator of the Centers for Medicare and Medicaid Services will share his insights. Main Stage sessions will plumb the expertise to help attendees understand what to expect – and what is at stake for their businesses – as November 3rd quickly approaches.

Many other aspects of previous, in-person events remain. Attendees will be able to choose from a program of over 30 sessions, featuring relevant, timely topics and 50+ industry experts and thought leaders. Our popular NIC Talks series returns – featuring innovative thought leaders and experts who will share insights and perspectives about how the future of aging and aging services will be impacted by COVID-19. The latest NIC data will be available, along with expert analysis and insights. Over 25 highly relevant, timely, and thought-provoking topics will be covered.

The program, as in previous years, is split into three tracks, covering topics in seniors housing, skilled nursing, and senior care more broadly. Operators and capital providers will find that the program is still divided into two focus areas, appropriate to their business needs: Managing Margins, which provides insights on operational strategies, property operations, and management; and Realizing Returns, focusing on capital markets, property investments, and capital flow subject matter. Importantly, NIC has put a great deal of effort into planning sessions that promise to present as engaging and interactive an experience as today’s technology will allow – which is considerable.

Participating in the event via a digital platform offers advantages that busy executives will find highly attractive. Understanding that many attendees value the event for its unique networking opportunities, NIC’s events team has placed a priority on delivering real opportunities to build and grow relationships, seek and connect with potential business partners and transactional providers, and experience high quality interactions on relevant subject matter in real-time. The conference will leverage the latest technologies to offer new ways for capital providers, senior living owners and operators, and service providers to connect with each other online.

Another advantage of the virtual experience is that it can be spread out and made more convenient for busy executives on tight schedules. Because everyone is logging in from home, rather than convening for three days in person, scheduling can be more relaxed. The traditional event crammed breakout sessions, general sessions, networking events, special receptions, and a variety of break-time activities all into an extremely busy three days. This fall, attendees can review a schedule spread over two weeks.

The first week is devoted to educational programming, running from Tuesday, October 6 to Thursday, October 8. “Business Education Week” offers three days of virtual networking, from Tuesday, October 13 to Thursday, October 15. In focus groups and surveys, regular attendees of the NIC Fall Conference are expressing excitement at the prospect of being able to attend networking and educational opportunities that they otherwise might miss. Whereas the traditional in-person event sometimes forces attendees to choose between a networking opportunity or a meeting slot and a programming session, this approach enables attendance and participation in both aspects of the conference.

Perhaps the most important advantage of the 2020 NIC Fall Conference will be its reduced price, which NIC hopes will encourage companies and executives to register their extended teams for the event. The virtual platform offers an opportunity for analysts, managers, executive directors, service providers, and other decision-makers to gain valuable industry insight, network with peers, and help get the most out of the event for their businesses.

As this historic pandemic continues to impact markets, drive disruption, and accelerate change across myriad socio-economic factors, the need to adapt and stay ahead of trends may be the new normal. While ‘the NIC’ Fall Conference is virtual, the need for the latest data, thought-leadership, strategic insights, and connections, is as real as ever. Don’t miss this unique opportunity to stay ahead of the disruption. Look for “early bird” notices in email and on the nic.org events page. Secure your access early to take full advantage of all the conference has to offer.

Impact of COVID-19 on Lending Practices Today: A Conversation with Sarah Anderson, Managing Director, Newmark Knight Frank and Austin Sacco, First Vice President, CBRE

By Sarah Peerson, Vice President, Senior Housing Finance, Wells Fargo

While there was some uncertainty in early March surrounding any impact that might be associated with COVID-19, it certainly felt like the nation was operating on a somewhat usual basis, if not fully usual, at least as we sit here today. By the time we reached the end of March, the sentiment was certainly a different story. As the topic of the coronavirus and the resulting economic outlook became the only headline in the news, the lending market for seniors housing assets quickly reacted. In general, seniors housing balance sheet lenders honored transactions that were past the term sheet stage and in some cases, but not all, certain structural points related to leverage, pricing and recourse were re-evaluated to reflect the volatile market conditions. On the other hand, most of the transactions that were in the earlier stages of vetting were put on hold as everyone waited to see what COVID-19 would bring.

While there was some uncertainty in early March surrounding any impact that might be associated with COVID-19, it certainly felt like the nation was operating on a somewhat usual basis, if not fully usual, at least as we sit here today. By the time we reached the end of March, the sentiment was certainly a different story. As the topic of the coronavirus and the resulting economic outlook became the only headline in the news, the lending market for seniors housing assets quickly reacted. In general, seniors housing balance sheet lenders honored transactions that were past the term sheet stage and in some cases, but not all, certain structural points related to leverage, pricing and recourse were re-evaluated to reflect the volatile market conditions. On the other hand, most of the transactions that were in the earlier stages of vetting were put on hold as everyone waited to see what COVID-19 would bring.

A few of the immediate impacts from COVID-19 on banks’ loan portfolios included higher outstandings on lines of credit, as clients drew on them to preserve liquidity, as well as stresses to the retail and hospitality sectors in the commercial real estate space. The loan portfolios of national lenders, as compared to regional lenders, have a higher concentration to each of these items, which has therefore caused them to be more on the sidelines in terms of originating new balance sheet deals for seniors housing assets. This will impact especially larger construction and portfolio transactions where the national lenders have traditionally been the main providers of debt.

In addition, across the board, lenders are having a difficult time underwriting cash flows for operating properties resulting in a challenging market for bridge loans. Sarah Anderson of Newmark Knight Frank indicates, “The good news is that seniors housing operating numbers for both April and May were not as dismal as everyone had predicted. In addition, early June reporting from Welltower is being viewed favorably with the REIT stating a slowdown in occupancy loss over the last two weeks of May, along with a decrease in COVID cases of 50% from the peak, as well as approximately 87% of communities in their portfolio that have reported no coronavirus cases at all. With that said, there is just not enough historical data yet for lenders to feel comfortable in their underwriting assumptions on absorption, rental rates and normalized expenses over the next 12 months.” What has shown as a positive is the restructuring activity occurring with lenders willing to address covenant restructures and maturity extensions for seniors housing loans in their current portfolios. Much of this willingness is a testament to both strong sponsorship and the high amount of liquidity in the sector, with no doubt the requirement for the borrower to post additional capital, re-margin the loan commitment and/or agree to more sizable pricing or more rigorous covenants in relation to these restructures.

For those lenders that are originating new balance sheet loans, the majority of that is happening on the construction side with the thought being that delivery of the asset will be post pandemic, albeit with a more stringent structure than was the case three months ago. As noted by Austin Sacco of CBRE, “For example, in early 2020, a typical structure for construction loans included partial recourse of between 15% and 25%, leverage at 65% of total construction costs, and pricing at a spread of low to mid 200 bps over LIBOR. That structure today may potentially result in a slightly higher recourse component with lower leverage of between 60% and 63% of total construction costs, and spreads widening anywhere between 25 and 50 bps. In addition, following the onslaught of the pandemic, LIBOR floors at one point reached a height of 100 bps, but have recently compressed to 50-75 bps given the low level of LIBOR, whereas earlier in the year, these floors were very low to nonexistent.”

For those lenders that are originating new balance sheet loans, the majority of that is happening on the construction side with the thought being that delivery of the asset will be post pandemic, albeit with a more stringent structure than was the case three months ago. As noted by Austin Sacco of CBRE, “For example, in early 2020, a typical structure for construction loans included partial recourse of between 15% and 25%, leverage at 65% of total construction costs, and pricing at a spread of low to mid 200 bps over LIBOR. That structure today may potentially result in a slightly higher recourse component with lower leverage of between 60% and 63% of total construction costs, and spreads widening anywhere between 25 and 50 bps. In addition, following the onslaught of the pandemic, LIBOR floors at one point reached a height of 100 bps, but have recently compressed to 50-75 bps given the low level of LIBOR, whereas earlier in the year, these floors were very low to nonexistent.”

It should be noted the agency market has been active over the last few months. For stabilized assets, Fannie Mae and Freddie Mac are committed to providing liquidity and have originated new loans with a heightened focus on the sponsorship. “Wells Fargo Multi-Family Capital continues to be active in the seniors housing agency space and has recently financed both refinances and acquisitions,” according to Lori Coombs, Wells Fargo Multi-Family Capital Seniors Housing group head. Each agency group has their own comfort level in financing communities where COVID-19 cases exist. The structures from both agency lenders being quoted today include slightly lower leverage, pricing for fixed rate loans to include treasury floors, as well as an increase in the requirement for sponsorship escrows which will vary by deal but can be as much as 12 months’ worth of principal and interest.

The most important item to keep in mind right now is that the current lending environment we are in is very fluid. It is very hard to determine what the near term will bring, but it is safe to say the bar has been raised relative to all aspects of deals including sponsorship and both project and economic return merits. As COVID-19 cases in seniors housing communities seem to have somewhat stabilized for the time being, it does feel like borrowers are trying to test the lending environment to see what capacity lenders have, with recent weeks bringing an influx of financing requests. According to Austin Sacco, “Realistically I think the lending environment over the summer months will continue to be a bit choppy as everyone tries to determine what the new normal is. Out of necessity, given the amount of capital, particularly that private equity funds who are dedicated to seniors housing have raised, and the fact that this money typically has a finite time period in which it needs to be deployed, I expect the fourth quarter to bring more activity and continue into 2021.” Sarah Anderson agrees, “It does feel like there is optimism out there, and that optimism is stemming from the amount of capital that is supporting the industry and the fact that this capital must be put to use to achieve returns in the very near future.”