Leveraging Innovative Ideas and Connections at the 2017 NIC Spring Forum

Focused on the theme of unlocking value through senior care collaboration, the 2017 NIC Spring Investment Forum attracted more than 1,500 industry leaders, including 300 first-time participants. The Forum was held March 22-24 at the Hilton San Diego Bayfront, San Diego. [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Three NIC-hosted networking receptions and several networking lounges helped attendees connect for conversations on business prospects, and the future of the wider industry. The three-day program included more than a dozen educational sessions highlighting three principal areas: capturing value; creating successful partnerships; and economic, capital and policy trends. Attendees were also able to visit the NIC MAP Data Service Hub for a virtual tour of its research and analytic tools.

What follows are key takeaways from the programming. For more coverage, visit http://www.nic.org/connections/connectionsspring-investment-forum-overview/2017-spring-investment-forum-rewind/

Day 1

More than 40 capital providers met with seniors housing and care owners, operators and developers during the pre-conference networking opportunity: Capital Connections that took place prior to the kick-off of the Forum. Capital providers included debt lenders, debt agency lenders, and equity, REITs and other partnership opportunities.

The Forum commenced with two educational sessions that were held Wednesday afternoon: “The Value-Based Care Revolution,” and “The Economy in 2017 and Its Impact on Seniors Housing & Care.” Economy panelist Timothy J. Fox, executive vice president/chief investment officer at Senior Resource Group, noted: “What the consumer wants has changed as product needs continue to evolve. We need to be innovative and improve our residents’ quality of life.”

A special “Power Hour” reception was held for first-time attendees later in the afternoon, followed by a welcome reception for all participants.

Day 2

The theme, “The New World of Senior Care Collaboration,” was introduced at the Forum’s opening general session by NIC’s CEO Bob Kramer. He explained that innovative partnerships with home care, care management, and primary care organizations can help operators and investors unlock new value in their properties. “There is opportunity to add value to investments in real estate-based care when a senior care organization innovates by partnering with health care organizations,” said Kramer.

A panel discussion followed, led by Anne Tumlinson, founder of Anne Tumlinson Innovations. She recapped recent research showing the benefits of collaboration while other panelists provided specific examples. Kelsey Mellard, head of health system integration at Honor, a San Francisco-based home care start up, noted how the company’s technology platform could partner with real estate-based providers.

Panelist and investor Kurt Read, principal, RSF Partners, said: “Our industry needs to change. We need to bring investors together with providers of outside services.”

Other highlights from Day 2 include:

* The morning educational sessions focused on emerging topics of importance to the industry, including managed care, increased competition, the role of seniors housing in the home care evolution, and real estate investment in a coordinated health care world.

* NIC Senior Principal Lana Peck moderated a panel on how to respond to increased competition from new developments. Experts weighed in with their lease-up strategies, as Peck provided insights on specific markets from the latest NIC MAP seniors housing data. Orlando is tops for independent living development, while Detroit is first in assisted living development. Cincinnati currently has the most new memory care development.

* A new NIC initiative was introduced by Bob Kramer at the Forum luncheon. NIC is awarding a grant to NORC at the University of Chicago, an independent research institution, to study the seniors housing middle market—those whose income and assets do not allow them to qualify for Medicaid, but who can’t afford to live in private-pay communities, or not for very long. The industry has an opportunity to serve this growing, and significant, segment of the elder population, said Kramer.

* Amid breaking news out of Washington on health care legislation, former U.S. senators Bill Frist and Tom Daschle provided their perspective during a luncheon discussion moderated by Kenneth Segarnik, chief corporate officer at Brandywine Living. The senators agreed that long-lasting, effective health care policy requires deep sector knowledge, a strategic approach, and, ideally, bipartisan support. “In this health care transformation, our success depends on resiliency, collaboration, engagement and innovation,” said Dashcle.

*Afternoon sessions focused on innovative technology, skilled nursing trends, hot new investments, and how to build partnerships for clinical and financial success. During the session on innovative technology, Craig Patnode, CEO at Simply Connect, described how the company serves 2,000 communities sharing health information among providers. “Senior living holds 75 percent of the data,” said Patnode. “We need to track it and use it to coordinate care.”

Day 3

The last day of the Forum gave attendees a final chance to network, and attend several educational sessions on quality metrics, redefining valuations in collaborative business models, local seniors housing market conditions, and the future of Medicaid reimbursement.

In the session on local markets, NIC Chief Economist Beth Burnham Mace identified oversupplied markets (Texas) as well as generally healthy areas (California). Mace noted that investors and developers need reliable occupancy rate and market performance metrics, charted over time, in order to determine future growth opportunities. “No two markets are the same,” she said.

The session on redefining valuations highlighted the challenge of determining the value of changing business models. Kevin Harbour, managing director and head of healthcare originations, Wells Fargo Capital Finance, said he believes the challenge will probably increase as skilled nursing facilities and seniors housing communities add more ancillary services to their businesses. Other panelists noted a variety of new revenue streams, including home health, in-house therapy services, dementia care, and areas of disease management specialization. “Organizations that develop competencies have tremendous value,” said Adam Klein, principal, ECG Management Consultants. [/expand] [cresta-social-share]

Thoughts from NIC’s Chief Economist

by Beth Mace

Fed Policy and Higher Interest Rates. In a widely anticipated move, the Federal Reserve increased interest rates at its March FOMC meeting, moving the targeted Federal Funds rate up 25 basis points to the 0.75% – 1.00% range. The increase marked the third since December 2015, and at least two or more rate hikes are expected during the rest of the year as the Fed continues its path of “normalization of rates.” At this point, the economy looks strong enough to withstand the effects of higher interest rates. The labor market is close to full employment, and inflation appears to be rising closer to the 2% Fed target. [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Collaboration and the Breakdown of Silos. The theme of NIC’s Spring Investment Forum, recently held in San Diego, was creating value in the seniors housing and care sector through collaboration with the health care system and care and service providers. Projected growth in frail, elderly adults, defined as those who need help with activities of daily living (estimated at 11 million currently) is beginning to change the way many in the field operate. Real estate-based senior care providers, such as skilled nursing properties and senior living communities, are now partnering with providers of health and wellness services, such as chronic and transitional care management, homecare, and care management technology services.

Increasingly, operators of seniors housing are looking for opportunities to better integrate their services. Connecting frail seniors to enhanced primary care delivered at home and other alternatives to hospitalization both increases the value offered by real estate-based providers and produces better outcomes for seniors. The transformation toward value-based care in the U.S. healthcare system is being promoted by changes in government policy and is making these partnerships increasingly common and breaking down the silos between care and housing that have existed in the past.

Based on these themes, NIC’s conference brought together hundreds of leaders in healthcare, seniors housing, home care, finance, and care coordination to discuss how the changing demographics of seniors, changes in healthcare delivery, and advances in technology are fostering opportunities to deliver more closely coordinated care. The goal of the 2017 Spring Investment Forum was to help facilitate more of these connections, and provide a firm foundation for valuable partnerships that help providers, operators, and investors – and the seniors they serve. Summaries of many of the key takeaways from the Forum can be found in other parts of the NIC Insider.

Rising Challenges for Operators: Labor Considerations. Wage rates and labor expenses are rising for many operators of seniors housing and care properties. In addition to pressures mounting from a tightening labor force, 21 states are expected to increase minimum wages in 2017. Some of the increases are modest (five to ten cents), while some are as large as one dollar or more (Arizona up $1.95 to $10 per hour, while Massachusetts and Washington State will both enact $1 increases to $11 per hour). A few of the 21 states are also in the process of multi-year hourly minimum wage increases. These include Arizona (which will push its minimum wage rate to $12 by 2020), California (up to $15 by 2022) and New York (up to $15 by 2021).

In addition to these pressures, potential changes in both U.S. immigration policy and the Affordable Care Act are adding another layer of uncertainty to the availability and cost of labor for many operators of seniors housing and care properties. And uncertainty is never a good thing for business decision makers. While the implementation of the Affordable Care Act provided health care options to many, it also altered expenses for some operators and spending patterns for staff. Changes in the law could alter these dynamics with direct and indirect consequences, some potentially positive, some less so.

Larger Rent Discounts Offered for Assisted Living Actual Rates than for Independent Living Properties. The NIC MAP® Data Service recently released national benchmark data through year-end 2016 for actual rates and leasing velocity. The NIC MAP Seniors Housing Actual Rates Report provides national data from approximately 250,000 units within more than 2,500 properties across the U.S. operated by 15 to 20 seniors housing providers. This monthly time series is comprised on end-of-month data for each respective month. Key takeaways include:

• Average initial rates were below average asking rates for both independent living and assisted living properties, with monthly spreads larger for assisted living properties throughout the entire reported period which starts with April 2015. As of December 2016, assisted living initial rates averaged 10.7% below the average asking rate, which equates on an annualized basis to an average initial rate discount equivalent to nearly 1.3 months. The discount for independent living was smaller at less than half a month’s rent.

• Average initial rates for independent living properties have been trending higher for the past 12 months, and in December, were 2.9% above year-earlier levels. This was more than the 2.5% increase seen in average asking rates for independent living. While assisted living average asking rates also continued to climb, average initial rates for assisted living were 1.2% below year-earlier levels.

• The pace of move-outs continues to be greater for assisted living than independent living. This demonstrates that resident turnover continues to be greater within assisted living properties than independent living properties. Move-outs have exceeded move-ins for six of the past 12 months for assisted living and five months for independent living.

The Nation’s Aging Seniors Housing Stock. Just like the nation’s population, the inventory of seniors housing is aging. According to the latest 4Q 2016 NIC MAP® data, the median age of the Primary and Secondary (largest 99 markets) seniors housing and care properties is 26.8 years old. Broken down into property type categories, majority nursing care properties are the oldest (38.0 years), followed by majority independent living properties (18.6 years), and majority assisted living properties (18.0 years). The median age of CCRCs is 32 years, and median age of memory care properties is 15 years. The oldest stock is in the Pacific (30.0 years), Northeast (29.8 years), and East North Central (28.0 years) regions, and the youngest stock is in the Mountain (20.0 years) and Southwest (19.3 years) regions.

On a unit basis, more than half of independent living units tracked by NIC are older than 25 years of age (56%). On the other end of the age spectrum, approximately 12% of the independent living (IL) inventory is less than 10 years of age. Within this cohort, less than 2% of today’s existing IL inventory is two years of age or younger. The age of assisted living units is also relatively old, but significantly younger than those at independent living properties. Only 27% of assisted living units are older than 25 years of age, while 32% are between 17 and 25 years of age. And, reflecting the recent concentration of construction in the AL sector compared with the IL sector, more than 6% of the assisted living stock is less than two years old, while 23% is less than 10 years old.

For operators, developers and capital providers, understanding the composition and the age of stock in a market can provide useful insights that can help support or detract from a thesis of development.

As always, I welcome your feedback, thoughts, and comments.

Beth [/expand] [cresta-social-share]

Skilled Nursing Trends and Strategic Responses

by Liz Liberman

At the 2017 Spring Investment Forum, NIC Senior Principal Bill Kauffman detailed for attendees the implications of NIC’s latest market data on the skilled nursing sector in the session titled, “Skilled Nursing Trends and Strategic Responses.” Kauffman provided an overview of NIC’s skilled nursing data through the end of 2016 and revealed some notable developments. Among some of the major headlines in the data was the fact that Medicaid continues to drive both patient days and revenue in skilled nursing—a salient point made moments before what could have been a groundbreaking vote in the U.S. House of Representatives to reform Medicaid as part of the repeal-and-replace legislative health care reform effort. Kauffman also highlighted institutional sale transactions trends, noting that the dollar volume of deals closed in nursing care has been relatively stable compared with seniors housing, as has the price per unit. Furthermore, a shift in the cost of capital may have influenced a decline in transaction activity among the REITs. [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Kauffman used the data to present a backdrop against which the session panelists proposed their strategies for combating pressures in the sector and adapting to changes in the industry. Panelist Nancy Schwalm, chief business development officer at Vivage Senior Living, expressed overall optimism about the sector despite some of the challenges, noting, “For every challenging moment that we’re facing right now, there are tremendous opportunities.” She explained that deepening relationships between skilled nursing providers and hospitals is a new phenomenon. “For the first time in years, hospitals all know our names and phone numbers and are calling us,” she said. While relationships are important, Schwalm stressed that data is paramount because hospitals, and managed care and partner organizations are all demanding it to make informed decisions.

Derek Prince, President and CEO of HMG Service, LLC, agreed with Schwalm that data is key. He implored operators to start collecting data right away if they aren’t doing so already, and to make sure the data is relevant for individual markets. Both Prince and Schwalm expressed that data is important for the value-based care evolution and for skilled nursing operators to be successful.

Each of the panelists acknowledged that challenges persist in skilled nursing. In fact, Wendy Simpson, Chairman, CEO, and President of LTC Properties, Inc., said: “There’s never a year in skilled nursing that isn’t a challenge.” But, she added, it seems like the volume of challenges has been higher lately. Despite those challenges, Simpson also expressed optimism for the industry and her willingness to use her position to mobilize capital to support operators in her portfolio. While rent cuts may be one way a REIT can help operators mitigate challenges, as Kauffman noted, Simpson explained that more creative solutions are available, such as transitioning assets away from ineffective operators, helping with networking, and supplying the capital needed to purchase integrative systems.

Workforce retention was another challenge the panelists discussed, as well as regulations and market share. Indeed, Schwalm noted that labor is an issue not only for long-term care, but for her state as well. Vivage is one of the largest employers in Colorado, she explained, so changes in the industry can create shockwaves beyond skilled nursing. In Texas, Prince’s tactic for labor retention is an annual car giveaway for employee of the year. [/expand] [cresta-social-share]

Unlocking Value with Quality Metrics

by Liz Liberman

The 2017 NIC Spring Investment Forum was all about partnerships, and a common theme expressed by attendees was that partners want data. Even assisted living providers may be expected to produce quality metrics, according to Kim Estes, senior vice president of clinical services at Brookdale Senior Living. And in skilled nursing, tracking quality metrics has never been more important, explained panelist Kim Barrows of KB Post-Acute Strategic Specialists. In a Friday morning session, panel moderator Michael Torgan, of First Quality Healthcare Group, asked Estes about the latest trends in quality metrics and how operators should be using data to demonstrate their value to partners, payors and customers. [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

In response, Estes stated, “Everybody’s collecting the data. The question is what are they doing with it?” Barrows suggested, for example, that operators can use internal metrics to help provide an additional perspective on a low Five-Star Quality rating. The score, given to all nursing homes by CMS, can take months or years to adjust even if the operator has made considerable strides toward quality improvement. In assisted living, Brookdale uses its quality metrics data to reduce the risk of litigation, improve internal processes and demonstrate worthiness to its own insurance companies. And while assisted living operators may not have to answer to the federal government in the form of a Five-Star Quality rating, they still must answer to their own customers. Tracking social media has also become an important part of Brookdale’s data collection strategy, Estes said.

In skilled nursing, the trend is toward more detailed data collection as required by CMS. Barrows mentioned a new metric, the Medicare Spend per Beneficiary—a measure being used by some providers that will likely become part of the Five-Star Quality rating. Other metrics skilled nursing operators should note include: discharge data, length of stay by diagnosis, and employee turnover, among others. These are the quality metrics sought by hospitals and payors when making educated decisions about partnerships, another reason why the validity of the provider’s data is so important, she stressed.

In closing, Torgan asked the panelists which metrics were the most important. Barrows listed some common measures, such as length of stay, census, and readmissions. Also, Estes suggested the Net Promoter Score, a metric tracked by hospitality companies such as hotels and restaurants, as among her top priorities. Both panelists agreed that quality metrics are paramount to running a successful business in this evolving industry where government, partners, payors and customers all want to know what strategies are being used to help residents thrive. [/expand] [cresta-social-share]

The Latest Skilled Nursing Trends

by Bill Kauffman

NIC released its latest Skilled Nursing Data Report on March 15, which included key data points from January 2012 through December 2016. The main takeaways include:

- Occupancy decreased year-over-year in 4Q 2016 to 81.8%

- Medicaid patient day mix continued to grow year-over-year ending 2016 at 66.2%

- Pressure continued on skilled mix in 2016

- The decline in managed Medicare revenue per patient day slowed significantly

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

The current report is based on data collected on a monthly basis but reported quarterly from approximately 20 operators and 1,500 properties. The data currently is reported on a national aggregate level. However, the plan is to grow the data set by adding more operators and properties which will allow NIC to report data at the state level. Operators around the country are all welcome to participate in this confidential data collection and receive a free benchmark report every month for their participation.

The Details

There continued to be much discussion last year about uncertainty within the skilled nursing sector, as the business model continued to transition from a fee-for-service business model to a value-based model. Uncertainty is likely to persist through 2017 as the actions of the new Trump administration unfold. Although no one knows what the future holds, it’s always a good idea to know where we stand now. And data allows us to do that.

Here are details on the most recent occupancy and revenue trends for the skilled nursing sector.

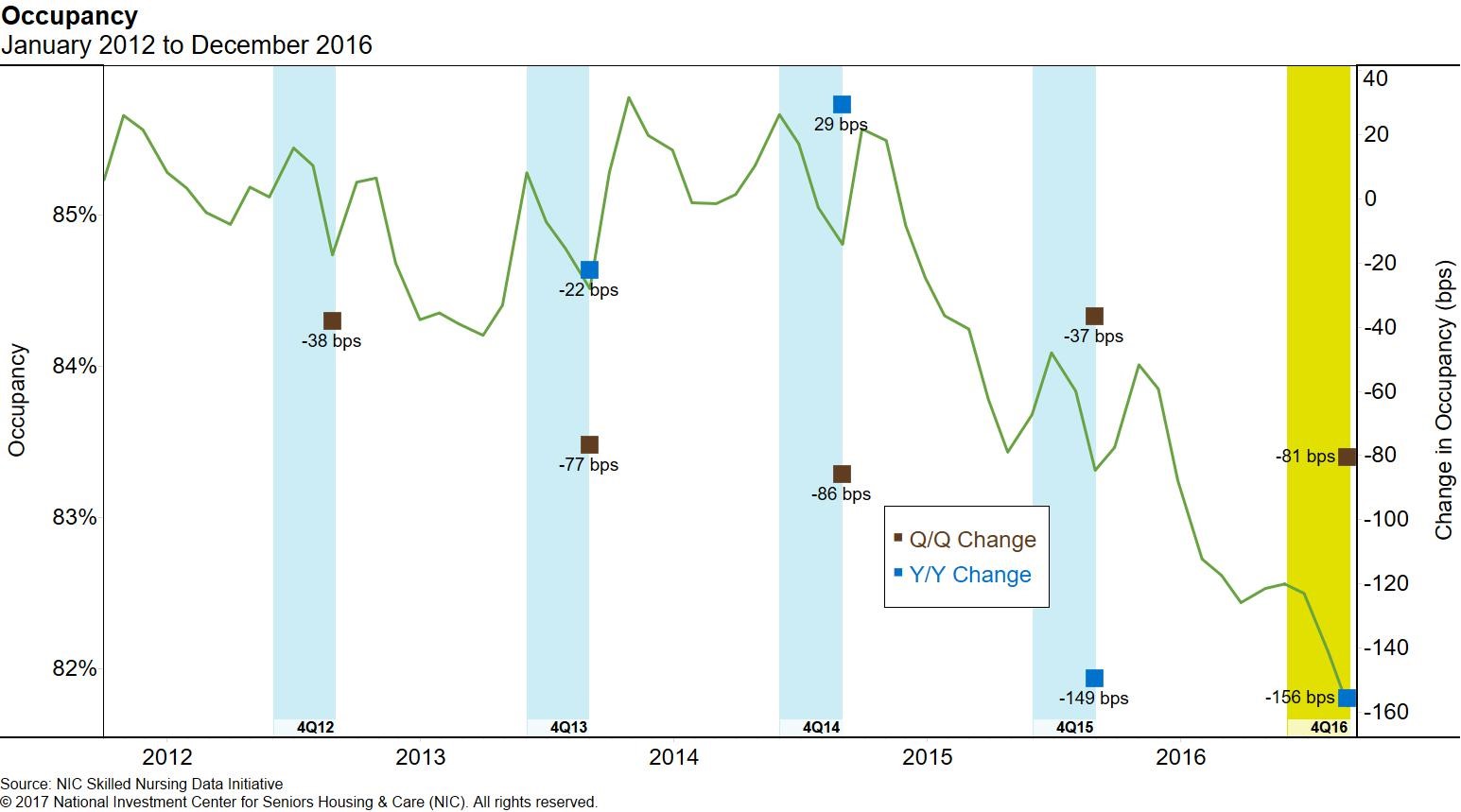

Occupancy Continued to Decline in 2016

Occupancy fell to 81.8% in 4Q 2016, a new low over the past five years, marking the third consecutive quarter in which occupancy reached its lowest point in the series. Unlike recent quarters, the decline in occupancy did not correlate with softness in quality and skilled mix, which both saw modest increases in 4Q 2016. Occupancy was down over 150 basis points year-over-year from 83.3%–the largest year-over-year decline for the fourth quarter in the data series, which is noted in the occupancy chart below.

The following chart shows occupancy trends over the past five years. It is worth noting that we have seen accelerated pressure over the past two years as the industry transitions to value-based payments.

Many operators have been dealing with occupancy challenges on the Medicare side of the business. More Medicare patients have enrolled in Medicare Advantage plans over the past couple years. This has put pressure on the length of stay, adding to the challenge to increase patient days at properties. In addition, more patients are now bypassing skilled nursing properties and going directly home for care. This is most likely due to the many Medicare payment initiatives around the country including bundled payments and the creation of accountable care organizations (ACOs). The added challenge of narrowed provider networks has resulted in the occupancy trend below. The question: how long can this trend continue? Many argue that occupancy trends will eventually reverse as the demand for long-term care increases exponentially in the next decade as the population ages.

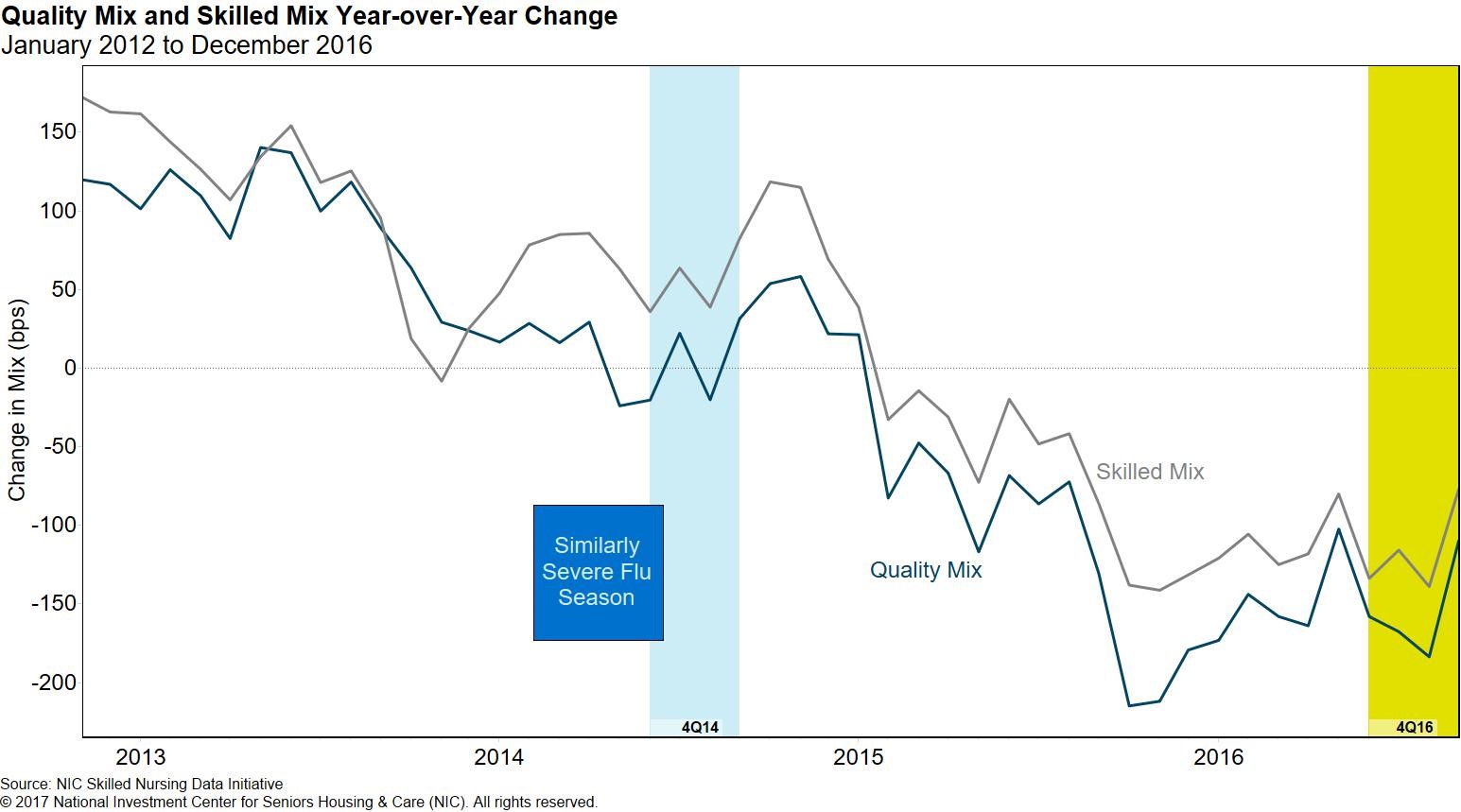

Skilled Mix Holds Steady in 4Q 2016, Down Year-over-Year

Skilled mix was up slightly in 4Q 2016. The increase in skilled mix may have been due to an early and significant flu season, which usually results in higher admissions to skilled nursing properties (see below chart). However, skilled mix fell by 0.8% year-over-year to 24.3%, which was only slightly higher than the lowest point in the series, reached in September 2012. The rate of year-over-year change in both skilled and quality mix has been negative since 2Q 2015, with the skilled mix decline slightly greater than the quality mix decline. The skilled mix decline has been driven by pressure on Medicare mix which reached its lowest level in the data series in 4Q 2016.

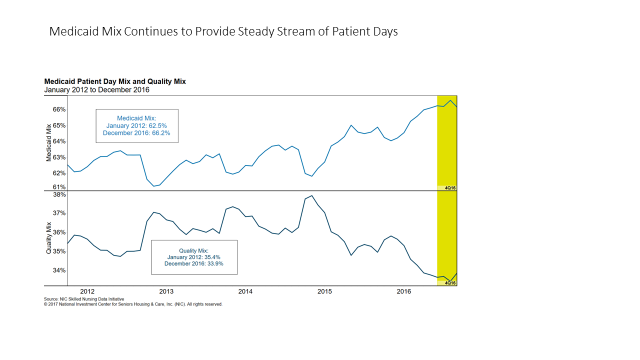

The Importance of Medicaid

Amid all the conversation regarding value-based purchasing on the Medicare side of the business, it might seem strange to discuss the importance of Medicaid. However, with at least 50% of most operator’s revenue coming from Medicaid, it is not only important but also vital to business success, especially considering the pressure on skilled mix. Although Medicaid reimburses providers at a lower rate than Medicare or managed Medicare, it still represents a relatively reliable revenue stream for operators. Taking it a bit further, just think about the next couple decades when the long-term stay Medicaid population/demand increases significantly. Though Medicaid reimbursement of nursing home care has not made headlines over the past couple years, it started to accelerate as Congress debated repeal and replace of the Affordable Care Act. It most likely will continue to be a hot topic in the years ahead as budgetary constraints persist. The latest data shows that Medicaid represents 66.2% of patient days as it continues to supply a steady stream of residents. Year-over-year, Medicaid patient day mix grew 1.3% from 64.9% in 4Q 2015. Furthermore, Medicaid patient day mix also has grown 3.6% over the data time-series since 2012. It is reasonable to predict that this mix will continue to grow since the aging population with long-term care needs is projected to explode in the 2020s, especially toward the end of that decade.

In addition, the 4Q 2016 data demonstrated the continued increase of Medicaid revenue per patient day (RPPD) as the rate rose to more than $200 for the first time in the five-year series. Medicaid RPPD was up 0.9% quarter-over-quarter, and 1.8% year-over-year. However, the year-over-year growth failed to keep up with wage inflation in the nursing home which was greater than 3%. Over this five-year series, Medicaid RPPD experienced a 1.4% compound annual growth rate.

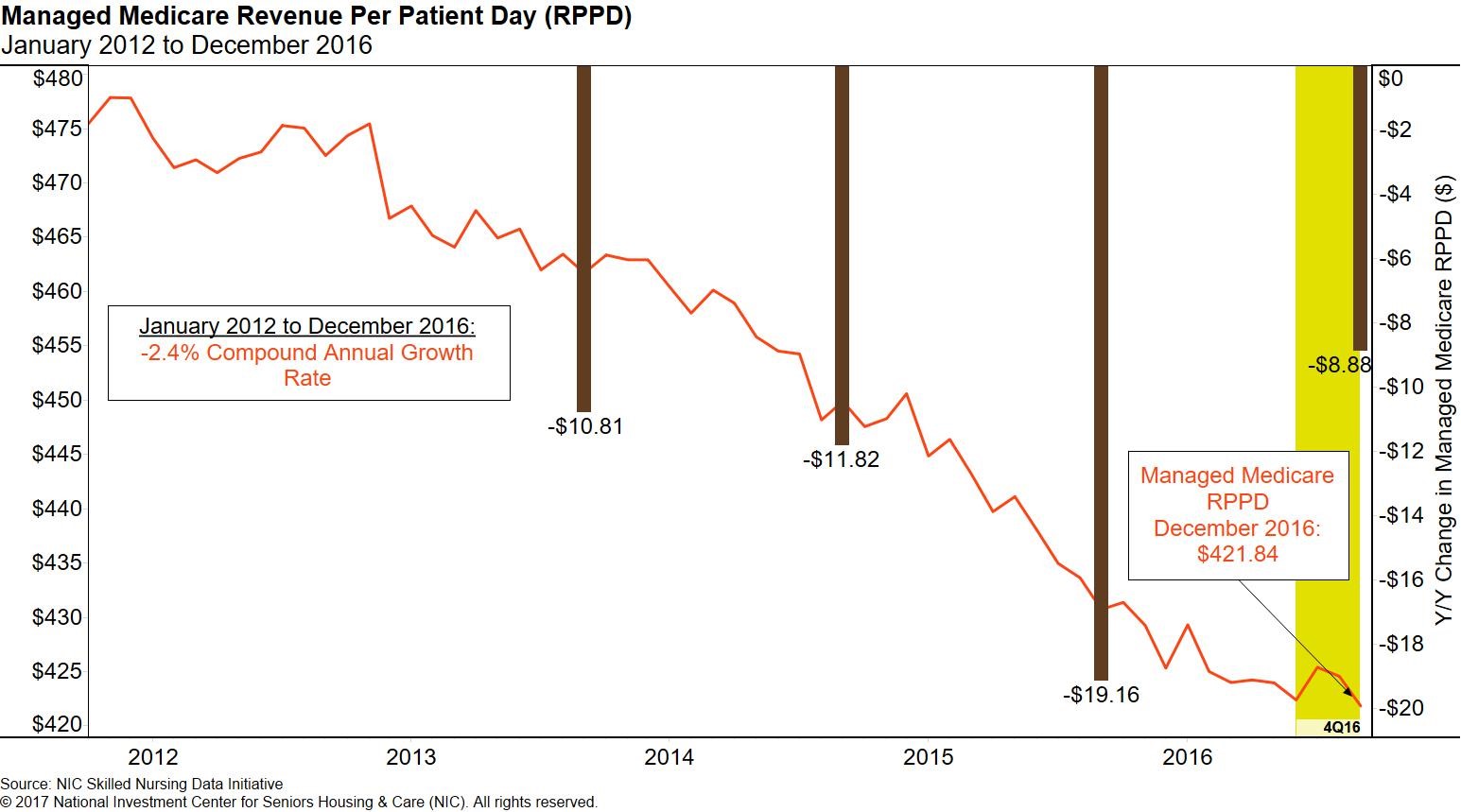

Managed Medicare Revenue per Patient Day: Signs of Stabilization

Managed Medicare has grown in importance as about one-third of Medicare beneficiaries are enrolled in managed care today. Also, narrowed networks coupled with the plans’ pricing power has brought some challenges on the revenue side to operators. However, recent data shows that revenue per patient day is showing signs of stabilization.

The decrease in managed Medicare RPPD was under $9, year-over-year, compared to a $19 decrease between 4Q 2014 and 4Q 2015. While revenue per patient day for managed Medicare reached its lowest point in the data set at $421.84 in 4Q 2016, the 2.1% decrease over 2016 was considerably less than the prior year’s 4.3% decline. The decline quarter-over-quarter was also notably less than in previous quarters at 0.1%–the smallest decrease in the past six quarters, portending that the year-over-year decreases may continue to shrink as time progresses.

Managed Medicare will become an even more pressing topic as nearly half of all seniors are expected to be enrolled in managed care over the next 10 years. This data trend certainly warrants attention.

We look forward to following up with the latest trends as they become available. Please feel free to reach out with any questions or comments.

NIC released its latest Skilled Nursing Data Report on March 15, 2017. You can download the latest report and future reports at: http://info.nic.org/skilled_data_report_pr [/expand] [cresta-social-share]