Thoughts from NIC’s Chief Economist

Seniors Housing Market Fundamentals in Equilibrium?

Data for the first quarter of 2016 suggest that seniors housing is a market in equilibrium. The occupancy rate for seniors housing averaged 90.0% for the nation’s largest 31 metro areas, a level it has been oscillating around for more than two years. During this period, roughly 25,000 units were delivered, virtually the same number of units that have been absorbed on a net basis.

Data for the first quarter of 2016 suggest that seniors housing is a market in equilibrium. The occupancy rate for seniors housing averaged 90.0% for the nation’s largest 31 metro areas, a level it has been oscillating around for more than two years. During this period, roughly 25,000 units were delivered, virtually the same number of units that have been absorbed on a net basis.

The performance by property type, however, has not been the same. As recently as the third quarter of 2012, the occupancy rates for both majority assisted living and majority independent living properties were the same at 88.7%. The most recent data for the first quarter reported an occupancy rate for independent living of 91.3%—just 10 basis points shy of its eight-year high-water mark reached in the fourth quarter of last year—while the occupancy rate for assisted living averaged 88.3%. The difference in the performance of the two property types largely reflects greater growth in the inventory of assisted living than independent living. Since mid-2012, the stock of assisted living units has increased by 13% versus 3% for independent living properties. Demand has exceeded growth in inventory for independent living over this period, explaining the increase in occupancy rates, while demand has fallen shy of the growth in stock for assisted living.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

That said, the assisted living sector appears to also be in equilibrium, albeit at a lower occupancy level. Since mid-2012, the occupancy rate has averaged 88.6% and stood just 30 basis points shy of this average in the first quarter. Therefore, while demand has not keeping up entirely with the significant growth seen in assisted living, it largely has been able to keep pace. In fact, during the first quarter, the rolling four-quarter rate of absorption for majority assisted living properties matched supply, with both absorption and supply registering growth of 4%. By contrast, the pace of demand growth for independent living was a lesser 1.5%.

This raises the question of, “If you build it, will they come?” Analysis conducted last year by Senior Housing Analytics and NIC showed that after 24–36 months, two-thirds of all newly constructed assisted living and independent living properties were more than 90% occupied, while 10% were less than 80% occupied and did not stabilize. Conditions affecting specific property-level outcomes may include location, operator, competition, and local market conditions.

Construction Starts Slip

First-quarter data also showed a marked slowdown in new development activity for the second consecutive quarter. Seniors housing construction starts totaled 2,737 units, comprised of 802 independent living units and 1,935 assisted living units. On a four-quarter basis, starts totaled 19,243 units, its weakest pace in a year. The decline in starts may suggest that the market is responding to well-publicized concerns about supply. Data for the second and third quarter will further illuminate this possibility. Anecdotally, some properties scheduled to break ground in the first quarter failed to do so because of higher construction costs, the discovery of new competition in the area, or because they were waiting on final financing approval.

Flu Impact

The U.S. Centers for Disease Control and Prevention (the CDC) tracks flu incidence across the U.S. on a weekly basis (www.cdc.gov/flu). For the 2015/2016 winter season, visits to the doctor for influenza remained below the high levels of the 2014/2015 and 2010/2011 winters until late February of this year. At that time, reports of influenza started to pick up and peaked in late March. By early April, the incidence was falling, but it still remained more intense than in recent years. This data suggests that move-outs related to illness likely increased in the latter part of March and early April. The impact on occupancy rates may have affected the data NIC recently reported for the first quarter of the year, where there was a slowdown in net absorption from the fourth quarter. It could also presage some occupancy pressures in the second quarter of 2016.

Rent and Expense Growth on the Rise

At 3.0% in the first quarter, annual asking rent growth for seniors housing accelerated to its highest level since 2008. Asking rent growth for assisted living was a lesser 2.7%, while for independent living, it was 3.2%. There is wide variation in rent growth among the metropolitan markets, however, with Las Vegas experiencing a decline of 0.8% in assisted living asking rents from year-earlier levels, for example, while San Jose saw a gain of nearly 9%. The wide performance in rents reflects the balance of landlord versus renter pricing advantage, which in turn reflects the competitive landscape, the availability of units within a market, and occupancy rates.

For some time, we have been hearing about rising pressure on wage rates from seniors housing and care operators. Broad wage data, however, has not shown this trend. However, sector-specific data on changes in average hourly earnings for assisted living properties, as tracked and monitored by the U.S. Bureau of Labor Statistics, do show upward pressure on wage rates. Indeed, average hourly earnings for assisted living workers accelerated from nearly flat growth as recently as late 2013 to 4% on a year-over-year basis as of the fourth quarter of 2015. This corroborates anecdotal evidence we have been hearing from operators for some time.

As always, I welcome your thoughts, comments, and feedback.

Beth

[/expand] [cresta-social-share]

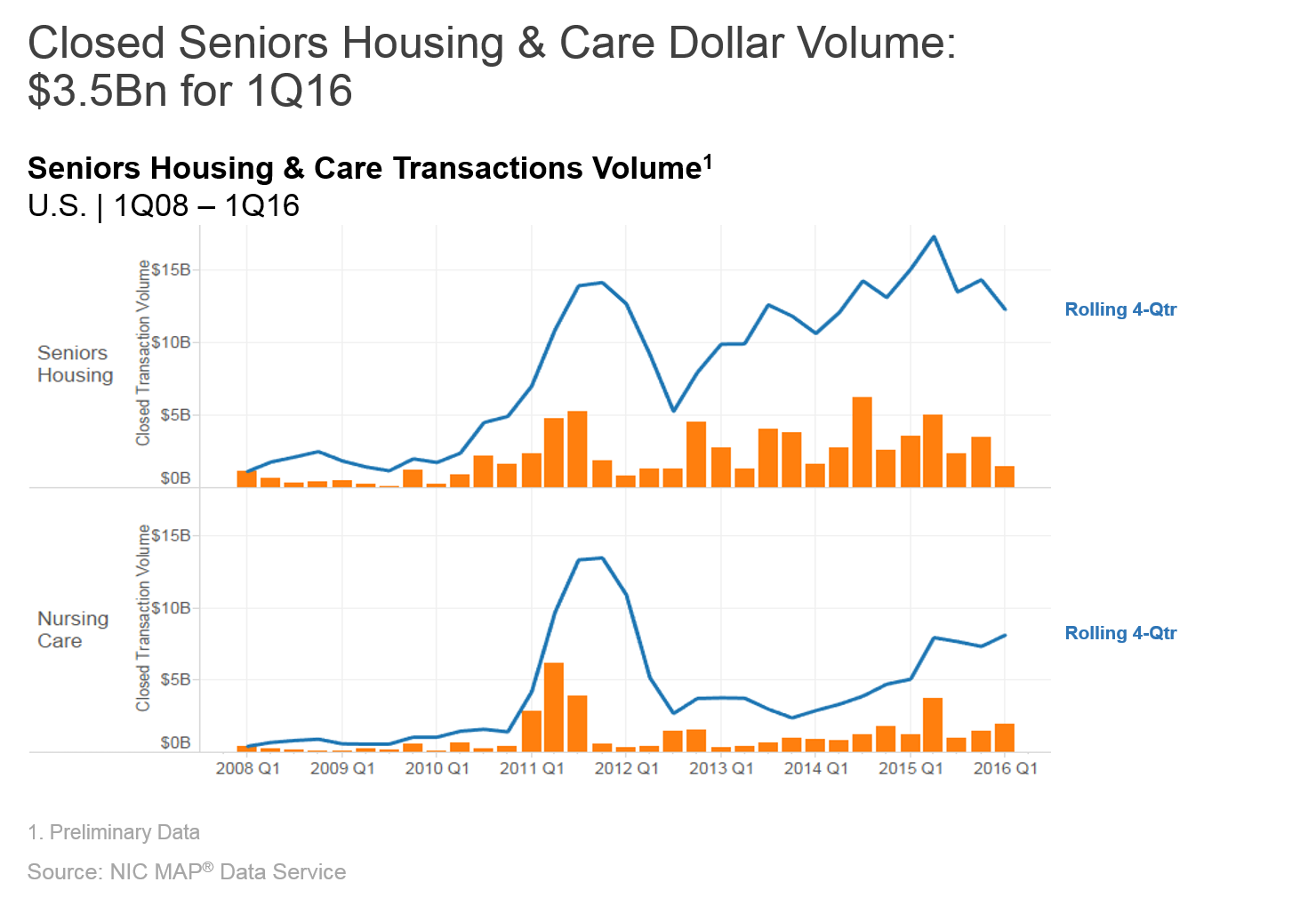

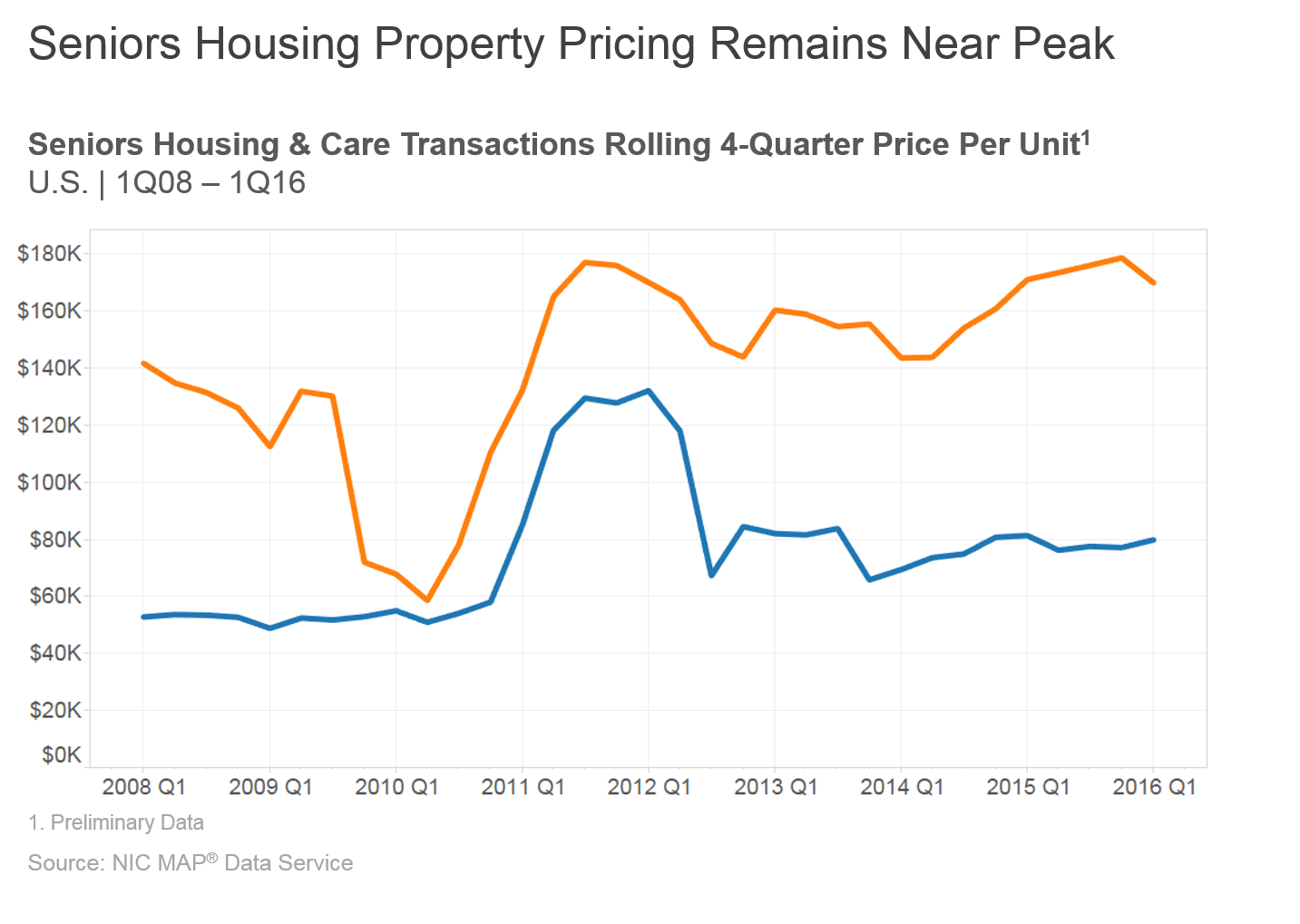

Property Sales Transaction Volume Slips in First Quarter

Sales transaction levels in the U.S. seniors housing and care property market slowed in the first quarter of 2016 due to a significant decline in the pace of seniors housing trades. Sales volumes for skilled nursing picked up.

Preliminary NIC MAP® data show first-quarter dollar volume of $1.5 billion for seniors housing, the weakest pace since early 2014. On a rolling four-quarter rate, sales volumes totaled $12.3 billion, down 29% from the second quarter 2015 peak of $17.4 billion. In contrast, quarterly sales volumes of skilled nursing properties exceeded those of seniors housing for the first time since mid-2012. Sales volumes totaled nearly $2 billion in the first quarter and $8.1 billion on a rolling four-quarter basis—the most since early 2012. The increase in nursing care volume may be related to the changing landscape of that sector and some owners opting to sell their existing properties to strategic buyers who plan to take advantage of the sector’s current opportunities. Combined, the rolling four-quarter total senior housing and care volume was $20.4 billion, down 6% from the prior quarter of $21.7 billion and 19% below its peak of $25 billion in the second quarter of 2015.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

The number of closed transactions was also lower in the first quarter and fell 21% to 114 from 145 closed transactions in the fourth quarter. Of the 114 closed transactions in the first quarter, 89 were single-property transactions (down 16% from 106 in the fourth quarter), while the remaining 25 were portfolio transactions (down 36% from 39). There is often a drop from the fourth quarter of the year to the first quarter due to the rush to close deals prior to year-end. On a year-over-year basis, transactions count also was off, however, declining 29% from 160 transactions in the first quarter of 2015.

Much of the drop in volume was caused by a slowdown in activity by public companies and, in particular, the public REITs. Indeed, deal volume by public companies fell 67% to $646 million in the first quarter of 2016 from $2 billion in the fourth quarter and was down 79% from $3.1 billion in the first quarter of 2015. It was the lowest volume by public companies in four years and may reflect the higher cost of capital many REITs are presently facing.

The absence of public REITs also influenced the size of the deals, with only two transactions valued at more than $500 million:

- The GE Capital Portfolio, a majority nursing care transaction for a total of $765 million, which came out to $87,133 per bed. The total bed count was 8,781 across 78 properties. The buyer was Formation Capital, and the seller was GE Capital.

- The Northstar Realty senior housing buyout portfolio, which was priced at $534 million and is the remaining buyout from the larger $890.8 million deal from last year. The price per unit was $227,718. The total unit count was 3,912 units across 32 properties. The buyer was Northstar Healthcare, and the seller was NorthStar Realty Finance.

The average price per unit for seniors housing properties remained high in the first quarter of 2016, but was off recent peaks, possibly reflecting the slowdown in buyer activity. The rolling four-quarter average price per unit for seniors housing properties was $169,800, down 5% from the fourth quarter of 2015 and down 0.7% from year-earlier levels. The rolling four-quarter average price per bed for nursing care properties was $79,800, down 2% from a year ago.

[/expand] [cresta-social-share]

Succession Happens: How Can You be More Prepared?

No matter how certain the future appears, succession planning is an essential part of doing business. Based on the 2014 U.S. census, the current average management term is 6.9 years. And yet in June 2015, U.S. Trust released the results of its “Wealth and Worth Survey,” which sampled business owners with at least $3 million in investable assets. The study found that nearly two-thirds of business owners did not have a succession plan. As baby boomers continue to retire in increasing numbers, the impact of succession planning will become even greater.

Ideally, a succession transition would be an orderly change with time for a thoughtfully planned and executed process. But as Noel Tichy, director of the Global Leadership Program at the University of Michigan’s Ross School of Business, points out in the January/February 2015 issue of The Corporate Board, 80% of corporations get succession wrong. Unfortunately, it often happens unexpectedly (or with little notice) due to any number of reasons, including performance issues, retirement, or opportunities elsewhere. And while the process of planning for smooth transitions can be daunting, organizations that ignore succession planning can place their companies at serious risk.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

As part of NIC’s ongoing commitment to leadership development, the topic of succession was discussed at a Future Leaders Council (FLC) meeting. Recently, FLC member Amy Coppens, marketing director with Senior Resource Group caught up with Eric Mendelsohn, president and CEO at National Health Investors and former FLC chair to discuss his experience with succession planning.

FLC: How does leadership transition typically happen?

Mendelsohn: Ideally, leadership transitions occur through training and grooming, perhaps drawing from a company’s “deep bench.” The successor will have a proven track record, people skills, and even a “sixth sense”—that intuitive ability to connect the dots. Unfortunately, often leadership transitions can happen suddenly, resulting from good people getting antsy or feeling the need to move on, or even less ideal circumstances, such as resignation, removal, or unplanned departures.

FLC: Where should you begin when thinking about succession?

Mendelsohn: There are several questions you can start with. First, is there an existing candidate who can take the reins for a time if a leadership position were to become vacant tomorrow? Second, who can you develop now so that he or she will be prepared tomorrow? Third, do you have a team strong enough to ease the transition and help that new leader?

FLC: If a transition becomes imminent, how can someone best position themselves?

Mendelsohn: When transitions happen, you want to be prepared. Try to position yourself to be in the right place at the right time. Use your free time to become a better leader. I tell my direct reports that every day is an interview for advancement. There is so much knowledge out there from people who have been through transitional situations. Take notes on the leaders you know and admire. Read and re-read business books, or listen to podcasts that inspire you. Keep a diary with your notes and best practices.

FLC: Do you have any recommendations on how to become better prepared?

Mendelsohn: I think there are some key areas that you can focus and start on now:

- Raise your hand when there is an opportunity to lead.

- Know your strengths and take on assignments outside your comfort zone.

- Fill in on an interim basis for people taking leave or while the search for a new candidate is in process.

- Try to be flexible with regards to geography. Oftentimes taking on a new project in a new region can expand your knowledge and experience as well as help your company.

- Ask for feedback. Don’t wait for a review. Be engaged and ask the obvious questions early on in the process.

- Be gracious if you are not chosen. There are often many reasons why decisions are made and not all of them are in your control. Support the new candidate. Transition happens. You may find the experience serves you well next time.

FLC: Any last thoughts?

Mendelsohn: Network, network, network. Opportunities come from many different avenues. Be involved in industry organizations like NIC. The Future Leaders Council offered me a great opportunity to connect with peers and competitors alike as well as to become more involved in initiatives. The experience allowed me to grow my experience, knowledge, and skills, and to network with others within the industry.

[/expand] [cresta-social-share]

Registration Opening Soon for the 2016 NIC Fall Conference

A Focus on the Industry’s Adaptability to Change

Registration for the 2016 NIC Fall Conference (formerly the National Conference) opens the first week of May. The conference will be held September 14–16 at the Marriott Marquis in downtown Washington, D.C.

The focus of this year’s conference is how owners, operators, and capital providers are adapting and responding to the sweeping changes reshaping seniors housing and care in America.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

“Last year at the conference, we were deducing a future that is just now starting to come into focus,” said NIC CEO Robert Kramer. “This year, we will be discussing how providers of both care and capital are implementing strategies to respond to today’s changes in policy and capital markets, as well as to tomorrow’s competitive landscape and more demanding customer.”

Keynote on the General Election

Politics will be a central talking point, with the nation heading to the polls less than two months after the conference ends.

Veteran political observers David Brooks and E.J. Dionne will speak at the Conference Luncheon. They will share their perspectives on the likely winners in November and the impact of a new president and new Congress on key areas of public policy, such as tax reform, health care, housing, and entitlement programs.

Strategies for the Near-Term and Visions of the Long-Term

The programming for this year’s conference will focus on today’s strategies in the face of tomorrow’s disruptive forces.

NIC Talks returns in 2016 with industry insiders and outside disruptors providing a window into the future of aging in America. The speakers will share how they believe the next ten years will revolutionize the aging experience of the boomers, who begin turning 80 in 2026, and will transform the field of housing, personal care, and health care for America’s elders.

The pre-conference Seniors Housing Boot Camp will provide capital providers and developers who are new to the seniors housing and care industry insight into the property investment decision process. This highly interactive workshop will use an actual case study to show participants how to analyze the key decision points for a property acquisition and how to assess a prospective transaction.

Other key topics include:

- Supply and demand conditions at the local market level and how they may change

- CMS’ initiatives and the transformation of the skilled nursing business

- The changing capital markets—who has the money and at what cost

- Underwriting properties in today’s supply growth environment

- Demographic changes and what they portend for markets and products

- Strategies for increasing property values and the value of operations

Early Registrants Save

NIC is offering an early bird discount for all who register by Friday, July 15. To be notified once registration for the 2016 NIC Fall Conference opens, complete this form.

[/expand] [cresta-social-share]

Seniors Housing & Care Industry Calendar

May 2016:

9-12 Argentum Senior Living Executive Conference, Denver, CO

18-19 Aging2.0 Global Innovation Summit, San Francisco, CA

June 2016:

7-9 REITWeek®: NAREIT’s Investor Forum, New York, NY

16-17 ASHA Mid-Year Meeting, Denver, CO

NIC Partners

We gratefully acknowledge our following partners: