Accelerating Demand for Seniors Housing Creates Long-Term Opportunity: A Conversation with Qahir Madhany of the Investment Giant Blackstone

Qahir Madhany

As the largest real estate private equity firm in the world today with $111 billion of assets under management, Blackstone is known for taking the long view of investments. This strategy dovetails squarely with the senior living market as a record number of people begin to enter their retirement years.

Qahir Madhany, managing director in the real estate group at Blackstone in New York, recently spoke with NIC’s Chief Economist Beth Burnham Mace. In their conversation, Madhany outlined the firm’s strategy and provided some thoughts on where the seniors housing and care market is headed.

Here is a recap of their discussion:

Mace: How long has Blackstone been investing in the seniors housing and care sector?

Madhany: We have been active in the seniors housing space for over a decade. Our first investment came in 2006. Since then we have acquired over 23,000 units and have a simple thesis. We want to create the best experience for our residents, so we buy communities, and then we make them better by adding amenities and investing a significant amount of capital. On average, we have been able to increase occupancy by over 10% in our communities through capital investment and careful management.

Mace: Why did the organization enter the sector? For a while, you stayed on the side lines. Now you are active again. Can you explain how you came in and out and in again?

Madhany: What is most attractive about the seniors housing space is that it has arguably the best positive long-term demand fundamentals of any asset class in the U.S. Senior housing demand is expected to grow by nearly 50% over the next 10 years. As we look further out, this trend is expected to accelerate, which means there will be increased demand over the next decade for seniors housing. We believe we can capitalize on this trend by providing a great product to the growing aging population.

Mace: What are the opportunities as well as the challenges you see for the seniors housing and care sector? In both the near-term and the long-term?

Madhany: I mentioned the opportunity – significant growth in the appropriate demographic of the U.S. population, which will lead to significant demand for housing. With this demand, comes an opportunity to provide a differentiated product. Whether utilizing new technology or increasing the standard of care, there exists a clear opportunity to provide a best-in-class product to residents. We believe the opportunity exists to utilize better technology and to be innovative in the sector, while providing a very high level of service and care. The challenges are the corollary to these opportunities. Given the importance of the quality of service provided, it is important that all operators provide a very high level of care and quality of product for their residents and also provide a positive experience.

Mace: Do you provide private equity to all seniors housing segments, which includes independent living, assisted living, memory care, and skilled nursing care? Is there one segment you favor over others? Are you national in scope?

Madhany: Our current portfolio is national in scope and focused primarily on assisted and independent living properties. We have some memory care units within our communities, but we do not have any standalone memory care facilities. We focus on opportunities where we can make capital and operational improvements to create a more desirable community for residents. Accordingly, we look at opportunities across all senior housing segments and in all geographies, but our typical investment is in a mature in-fill location where our reinvestment strategy can result in dramatic improvement of the property and its operations.

Mace: When do you turn down a deal? Are there any immediate red flags?

Madhany: As we make investment decisions, we are focused on a number of factors, but our investment thesis is centered on buying communities that we can improve. We are more cautious in high supply markets. If the community is physically flawed, either from being poorly maintained or obsolete from a layout perspective, we will be less interested in the opportunity.

Mace: There are a lot of newcomers to the industry, including new private equity groups. What challenges do they face?

Madhany: One is that there is a significant amount of new supply in the sector, so buying in markets with limited new supply or strong demand fundamentals will provide the best investment opportunity. Secondly, it is important to work together with operators so that we are all thinking creatively about how to deliver the best level of service for our residents. This will allow you to differentiate your community and generate strong demand. Great operations and a positive partnership between owners and operators is the key to success in the space.

What You Should Know about Population Health: A Conversation with NIC’s New Board Member Dr. David B. Nash

Dr. David Nash, MD, MBA

In recognition of the dramatic disruptions anticipated in seniors housing and care, NIC is expanding its board of directors to include representatives of the healthcare community. This realignment reflects the growth of the delivery and coordination of a wide variety of healthcare care services in senior living communities.

The new composition of NIC’s board comes after a strategic review in 2014-15 of its market and mission, which confirmed that the next generation of residents will demand a different type of community. Also, innovations in technology, such as the emergence of telemedicine, and changes in healthcare delivery and payment mechanisms suggest that seniors housing will play a more central role in resident healthcare going forward.

In order to meet these challenges, NIC has announced several new board appointments, including Dr. David Nash, M.D., MBA, Dean, Jefferson College of Population Health, Jefferson University. He is a renowned policy expert and world leader in population health and the application of data to provide transparency to improve healthcare delivery and outcomes. Dr. Nash is also a member of the board of directors of Humana, Inc.

NIC recently talked to Dr. Nash about his work and how it relates to the seniors housing and care industry. Here’s a recap of the conversation.

NIC: What attracted you to serve on NIC’s board of directors?

Nash: The mission of NIC to serve the elderly in its capacity as a nonprofit organization aligns perfectly with one of the goals of our college, which is to promote population health. Secondly, from a research perspective, I’m fascinated by the NIC MAP® Data Service and assessing how we can conduct population-based research using the incredible data set NIC has created. Thirdly, and more personally, I’m very interested in healthy aging with my wife, and maybe even being a leader in helping people achieve good health during the later stages of life. NIC includes an incredible group of accomplished professionals and reaches a wide network of national experts. Working with NIC brings everything together nicely for me — the mission, the research, and my personal and professional life.

NIC: What is population health?

Nash: Population health connects health and health care in a new way. It builds on the core of good work that comes from public health, such as epidemiology, behavioral issues, clean water, vaccinations and obesity reduction. But population health adds another layer: what does all of that cost? Are we achieving value when we deliver healthcare? And what is the quality and safety of the care we are delivering? Public health programs have been around since World War II. Population health is the umbrella over public health that covers the missing pieces of cost, quality and safety. Jefferson is home to the first college of population health in the nation. There are six more such colleges in development across the country, and we are assisting all of them. Population health is a movement—a recognition of the complexity of healthcare system and its costs.

NIC: What long-term factors are driving the growth of population health?

Nash: The unsustainable nature of costs in our system. We spend $3 trillion on healthcare annually. That’s $10,000 per person. Experts believe that one-third of that $3 trillion is of no value. That is an unsustainable situation. Our country has failed to have the conversation about whether healthcare is a right of citizenship or a commodity that must be purchased. Our college believes that universal access is a right of citizenship. That doesn’t mean everything should be paid for, but health care should not be denied to anyone, and no one should go bankrupt from the inability to pay for medical care. We embrace universal access because that’s how you improve the health of the population.

NIC: What role do outcomes, data and transparency play in population health?

Nash: Ten years ago, Dr. Donald Berwick, at the Institute for Healthcare Improvement, wrote an important paper on the need to promote the “Triple Aim,” a vision for reforming the American healthcare system. His paper came out the same year our college was created. The “Triple Aim” was to improve the health of the population, reduce the costs of healthcare, and improve the experience of care for the patient. We believe population health is a cornerstone of the “Triple Aim.”

You can’t reduce costs without transparency of the data. Why get my knee replaced in your hospital if it costs $10,000 more than another hospital, with no better results? Because there is no transparency, consumers can’t make an informed choice about where to go. Also, without transparency, you can’t reduce medical error—the fourth leading cause of death in America. We have a saying, “Sunshine is the Best Disinfectant.” We are totally aligned with transparency.

NIC: What opportunities and challenges does the rapidly increasing focus on population health create for seniors housing and care providers and investors?

Nash: Of course, the fact that there are 10,000 people turning 65 a day represents a huge economic challenge. We want to find a way to assure adequate and appropriate housing. We want people to be able to safely age in place, bringing appropriate services to them wherever possible, and work to coordinate their care. We believe that will help to improve health, reduce visits to the hospital, avoid complications, and unnecessary testing. It’s all interconnected. We want to provide our growing elderly population with a good experience when they do engage with the healthcare system. If we do all that, we will have better outcomes at a lower cost. In our language, that is value.

NIC: Any advice to providers of seniors housing to take advantage of the opportunities in the quickly evolving world of value-based care?

Nash: I am particularly interested in finding new ways to use technology to bring outstanding medical care directly to seniors wherever they are. I’m excited to be a part of the NIC board as technology improves in the areas of telemedicine, teleradiology and telebehavioral health. The last place we want to send a senior is to the emergency room of a hospital. It’s really amazing how it all fits together.

NIC: How can senior living providers learn more about their role in population health?

Nash: A valuable way to get a better understanding of the opportunities for seniors housing and care providers is to attend the upcoming Population Health Colloquium that I’m chairing. The event is being held March 19-21 at the Loews Philadelphia Hotel in Philadelphia. It is also being live streamed for those who can’t attend in person.

The Colloquium brings together a wide range of healthcare stakeholders including managed care executives, medical directors, and C-suite executives. The program will feature a lot of content of interest to the senior living industry, such as leveraging data and technology to provide better care, optimizing outcomes, and exploring solutions to the challenges posed by today’s dynamic healthcare environment. Everyone is invited to attend. This is the 18th year we’ve held the Colloquium, and we’re hoping to set a new record of more than 800 attendees this year.

If you’d like to learn more about the upcoming Population Health Colloquium, please visit https://populationhealthcolloquium.com/.

Vertical Integration of Healthcare Payors and Providers Foreshadows Transformative Shift in Senior Care

NIC Spring Forum session to address impact for investors

Recent corporate mega-mergers in the healthcare industry are a signal that the delivery and payments system is undergoing a massive shift. This transformation is expected to have a lasting impact on the seniors housing and care sector, as providers and insurance companies integrate their services to reduce costs and provide better patient and resident outcomes, and access to services.

“Healthcare providers and payors are merging, and the senior living industry has to be a part of that change,” said Anne Tumlinson, CEO at Anne Tumlinson Innovations, who will lead a session for investors on the topic at the upcoming 2018 NIC Spring Investment Forum, March 7-9, at the Omni Dallas Hotel. “We must get ahead of this trend.”

The merger of payors and providers is picking up steam. In fact, three big transactions were announced just in December:

- Insurance giant Humana (NYSE: HUM) announced its intent to purchase Kindred Healthcare (NYSE: KND) in a $4.1 billion deal. The transaction will spin off Kindred at Home, the nation’s largest home health and hospice care provider, in order to enhance access to care and reduce costs. Humana plans to leverage Kindred’s operations to manage its Medicare Advantage population at home, according to a company press release.

- Pharmacy company CVS (NYSE: CVS) agreed to acquire Aetna (NYSE: AET), the nation’s third largest insurance provider in a transaction valued at $69 billion. The combined company aims to offer consumers services at CVS locations and to expand community based and in-home care.

- Managed healthcare provider UnitedHealth Group (NYSE: UNH) announced that it had reached a $4.9 billion deal to acquire DaVita Medical Group, a healthcare services company with nearly 300 clinics, 35 urgent care centers, and 6 outpatient surgery sites. DaVita Medical Group treats about 1.7 million patients annually.

The mergers are reflective of three long-term trends, said Tumlinson. The first is recognition that the delivery of support services and medical care at home is a powerful way to reform and change the healthcare system. Tumlinson cites the example of an elderly frail woman with cognitive impairments who was treated three times in the hospital for a gastrointestinal problem. The doctors could not determine the cause until one of them visited her at home, where she lived alone, and found she was eating spoiled food. An initial touch point in the home would have avoided hospital charges of about $50,000.

“The effort to get more information on a personal level will help payors that are taking the risk for healthcare to better manage senior populations. This trend is just the tip of the iceberg,” said Tumlinson.

The merger uptick is being fed by another long-term trend: consumers want home care and person-centered care. Tumlinson makes the comparison to Amazon, the online shopping giant that delivers whatever you need to your doorstep. “That’s what consumers expect,” she said.

The third trend is the alignment of the different roles in the healthcare space. In the past, healthcare services have been organized in clearly delineated silos of payors, service providers and clinicians. But the healthcare sector is evolving into a world where the provider of the service and the bill payor are becoming a single entity which manages the heath of a population with a pool of dollars, noted Tumlinson. “The system is being totally transformed.”

Impact on seniors housing and care

While home-based care has traditionally been viewed as a competitive threat to seniors housing and skilled nursing properties, the emerging paradigm emphasizes partnerships and cooperation, said Tumlinson. Competition will not be between a senior living provider and a home care provider trying to keep an elder at home, she explained. Instead, senior living operators along with their health and home care provider partners will be competing against other senior living operators and their strategic partners.

“Whichever provider offers the best solution for a high quality of life, along with wellness services, coordination of care and support for the family will win the most business,” said Tumlinson.

These concepts will be explored at NIC’s Spring Forum during Tumlinson’s session titled, “What Seniors Housing & Care Investors Need to Know About Healthcare and Why It’s Important.”

The session is one of 17 educational breakout sessions planned at the event. The Spring Forum draws over 1,500 attendees and brings together leaders in seniors housing, skilled nursing, healthcare, home health and home care, finance, and care coordination to share game-changing ideas and cutting-edge success strategies.

The theme of the three-day Spring Forum is “Unlocking New Value in Senior Care Collaboration.” In addition to the educational sessions and two general sessions, the event offers networking opportunities, ample meeting areas, and nightly receptions.

Key takeaways from Tumlinson’s session for investors will include:

- A working knowledge of the major healthcare payors, both government and private, and how their respective roles are shifting as well as how that affects the value of investments

- Major trends in how different programs finance care, and how senior care providers are adapting to the changes

- The variety of ways senior care providers are being impacted and adapting to changes in the healthcare sector

“I’m really excited about this session,” said Tumlinson. She acknowledges the reluctance of some investors to address the issue of healthcare, but this session will provide a roadmap of where the trend is headed and why it’s important.

Investors need to adjust their concept of “home,” said Tumlinson. It’s not just a single-family house or condominium. “Home” for many frail elders is a seniors housing and care property. And residents, and their families, are seeking on-site healthcare and care coordination.

Partnerships with providers and cutting-edge technology will be a big part of the solution, said Tumlinson. She points, for example, to Juniper Communities with its Connect4Life program which coordinates and oversees healthcare on behalf of its residents. “It’s another way to prevent people from having to move to higher acuity care settings,” said Tumlinson. (Juniper’s Founder and President Lynne Katzmann will be featured on a number of panels at NIC’s Spring Forum.)

Tumlinson points out that as healthcare providers and payors merge, seniors housing and care investors and operators should carefully evaluate how they’re keeping up with these trends. “The senior living business model is at risk if they don’t think about what value they can add to the housing equation,” she said.

Registration for the 2018 NIC Spring Investment Forum is open now. Click here to register.

Seniors Housing Occupancy Unchanged, While Same-Store Rent Growth Decelerated

Five Key Takeaways from NIC MAP’s Fourth Quarter Seniors Housing Data Release

NIC MAP® Data Service clients attended a webinar in January on the key seniors housing data trends during the fourth quarter of 2017. Five key takeaways emerged:

- Seniors housing occupancy was unchanged at 88.8%

- Annual inventory growth and annual absorption for both assisted living and independent living flattened during the quarter

- Nearly one-third of seniors housing inventory growth in past three years occurred in eight metropolitan markets

- Same-store rent growth decelerated

- Closed transaction volume slowed in fourth quarter, but preliminary annual estimates for 2017 are generally comparable to 2016

Let’s take a closer look at some of these trends.

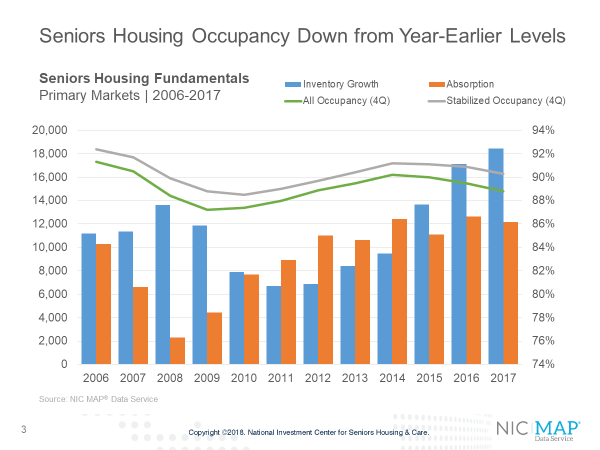

Seniors housing occupancy was unchanged at 88.8%

The all occupancy rate for seniors housing, which includes properties still in lease up, was 88.8% in the fourth quarter, unchanged from the third quarter. This placed occupancy 1.8 percentage points above its cyclical low of 87.0%, reached during the first quarter of 2010, and 1.4 percentage points below its most recent high of 90.2% in the fourth quarter of 2014. For the four quarters ending in the fourth quarter, 18,500 units were added to inventory versus 12,200 units absorbed. As a result, occupancy fell 70 basis points from the fourth quarter of 2016.

Stabilized occupancy for all senior living properties (defined by NIC as properties that have been open for at least two years or, if open for less than two years, with an occupancy level of 95%) was higher than all occupancy and stood at 90.3% in the fourth quarter, down 60 basis points from its year-earlier level. The difference between all occupancy and stabilized occupancy was 150 basis points, up from 140 basis points at the end of last year. The size of this gap reflects the large number of properties recently opened and still in lease up.

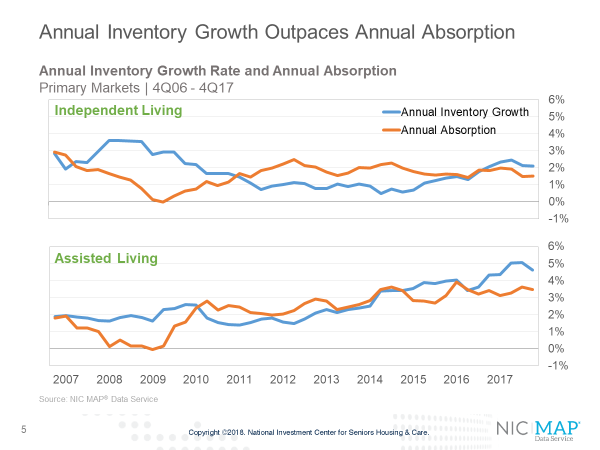

Annual inventory growth and annual absorption for both assisted living and independent living flattened during the quarter

Assisted living inventory growth has been ramping up for a longer period than independent living in the Primary Markets. In mid-2012, the occupancy rate of independent living was the same as for assisted living at 88.8%. Since that time, there has been a clear divergence in occupancy performance reflecting the differences in supply growth and demand for the two property types.

For majority independent living properties, inventory growth exceeded absorption by 60 basis points in the fourth quarter—2.1% versus 1.5%. The occupancy rate for majority independent living properties was 90.6% in the fourth quarter.

Annual inventory growth for majority assisted living properties was 4.6%, down a bit from the third quarter. Annual absorption slipped back to a pace of 3.6%. The occupancy rate for assisted living was 86.5% in the fourth quarter.

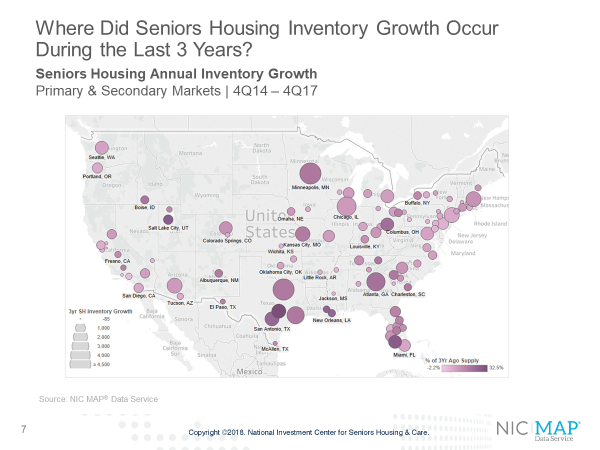

Nearly one-third of seniors housing inventory growth in past three years occurred in eight metropolitan markets

During the past three years, there have been nearly 79,000 units added to the stock of seniors housing inventory among the Primary and Secondary markets. Nearly one-third of this growth occurred in eight metro areas: Dallas, Minneapolis, Chicago, Atlanta, Houston, Boston, Phoenix, and New York. Dallas alone accounted for 5% of all new seniors housing inventory in the past three years. This is depicted in the map exhibit below by the size of the purple circles, with the larger the circle, the more the absolute number of units of inventory growth.

Relative to each metropolitan area’s own inventory, there were eleven geographies that experienced gains in inventory of more than 20% over the course of the past three years. They include Austin, Fort Myers, Salt Lake City, Baton Rouge, New Orleans, San Antonio, Columbus, Atlanta, and Boise and are depicted by the darker shades of purple circles on the map.

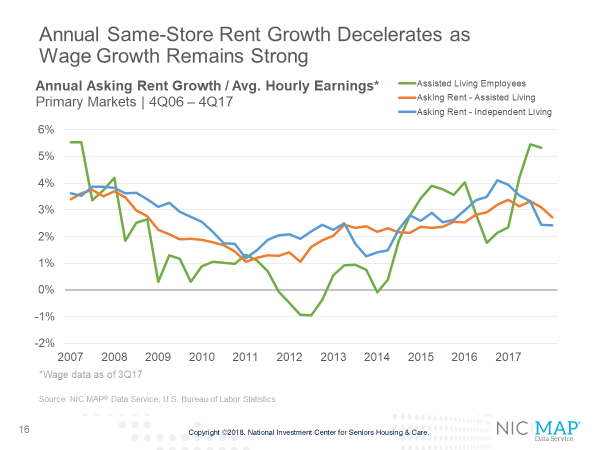

Same-store rent growth decelerated

Same-store asking rent growth for seniors housing slowed in the fourth quarter, with year-over-year growth of 2.6%. This was down from 3.7% in the fourth quarter of last year when it reached a cyclical peak but was equal to its long-term average pace experienced since late 2006 of 2.6%.

Asking rent growth for majority assisted living properties was 2.7% in the fourth quarter, down 40 basis points from the third quarter. For majority independent living, rent growth remained at its third quarter pace of 2.4%, but was well below the 4.1% pace it achieved in the third quarter of 2016 when rent growth reached its highest pace since NIC began collecting this data.

There is wide variation in rent growth. Among the Primary Markets, the top ranked metropolitan areas for year-over-year rent growth in seniors housing were San Jose, Seattle, Los Angeles, Las Vegas, and Portland, Oregon. The weakest rent growth was in Kansas City, Atlanta, Chicago and San Antonio. Many of these latter markets also had some of the lowest fourth quarter occupancy rates in the nation.

Closed transaction volume slowed in fourth quarter, but preliminary annual estimates for 2017 are generally comparable to 2016

The fourth quarter saw a slowdown in closed transaction volume. Preliminary data shows that seniors housing and care transactions volume totaled $2.1 billion in the fourth quarter, which is the sum of $900 million in seniors housing sales and $1.2 billion in nursing care. The total volume was down 37.6% from a year ago and was the lowest quarterly volume since the second quarter of 2013.

For the year, seniors housing and care transactions volume totaled $14.1 billion, comprised of $7.9 billion in seniors housing and $6.2 billion in nursing care transactions. The total volume was down 2.8% from 2016 and 35.5% from 2015.

There were 466 closed deals in 2017. Of this, 90 were portfolio transactions, and 356 were single property transactions. In 2016, these numbers were 538, 109, and 429, respectively.

Seniors housing ranks high in 2018 Emerging Trends Real Estate®

Lastly, its notable that seniors housing is getting more attention from the investment community. In the recently released 2018 Emerging Trends in Real Estate®, produced jointly by PwC and the Urban Land Institute, seniors housing ranks high for best prospects in 2018 for both investment and development. According to the annual survey’s U.S. respondents, seniors housing ranked:

- Third among all 24 commercial and multifamily subsectors, and

- First among the 7 residential property types.

The report further highlights the strength of seniors housing’s investment returns and its rising liquidity based on sales transactions volumes. These survey results bode well for continued interest among investors and developers in seniors housing properties going forward.

What are the Latest Trends for Skilled Nursing Properties?

By Bill Kauffman

The skilled nursing sector continues to face significant challenges from staffing issues, and occupancy and length-of-stay declines, to reimbursement pressure from insurance companies. Some have called the current operating environment a “perfect storm” or “being backed into a corner.” The reality is that we will continue to see some consolidation, and operators will question their current business model (e.g., Does partnering make sense? Is it best to offer other services?). Or perhaps, operators will think about exiting the skilled nursing business.

Although the challenges are persistent and can vary (and it certainly depends on the local market), some investors are taking the contrarian view and making bets on the strength of the industry going forward based on aging demographics or the need for care specializations in certain markets. However, one of the items on the checklist that operators and investors need to understand, before making their decisions, are the current trends.

NIC released its latest Skilled Nursing Data Report in December 2017, providing key monthly data points on skilled nursing market metrics from October 2012 through September 2017.

Occupancy

Occupancy at skilled nursing properties has continued to be challenged for a variety of reasons, which could include declining lengths of stay due to pressure from insurance companies and hospitals and/or competition from other alternative options like home-based care. The third quarter of 2017 marked a new low for occupancy over the past five years despite an uptick from July to August. Occupancy reached 81.6% in the third quarter of 2017, down 29 basis points from the second quarter.

One could ask about seasonality and how that affects the third quarter occupancy each year. However, within the data set, the third quarter from July to September has not seen a consistent seasonality pattern of declining occupancy, as has usually been seen, for example, from March to June each year.

When we look at the year-over-year comparison, we see that occupancy declined a steep 167 basis points, which is the second largest annual decline in the last five years for the third quarter. Downward pressure on occupancy has been steady since May 2015, which was around the time when the Centers for Medicare and Medicaid Services (CMS) started to roll out payment initiatives throughout the country. Occupancy is down 343 basis points since May 2015.

So what can operators do, and investors look for, to mitigate these pressures? Depending on their markets, many operators might have to redefine their businesses. Whether that be through innovative care models, running their own insurance plan, specializing in higher acuity, or perhaps all of the above. One thing is for certain, doing nothing is not an option for survival.

Patient Day Mix

As we peel back the occupancy figures, the latest report shows the main driver of lower occupancy continues to be the decline in Medicare patient day mix. It declined 58 basis points from the second quarter and 84 basis points from year-earlier levels, coming in at a new low of 12.2% in the third quarter of 2017. The trend has clearly been on the downside as the average Medicare patient day mix for the 12-month period ending in September 2017 was 13%, compared to 14% from September 2015 to September 2016, and 15% in the 12-month period from September 2014 to September 2015.

Numerous factors have been contributing to this downtrend, including competition from home health, pressure on length of stay as mentioned above, and the increase of procedures being performed in an outpatient setting instead of the hospital, therefore limiting the pool of potential patients going to skilled nursing properties.

While Medicare mix has been shrinking, Medicaid mix continues its climb. Medicaid patient day mix continues to make up a growing share of occupancy, reaching its highest point in the five-year time-series at 66.8%. Medicaid mix was up 80 basis points from last quarter and 112 basis points from a year ago. It has increased 422 basis points in the last five years, from 62.6% in the third quarter of 2014.

Managed Medicare patient mix has also been growing. In the latest 12-month period ending September 2017, it was up to 6.3% compared to 5.9% for the previous 12-month period ending September 2016. Over the five-year time-series, Managed Medicare patient day mix is up from 5.1% in October 2012.

Lastly, let’s discuss the private mix. At 9.1%, private patient day mix again matched its lowest point in September 2017, which previously had occurred in April 2017. The lowest private patient day mixes in the five-year time series have occurred in 10 of the last 12 months. It is down 25 basis points from June 2017 and down 73 basis points compared to a year ago.

Revenue Per Patient Day

When it comes to revenue per patient day (RPPD), the latest report shows that Medicaid RPPD grew close to 1% from the prior quarter, and it grew at a relatively strong 2.4% year-over-year pace. It ended September 2017 at $203. Private RPPD also grew; up 0.12% from the prior quarter and 2.8% year-over-year.

Switching gears a bit, we turn to look at an RPPD story NIC has been following closely the last couple years relating to managed Medicare RPPD. As enrollment in managed Medicare, a.k.a. Medicare Advantage, has increased across our country, it has become a hot topic in healthcare. We see, as stated above, that the patient day mix has been growing. Yes, slightly, but still growing, and that trend is likely to continue. Additionally, the RPPD, which skilled nursing properties receive from these insurance companies, has been trending down the past five years.

Managed Medicare RPPD declined from the prior quarter to set a new low within the time series at $431. This represents a total decline of 13.2% from five years ago, or a negative 2.8% compounded annual growth rate over the same time period. Quarter-over-quarter, the rate fell 1.8%, which was a significant deterioration from the prior quarter’s decline of only 0.2%. The rate fell 2.1% from the year-earlier level of $440 revenue per patient day. This trend continues to warrant attention, and NIC will keep you informed with the next report due to be released in March 2018.

You can download this latest report here: http://www.nic.org/analytics/nic-initiatives/skilled-nursing-data-initiative.

The next NIC Skilled Nursing Data Report, scheduled for release in March, will include new data cuts—both urban vs. rural metrics, as well as revenue mix.

Thoughts from NIC’s Chief Economist: Tax Policy and the Economy

By Beth Burnham Mace

The $1.5 trillion, 10-year tax cut passed by Congress and signed into law by President Trump on December 22nd is expected to moderately boost economic growth for the next two years before slowing it down thereafter according to the view by many, but not all, economists and pundits. Longer run, the deficit-financed tax cuts will add to the government’s deficits and debt load.

Through the remainder of the decade, the fiscal stimulus associated with the tax cuts is projected to boost GDP growth from 2.5% per year to 2.9% per year according to estimates by Moody’s Analytics and others. The impact is less than it may have been, however, due to today’s already strong economy (which has now generated more than 2 million jobs per year for seven consecutive years for only the second time in history) and the tightness of current labor market. With a December 2017 unemployment rate of 4.1%, a fiscally-stimulated stronger economy could possibly push the jobless rate to its lowest level since the 1950s—near 3%.

Tighter labor markets theoretically should result in upward pressure on wage rates and inflation expectations, which in turn is likely to force the Federal Reserve to raise interest rates as it tries to prevent the economy from overheating. It is notable though that the jobless rate has fallen to a 17-year low, and wage pressures by most accounts are still generally benign. In December, average hourly earnings were up by only 2.5% from year-earlier levels, although they were up significantly higher for assisted living wages at 5.3% in the third quarter. Many pundits are projecting three or more 25-basis points hikes in the federal funds rate in 2018 with more to follow in 2019.

Higher interest rates will counteract some of the stimulus created by the tax cuts, with the potential for a slowing economy in 2020 and thereafter. None of this is certain of course and, with Jerome Powell as the new Federal Reserve Chair in February, the response by the Fed may be different than that which would have happened under Janet Yellen. Longer term, the tax cuts will almost certainly result in higher debt levels and growing deficits which in turn may crowd out other investments, potentially adding further upward pressure to interest rates.

Tax Policy and Commercial Real Estate

In terms of the specifics of the tax law changes and the impact on commercial real estate, businesses and individuals, several analyses have been conducted, and a few are provided here.

- Tax Form Webinar Presentation by American Seniors Housing Association

- http://www.colliers.com/en-us/us/insights/marketnews/2018-tax-overhaul-special-report

- http://www.us.jll.com/united-states/en-us/research/snapshots/515/jll-guide-to-tax-reform

How Can Operators Grow Penetration Rates?

The occupancy rate for seniors housing was unchanged in the fourth quarter of 2017 at 88.8%, but remained 1.4 percentage point below its most recent high of 90.2% in the fourth quarter of 2014 as supply pressures in many markets continue to outflank demand. In markets where there is an unfavorable supply/demand imbalance, growing demand penetration rates might be a way to offset supply threats and downward pressures on occupancy rates. With that in mind, how can operators grow their own and the industry’s collective penetration rates?

Below is a list of some possibilities:

- Create the new “independent living” design and prototype aimed at the “boomerang generation”—individuals aged 70-plus who want to re-invent themselves with active living, continuing education, second “careers,” and volunteerism

- Provide greater service offerings that help the adult child manage the day-to-day needs of their aging parent residents with concierge-type services

- Engage in an industry-wide “Got Milk?” campaign to demonstrate the benefits and advantages—the value proposition—of residing in a seniors housing property

- Find solutions to relatively high-cost housing and fee structures to better make available senior living to lower income-threshold households

- Reduce the use of high-cost acute services by becoming part of the broader health care continuum and population health management practices that embrace the whole person in a value-based medical system, versus a fee-for-service system, by creating design-efficient, attractive housing with enhanced service and care features

- Create up-stream and down-stream relationships with hospitals and skilled nursing properties to create comprehensive and coordinated care

- Provide on-site services such as occupational and physical therapies, and regular exercise and wellness programs, to elongate residents’ length of stay and improve quality of life

- Focus on specialty care segments such as residents with COPD, diabetes, memory care and other care-intensive needs

- Offer services to the broader local community to familiarize it with seniors housing, while also offering fee-for-service care to the broader community

- Use technology to empower search engines for best-in-class marketing and leasing opportunities

- Employ technology to improve work efficiencies to afford staff more time with residents and improve quality and quantity of care

- Improve employee retention by providing a culture and work environment that makes staff want to stay in place to enhance long-lasting relationships with residents

- Provide a stimulating and enhanced environment with opportunity for community-based involvement including programs with young adults and children

- Offer choice of services, programs, dining experiences, room configurations, social outings and events

- Create outstanding offerings in customer service and customized experiences

Finally, think outside the box and reinvent seniors housing as we know it today. The “Silent Generation” currently residing in seniors housing was born between 1928 and 1945 and is setting the stage for the upcoming wave of baby boomers who will become prospective residents of seniors housing starting in 2026, when the first of them born in 1946 turns 80. This boomer generation has proven over the decades that it doesn’t do things the same way as their parents. And for this, we all need to be approaching the market in new and different ways.

As always, I welcome your feedback, thoughts, and comments.

Beth