Industry Leaders Look Ahead to 2015: Part 2

Brian Beckwith, CEO of Formation Capital, a private investment firm, based in Georgia, specializing in seniors housing and care, post-acute and health care real estate investments: Development has certainly increased and the activity levels are high. We still believe the industry is able to absorb the product in the pipeline, but the dynamics of a local market are the most important, as always.

Sheila Miller, director of seniors housing production and lender relationships, Fannie Mae, Washington D.C.: I think we are still on the upward slope of development cycle, but we are watching activity. It has been dispersed throughout the country, not in one particular market, but we are monitoring it closely. We are starting to see and hear from some borrowers looking at new construction that it’s getting difficult to find contractors.

Steven Schmidt, national director, seniors housing group, Freddie Mac, Chicago: When you look at NIC data, annual absorption and inventory growth are in good balance in independent and assisted living. But freestanding memory care has seen occupancy drift down since 2010, from about 89 percent to 85.5 percent. Independent and assisted living have generally been increasing their occupancies since 2010. Annual inventory growth of memory care was 9.0 percent, according to NIC MAP’s third quarter 2014 report. That compares to 3 percent for assisted living and 0.8 percent for independent living. I’ve heard anecdotally of a few cases where memory care is being converted to assisted living. But overall, I’m not too concerned about overbuilding. The last time the industry had overbuilding was in late 1990s before NIC had a robust data set. Investors today know where there’s construction and can’t ignore it.

NIC: What is the biggest challenge facing the industry in 2015?

Treffert: Understanding the incredibly dynamic health care landscape will be a challenge for every player as they make their plans for 2015 and beyond. We know changes are coming with bundled payments and the continued evolution of ACOs. Predicting the future may not be possible, but remaining nimble enough to navigate a variety of scenarios should be the goal of every operator.

Hutchens: Interest rate uncertainty is my biggest concern for 2015 given the direct relationship between cap rates and interest rates. As rates rise, cap rates will follow, but any delay will slow down deal flow while valuations get sorted out.

Martin: Talent. At the community level, hiring and retaining leadership is critical. Strong executive directors are a significant success factor for a community, as are program directors, marketing directors, and care givers.

Beckwith: For the first time in a while, the biggest risks for the industry luckily don’t seem to include material reimbursement changes. The biggest risk seems to be managing the exuberance and the aggressiveness that can come with very strong access to capital and new entrants to the market.

Miller: Owners and operators are looking to grow, but it’s difficult to acquire assets. REITs and institutional players are running up acquisition prices. It’s more challenging for small and mid-size operators to find properties in a reasonable price range to make it work for them.

Schmidt: Short term, the concern is overbuilding in select markets—both what is under way and what is permitted. Longer term, the challenge is to create affordable housing for seniors. As with college education, you reach a point where people can’t afford it. We’re catering to the upper quartile or 50 percent of the senior population in terms of income. If you want to grow, you don’t want to price yourself too high. But I don’t see anything on horizon technologically to have an impact on operating expenses. This is a very labor intensive business, and it takes kind and dedicated people to care for seniors. We would love to work with those who have interesting, new models in that respect.

Didn’t catch Part 1? Read more on what top executives in the industry think of what’s to come in 2015 in the first part of this two-part series. – See more at: http://www.nic.org/insider/stories/Industry_Leaders_Look_Ahead_to_2015_Part_2#sthash.ZF8DziYi.dpuf

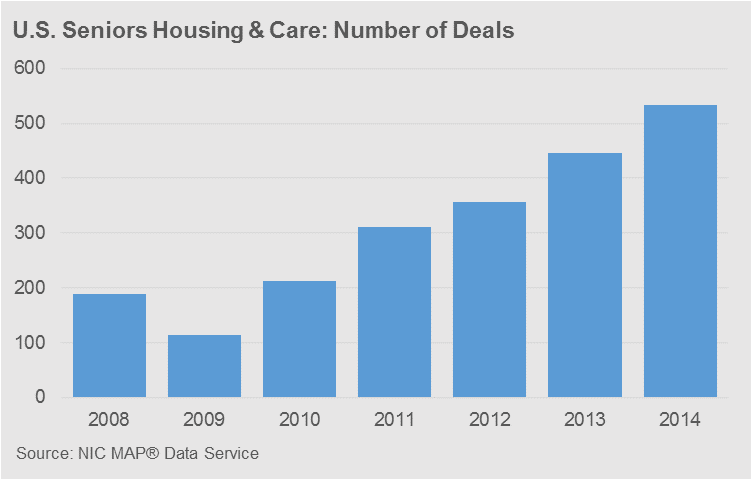

Transactions Market Ends Year on a Strong Note

More than 500 Deals Closed in 2014

The robust investment activity in seniors housing and care continued through the end of the year, with preliminary figures showing nearly $4bn in property sales during the fourth quarter. Overall, more than $17bn in seniors housing and care properties were acquired in 2014, up nearly 20% from last year.

![]()

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Sales volume during 2014 was second only to 2011’s staggering total of $27.6b, which was dominated by a handful of multi-billion dollar REIT transactions. In terms of the number of deals, 2014 was the most active year on record, with more than 500 deals closing.

The market continued to be dominated by the publicly-traded companies, with their volume totaling nearly $10bn last year. Private companies also remained very active, with their acquisitions at more than $5bn during 2014. Institutional investors continued to be the smallest investor type, but their investment activity has been consistently growing during the last few years. In 2014, institutional players acquired $1.8bn in seniors housing and care real estate, up 13% from last year.[/expand][cresta-social-share]

The Future Leaders Council New Member Spotlight

Susannah Myerson, vice president, Wells Fargo Bank, CRE – Senior Housing Finance

An industry veteran with particular expertise in market feasibility, Myerson joined the FLC in 2014 seeking to explore best practices and identify new initiatives in an effort to advance the industry. Myerson recently spoke with current FLC members, Amy Coppens of Senior Resource Group (SRG), and Melissa Owens of Elmcroft Senior Living. Here is an edited transcript of the conversation which highlights Myerson’s goals for the FLC.[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

FLC: What do you hope to gain from your term with the FLC? How would you characterize your experience so far?

Myerson: I hope to gain a deeper understanding of forces affecting the industry, and how those forces will help shape the industry in the next 10 to 20 years. And I hope to be part of the group that helps shape the industry!

What I have experienced so far with FLC is great. I am enjoying getting to know others at NIC and discussing topics for conferences, generating new ideas, and helping to advance the mission of NIC.

FLC: What’s the biggest trend impacting senior living today?

Myerson: I think affordability is a major issue. Millions of age 75+ households have incomes that are too high for them to qualify for affordable housing, yet too low for them to comfortably afford market-rate seniors housing. I think there is a huge need for the development of moderate priced seniors housing that operates in a way that does not sacrifice quality.

FLC: How do you hope to impact the industry through the FLC?

Myerson: One of the committees I am serving on is the University Internship Program, which I think is so important. I really enjoy helping to get this industry in front of students and attracting the best and the brightest to this business. Most college students probably have never considered working in the seniors housing field – much less visited a facility. But once they realize all the intricacies of the business, the rewarding career opportunities, and the great growth potential of the industry, I think they’d certainly be interested.

FLC: Is there any specific issue you hope to address during your tenure?

Myerson: That is a good question. One issue I’d like to help address is broadening the scope of the industry – both in terms of product type (such as including age-restricted apartments or co-housing communities) and in terms of geography (looking at seniors housing in other countries).[/expand][cresta-social-share]

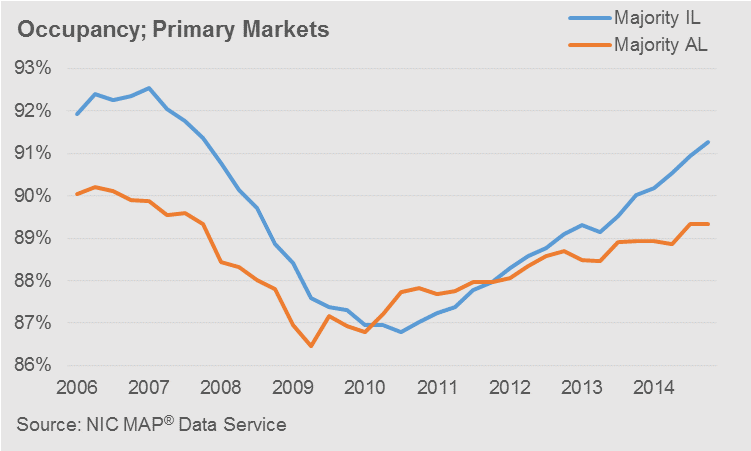

Independent Living Drives Fourth Quarter Occupancy Gains

Assisted Living Occupancy Flat Despite Solid Absorption

Independent living occupancy continued its recovery during the fourth quarter, while assisted living occupancy remained flat despite a healthy rate of absorption. During the fourth quarter, independent living occupancy rose 40 basis points to 91.3 percent, while assisted living occupancy remained stagnant at 89.3 percent.

[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Despite assisted living’s occupancy remaining unchanged during the fourth quarter, absorption continued to remain rather strong, however, it was offset by equally strong inventory growth. On a percent basis, absorption and inventory both increased by 0.8 percent for assisted living. To put into context, independent living’s absorption increased a 0.5 percent rate, but its supply only grew by 0.1 percent.

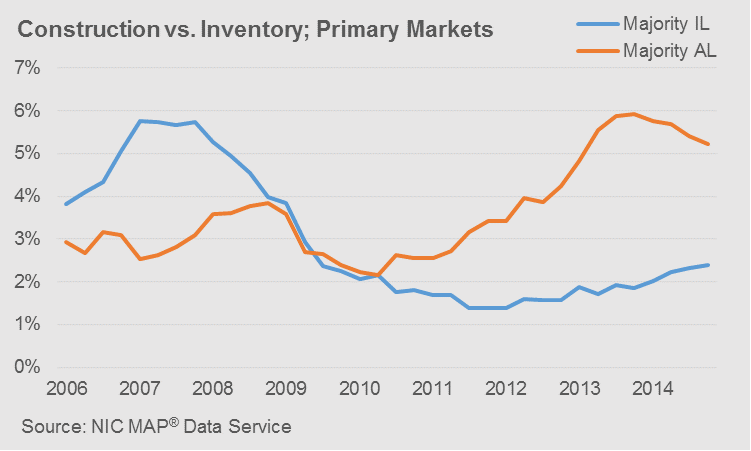

Recent trends in construction remained in place, with continued moderation in assisted living and modest acceleration in independent living, despite assisted living continuing to maintain a higher rate of construction. As of the fourth quarter, assisted living construction represented 5.2 percent of its supply, compared to 2.4 percent for independent living. Compared to a year ago, assisted living construction has slowed by 70 basis points, while independent living construction has risen by 60 basis points.

Based on recent construction activity, inventory should continue to grow near recent rates for each property type. Assisted living will continue to experience relatively strong rates of growth, while independent living will continue to experience little impact from new supply. Despite the likelihood assisted living will continue to grow at a robust pace, NIC Research forecasts a fairly balanced supply-demand scenario for 2015. Independent living occupancy will likely continue along its current trajectory, as it continues to enjoy the benefits from tempered supply.[/expand][cresta-social-share]

Long-Term Care Policy Expert Dr. Bruce Chernof to Headline NIC 2015 Forum

Key takeaways:

– Focus on quality of life.

– Housing and care plays pivotal role.

– Opportune moment for industry.

As the health care system undergoes a dramatic shift to focus on value-based outcomes, seniors housing and care providers will be a powerful voice in the discussion of how best to improve the quality of life for elders. “We are on the cusp of the health system starting to understand the importance of the living environment to sustain independence,” says Dr. Bruce Chernof, president and CEO of the SCAN Foundation, a California-based non-profit organization dedicated to transforming care for older adults.[expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Much of the failure to improve the quality of life of older people is really a failure to address their functional needs, explains Dr. Chernof, former Chair of the Commission of Long Term Care—a bi-partisan committee appointed by President Obama and members of Congress in 2013 to find comprehensive funding solutions for long-term care. He notes that people’s physical environment—where they live and the support services they receive—is often the biggest factor affecting their health and quality of life. “When the physical environment fails, that’s when they end up in the emergency room,” he says.

The intersection of seniors housing and care and the evolving health care system will be detailed by Dr. Chernof as keynote speaker at the NIC 2015 Capital & Business Strategies Forum, March 31- April 2, in San Diego. The presentation will be followed by a panel discussion among senior level industry leaders on Dr. Chernof’s observations.

Offering a preview of his NIC presentation, Dr. Chernof notes that housing and care providers have the tools to help people age in place, wherever they happen to live. “That is not what the medical system knows how to do,” he says. For example, seniors housing and care providers can act as an early warning system to help avoid hospital admissions and readmissions often with simple, low-cost interventions such as medication management.

Dr. Chernof will detail other points of convergence between the health system and seniors housing and care, including:

- Transparency. Housing and care providers will be involved in health outcomes by tracking data and making it available to medical groups, insurance companies and hospitals. Dr. Chernof proposes that shared data and outcomes should result in shared reimbursements with housing and care providers. “It’s a value proposition,” he says.

- Managed care. Risk-bearing organizations that provide payments will incorporate more social supports, such as community based services. Housing providers in particular could offer services outside their walls to prevent unnecessary medical care.

- Person-centered approaches. Medical and personal goals will be aligned. Instead of treating a series of ailments, medical providers will consider the person’s goals and then work to structure supports, including housing and care services, to meet those goals.

- The latest computer application or monitoring system may look intriguing, but Dr. Chernof asks: “Is there value?” Seniors housing and care providers can bring a dose of realism to the discussion since they work in a built environment that demands practical approaches.

Dr. Chernof challenges the notion that health systems are well acquainted with the wide array of services offered by housing and care providers. Housing and care providers can emerge as the champions of the elderly in the quality of life discussion, he says, and fill the void left by the medical system. He adds: “I would encourage the housing and care sector not to misread the shift taking place.” “There would be a number of years of shift and more opportunities to be part of a broader solution as providers re-imagine their role as a community resource.”[/expand][cresta-social-share]