CFG Keeps Calm and Carries On: A Conversation with Capital Funding Group’s Erik Howard

When other financing sources headed for the sidelines during the pandemic, Capital Funding Group (CFG) stayed the course. The long-time healthcare lender continued to support its borrowers through this difficult time and, in fact, has had one of its most successful years yet. NIC’s Senior Principal Bill Kauffman recently talked with CFG’s Executive Managing Director Erik Howard about the company’s growth strategy and the outlook for buyers and sellers. As Howard says: “We try to identify and do business with good operators and support them any way we can.”

When other financing sources headed for the sidelines during the pandemic, Capital Funding Group (CFG) stayed the course. The long-time healthcare lender continued to support its borrowers through this difficult time and, in fact, has had one of its most successful years yet. NIC’s Senior Principal Bill Kauffman recently talked with CFG’s Executive Managing Director Erik Howard about the company’s growth strategy and the outlook for buyers and sellers. As Howard says: “We try to identify and do business with good operators and support them any way we can.”

Kauffman: Erik, can you please tell us about yourself and your position at CFG?

Howard: I’m the executive managing director of business development and marketing for our healthcare business. This is my 17th anniversary with the company. CFG has continued to grow over the last 18 months by supporting the sector through the pandemic. My role is to provide the general direction of our dedicated business development team of 10 to 15 individuals who work on day-to-day transactions. I also work on various capital plans that involve CFG Bank, as well as CFG Credit Partners.

Kauffman: What products do you offer, and what are you best known for in terms of providing capital to private pay senior housing and skilled nursing?

Howard: We provide one-stop shop financing solutions for our clients. Very simply, we say, if you need capital, we have it. This started many years ago with our core HUD business. We are one of HUD’s largest healthcare lenders. CFG has closed $2.3 billion in bridge-to-HUD financings and $536 million of HUD financings already in 2021. In the late 1990s, we grew our bridge loan business surrounded by other product types, including accounts receivables financing for long-term care, and mezzanine and subordinate debt financing. We offer a traditional suite of commercial bank products through CFG Bank, which we bought in 2009. We offer equity-type capital as well, where we partner with owners and operators to buy assets with strategic purchase price options. We launched a new program – CFG Credit Partners – last year for off-balance sheet financing. What we’re really known for is our creativity, flexibility, and ability to show up for the industry. Our word and reputation are the gold standard in the sector. When we say we are going to get something done, we get it done.

Kauffman: How much capital are you allocating to lending in senior housing and skilled nursing?

Howard: We don’t have an allocation like other institutions. Over the past year, when so many lenders sat on the sidelines, we took a different approach to support the senior housing and skilled nursing sectors, knowing that our borrowers and partners needed capital. We did this during the financial crisis and at other times, too. When unfortunate events happen, we try to support the industry. Going into 2020, we probably wouldn’t have thought that we would deploy over $3 billion last year, but we were happy to do it; and we’re already approaching $3 billion this year. Our unique ownership structure provides us the flexibility to make strategic decisions that other groups may not be able to make – and do so more quickly. In times of crisis, the industry needs decisiveness and leadership – we provided both. We have a saying: We try to identify and do business with good operators and support them any way we can.

Kauffman: How has the pandemic impacted your business? What changes have you made due to the pandemic when it comes to your business?

Howard: We’re grateful to have the trust and support of borrowers through such a challenging time. It reinforced our recognition that the industry was almost too big to fail because of where it fits in the healthcare continuum. The operators, owners, and staff have done such a terrific job, showing the world the need for an industry that typically doesn’t get good news stories written about it. We saw healthcare heroes get the recognition for the challenges they face every day. We knew we would get through this because of them. In terms of underwriting, we’ve stuck to the basics, looking at well-capitalized operators with some longevity in the industry that knew how to navigate this challenge with a good partner like CFG.

Kauffman: What do you see as the biggest difference between 2020 and 2021 thus far?

Howard: The number of deals has started to slow in the back half of 2021. The first half of 2020 was comprised of residual 2019 deals that had stalled because of the pandemic. We saw some acceleration in transactions in the back half of 2020 which worked its way through 2021. Several factors were involved. Some large national firms divested their portfolios. Also, the sophistication and complexity required to care for medically complex residents in seniors housing and skilled nursing facilities has been challenging for smaller operators. Then, going into the pandemic, the industry had only experienced one quarter with Medicare’s new Patient Driven Payment Model (PDPM). The changes and complexity of that brought about some consolidation. Operators thinking about exiting the skilled nursing sector because of PDPM then had to deal with COVID-19. It was a one-two punch.

We have continued to see consolidation with good, well-capitalized operators in the long-term care space into 2021. We’ve executed some mega-deals, as well. We have now financed four deals in excess of $250 million in the last nine months. In July, we closed a bridge-to-HUD loan in excess of $650 million, representing the largest single financing deal CFG has executed in 10 years. However, the $30 million to $50 million deals with 5 to 10 assets have slowed.

Interestingly enough, we have not seen a decline in prices. I think that’s because coming into 2020, the skilled nursing sector was in one of the best positions it had been in for 15 years. If it weren’t for the pandemic, the trajectory of the long-term care market would have been tremendous with continuous acceleration in pricing as more capital came into the sector. While sellers in 2021 wanted to get out for various reasons, another cohort of potential sellers thought the price might be impacted by low occupancies and other factors. This recent pause is more a function of sellers waiting for occupancies to pick back up to get a higher price. We expect to see more deals in 2022. Buyers have capital, and they’re still bullish.

Kauffman: What is your view on valuations in both private pay senior housing and skilled nursing?

Howard: One of the biggest factors that will weigh on all of this is staffing. It’s been an age-old problem for the industry, and the vaccine mandates that have been put in place could be a factor in slowing growth in valuations by further increasing the shortage of staffing nationwide. If we continue to have to redline staffing to cut expenses, it could slow what would otherwise be the normal course growth in per-unit and per-bed value on a go-forward basis. There are staffing initiatives under way. We launched The Jack and Nancy Dwyer Workforce Development Center, Inc., a first-of-its-kind, nonprofit program that provides CNA (Certified Nursing Assistant) and GNA (Geriatric Nursing Assistant) job training, job placement, wraparound services, and case management to unemployed and underemployed individuals who aspire to have a career in the healthcare industry. The program launched first in Baltimore, where CFG is headquartered. We’re trying to help the industry move forward and support it in any way we can.

We’ll see slow growth in valuations until COVID-19 is further in the rear-view mirror as long as we don’t have challenges with new variants. If rates remain low, I don’t see a negative trend in valuations. We expect to see moderate growth in the next 6 to 12 months and then possibly some acceleration after that. The occupancy recovery will play a big part in that. When the market starts to improve and feel better about senior living – because we’ve done a good job handling the pandemic, getting people vaccinated and increasing occupancy – we’ll see more acceleration.

Kauffman: In terms of the transactions market overall, what are you seeing that is most noticeable and also what might readers not know about the markets right now?

Howard: We continue to see larger players diversifying on the publicly traded REIT side and consolidation among certain operators. We think consolidation will continue in the skilled nursing and senior housing sectors as operators encounter the challenging health complexities of their residents. While new construction has slowed, we’re bullish on the senior housing sector looking out beyond the pandemic. We like good sponsors in good markets. We have a number of senior housing construction loans in the pipeline, totaling in excess of $250 million. We’re excited about that.

One overarching theme over the last 18 months is the continued partnership of the industry with HUD. The agency has really helped borrowers in a number of ways and has used creativity – with our input – to provide liquidity. We think the supplemental HUD 241 loan program will be useful to improve the physical plant at long-term care and older senior housing buildings. The program provides an opportunity for existing borrowers to finance renovations, additions, and equipment purchases. The rates are extremely low at 2.25% today with a loan-to-cost ratio of up to a 90%. The amortization period is the unexpired amortization period of the primary loan. It’s a little-known financing vehicle that can be extremely beneficial.

Kauffman: What are you hearing right now from the operators you work with? What are the main challenges, and how are they dealing with them?

Howard: Staffing continues to be the focus. One of the things we’re trying to do is to create healthcare field awareness in partnerships with hospital and university systems, highlighting what it’s like to work in the long-term care and seniors housing sectors. What are the myths? What are the facts? We can’t buy our way out of this problem with higher pay. There is some discussion in Washington, D.C. about minimum staffing levels and mandates, and hopefully that would be accompanied by higher rental rates. Operators would love to have more staff, but it becomes a matter of how to pay for more staff. The pandemic has shown us that we need to take a collaborative approach with CMS to provide some incremental dollars for the sector to hire more staff. The residents would benefit in the end, and that’s everybody’s goal.

Kauffman: Is there anything else you would like the readers to know about CFG?

Howard: CFG continues to be on the cutting edge with new products and ways to provide flexible financing options and capital to long-term care and senior housing owners and operators. We anticipate launching a senior housing credit fund toward the end of the year that will propel us further into the sector. One of the things about our company that has been so important is our longevity and entrepreneurial attitude that supports everything we do. We’ve been a bellwether for over 25 years and showed that during the pandemic, when other groups were on the sidelines, we were there to help the industry. We will move forward, executing good loans with good partners and will continue to grow our platform.

Top Economists to Weigh in at NIC Fall Conference: A Preview of the Economic Outlook and its Impact on the Industry

Two of the nation’s most influential economic thinkers, Paul Krugman and Lawrence H. Summers, will face-off in person at this year’s NIC Fall Conference. Both have strong, often differing, opinions about the economy and the path forward. The lively discussion will be moderated by Angela Mago, president, Key Commercial Bank & KeyBank Real Estate Capital.

Krugman is a Nobel Prize winning economist and professor emeritus of Princeton University’s Woodrow Wilson School. Summers is the former Secretary of the U.S. Treasury and president of Harvard University and served in many U.S. executive branch administrations.

To provide context for the upcoming discussion with Krugman and Summers, NIC’s chief economist, Beth Mace, recaps the big issues driving the economy, and talks with Angela Mago on why the issue matters and what to expect to learn at the upcoming Fall Conference session.

Growth Outlook

As of the second quarter, real GDP in the U.S. had surpassed its pre-pandemic level, rising at a fast 6.7% annualized clip. That is great news. That said, growth is likely to be much slower in the coming months as the vast pandemic-related fiscal stimulus starts to wane, pent-up demand begins to fade, and as the COVID-19 delta variant takes its toll.

Mace: I think it’s fair to say Krugman and Summers will have broad views on the shape of the post-pandemic recovery. As a banker, why is the growth path of the U.S. economy important to consider?

Mago: The path of growth matters because a healthy economy adds jobs, raises the standard of living, and increases our ability to invest in new technology. Healthy growth is good all around. For banking, the system has a lot of liquidity because of the pandemic. Companies and consumers are sitting on a lot of cash. Borrowing rates on lines of credit are at all-time lows. That impacts the banks’ net interest margins and net interest income. We’d like to see a return to healthy growth and normal borrowing to absorb some of the liquidity.

Inflation: Yes, No, or Maybe?

Inflation had been a non-topic for a very long time, and, during the recovery from the Great Financial Crisis, in fact, disinflation was a worry of policymakers. Since the recovery from the pandemic has begun, however, inflation has increased due to supply chain disruptions and reopening effects. The policy question has become whether this inflation growth is transitory or will become more permanently embedded in consumer and business expectations.

Mace: The inflation discussion by Messrs. Summers and Krugman will be fascinating. As someone who has been involved with the senior housing sector for a long time, why do you as a banker care about inflation? Why does this debate and the desire to contain inflation matter to senior housing and care owners, operators, and developers? What stake do they have in this issue, and why?

Mago: Healthy growth and healthy inflation have benefits. But it becomes a problem for consumers when the cost of goods and services outpaces wage growth, or for companies when the cost of goods sold rises faster than their ability to increase prices and grow revenue. That causes margin compression and erosion. Companies may not be able to cover fixed charges or invest in continued growth and job creation. So that’s why we care about it. In the senior housing and care space, the biggest cost is labor. The cost of debt, insurance, and food are also big factors. There is often a lag effect for senior housing and care operators. They are dealing with near-term pressure on expenses but a lag in terms of their ability to recoup costs through higher rents or increased reimbursements. Good inflation is a good thing, but when it gets out of control, it can push the economy in the wrong direction. Right now, it feels like there is lots of inflationary pressure. But when we study the data, it could be temporary in nature. We’ll find out in the months ahead which is correct.

Higher Fixed Incomes

Inflation can help senior housing residents and nursing care patients. Since the cost-of-living adjustment (COLA) for Social Security participants is tied to the rate of consumer price inflation (CPI-W), a higher inflation rate can translate into an increase in their monthly government checks. For example, based on the change in the CPI-W between the third quarter of 2019 and 2020, Social Security recipients saw a 1.3% COLA adjustment for 2021. For 2022, this may be higher. For example, the 12-month change in the overall CPI Index was 5.3% in August. The actual change will depend on changes in prices between July and the end of September.

Mace: Do you think Social Security beneficiaries will get a big increase?

Mago: I think you will see a nice windfall in 2022, maybe the best since 2009. But, again, there is a lagging effect. People are dealing with increased prices today for housing, gas, and food.

Labor Pains

The U.S. unemployment rate stood at 5.2% in August, 1.7 percentage points above the pre-pandemic level of 3.5% seen in February 2020, but well below the 14.7% peak seen in April 2020. Meanwhile, the Labor Department reported that nonfarm payrolls rose by 235,000 in August 2021. Employment is now up by 17.0 million since April 2020 but is down by 5.3 million or 3.5% from its pre-pandemic level in February 2020. Increasingly, we hear from employers of all industries, and importantly, seniors housing and nursing care are among these industries, that finding workers is a limiting factor to business expansion. Certainly, one part of the discussion on labor shortages is around what is causing so many low wage workers to stay out of the labor force now. Factors include extended unemployment benefits; kids still at home who need care; fear of dangerous working conditions from exposure to COVID in the workplace, fear of vaccines; and the desire to find a better job with higher wages, more benefits (sick leave), or a career path.

Mace: What do you think is causing the labor market shortages? And what are you hearing from your borrowers about the root cause of these shortages? More broadly, do you think labor shortages are a short-term or longer-term concern?

Mago: As your overview indicates, it’s probably a combination of many things. All of our borrowers, regardless of their industry, say that labor is their number one concern, full stop. That and the supply chain disruption. But labor is a huge issue. One client, not in seniors housing, but in a space where labor is a concern says it’s the worst it’s been in 30 years. Companies feel that supplemental unemployment benefits, which will be ending, are keeping people out of the applicant pool. We’ll have to look at the data on that to prove it out. But seniors housing and care has its own challenges. It has always been a space where labor has been a challenge, and there has always been high turnover. The preponderance of care workers are women, and we know women were disproportionately negatively impacted during the pandemic. They fell out of the workforce to care for children, and that’s still a real issue. The other reality is that if you have an opportunity to find a job in a sector that is going to pay you better, you have some flexibility today. Care workers are worried about COVID. There is some fear about vaccines too. Vaccine mandates by operators to protect residents may impact the ability to attract talent. There are a multitude of factors causing the labor shortage. Operators have to get creative to recruit and retain workers.

Mace: Immigration reform could be a big solution longer-term. The working population is shrinking compared to the non-working population. The workforce of those ages 18-64 is supporting more and more people as the number of older people grows. The labor issue is not going away.

Mago: Considering the demographic shifts underway, I agree that the labor issue is not going away. It’s a good question for Messrs. Krugman and Summers.

Interest Rate Debate

Federal Reserve Chairman Jerome Powell recently said that interest rate hikes are not on the Fed’s radar for now. That has poured some cold water on the idea of rate hikes as soon as 2022. But the markets and some of the Federal Reserve Board members may not agree with the pace and timing of expected interest rate increases.

Mace: As a banker, how do you feel about the prospect of higher interest rates, and what advice would you give your clients on when and what type of debt they should secure?

Mago: I think you have to pay attention to what the Fed is doing on short-term interest rates and tapering bond purchases. That will have an impact on long-term rates. We are in a global economy, and whenever there’s a flight to quality for whatever reason, long-term rates are impacted. The delta variant is definitely having an impact on rates. We went into the year thinking we would start to see long-term rates rise, but the opposite happened because of the emergence of the delta variant. I tell borrowers that it’s a great time to be a borrower. A lot of capital is available, and rates are low. If you can lock in long-term rates in the low- to mid-3% range, you should do it all day long. If you need more flexibility, short-term rates are low by historical standards as well. I don’t have a crystal ball; we’ll have to watch all these factors. But our expectation is that as the economy starts to improve, we should see rates rise.

Mace: The Secured Overnight Financing Rate (SOFR) is the interest rate benchmark replacing the London Interbank Offered Rate (LIBOR). Are you using the SOFR?

Mago: Our senior housing group has been quoting SOFR since the first half of 2021. The entire bank is not there yet, but it will be using SOFR no later than January 1, 2022. The big agency lenders—Fannie Mae and Freddie Mac—started using SOFR for their floating rate loans beginning in September 2020. The industry followed quickly. We did not have a struggle with uptake in the real estate spaces unlike the general commercial and industrial sectors which have been slower to adopt SOFR. Now that the Alternative Reference Rates Committee has formally recommended the CME Group’s Term SOFR rates, we should see more adoption. There are also credit sensitive indexes such as BSBY being quoted by some lenders as an alternative to SOFR. We expect to see more clarity around this as banks prepare to cease quoting LIBOR by January 1.

Send Us Your Questions

Mace: What other topics do you expect to address with these two very interesting and well-informed policy wonks?

Mago: The size of the infrastructure and budget package has created a lot of debate. Are we spending too much? Or the right amount? I’d like to hear their opinions. I’d also welcome NIC readers to send questions they’d like addressed during the session. What topics do the industry stakeholders want to hear about?

Let us know. Click on this link, and send us your questions.

Executive Survey Insights Wave 32: 8/9/2021 - 9/6/2021 By Lana Peck

NIC’s Executive Survey of operators in senior housing and skilled nursing is designed to deliver transparency into market fundamentals in the senior housing and care space as market conditions continue to change. This Wave 32 survey includes responses collected August 9 to September 6, 2021, from owners and executives of 92 small, medium, and large senior housing and skilled nursing operators from across the nation, representing hundreds of buildings and thousands of units across respondents’ portfolios of properties.

Detailed reports for each “wave” of the survey and a PDF of the report charts can be found on the NIC COVID-19 Resource Center webpage under Executive Survey Insights.

Wave 32 Summary of Insights and Findings

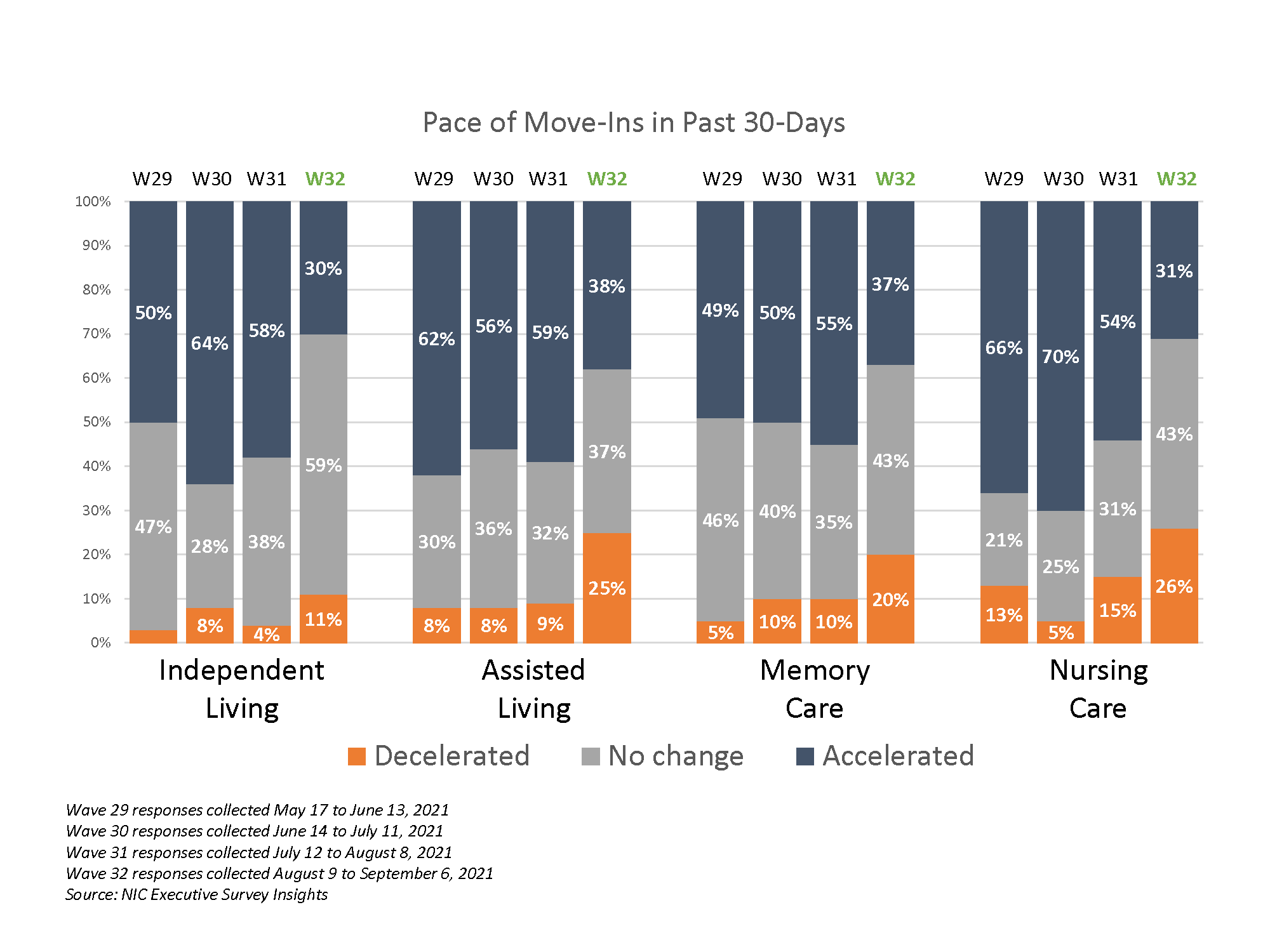

- As shown in the timeline below, across the survey time series from March 24, 2020 to September 6, 2021, the Executive Survey Insights results have shown clear trends that have corresponded with the broad incidence of COVID-19 infection cases in the United States. By Wave 18 (in the latter half of December), the COVID-19 vaccine had begun to be distributed across the country through the Long-Term Care Vaccination Program and more and more respondents noted that the pace of move-ins accelerated for the most part from Wave 19 through Wave 31. In Wave 32, the shares of organizations reporting an acceleration in the pace of move-ins in the past 30-days dropped notably, possibly due to due to the spread of the COVID-19 delta variant primarily among the unvaccinated.

- Between roughly 30% and 40% of organizations report that the pace of move-ins accelerated in the past 30-days—compared to roughly 55% and 60% in Wave 31. Of note, about one-quarter of organizations with assisted living units and/or nursing care beds, and about one in five with memory care units reported a deceleration in the pace of move-ins. However, more than half (59%) of organizations with independent living residences reported no change in the pace of move-ins.

- In Wave 32, between roughly 45% and 55% of organizations with independent living, assisted living and/or memory care units reported an increase in occupancy across their portfolios of properties in the past 30-days. However, only about one-third (32%) saw an increase in nursing care occupancy. This is down significantly from Wave 30 (6/14 to 7/11) when three-quarters of organizations with nursing care beds saw occupancy increases in the 30-days prior (76%).

- Indeed, across the four care segments, nursing care occupancy has taken a jolt with nearly 40% of organizations indicating that occupancy declined across their portfolios of properties in Wave 32 (and about 20% reported a decline in occupancy of 3 percentage points or more).

- The chart below shows the shares of organizations with nursing care beds that saw an increase, decrease, or no change in occupancy across their portfolio of properties in the past 30-days, across 32 waves of survey data since near the beginning of the pandemic.

- The shares of organizations with nursing care occupancy declines in the Waves 31 and 32 surveys show a similar trend compared to Waves 11 and 12 (August 17 to September 27, 2020) leading up to autumn’s surge in COVID-19 cases across the country. Whether the pattern of declining occupancy rates will continue or not is uncertain.

Wave 32 Survey Demographics

- Responses were collected between August 9 and September 6, 2021, from owners and executives of 92 senior housing and skilled nursing operators from across the nation. Owner/operators with 1 to 10 properties comprise roughly two-thirds (63%) of the sample. Operators with 11 to 25 properties and 26 properties or more make up 20% and 16% of the sample, respectively.

- Approximately one-half of respondents are exclusively for-profit providers (51%), more than one-third operate not-for-profit (37%), and 12% operate both.

- Many respondents in the sample report operating combinations of property types. Across their entire portfolios of properties, 66% of the organizations operate senior housing properties (IL, AL, MC), 23% operate nursing care properties, and 37% operate CCRCs (aka Life Plan Communities).

Referenced by The Wall Street Journal on August 31, 2021 (Senior Housing Industry Faces Higher Costs as It Plays Lead Role in Vaccine Mandates), NIC’s Executive Survey Insights continues to be closely watched by the media, and we ask for your continued support.

The current survey is available and takes less than ten minutes to complete. If you are an owner or C-suite executive of senior housing and care and have not received an email invitation to take the survey, please contact Lana Peck at lpeck@nic.org to be added to the list of survey recipients.

NIC wishes to thank survey respondents for their valuable input and continuing support for this effort to bring clarity and create a comprehensive and honest narrative in the seniors housing and care space at a time when trends are continuing to change in our sector.

Finding Purpose and Opportunity in Senior Living

Last month’s NIC Insider article entitled “A New Generation of Leaders” highlighted how NIC has been catalyzing new academic programs in top universities focusing on careers in senior living. As the industry continues to mature, it faces significant challenges, both immediately and in the years ahead. Major issues, such as the COVID-19 pandemic, workforce shortages, the aging of millions of baby boomers, shifting regulatory and policy landscapes, and the emerging need for lower cost solutions, are disrupting senior housing and care. Investors, operators, and other industry stakeholders will need a new generation of leaders with the tools, vision, and, in many cases, the entrepreneurial drive it will take to help overcome those challenges and seize the opportunities they offer.

Academic leaders have seen the potential of such careers for their students and are championing new programs designed to set them up for success. “We want to help develop that next generation of awesome senior living leadership,” said Dr. Nancy Swanger of the Granger Cobb Institute for Senior Living at Washington State University. But she also pointed out that there’s more demand for senior living graduates than current programs can produce. Referring to the many challenges facing the industry today, she emphasized the need for many more graduates than are currently being produced. She said, “We wouldn’t churn out enough graduates now to solve the problem, and, when you think about adding the demand from the baby boomers, it’s not there.”

The industry has plenty to offer these students, most of whom desire to enter a career that offers more than just a paycheck. According to Dr. Swanger, “For this generation of students, particularly the ‘Gen Z’ students, the oldest of whom is 25 right now, the kind of work they do matters. It has to be meaningful, purposeful work. It can’t be ‘just a job.’ This is also a generation that is very entrepreneurial. When you take those entrepreneurial desires and the desire for meaningful, purposeful work…wow, senior living is a perfect fit. You get to make a difference in the life of a real resident every single day. The industry marries two very important pieces to talent in that age group.”

While the ongoing partnership between NIC, academic leaders, and the business community has helped grow and shape new programs across the country, they are still very new. Some programs are so new that they’re just beginning to enroll their first students. Others have already helped to launch a few classes of graduate and undergraduate students into their careers. At many academic institutions, leaders within hospitality, gerontology, healthcare, business management, commercial real estate, and other related fields are beginning to consider adding senior living specialties to their programs.

Beyond raising funding for these new programs and bringing industry leaders into classrooms to help educate and inspire young people, academics face the challenge of overcoming the all-too-often negative impressions that many people have of ‘nursing homes.’ Xavier Aburto, who is currently a senior at Washington State University, first had to overcome his own negative impressions of the industry, which included the misperception that it’s not an industry worth considering for a career at all. “People don’t see senior communities as a business. They just have this perception of this being a negative thing.” He took his first senior living course this spring, taught by Dr. Swanger, despite having a few reservations. “At first I didn’t know what to expect. I thought this was going to be boring, probably. But I came to realize that it’s a whole new world,” he said.

Part of what helped Aburto change his mind on senior living was the influence of industry professionals who regularly share their stories and insights with Dr. Swanger’s students. “The best part of that class was that we had guest speakers every week. These are people who are in the business. They would talk to us for a whole hour and would give us all this information. This is their living; these people have a lot of experience. For me that was a huge highlight,” Aburto said.

Rachel Kelly also took her first senior living course as a senior, as part of her undergraduate degree program at the Cornell Institute for Healthy Futures, back in 2017. After graduating with a Bachelor of Science in Human Biology, Health & Society, with a minor in health policy analysis and management, Kelly opted to stay at Cornell for graduate school, where she enrolled in the new senior living program, run by Executive Director, Brooke Hollis. “Since taking Brooke’s class I’ve never looked back. I’m definitely staying in senior living,” she said.

Hollis was able to help connect Kelly with a network of people working in the industry. She secured an operations internship at Belmont Senior Living in Albany, California. There, she rotated through every department, gaining valuable practical experience, even as she completed her studies. After graduating in 2019, Kelly returned to Belmont, moving to San Francisco to start in the sales department. “I don’t know how I would have connected with Belmont without having been a part of Cornell and that network and been part of Brooke (Hollis)’s class,” she said.

Kelly has since transitioned to the operations side, where she is a senior administrative specialist. And she’s planning to explore her senior living career opportunities some more. “I’m really enjoying the operations side, … and I have my sights set on exploring the development side as well. I feel lucky to work for a company that has operations and development under one roof, so I’m looking forward to exploring that next in my career.”

Reflecting on her decision to commit to a career in senior living, Kelly credited the exposure to industry professionals at Cornell. “I was so moved by the passion that these professionals had to share with people who generally didn’t know much about their industry…it was really impactful. Every speaker had the same message,” she recalled: “Senior living offers the opportunity to do well by doing good. That hit on everything that I wanted out of a career. I was impressed by how much these people cared about the purpose they were serving – and was equally impressed by the financial returns they shared. That was a combination I couldn’t shake. I took two hours of this course, walked out for the night, and called my dad and said, ‘I know what I’m doing for the rest of my life; its senior living.’ It was just so impactful to feel like the stars finally aligned with an industry that could fuel my purpose-driven desires while also obtaining the business success that I wanted.”

NIC staff, members of NIC’s Future Leaders Council, and a number of industry leaders continue to give their time to address new students in several programs around the country. Student comments, collected by Swanger at the end of each course, illustrate how these speakers help them shed their misperceptions, find inspiration, and gain a passion for a career that they likely weren’t considering seriously at the beginning of the semester.

Each of the following comments is from a different student taking Swanger’s class last semester:

“It is extremely motivating to feel wanted by an industry, especially when these top tier professionals offer their contact information and willingness to have a conversation. Those types of presenters who you can feel the energy and love of what they’re doing rubs off and makes any career enticing, and that is what I felt from Bob (Kramer), Meg (Davidson), Holli (Korb), Bill (Pettit), and especially Tana (Gall).”

“He is not only knowledgeable about the field of senior living, but his enthusiasm for it transmits through his words and ideas. He helped me see this industry with different eyes and destroyed whatever erroneous perceptions I may have had prior to taking this class. Thus, I am very glad to have taken this course. I must admit that, at first, I had no idea what I was getting myself into, but, as I finish it, I see this industry with more humane eyes and can, certainly, visualize it as a future field of profession.”

“Bob Kramer left a lasting impression on me because he completely changed my opinion about senior living communities. I had always had negative feelings towards the senior living business, and, after his presentation in week one, I’ve had an open mind and may even consider a career in senior living on the HR side of the company.”

“His information not only complemented that week’s presented information but gave great insight into the business of senior living as a whole. Providing knowledge on the constant growth and opportunity the industry has to offer opened my eyes to looking further into pursuing a career in the senior living industry. I was most thankful to learn from Bob (Kramer) what the industry actually is and what senior living entails rather than my original perception going into the course.”

In addition to visiting classrooms, NIC helps students secure connections and internships, as another means to encourage careers for talented young leaders. Every year, NIC encourages the industry to offer paid internship programs, and helps match those programs with talent from some of the same academic institutions discussed above. NIC’s internship page can be found here. NIC also provides grants for select students to participate in the premier national events for the industry, the NIC Fall Conference and NIC Spring Conference. Nominations are submitted through the academic institution and awarded by NIC.

NIC also is among the sponsors for Vision 2025, an effort to amplify the growth and development of talent within senior care administration. The group focuses on helping to meet the demands of an ever-increasing senior population, with the goal of creating 25 robust university and college programs and 1,000 paid internships across the industry.

Key Points for Success Navigating Labor and Recruiting By Craig Ahlstrom – Chief Operating Officer, Avista Senior Living

A few years back (prior to the COVID 2020 pandemic), I attended a NIC conference where the keynote speaker displayed all the encouraging trendlines promoting an endless stream of opportunities in the senior living industry for the next 20 years. As an operator sitting in that conference, I remember feeling perplexed because day to day the staffing piece was so difficult to solve for, yet so many new entrants were sitting in that meeting salivating over the opportunity to get into the assisted living and memory care space and build more. I couldn’t help but wonder where all the team members would come from for all the new communities that were being proposed. I raised my hand at that time and asked this question. The presenter didn’t seem to know much about this portion of the business, sidestepped the question, and moved on. I was dissatisfied, but I understood that it’s not an easy problem to solve.

A few years back (prior to the COVID 2020 pandemic), I attended a NIC conference where the keynote speaker displayed all the encouraging trendlines promoting an endless stream of opportunities in the senior living industry for the next 20 years. As an operator sitting in that conference, I remember feeling perplexed because day to day the staffing piece was so difficult to solve for, yet so many new entrants were sitting in that meeting salivating over the opportunity to get into the assisted living and memory care space and build more. I couldn’t help but wonder where all the team members would come from for all the new communities that were being proposed. I raised my hand at that time and asked this question. The presenter didn’t seem to know much about this portion of the business, sidestepped the question, and moved on. I was dissatisfied, but I understood that it’s not an easy problem to solve.

When we are promoting the industry’s demographic trends of aging seniors, we should never lose sight of how critical it is to keep a focus on not only how we are going to recruit new residents but also how important it is to recruit team members to support their care.

Whether you are an owner, an operator, a lender, or an investor, staffing and recruiting during the past 18 months has been on your mind. No matter how great the upcoming demographic trends appear to be for our industry, taking care of those needing assistance will be a real struggle with a much more competitive, and what appears to be, a reduced workforce.

Avista Senior Living owns and/or operates roughly 1,200 beds across assisted living and memory care communities. We currently have roughly 850 team members that support the 13 communities we are involved with. In order to properly support the teams with hiring and recruiting, a member of our team at the home office works with the communities day to day identifying the jobs that need to be filled, posting ads for those jobs, and then making sure the teams get paired up with applicants that could be a great fit for that team and that position.

As we meet weekly to discuss jobs with our teams, we have recognized that the communities having the most success filling positions in this tough environment are doing some key things consistently. When these key actions are taken consistently, there have been fewer holes on the staffing schedule, dependency on outside staffing agencies have been reduced, and the morale of the teams onsite have improved. All of this has led to higher satisfaction with our great residents.

These key items for success in addressing staffing are listed below:

- There needs to be a daily focus on jobs by a point person at the community level. The communities having more success hiring and recruiting in this environment have a defined structure. There is no question as to who is following up with these potential candidates. When everyone on site assumes someone else will do it, progress is limited.

- Job postings should be creative and oftentimes may need to include hiring incentives. Know what your competitors are offering to employees, and make sure you stand out somehow. Too many times, we try to solve new problems with old, antiquated methods that don’t work. We must continuously be looking for ways to innovate and evolve if we want to be successful recruiting great team members.

- Work with urgency! Finding the right team members is life sustaining, like oxygen to the brain or water to the body! If a community goes a day without reviewing and following up with potential candidates, they are falling behind.

We are all engaged in one of the most important challenges of our day, which is to support an ever-increasing number of people as they age. The opportunities are all around us. It’s likely the companies that succeed over the next couple of decades will be those that consistently apply time and other resources to solving the labor and recruiting challenges.