Insurance Giant Sharpens Focus On Seniors Housing: A Conversation With Northwestern Mutual's Mike Dorsey

Mike Dorsey

Since the recession, the outsized investment returns of seniors housing haven’t gone unnoticed. New capital sources have been attracted to the sector not only because of its resilience during the downturn, but also by the prospects of a graying population that will need more seniors housing.

Those are two reasons why Northwestern Mutual, a relatively new capital provider to the sector, decided in 2014 to step up its investments in seniors housing.

NIC’s chief economist Beth Burnham Mace recently talked with Mike Dorsey, director of Northwestern Mutual Real Estate, Milwaukee, Wisconsin. What follows is a recap of their conversation with insights into the insurer’s lending objectives and why seniors housing is a shrewd long-term play.

Mace: Can you tell us about yourself and your role at Northwestern Mutual?

Dorsey: I have worked in real estate for 17 years, and I started at Northwestern Mutual in 2011. I’ve had a few different roles at Northwestern Mutual, but now I am a production director focused on the central U.S. All of our real estate investments are part of the General Account – the company’s $230 billion investment portfolio that is managed for the benefit of the 3.9 million policy-owners of our life insurance.

Mace: Can you explain more about how a life insurance company invests?

Dorsey: A well-established company like ours has a consistent flow of premiums coming in on new and existing life insurance policies. In addition, the General Account, which includes the majority of the company’s assets, constantly generates substantial investment income. To ensure that we will always be able to cover our liabilities, like paying claims, and return value to policyowners, usually in the form of a dividend, we have a large team of professionals investing these assets. We’re heavily invested in investment-grade fixed income, but the General Account also includes other asset classes that meaningfully enhance the portfolio’s returns. At the highest level, we’re divided into three investment teams: Public Investments, Private Investments, and the group I’m a part of, Real Estate.

Northwestern Mutual is one of the largest real estate investors in the nation, with commercial mortgages and equity investments across all major property types. Our real estate portfolio is valued at more than $43 billion.

Mace: What level of returns do you seek to generate on your investments?

Dorsey: Our popular life insurance products have a cash value that can’t go down, so we seek to achieve returns that compare attractively to high-quality fixed income. Our expected 2018 dividend payout is $5.3 billion.

Mace: How long has Northwestern Mutual been involved in the seniors housing and care sector? Why did the company enter into the space?

Dorsey: We’ve been active since the 1990s, though seniors housing was not a big focus, and we mostly chose to lend on independent living properties. In 2014, I was part of a group tasked with studying new areas in which to invest our time and effort, and ultimately our funds. We looked at a lot of different opportunities, and seniors housing emerged as the most interesting and viable option. Seniors housing had strong demographics, and we met a number of solid owners and operators. Since then, we have increased our national exposure to the product type. We’ve also become more comfortable pursuing opportunities in properties that have an assisted living and memory care component, as well as independent living.

Mace: Who is your typical customer?

Dorsey: Our typical borrowers are institutional investors such as pension funds, REITs, and high-net-worth family offices. Specific to seniors housing, we also have had some long-term successful relationships with regional owners/operators.

Mace: Why would a borrower choose Northwestern Mutual over other debt providers?

Dorsey: We offer attractive long-term fixed interest rates for lower leverage loans on high quality assets. As a large balance sheet lender, we have in-house legal and closing teams, and we service our own loans. Some of those services are not available from other debt sources. Our documentation and closing processes are very efficient, especially for repeat clients.

Mace: Do you provide debt financing to all seniors housing and care segments, which include independent living, assisted living, memory care, and skilled nursing care? For-profit and not-for-profit providers? Single-property and portfolio deals?

Dorsey: Everything we’ve done so far has been with for-profit providers. We don’t finance skilled nursing or CCRCs. We do finance both single-property and portfolio deals.

Mace: Do you have a property type preference within the different seniors housing segments?

Dorsey: Our preference is a property or portfolio that has a continuum of care. We are generally more comfortable with independent living and assisted living, since memory care is a more specialized business.

Mace: Do you provide debt for existing, stabilized purpose-built properties, for acquisitions, refinancings, construction and bridge loans?

Dorsey: We are focused on stabilized properties and provide loans for acquisition or refinancing on those. At this point, we do not offer construction financing. Given our investment horizon of five to ten years or longer, we do not offer bridge loans.

Mace: Are your operations national in scope, or are there areas of the country that you avoid?

Dorsey: We are national in scope. We tend to focus on the top 15-20 MSAs. We are headquartered in Milwaukee, however Northwestern Mutual Real Estate has several field offices throughout the country, including on both coasts. Our field offices originate loans and service our portfolio.

Mace: What is the volume of debt supported by Northwestern Mutual?

Dorsey: We do about $5 billion of mortgage production a year. Seniors housing is small percentage of that, but there’s room to grow.

Mace: What do you look for in a good sponsor?

Dorsey: We choose sponsors based on their track record, and we especially like to see dedication to the seniors housing industry. We want the operator to have an ownership stake in the property, even if it is a small position. We typically work with operators that have a long track record of success in the industry. More sponsors are emerging that are run by seniors housing veterans and are backed by pension fund money. We like that.

Mace: What are your standard terms?

Dorsey: We are a lower leverage lender with a maximum loan-to-value ratio of 60 to 65 percent. All of our loans are fixed rate with a term of five years or longer, with a preference of 7-10 year terms. We are focused on larger deals of at least $20 million in size per loan.

Mace: When do you turn down opportunities? Are there any immediate red flags?

Dorsey: Most of the opportunities we turn down are due to higher leverage, smaller deals or market size, or lack of stabilized operating history.

Mace: What do you like about the seniors housing and care sectors? What makes you worried?

Dorsey: We like the demographics. They will provide a huge tailwind to the industry over the coming years. As a lender, we like the fact that the sector is drawing attention from smart people and those people tend to be our borrowers. All the attention the industry is getting has positives and negatives. Obviously, the positives are that the industry is producing a higher quality product and more market data. The main negative right now is more supply which could be a challenge in the short term. But as a long-term lender, we focus on what the situation will look like when our loan matures, and that’s when the demographics will start to kick in. Another concern shared by many is the availability and cost of labor, especially considering that this sector is more labor intensive than other property types we invest in. We will continue to keep a close eye on that as we evaluate opportunities.

Mace: Any sense of where pricing is headed? Will valuations be affected by a higher interest rate environment?

Dorsey: As a lender, higher interest rates provide us a stronger return, but it can stress our deals. So I would like to see rates go up in a moderate, orderly fashion. On pricing, rising interest rates will have an upward impact on cap rates. But we continue to see new institutional interest in the sector, which has a downward impact on cap rates. So if I had to guess, I would say those two factors roughly balance each other out, and we expect fairly steady, flat valuations.

Mace: Anything else we should know about Northwestern Mutual as a lender?

Dorsey: As a mutual life insurance company, in contrast with many public companies, we have a long-term time horizon, so we can lock in fixed interest rates for 10 to 15 years or longer. We consider ourselves a partner with the borrower.

We cover the market geographically. We have 15-20 producers—myself and my colleagues—who are the front-line investment producers and points of contact. So if I am the producer on a loan, I will be the point of contact for any servicing request throughout the life of that loan. That is unique relative to other sources of debt.

Mace: Any other thoughts you would like to share

Dorsey: I’m a proud Northwestern Mutual employee. As a company, we help millions of clients pursue and achieve financial security. We also have a wonderful charitable foundation that gives back by funding childhood cancer research. It’s a great company, and we’re pleased about the progress we’re making in the seniors housing sector.

Newer Seniors Housing Pros Step Up At NIC Boot Camp: Registration Is Now Open

Brandi Healey

Ryan Chase

Seniors housing isn’t quite like other commercial real estate investments. Returns and valuations are affected by operational performance which makes investment decisions more complex.

While professionals new to the industry can find the deal-making process difficult to dissect, they’ll get a leg up at the 2018 NIC Seniors Housing Boot Camp. The program—The Art of Assessing the Deal—will be held Wednesday, October 17 from 10 a.m. to 2 p.m. at the Hyatt Centric Chicago.

Designed for professionals with 1-3 years of seniors housing experience, the Seniors Housing Boot Camp is structured around a real acquisition case study. Participants will learn from experts how to evaluate a prospective transaction and then formulate a bid on a property. The actual outcome of the case study will be revealed at the end of the program.

The Seniors Housing Boot Camp is sponsored by NIC’s Future Leaders Council. The event is co-chaired by Council members Brandi Healey and Ryan Chase.

“Boot Camp is an interactive workshop for professionals looking to familiarize themselves with the unique aspects of investing in seniors housing,” said Healey, vice president, asset management, Sabra Health Care REIT, Irvine, California.

Chase added: “Individuals with deal-making experience in other sectors will gain a lot of knowledge by analyzing a real seniors housing deal with the input of talented industry veterans.” Chase is managing director, Blueprint Healthcare Real Estate Advisors, Chicago, Illinois.

Back by popular demand for a third year, the Boot Camp is being held as a stand-alone and expanded event for the first time this year. It was previously held in conjunction with the NIC’s Fall Conference. (The 2018 NIC Fall Conference is being held Oct. 17-20 at the Sheraton Grand Chicago.)

Learn from veterans

In advance of the Boot Camp, the registered participants receive the case study outlining the key characteristics of an acquisition opportunity.

During the morning session, experts detail how to analyze a seniors housing investment opportunity. Topics include:

- Supply and demand/market dynamics

- Occupancy

- Operational performance

- Net income

- Rents

- Cost of care

- Staffing

The information is used by participants in small teams to develop a bid for the property. Each group is guided by a table captain, a member of NIC’s Future Leaders Council.

“Participants will learn how to use tools such as the NIC MAP® Data Service which can be applied to future opportunities,” said Healey.

This year’s expanded Boot Camp program features several notable changes.

Industry pioneer Bob Kramer is the keynote luncheon speaker. As NIC’s founder and strategic advisor, Kramer will provide keen insights into the trends impacting the industry, including the growing importance of healthcare and technology. “Bob will be a highlight of the Boot Camp. He’s an incredible resource,” said Healey.

Another twist this year is an analysis of the case study during a Q&A session with two veteran seniors housing operators led by Ben Firestone, founding partner and senior managing director at Blueprint Healthcare. Each operator—one national and one regional—will offer a different perspective. “It’s an opportunity to hear two experts with hands-on experience detail how they make acquisition decisions,” said Chase. “It will be a dialogue-driven discussion.”

About 60 participants are expected at the Boot Camp. Attendance is limited in order to ensure enough time for questions and answers.

Towards the end of the program, teams present their property bids along with the rationale for their offers. “We want to get feedback on what they were thinking,” said Chase.

The results of the actual deal are then discussed so participants can judge their work against the real outcome. “It’s a chance to walk a deal from start to finish,” said Chase. “It’s also a great opportunity to network and get to know your fellow future industry leaders.”

“The Boot Camp is unique in the industry,” noted Healey. “This is a rare opportunity for those new to the sector to hear industry experts discuss how to invest in seniors housing.”

Registration is now open for the 2018 NIC Seniors Housing Boot Camp. (click here to register)

2018 NIC Talks: How Am I Changing The Future of Aging?

Fall Conference NIC Talks Speakers

At the 2018 NIC Fall Conference, the highly popular NIC Talks series returns with eight speakers, representing outside experts and an industry leader, who will all address the theme of “How am I Changing the Future of Aging?” These 12-minute TED-style talks are designed to be insightful as well as thought provoking and perhaps challenge people’s perspectives on the future of aging. In last month’s NIC Insider, we highlighted four of this year’s speakers. This month, we introduce you to two more upcoming NIC Talks speakers. Look for next month’s Insider to read about our final two featured NIC Talks speakers at the 2018 Fall Conference.

Lisa Marsh Ryerson

What Did You Do Today?

Lisa Marsh Ryerson will focus on the value of socialization as well as the impacts and threats of isolation and loneliness. Drawing on her experience as the president of AARP Foundation, which works to end senior poverty, Ryerson has a message: In the future, senior living residents will be known not just for what they did but also for what they are currently doing. She will illustrate how the paradigm is shifting from the needs of past generations focused on safety, security, and comfort to that of a new generation that calls for engagement, connection, and purpose. Ryerson’s work with the highly regarded Connect2Affect initiative indicates that, beyond adapting to shifting attitudes, investors, owners, and operators stand to gain significant benefits by providing social engagement for tomorrow’s seniors.

Susan Dentzer

Healthcare Without Walls

Bringing healthcare to where seniors live is the focus of Susan Dentzer’s NIC Talk. As the President and CEO of the Network for Excellence in Health Innovation, Dentzer seeks innovations in improving health and healthcare at sustainable costs. She will present “Healthcare Without Walls,” in which providers collaborate, both upstream and downstream, to bring healthcare to seniors where they live. Her talk will highlight what needs to happen to bend the cost curve and achieve better outcomes, while pointing to the most promising areas for reform and innovation. Social determinants of health, such as loneliness, depression, food insecurity, transportation, housing, and behavioral health will be highlighted as critical considerations of senior living.

To learn more about the NIC Talks, please visit the NIC Fall Conference website.

How To Unlock The Mystery of Valuations: Panelists Preview Timely NIC Fall Conference Session

Valuations can seem baffling today. Property values have remained relatively steady despite declining occupancies. A panel of experts will detail the current dynamics of property valuations at the 2018 NIC Fall Conference. The session is titled, “What’s It Really Worth?”

Panel moderator Steve Monroe, editor, The Senior Care Investor, recently previewed the session with the panelists: Charles Bissell, managing director, JLL Valuation & Advisory Services; Chris Claps, managing director & principal, Locust Point Capital; and Bill Kauffman, senior principal, NIC.

What follows is a transcript of their comments, edited for clarity.

Monroe: Thank you for joining me today in the lead up to the 2018 NIC Fall Conference. Let’s start with a basic question. Why are accurate valuations so important in today’s market?

Bissell: Accurate valuations are important because they set the basis for many transactions. If properties are undervalued, then the appropriate level of capital is not available to the owners. And if properties are overvalued, there is the danger of distress and foreclosure and other issues that may give the industry as a whole a black eye, which can cause a wide variety of issues.

Monroe: We’ve seen overvaluations more frequently in the last couple of years, and we’ve seen what’s happened in the capital markets as properties are traded. Do you think the higher valuations of the last few years were a mistake?

Claps: I think that we’re deep into a growth cycle here, and people have made projections going forward that may have been overly aggressive. I think some of the inputs may have been too optimistic, resulting in a re-valuation of equity returns. What you’ve seen in retrospect is that certain transactions were overvalued.

Monroe: Should there be sub-specialties within the seniors housing and care valuation sector? Do we need specialists in skilled nursing, seniors housing, and CCRCs?

Kauffman: I think it certainly makes sense to have sector expertise. From the skilled nursing perspective, there’s been a lot of rapid change over the last few years, as far as the payment structures and obviously the whole transformation in the healthcare industry in general. We’re going to have another payment model introduced, likely in October 2019. So, when you throw that dynamic into the equation, it will certainly begin to affect valuations. So yes, I think you want to have the proper expertise when valuing skilled nursing facilities.

Monroe: Charlie (Bissell), in your practice, are there valuation experts who spend more of their time on the skilled nursing sector versus the CCRC sector because of that needed expertise in markets that are getting more complicated every year?

Bissell: Yes, the big seniors housing valuation firms have specialists, and one or more people will focus in a certain area. Typically, there will be somebody who is a CCRC expert, as CCRCs are one of the most complex properties that can be valued. There are just so many nuances to them.

Monroe: But people think that skilled nursing and seniors housing are so different. And the buyer pool usually does not overlap very much. But they’re both being impacted by two major, similar headwinds: labor costs rising and occupancy levels falling. Do these headwinds have a different impact on the two distinct sectors from a valuation perspective?

Claps: From a valuation perspective, both seniors housing and skilled nursing facilities are high fixed-cost businesses, and both are subject to some of the same headwinds that impact both the numerator and denominator of the cap rate calculation. But we haven’t seen significant recent changes in cap rates that we feel are related to potential occupancy or labor issues. Personally, I think the labor and occupancy issues vary greatly across geographic markets, and perhaps the more significant generalized risk is capital markets risk, which I think would disproportionally impact seniors housing assets.

Bissell: I’d say the impact varies by market. In some markets, you do see labor rates going up at or above the rate of inflation. And in some markets, it’s due to supply and demand imbalances. We’ve just added more supply in some markets than was warranted in a short period of time, and that’s led to increased competition between facilities for not only residents but also increased competition for staffing.

Kauffman: When we’re talking about skilled nursing and seniors housing valuations and transactions, I think we need to certainly talk about the data. When I looked at recent data, we have seen the price per bed for skilled nursing come down over the last 18 months, likely reflecting pressures in the sector. But on the seniors housing side, we really haven’t seen what you would expect to see in terms of a potential pricing adjustment or valuation adjustment in the transaction market.

Monroe: So, when we’re in a period of operating disruption or financial disruption for some, what is the most difficult part of valuing a property, whether it’s a skilled nursing facility or seniors housing property?

Kauffman: If we are talking about operating or financial disruptions, how do you determine the effects of supply coming online for seniors housing? Sure, you can dig into the data and make projections from the supply pipeline, but how is that really going to impact your pro forma, especially over a 7-10-year time horizon? I want to ask, are the next 7-10 years going to look like the last five years? I think from a valuation perspective, that’s pretty tough to think about.

Monroe: Chris (Claps), what’s the biggest or most frequent mistake that investors make when valuing a property or portfolio that they’re buying?

Claps: I think the biggest mistake that we’re seeing in requests for financing are investors who do what I call misapplying cap rate data. For example, taking headline transactions, which are often larger, and often times hospitality-based seniors housing facilities, and then applying those cap rates to facilities that we wouldn’t consider comparable. Whether they’re smaller or more care intensive or in less desirable markets, applying those lower cap rates to their projected exits can be a mistake.

Bissell: The things we see, first of all, are on the occupancy side. If you’re in a saturated market and the markets going to be saturated for 3-5 years, it’s probably not reasonable to forecast that occupancy is going to increase to 95% and stay there. If you’re in that type of market, it’s not reasonable to expect you’re going to increase rents by 3% to 4% a year. And it’s not reasonable to expect that you’re going to see your expense ratio diminish. Other areas where we see issues are property taxes. Those will tend to increase following a sale or even a financing, and a lot of buyers do not recognize that. And as residents age in place and require more care, we see many pro formas where the revenue is growing at a pretty good pace on the care side, but the expense side has not grown accordingly to provide that staffing. And, I would say that many purchases now are being made based upon the expectation that, in 2026, as the boomers start turning 80, there’s going to be above-inflation rate increases in revenue. And there also is possibly going to be cap rate compression.

Monroe: That’s a good segue into the next question. How relevant are forecasts today in a valuation? No one really knows what’s going to happen with labor costs and supply, occupancy levels, or in changing demands from the baby boomers. But on the skilled nursing side, isn’t it almost easier, for example, with relatively steady increases in Medicaid rates?

Kauffman: Yes, I think this goes back to the history conversation, right? I think some of us have seen the charts and the trend lines that show stability when you’re looking at a long-term trend of Medicaid or Medicare rate reimbursement. Sure, there’s been a few hiccups along the way with Medicare when there have been adjustments. But over the long term, it’s been pretty stable from the reimbursement perspective. I think history has taught us time and time again that it’s important to be aggressive in some periods and conservative in other periods when you’re projecting forward. So, I would say that today is a time when you want to be a little more conservative in your forward projections because of where today’s markets are. But I think in general, the skilled nursing sector has shown a history of reimbursement that’s been stable when you look at it from a long-term perspective, for example over a 10-year period.

Monroe: Well, I think we’re going to take a deeper dive into all these questions at our session at the NIC Fall Conference. We hope to see you there!

“What’s it Really Worth?” will be held Wednesday, October 17, from 4:00 PM to 5:00 PM. 2018 NIC Fall Conference, October 17-19, Sheraton Grand Chicago. To learn more about the NIC Fall Conference, please visit the NIC Fall Conference website.

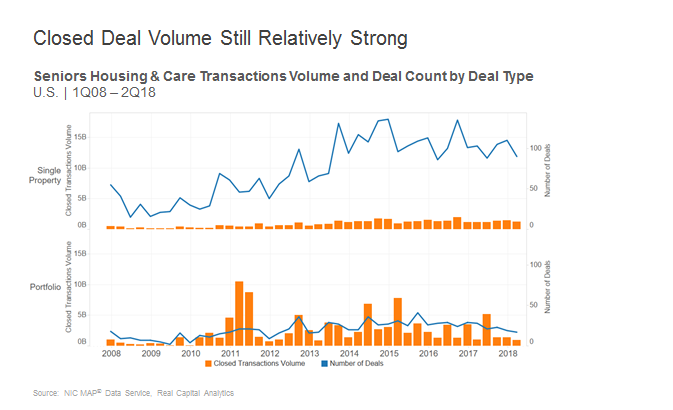

Who Is Driving Property Sales Transaction Activity?

The seniors housing and care property sales transactions market has been active in the first half of 2018, with deal flow keeping pace with over 100 transactions closed in each of the first two quarters of 2018. However, the actual dollar volume of the closed transactions has decreased from the first half of 2017. This is mostly due to the fact that relatively smaller deals are closing, in terms of the dollar amount.

Bill Kaufman

Deal flow still active, dollar volume down

Although a bit slower in terms of activity compared to the first half of 2017, the first half of 2018 saw a robust number of transactions with a total of 236 deals closed as of the second quarter. That compares to 261 deals closed in the first half of 2017, representing a 9.6% year-over-year decline. However, the second quarter of 2018 tallied 107 closings, representing the 19th consecutive quarter of over 100 closed transactions—still relatively robust activity.

As far as the dollar volume, which we will address below, it’s important to note that portfolio sales drive total dollar volume and account for much of the volatility from quarter to quarter. Dollar volume has been relatively low, with another drop in the second quarter of 2018. One reason is that larger portfolio deals have been scarce lately. We have not seen any deals of $500 million or more close in the last two quarters, and we have not seen a deal of $1 billion or more close in the past three quarters.

Seniors housing and care transactions dollar volume in the second quarter of 2018 registered $2.2 billion. That includes $1.6 billion for seniors housing and $600 million in nursing care transactions. The total volume was down 22% from the first quarter’s $2.8 billion, but it was flat when compared to the second quarter of 2017. The rolling four-quarter total seniors housing and care transaction volume was basically flat at $14.3 billion. The rolling four-quarter volume in nursing care was down at $6.5 billion and seniors housing was up at $7.7 billion.

As the data shows us, the activity in the transactions market seems to be relatively healthy but the dollar volume has slowed because of the lack of larger deals, as

explained above. But who is making up the current dollar volume lately? Let’s take a look at the details below.

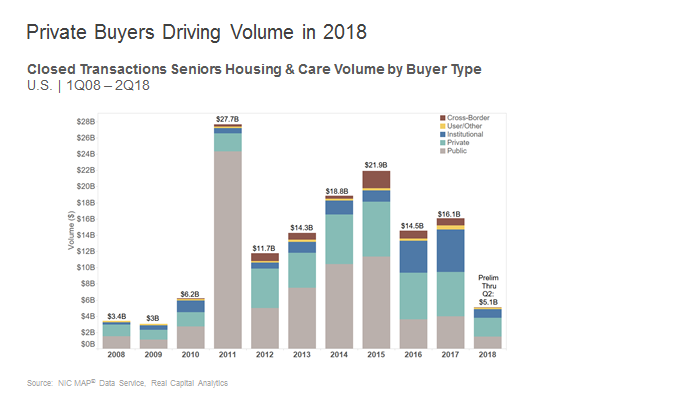

Private buyers drive volume in first half of 2018

As we look at transaction dollar volume for 2018 through the second quarter, the total volume closed across all buyers is $5.1 billion. The private buyer has been the most active participant so far; representing almost half of the closed volume (45%), closing $2.3 billion through the second quarter of 2018 and averaging more than $1 billion a quarter. For comparison purposes, the private buyer represented 34% of total volume for the 2017 year, registering $5.5 billion. However, the private buyer volume did decrease 42% from the first quarter to the second quarter of 2018 from $1.5 billion to $800 million. Private volume for the second quarter of 2018 decreased 38% from the second quarter of 2017 when it totaled $1.4 billion.

The public buyer represented 29% of the transaction volume in the first half of 2018, totaling $1.5 billion. As you can see in the above bar chart, the public buyer represented most of the volume in the prior years of 2013 through 2015. But since then, the cost of capital as well as different market dynamics and strategies have left the public buyer representing less of the buyer activity. However, the public buyer volume did tick up in the second quarter, albeit from a relatively small base, increasing from $573 million to $893 million. Compared to a year ago, the public buyer volume doubled from a very low dollar volume of only $440 million in the second quarter of 2017.

The Institutional buyer volume for 2018 through the second quarter registered $1.1 billion, which represents 21% of volume. On a quarterly basis, as with the private buyer, the institutional volume decreased 39% from the first quarter falling to $412 million from $676 million. Institutional buyer volume has been declining since the third quarter of 2017 when it registered over $2 billion. Compared to a year ago in the second quarter of 2017, institutional volume is up 49% from the minimal activity of only $275 million.

Lastly, as we look at cross-border transactions, there has been minimal activity over the past few quarters with the fourth quarter of 2017 being the highlight with $202 million closed in dollar volume. Just to give some comparison here, over the past four quarters we have seen only $236 million in transactions closed, compared to the previous four quarters with $1.4 billion of cross-border transaction volume. The activity from Asian markets, which was a hot topic in late 2016 and early 2017, has slowed for the time being. Capital controls in countries like China could be a factor, and now we of course have tariff issues across the globe, along with some turmoil in currency markets, that could keep cross-border deals at a minimum for the short-term.

In summary, the seniors housing and care transaction market has enjoyed very liquid markets like most sectors during the last few years. Although 2018 has represented somewhat of a slowdown thus far in terms of the actual dollar volume closed, we have still seen robust transaction market activity in terms of the number of deals closing. The most active buyers have been the private buyers represented by individual owner/operators or smaller investment partnerships. The market will likely continue to be active for the remainder of the year barring any economic/capital market surprises or liquidity issues.

To learn more about the buyers in the market, in addition to a discussion on valuations, join us for our NIC Fall Conference session: “What’s It Really Worth?” To find out more, please visit the NIC Fall Conference website.

NIC Skilled Nursing Metrics – Quality Matters

As the skilled nursing sector evolves, so must the analysis of its properties. Investors and operators are learning that as the system continues to move to more reimbursement for quality and outcomes, it’s becoming more important to pay attention to quality metrics when evaluating any given skilled nursing property. Anyone wishing to complete an accurate pro forma today will need to understand the quality of a building’s medical care, as reflected by metrics such as rehospitalization rates and CMS Five-Star scores, in addition to its brick-and-mortar profile.

In an effort to improve the analytical tools available, and increase the level of transparency in the sector, NIC recently launched quality metrics data on its NIC MAP® Data Service platform through a strategic relationship with PointRight. The combination of CMS Five-Star data through PointRight Pro30 and the data available on the NIC MAP platform provides a wealth of insight. Accessing the data should be intuitive for NIC MAP clients, and valuable insights can be garnered by using these different data sets in combination.

“Quality metrics tools present a way to get a lot of information with only a few data points. By comparing a CMS score to the PointRight scoring, for example, you can understand what questions to ask when digging deeper,” said Liz Liberman, NIC healthcare analyst.

Because there are regulatory benefits to the skilled nursing community of achieving a Star rating of 3 or above, the score has some value in and of itself. But it is important to conduct a comparative analysis because the score may be skewed by geographic area due to the subjective nature of the process. Scoring relies on the judgment of generally one surveyor in a geographic area across many factors—for example, when looking at kitchen cleanliness, one person’s 4 may be another’s 3. For this reason, it is essential to know the average scores for any given property’s geographic area and view national benchmarks. NIC MAP offers the tools to provide this comparative analysis component.

NIC MAP subscribers can access quality metrics data in reports, while raw data can be downloaded and easily rolled into proposals. Rhapsody Carrington, NIC senior client services specialist, recommends that clients use a variety of access points to look for the impact of quality on market performance. She suggests, “Explore correlations in recent skilled nursing sales, between transactions and quality metrics scoring. Look at asking rates, too. Distinct Property Information Reports provide quality metrics data. In one click you can link to other properties in the report. Savvy users can download all that data into an Excel file, enabling their own path to aggregation of their own design.”

Operators will find combining quality metrics within NIC MAP data useful, too. The NIC MAP platform now provides the means available to compare their properties with peers in the same market. While operators have access to detailed data through CMS, until NIC added quality metrics data, there were very few options for providing an efficient local market snapshot. The platform also provides operators with the benchmarking tools they need to present high-level data to their partners, produce sales material, and share with other key stakeholders.

A video tutorial can be found on the NIC MAP support page. NIC looks forward to investors, developers, owners, operators, and other stakeholders taking advantage of this powerful new tool, as the skilled nursing sector continues to experience a significant shift towards value-based care.

Designing For Convertibility Extends The Lifecycle Of A Seniors Housing Property

Richard Wang

By Richard Wang, Vice President of Investments & Strategy at Belmont Senior Living Village.

Developers come in all shapes and sizes. A merchant builder will underwrite and build to very different economic targets than an integrated developer/operator with a long-term strategy. Capital providers have diverse investment horizons and appetites for risk. As developers, we often find ourselves juggling many variables—ranging from optimizing building efficiency and maximizing floor area ratios, to figuring out a project’s economics—to the point that designing for post-operational convertibility naturally takes a back seat.

Every deal boils down to a question of cost. The submarket and location typically dictate the appropriate construction standard. A high-rise in an urban setting will call for non-combustible construction, whereas a project in a rural setting may only pencil out if it is built with a wood frame. As I share some of the things that Belmont Village Senior Living has done to design for convertibility, let’s leave the topics of cost and project-specific applicability for another discussion. As a developer/owner/operator that still co-owns and operates every community we’ve ever built, our firsthand experience on how operational needs evolve over time has taught us many valuable lessons over the years.

Built-in flexibility is what makes a building convertible and adaptable

Flexibility relies on two critical components: structure and licensure. Investing in a steel or concrete structure means that interior walls can be non-load bearing and easily moved—like an office space customizable to meet a tenant’s needs. Building a project to code that allows full licensure means that units are not constrained by their original acuity level designation. Combined, these two factors open up a world of possibilities.

For example, before handing off a project to an outside architecture firm, Belmont’s in-house architects lay out the preliminary building footprint and the units on each floor. Though every building is custom and unique, the units within are fairly standardized, with consistent widths and bay depths. Units are then strategically arranged so that two or more adjacent units can be seamlessly combined into larger apartments. Once operating, we can quickly adjust the product mix to meet changing market demand—and at relatively low cost. To illustrate, we opened Belmont Village Hunters Creek (Houston, Texas) in 2014 with 160 fully-licensed units. Because demand for large units has been astoundingly strong, the original mix gradually evolved into the 126 apartments there today.

Although the trend we’ve seen portfolio-wide has gravitated towards larger units, flexibility also works the other way around. In a downturn scenario where residents seek to downsize, de-combining larger units into smaller, lower-priced units can mitigate market risk.

Next, let’s talk about the benefits of licensing the entire building. As a building ages, so do the residents. Many subscribe to the ageist stereotype that proximity to assisted living residents is unwelcome by independent living residents. In our experience, this is simply not true, provided that the community is vibrant and engaging. Residents who move in as independent will eventually need assisted living support. In a fully-licensed building, the conversion from independent to assisted living is instantaneous. If the resident is able to dictate the care they need at any point in time without having to relocate, there is no leakage with respect to revenue or the continuity of care.

Furthermore, as residents age in place, the overall acuity of the building increases. In response to internal demand, we have converted entire wings of assisted living into secured memory care throughout our portfolio. This is achievable because areas have already been mapped out during architectural design for on-demand, future conversion. Infrastructure is already in place, such as extra parking to accommodate more caregivers, and pre-wired electronic locks to secure entire wings as needed. New memory care program spaces such as activity and dining rooms are created from former units. When the cure for dementia is discovered one day, these program spaces can always be converted back into rentable assisted living units.

Finally, it is important to note is that however well intended, the execution of a conversion requires intricate coordination with operations to minimize disruption to residents—especially when a building is full. When designing for future convertibility, it is also critical to have a firm grasp of the economics behind staffing efficiencies and return on investment. In our experience, adding a new secured memory care wing with only 12 units is oftentimes not accretive due to incremental payroll expense driven by high staffing ratios. If we add more than 24 units, extra shifts may be needed to ensure quality. Every operator staffs differently, and what works well for us (i.e. 18-24 units per secured memory care section) may not work for others.

All in all, built-in flexibility is a key factor that allows a seniors housing building to adapt and convert, thereby extending its lifecycle. It requires due diligence, upfront investment, and more importantly, a willingness to think and act before the first shovel hits the ground.