Inside the November Issue

In this month’s NIC Insider, find actionable insights in Omar Zahraoui’s newest analysis on lengthening construction durations for senior housing. Perspectives on challenges in today’s capital markets are provided in articles by NIC senior advisor Beth Mace, and Future Leaders Council member Sarah Anderson. Read highlights from the 2023 NIC Fall Conference where industry leaders convened to network, learn, and identify strategic opportunities. Learn about the work Bill Ferguson is doing to promote diversity in the industry, and get to know Lisa McCracken, NIC’s new Head of Research & Analytics.

Industry Veteran Launches Fund to Boost Executive Diversity: A conversation with Bill Ferguson

Bill Ferguson is on a mission. A long time professional in executive search and recruitment, Ferguson is leveraging his expertise to advance gender and ethnic diversity in the real estate industry, and specifically senior housing.

Bill Ferguson is on a mission. A long time professional in executive search and recruitment, Ferguson is leveraging his expertise to advance gender and ethnic diversity in the real estate industry, and specifically senior housing.

NIC Chief Operating Officer Chuck Harry recently spoke with Ferguson, chairman at Ferguson Partners. Here is a recap of their conversation on Ferguson’s initiative to bring the next generation of leaders into the industry.

Harry: Can you tell us about Ferguson Partners?

Ferguson: The company was founded 34 years ago. We are now a global talent management platform specializing in executive and board recruitment, along with consulting services across four sectors: real estate; healthcare; infrastructure; and healthcare real estate, primarily senior housing. We have nine offices around the world and 125 team members.

We have close relationships with NIC, ASHA and Argentum, and we do a lot of advisory work in senior housing. I gave up the CEO position about 14 months ago and became chairman of the firm. In addition to my ongoing client work, I serve as Executive-in-Residence for New York University’s C. H. Chen Institute for Global Real Estate Finance and as fellow for The University of Virginia’s Center Frank Batten School of Leadership and Public Policy.

When I became chairman, I launched the Ferguson Family Foundation. Its principle operating business is the Ferguson Centers for Leadership Excellence.

Harry: What is the focus of the Centers for Leadership Excellence?

Ferguson: Our focus is to enhance gender and ethnic diversity across the sectors we serve. The real estate sector, in totality, is the largest industry in the country and the world, but we are not the market leader in recruiting diverse talent.

Harry: Can you tell us more about the Centers for Leadership Excellence?

Ferguson: The concept is modeled on the Marriott-Sorenson Center for Hospitality Leadership. The Marriott family provided a $20 million endowment to launch the Center at Howard University, one of the nation’s leading Historically Black Colleges and Universities (HBCU). The gift was in honor of Arne Sorenson, the CEO of Marriott International who died prematurely of pancreatic cancer. The Marriott-Sorenson Center’s mission is to build a more diverse and inclusive executive workforce within Marriott and the hospitality industry.

A lot of colleges, principally the HCBUs, had no opportunity for students to develop a background for a career in hospitality or to avail themselves of job opportunities. The Marriott-Sorenson Center provides students with exposure to the hospitality business starting in the sophomore year through courses and internships, and then by connecting them to job opportunities in their senior year. I helped Arne’s widow raise money for the Center.

Harry: What is your approach for the Centers for Leadership Excellence?

Ferguson: I decided to tweak the Marriott model to focus on real estate and related sectors. We started with Howard University and have scaled up. This year we have 25 college partners. We focus on colleges that have high potential for diverse talent. Some of our partners include Baruch College, Georgia State University, Florida A&M, Fisk University, University of Houston, UNLV, and Roosevelt University in Chicago, among others. We ask the colleges to nominate students for a fellowship. We provide a three-part value proposition to admitted students: 1) tuition assistance; 2) a holistic mentorship experience; and 3) summer internships for sophomores and juniors, and career opportunities for seniors.

Harry: Can you tell us more about your emphasis on real estate and senior housing?

Ferguson: We have three academic/career tracks with our college partners: operations, finance, and development. Those tracks apply to senior housing, other real estate sectors, as well as hospitality and infrastructure. Senior housing is especially for students who are mission driven. A career in senior housing or affordable housing really resonates with them. We’re excited to work closely with the senior housing industry given the students’ passion for making a difference.

Harry: Your foundation is launching the George Chapman Endowment Fund. Can you tell us about that?

Ferguson: George Chapman was a longtime senior housing executive and a friend of ours. He was the CEO of ReNew REIT and previously of Welltower before he passed away last spring. He was beloved in the industry, and we wanted to honor his legacy. We are raising a $5 million fund in his honor. It will generate $250,000 in investment income a year. That money will be used to recruit 50 college students annually into senior housing tracks with internships for sophomores and juniors, and full-time roles for seniors. We put a leadership council together to raise the money. We already have about $2.5 million in donations before we even officially launch the campaign.

Harry: When is the official launch of the fund?

Ferguson: We will officially launch the fund-raising campaign in January at the ASHA Annual Meeting. George Chapman will be inducted then into the Senior Living Hall of Fame at the meeting. We hope to reach our fundraising goal by June.

Harry: Is there anything else you’d like to add?

Ferguson: We’re going to drive more gender and ethnic diversity in the senior housing industry. These individuals will become leaders and address the economic divide in this country. We are going to make a difference.

You too can make a difference! The George Chapman Endowment Fund supports gender and ethnic diversity in the senior living industry by providing college students with tuition assistance, internships, and job opportunities. Click on this link to find out how you can help.

Higher for Longer, but How High is Higher and How Long is Longer?

By: Beth Mace, Senior Advisor, NIC

The Federal Open Market Committee (FOMC) has met thirteen times since March 2022. At each of these meetings, the Federal Reserve has raised the short-term fed funds interest rates by 25 to 75 basis points. The exception has been the two most recent FOMC meetings (September 20th and November 1st) where the Fed stood pat and kept rates in a range of 5.25% to 5.50%. Fed Chair Jerome Powell has repeatedly stated that the Federal Reserve’s monetary policy decisions on interest rates are data dependent on government statistics and other measures of the economy’s performance. In recent announcements, he and other spokespersons for the Fed have strongly suggested that rates will remain “higher for longer” and that a significant course correction in interest rates is not imminent. While that is not necessarily the viewpoint of the bond market, the Fed does seem to be resolute. The Fed believes that the only way to reduce inflation and inflation expectations is to slow demand and weaken the overall pace of spending and growth.

The Federal Open Market Committee (FOMC) has met thirteen times since March 2022. At each of these meetings, the Federal Reserve has raised the short-term fed funds interest rates by 25 to 75 basis points. The exception has been the two most recent FOMC meetings (September 20th and November 1st) where the Fed stood pat and kept rates in a range of 5.25% to 5.50%. Fed Chair Jerome Powell has repeatedly stated that the Federal Reserve’s monetary policy decisions on interest rates are data dependent on government statistics and other measures of the economy’s performance. In recent announcements, he and other spokespersons for the Fed have strongly suggested that rates will remain “higher for longer” and that a significant course correction in interest rates is not imminent. While that is not necessarily the viewpoint of the bond market, the Fed does seem to be resolute. The Fed believes that the only way to reduce inflation and inflation expectations is to slow demand and weaken the overall pace of spending and growth.

The question is how long is longer and how high is higher? Recent economic data certainly does not suggest that the economy is slowing at the rate likely anticipated and desired by policy makers. In fact, preliminary data measuring the pace of overall US economic growth came in at a whopping 4.9% annual rate in the third quarter, according to the Commerce Department. This marked the strongest performance since late 2021 and was more than twice that of the second quarter. Clearly, the 500-basis point increase in short-term interest rates orchestrated by the Federal Reserve since March 2022 has not yet caused a recession or even a soft landing, as some pundits had projected for this point in the economic cycle; in fact, economic growth has remarkably accelerated.

Consumer spending is an important component of overall economic growth in the US and represented more than half of the third quarter gain in output. Buttressed by a still very strong job market, measured by an unemployment rate below 4% for 20 consecutive months, monthly job gains of more than 250,000 per month during the third quarter, wage growth as measured by average hourly earnings of 3.4% year earlier levels and relatively strong savings, the consumer has remained surprisingly resilient.

And while inflation, as measured by the consumer price index (CPI), has decidedly decelerated from a year-over-year pace of 9% in June 2022 to 3.7% in September, it remains well above the Fed’s desired pace of 2%. Even the Fed’s preferred measure of inflation, the personal consumption expenditure (PCE) deflator, rose 3.4% from year-earlier levels in September.

Hence, the data-dependent Fed is likely to keep rates high through year-end 2023 and into 2024. The Fed will not shift its policy stance until there is undisputable and sustained evidence of reduced pressure on inflation, especially services inflation. So-called sticky price inflation, a measure of rents, services and insurance costs, grew 5.1% from year-earlier levels in September, while flexible price inflation was a tamer 1.0%.

That said, the long-end of the yield curve, as measured by the 10-year Treasury yield has spiked in recent weeks, reaching a 16-year high of 5% in late October. Some pundits believe that higher long-term rates will do some of the work of the Fed by slowing the economy further since so many interest rates are benchmarked off the 10-year Treasury yield. Fixed rate mortgages climbed above 8% recently, for example. Such high mortgage rates will cripple much of the residential home market, especially considering the rapid change in rates from just a few years ago.

Impact of Higher Interest Rates. The rapid ascent of interest rates and the sharp reduction in lending by traditional debt providers such as regional and national banks have had a devastating effect on real estate in general, including senior housing and more broadly all types of commercial real estate. Borrowing for new construction, capital expenditures, acquisitions, and property re-positionings is challenging even for best-in-class senior housing sponsors.

Borrowers who need to refinance and recapitalize existing loans are facing especially significant challenges because paydowns on principle are often needed and loan proceeds are often lower. With $10 billion to $14 billion of senior housing loans maturing in the coming two years, the need for recapitalization finance is formidable and problematic. Borrowers with adjustable-rate debt are often facing unsurmountable debt service costs, as adjustable-rate mortgages roll over to significantly higher rates and often include a costly interest rate cap or hedge as well. And, many 10-year loans issued in 2008 and 2009 had five-year interest-only covenants, and amortization of the principle is now being added to debt service costs.

Further, the transactions market has slowed sharply. Through the third quarter, NIC MAP Vision reports that transaction volumes for senior housing totaled $2.9 billion, 44% of the flow that occurred in 2022 as financing has been challenging and as pricing transparency has been vague at best.

There is evidence of some capitulation in the capital markets, however, as the immediate shock of rate hikes has worn off and buyers and sellers of all types of institutional real estate clamor to transact. Bid-ask spreads are starting to narrow as sellers alter their expectations for sales prices and cap rates, and as buyers adjust their pro forma return expectations and input assumptions on the cost of debt, cap rates, and other variables.

In some instances, closed-end equity funds need to transact as the length of their funds can no longer be extended. In other instances, a sale may be forced if debt service obligations can no longer be met, thereby creating a nascent market for distressed assets. And, in other cases, deals are being purchased for all cash through off-market existing relationships that have a guarantee of quick execution.

The long and short of it is that the transaction market for senior housing will recharge in 2024, albeit at a set point with lower prices and higher cap rates. While the market may not get back to the $11.9 billion trading volumes of 2021, it will surely exceed the pace of deals closed in 2023.

The question remains for how much longer will uncertainty about interest rates keep real estate hostage? In the FOMC’s September Summary of Economic Projections, the median estimate of participants for the federal funds rate was 5.1% in 2024, down from 5.6% in 2023 before sliding further to 3.9% in 2025. The question is whether the Fed will be able to stick to its playbook.

There are many forces outside the purview of the Fed and the domestic government statistics that it monitors that influence the Fed’s decisions. Risks related to the war in the Middle East and the possibility of Iran or the United States getting drawn more directly into the conflict remain top of mind for many reasons, among them the impact an extended war could have on the global oil markets. The price of oil and its direct and indirect impact on inflation, consumer confidence and broad economic growth have been demonstrated time and again—four of the last seven recessions have been influenced by an oil price shock. The dysfunction of the U.S. Congress is also top of mind—there is still a need to pass a budget or an extension to keep the federal government open past November 17th. The Russian invasion of Ukraine, the growing tensions in U.S. Chinese relations, and other geopolitical tensions also add risk the direction of monetary policy as the Federal Reserve must take these considerations into account as well.

Unfortunately, these circumstances create an environment of broad business uncertainty for the foreseeable future. Senior housing investors and operators carry one less risk, however, and that is that demand for their product is and will continue to be strong for the near and foreseeable future.

As always, I appreciate and welcome your comments, thoughts, and feedback.

2023 NIC Fall Conference Accelerates Change - Senior Housing and Care’s premier event delivers three days of content, connections, and actionable insights.

With the senior housing and care sector at a crucial inflection point, the 2023 NIC Fall Conference convened a cross section of industry stakeholders to network, learn, and identify strategic opportunities.

The NIC conference theme, “Accelerating Change” provided a timely framework to address the disruptions that continue to be felt throughout the U.S. economy, the healthcare services sector, the labor and capital markets, and the evolving preferences of aging consumers.

“Transformational disruption demands a pivot,” said NIC Board Chair Susan Barlow, co-founder and managing partner at Blue Moon Capital Partners. “With the pain comes great opportunity for the industry.”

The conference was held October 23-25 at the Sheraton Grand Chicago. Highlights included:

- An economic keynote conversation with former Speaker of the U.S. House of Representatives Paul Ryan on the influence of policy and economics in today’s global risk environment.

- The welcome return of “NIC Talks,” the 12-minute Ted-style talks that offer innovative insights and creative solutions to industry challenges from visionary thought leaders.

- A skilled nursing keynote with Phil Fogg, Jr. on the headwinds and tailwinds driving the sector.

- A multi-layered market analysis from CEO’s of the sector’s top REIT investors—Debra Cafaro and Shankh Mitra.

- Deep dives into the challenges facing the capital markets and what’s ahead.

- An update from executives at the Alzheimer’s Association—Dr. Joanne Pike and Robert Egge—on encouraging medical breakthroughs that will change the course of memory care.

- Multiple daily, formal and informal, networking opportunities.

The conference drew 2,800 attendees, with 74% comprised of C-suite and executive decisions makers. Operators, developers, and capital providers represented 72% of attendees, a mix that supports conversations to promote housing access and choice for older adults. First-time attendees were 23% of conference participants.

Networking Opens Professional Opportunities

Attendees enjoyed multiple occasions to engage in results-oriented meetings with other industry stakeholders. The venue included networking lounges, a large cafe with comfortable seating, and convenient huddle spaces.

Attendees enjoyed multiple occasions to engage in results-oriented meetings with other industry stakeholders. The venue included networking lounges, a large cafe with comfortable seating, and convenient huddle spaces.

The conference featured several well-attended receptions, including one for first-time conference attendees. A Women’s Networking Meetup drew several hundred women who exchanged ideas and made connections. Women represented 23% of attendees at the conference.

NIC Board Chair Barlow spoke to the women’s meetup and relayed her own story of how she and Kathryn Sweeney shared a cab ride after an industry meeting and then decided to launch their company, Blue Moon Capital Partners. “This gathering is an actionable event,” said Barlow. “Identify opportunities in your organization and ask yourself what you are doing to move forward. Get involved.” She added that her participation in NIC had prepared her to succeed throughout changing business cycles.

NIC hosted a reception for college scholars who are currently enrolled in senior living programs and attended the conference via conference scholarships sponsored by Welltower. NIC Co-Founder and Strategic Adviser Bob Kramer spoke at the reception. He emphasized that senior living offers excellent career opportunities for those inspired to “do well by doing good.”

A NIC Academy Skilled Nursing Boot Camp was held on site on the final day of the conference. Participants analyzed a case study on whether to buy, sell or hold a nursing property. The Boot Camp is part of the NIC Academy which offers programs for senior housing and care professionals, including an education certificate program on how to underwrite senior housing properties.

Experts Discuss Relevant Topics

The conference offered 10 stand-alone educational sessions. Many of the discussions addressed both the tailwinds and headwinds faced by the industry. (High quality videos of most educational sessions are available to attendees in the conference mobile app. Click here to access the app.

A standing-room only crowd packed the ballroom for the keynote session with former U.S. House Speaker Ryan. He held a conversation on stage with Bob Hillis, chairman, CEO and founder of Direct Supply/Aptura.

Known for his policy expertise, Ryan expects capital to be more expensive for a longer period of time. He said that the massive amount of U.S. Treasury debt offerings coming due will need to be refinanced at attractive yields which will keep interest rates high.

Ryan also pointed to positive tailwinds for the industry, including a healthy jobs market and an aging population. The discussion also covered the regulatory environment, technology, immigration, and the current political landscape. Ryan noted that it was never a good idea to bet against free enterprise.

NIC Talks featured four main-stage speakers. The session was curated by NIC’s Kramer. “These speakers inspire us to think differently about senior housing and care,” he said.

Caroline Pearson, executive director of the Peterson Center on Healthcare challenged the audience to embrace the integration of healthcare and senior housing. “Think about ways to locate healthcare services in your community,” she said, explaining that healthcare is both a need and a want of residents.

Former Apple executive Dhaval Patel provided a roadmap on how to sort through various technology offerings and select the right ones. His advice: Ask yourself if the technology is solving the right problem.

Other provocative topics presented by NIC Talks speakers Hanh Brown, Founder and CEO of ThinkA16, and Gerard van Grinsven, CEO of Van Grinsven Hospitality Group, included the impact of artificial intelligence on senior living and how to delight and surprise consumers.

Capital Markets Under Strain

Several sessions addressed the state of the capital markets and financing challenges. However, the panelists agreed that a huge wave of new demand from aging baby boomers will change market dynamics.

The opening panel discussion paired Ventas Chairman and CEO Debra Cafaro and Welltower CEO Shankh Mitra. The session was moderated by Randy Richardson, former CEO, president and strategic advisor at Vi Living.

Out of control construction prices and the dramatic spike in the cost of capital will continue to dampen new development, according to Mitra. Cafaro said that a big company with staying power helps to ride out commercial real estate cycles.

A deep dive into the debt market and a separate session on valuations illustrated the challenges faced by investors. Arick Morton, CEO at NIC MAP Vision provided some perspective on market fundamentals. Occupancy is recovering and rent growth has caught up with wage growth. Demand is strong.

The final day of the conference kicked off with a keynote discussion titled, “Navigating the Current Skilled Nursing Environment.” Phil Fogg Jr., CEO at Marquis Companies, was interviewed by Steve Monroe, editor at large at Irving Levin Associates.

As immediate past Board Chair of the American Health Care Association, Fogg gave a thorough analysis of the skilled nursing sector. He is concerned about proposed regulations that mandate new staffing minimums. But Fogg expects providers to have more negotiating power with payers in the next 3-5 years.

Attendees also heard from experts on promising Alzheimer’s research, the alignment of management companies and owners, and how to establish inclusive labor practices.

During a session on how to appeal to the new consumer, moderator Helen Foster, principal at Foster Strategy, challenged attendees to experiment. “Baby boomers will change our industry,” she said. “So many solutions are needed. True innovators are looking to outside sources for inspiration. We have to take risks.”

Mark your calendar! Join us March 5-7 at the 2024 NIC Spring Conference in Dallas. Watch for more information later this month.

Get to Know Lisa McCracken, Head of Research & Analytics at NIC

Recently, NIC announced the appointment of Lisa McCracken as Head of Research & Analytics. A nationally recognized expert in senior housing, corporate finance, and healthcare, McCracken will further NIC’s goals of providing actionable insights and thought leadership to enhance access and choice for older adults.

The NIC Insider spoke with McCracken at last month’s 2023 NIC Fall Conference in Chicago to learn more about her new role, how implementing NIC’s Strategic Plan can benefit the industry, and what excites her about the future of senior housing and care.

WATCH NOW

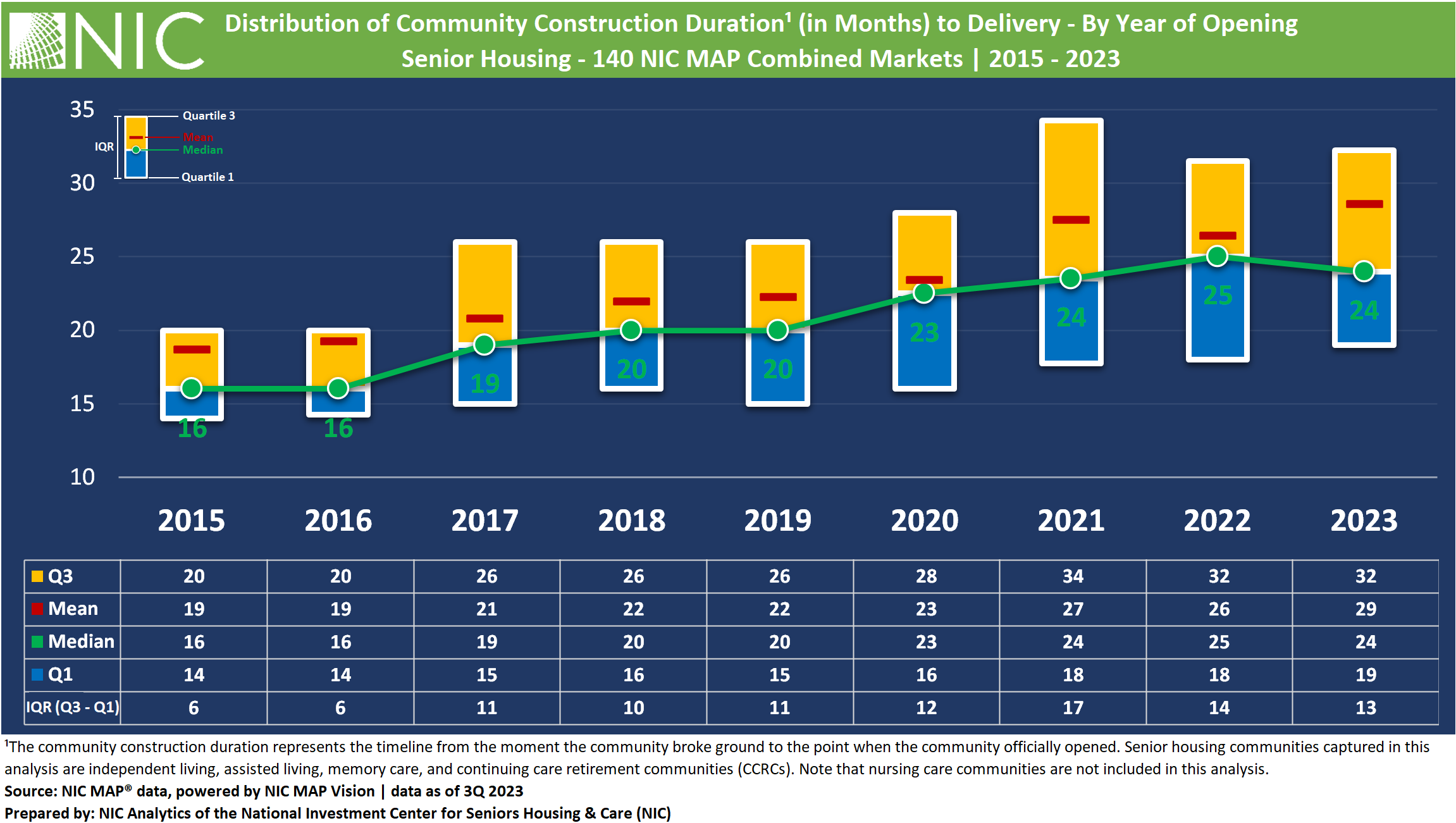

Rising Construction Durations in Senior Housing: Beyond the Pandemic Effect

By: Omar Zahraoui, Principal, NIC

The construction of senior housing communities has faced a myriad of challenges in recent years, evidenced by a marked decline in construction starts and extended construction durations. These challenges have been apparent since the onset of the COVID-19 pandemic, and have been further compounded by labor shortages, a lack of building materials, and inflation. Additionally, the quick and large rise in interest rates orchestrated by the Federal Reserve has led to higher construction financing costs, limited availability of debt, and increased development costs. These combined factors have prolonged the time it takes to bring a senior housing project from the planning stages to the construction phase and eventually to its final delivery and eventual opening.

This analysis examines how the length of time to bring a project to its completion has changed in recent years (construction duration as measured in months) across the 140 NIC MAP All Markets.

Key Takeaways:

- The data shows that there has been a steady and consistent increase in the time it takes to construct a senior housing community from 2015 to 2023, suggesting that extended construction duration is not exclusively a post-pandemic trend.

- Median construction durations have risen from 16 months in 2015 and 2016 to 19 months in 2019 to then 25 and 24 months in 2022 and 2023, respectively.

- Heightened project deliveries and “oversupply” have played a role in the variability of construction durations and have contributed to a protracted construction process.

- Fewer construction starts and extended durations of project deliveries provide short-term support for the sector’s occupancy recovery.

- There will be a pressing need for new construction to meet future demand and adapt to evolving resident profiles and changing requirements.

- About 41% of senior housing communities are more than 25 years old, and the population age 80 and older is expected to grow by 5.1 million by 2030, equivalent to a 35% increase.

- Notable shifts in construction timelines are not uniform and vary widely by region.

Methodology:

NIC Analytics conducted an in-depth analysis to examine the length of time required to build a senior housing property, i.e., the construction duration (in months) across the 140 NIC MAP All Markets and explore the shifts taking place in construction timelines across different regions. This analysis primarily focuses on new property developments and captures a minimum of 83 construction completions annually, spanning the period from 2015 to 2023.

The construction duration represents the timeline from the moment the community broke ground to the point when the community officially opened. This analysis uses the community type designation. Senior housing communities captured in this analysis are independent living, assisted living, memory care, and continuing care retirement communities (CCRCs). Note that nursing care communities are not included in this analysis.

Prolonged Construction Duration for Senior Housing: A Post- Pandemic Challenge?

The exhibit below depicts the distribution of community construction duration in months, from 2015 to 2023, by year of opening, and demonstrates a clear and consistent trend of increasing construction durations over the time period, with a noticeable increase since the onset of the pandemic in 2020.

The analysis also reveals that the extended construction duration is not exclusively a post-pandemic trend. Even prior to the pandemic, particularly from 2016 to 2020, construction durations were on the rise. This trend was largely attributed to a period of heightened project deliveries.

During the delivery boom from 2016 to 2020, the senior housing market saw a surge in new project completions, causing a temporary oversupply of senior housing units, a moderate absorption-to-inventory velocity (AIV ratio) falling below the AIV threshold, and a decline in occupancy rates. This in turn led to a protracted construction process. Challenges stemming from the pandemic, high interest rates, and other economic factors only contributed to the observed prolonged construction duration.

The median construction durations have consistently risen since 2015, from 16 months in 2015 and 2016 to 19 months in 2019, to then 25 and 24 months at their peak in 2022 and 2023, respectively. However, construction durations are not uniform. The analysis highlights a wide range (Interquartile range, IQR) in construction durations within the senior housing sector, where some projects are completed relatively swiftly, while others take longer to reach completion. Specifically, for the senior housing projects delivered in the last three years (2021- 2023), 25% of senior housing communities were completed in less than 20 months (Quartile 1, Q1), while another 25% took more than 30 months for delivery (Quartile 3, Q3).

The variability in construction durations – influenced in part by factors such as community type and size – also highlights the differences in access to capital and financing within the senior housing sector. Notably, even amidst the challenges posed by the pandemic, elevated interest rates, increased development costs, and economic uncertainties, there remain senior housing operators who retain the ability to successfully secure financing and complete projects within reasonable and efficient timeframes.

While construction starts plummeted in recent years and some projects took longer to complete, providing short-term support for the sector’s occupancy recovery, there will be a pressing need for new construction to meet future demand and adapt to evolving resident profiles and changing requirements. Notably, approximately 41% of senior housing communities are more than 25 years old. Additionally, the U.S. population aged 80 and older is projected to grow by 5.1 million by 2030, a 35% increase, according to U.S. Census 2022 projections.

Separately, the 1Q 2023 NIC Lending Trends report points to a cautious lending climate, with a notable slowdown in construction requests and issuance of debt financing new construction for senior housing. The survey indicated that lenders are responding to these changing conditions by focusing on strong sponsorship and strong credits. This trend reflects a reaction to a jump in the SOFR and 10-year Treasury rates, lower loan-to-value (LTV) ratios, tighter spreads, leaner proceeds, and higher equity requirements. Additionally, new construction loan closings for senior housing remained notably weak in the first quarter of 2023 compared to historical standards, with only two other periods in the time series matching this low level — the third quarter of 2022 and the first quarter of 2021.

Extended Delivery Times for Senior Housing Projects Compared to the Pre-Pandemic Era, with Regional Timeframe Variations

The exhibit below shows the distribution of construction durations (in months) for senior housing communities by region. It provides a comparison of project completions in the three years preceding the pandemic (2017-2019) with the three years following the onset of the pandemic (2021-2023).

Prior to the pandemic (2017-2019), senior housing construction durations displayed regional variations. In the post-pandemic era (2021-2023), we observed notable shifts in construction timelines. However, these changes are far from uniform and vary widely by region.

The Mountain Region stands out with a notable increase in median construction duration, rising by 10 months from 19 to 29 months when comparing the pre-pandemic and post-pandemic periods. This is followed by the Northeast, with an increase of 9 months (from 17 to 26 months), and the Pacific, showing an increase of 8 months (from 16 to 24 months). Notably, these regions exhibited some of the shortest median construction durations in the three years leading up to the pandemic, whereas, in the last three years (2021-2023, post-pandemic), their median construction durations ranked among the highest in the country.

Conversely, the West North Central region sustained a relatively steady median construction duration, with merely a 3-month difference between the two periods, shifting from 18 to 21 months. The West North Central region had the shortest median construction duration across all regions in the most recent three years. In the Southeast and Southwest, although there were relatively small increases in construction duration during the last three years, at 26 and 24 months, respectively, they still stand comparably high in contrast to the overall construction durations seen in the pre-pandemic era.

In summary, the data suggests a widespread increase in construction durations across all regions during the post-pandemic era. The widening of the interquartile range reflects increased variability and broader shifts in construction timelines. These changes have been primarily attributed to disruptions in the supply chain earlier in the pandemic and more recently to labor challenges, inflation, increases in construction wages, and higher interest rates, collectively impacting various facets of construction financing, elevating development costs, and impeding the pace of construction starts and completions.

In future publications, NIC Analytics will explore units under construction, comparing the Great Financial Crisis with the pandemic era and examining construction in the pipeline across U.S. regions and senior housing community types.

The aim of this analysis, along with the comprehensive work conducted by NIC Analytics, extends beyond highlighting differences in construction duration and providing comparisons between the pre- and post-pandemic eras. The core message is to increase transparency and highlight that short-term challenges bolster the sector’s resilience, as demonstrated in recent years. Obstacles can spark innovation, ultimately leading to enhanced access and choice for the older adults of today and in the future.

Looking ahead, the senior housing sector is at the precipice of transformative change. The fundamentals are evolving, with favorable demographic trends but a “higher-for-longer” interest rate environment, and those operators who can assess and embrace these changing trends, adapt with agility, and drive innovation will undoubtedly experience remarkable growth in the future.

Market Insights Interview with Chad Lavender, Newmark’s President of Capital Markets for North America and Co-head of Healthcare and Alternative Assets

By: Sarah Anderson, Senior Managing Director, Newmark

I recently spoke with Newmark President of Capital Markets, Chad Lavender, to hear his thoughts on today’s markets and activity in senior housing and care.

I recently spoke with Newmark President of Capital Markets, Chad Lavender, to hear his thoughts on today’s markets and activity in senior housing and care.

Anderson: What are you seeing in terms of transaction activity for senior housing?

Lavender: Transaction volume in 2023 will be well below years past as we started the first half of the year with a major bid-ask gap between buyers and sellers. Really it started at the end of last year after the Fed continued its raising of interest rates from effectively 0% in March of 2022 to almost 5.5% today. The writing was on the wall that interest rates would go up but doing so 11 times over this long of a period meant a slower reaction from the capital markets. I believe we are now at a point where buyers and sellers are capitulating and finding solutions that work for both parties.

Anderson: So, you are seeing an increase in deals trading this month?

Lavender: We are starting to see the bid-ask gap narrow between sellers and buyers following a major price dislocation due to elevated interest rates and lack of debt market liquidity that hindered the investment sales market. The market now understands that unfortunately it does not look like interest rates will be decreasing in the near future. This means that a seller would have to be able to increase property-level NOI and performance to improve the value of their property rather than simply relying on cap rate compression to derive value. Volatility is also at an all-time high, with the 10-year treasury swinging up and down by 15 basis points in a single day. When the treasury moves that quickly, there is a direct impact to the pricing of debt and therefore the purchase price on an acquisition. So, buyers are pricing in that risk, and sellers are seeing that playing out in real time.

Anderson: Where do you see opportunities in senior housing right now?

Lavender: I think this is a great time to be investing in senior housing. We are at the precipice of improving operating fundamentals, limited new supply, and increasing demand from baby boomers. With only a little over 2,800 new units that started construction in the second quarter, which is the lowest number of starts since 2009, this should lead to a meaningful improvement in senior housing occupancy and performance. We expect, given that the banks are extremely selective or some entirely out of the market for construction, this will only continue through 2025.

In the meantime, we are fielding calls almost daily from equity groups that are trying to find ways to invest in senior housing. Many of them don’t have an existing senior housing portfolios, so they have a “clean slate” to enter the space. Senior housing has and will continue to offer a very attractive risk-adjusted return to investors. Right now, an investor has the opportunity to buy a nearly brand-new community that is still in lease-up at a significant discount to replacement cost, and they can underwrite to a return that we would have previously only seen from a ground-up development. You’re also able to buy core, well-performing deals for approximately 6.5% cap rates, which is 200 basis points above where those same deals traded over the last five years.

Anderson: Is there a certain product type that new and existing investors are more interested in right now?

Lavender: In terms of acuity, we are definitely seeing a lot of interest if a community has a full offering of independent living, assisted living, and memory care. Stand-alone memory care is out of favor and combined assisted living and memory care is still getting attention, but the community has to be big enough to achieve an attractive margin to make the numbers work. There is also still a lot of appetite for active adult right now given there is more liquidity for active adult on the debt side. Lastly there’s also a trend towards properties that have a higher one- and two-bedroom count than studios. A recurring trend we are seeing across the deals we are working on is a softness in studio occupancy and an increase in concessions being offered on those units.

Anderson: So, if you can find a buyer and seller that are willing to agree on a price, how are buyers financing these acquisitions?

Lavender: For properties that are stabilized and have a strong operating margin and in-place cash flow, buyers are going to the GSEs and life companies primarily. Freddie Mac and Fannie Mae are both being highly selective on the deals that they quote, however, their terms are still competitive. Neither Fannie Mae nor Freddie Mac are expected to hit their stated lending caps for the year, so we don’t have the scarcity of loan dollars from either lender like we typically would at the end of the year.

For properties and portfolios that include properties that are not yet stabilized from an occupancy and NOI perspective, some buyers are unlevered, some are leaning in on their banking relationships, and others are looking to debt funds if the property can support the higher interest rates associated with that source of financing.

Anderson: What do you anticipate the capital markets and the senior housing industry will look like in 2024?

Lavender: In my opinion, independent living, assisted living, and memory care communities are going to be one of the only commercial real estate sectors where the underlying performance is expected to have outsized growth with demographics spiking significantly starting in 2026. Green Street is forecasting 20%-plus NOI growth for our industry over the next two years, and I don’t know of another commercial real estate property that is expected to achieve the same improvements. There is also $250-plus billion of multifamily loan maturities in 2024 across all lender classes which is going to be a driving motivator for sellers. So, while the industry is feeling and will continue to feel some short-term pain, we and our clients are preparing ourselves for brighter days ahead.