Private Investors Put Big Money into Care Delivery Start-Ups

New Platforms Offer Opportunity for Building Owners to Add Value

An under-recognized investment trend is gaining momentum that has the potential to enhance senior living operations and boost returns.

Private equity and venture capital firms are pouring hundreds of millions of dollars into innovative business models related to home care, primary health care coordination, and new technologies targeted specifically at frail seniors. [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

These burgeoning enterprises serve the same population as seniors housing operators, but they’re not typically tied to a bricks-and-mortar model. Instead, they offer new ways to deliver care and services to elders, which presents an opportunity for savvy seniors housing operators and investors.

“You can’t care for seniors and be a successful operator in the future without having a greater awareness of the innovation taking place in aging care service delivery,” said Anne Tumlinson, CEO at Anne Tumlinson Innovations, a consulting firm based in Washington, D.C. “Real estate-based operators need to expand their capabilities and leverage these new platforms.”

The upcoming 2017 NIC Spring Investment Forum will feature a session on the topic moderated by Tumlinson titled “Hot New Investments in Senior Care.” The NIC Spring Investment Forum is being held March 22-24 in San Diego at the Hilton San Diego Bayfront. The Forum’s programming will have three areas of focus: capturing value; creating successful partnerships; and economic, capital, and policy trends.

An “aha” moment sparked the idea for a NIC session on hot senior care investments. After conversations with owners and operators, Tumlinson identified that the massive investment deal flow into senior care start-ups is practically unseen by real estate investors. “These deals exist in an almost parallel universe,” said Tumlinson. “There’s a broader market out there. We need to connect the dots.”

A myopic focus exclusively on real estate-based delivery won’t serve operators and investors well in the future, Tumlinson explained. The NIC session aims to raise awareness of the incredible amount of confidence that venture capital and private equity firms have in non-real estate-based investments to deliver value to payors and consumers in a risk-based world. “These investment firms get it,” she said.

Session attendees will learn how new care delivery platforms can be leveraged to add value to their operations, said Tumlinson. “Our thesis is that when you add value for the consumer and improve the efficiency of the health care system, you add value for the investor,” she said.

Tumlinson will be joined on the panel by Melanie Bella, an industry consultant who has spent her career focused on transforming care for complex and costly populations in the Medicaid and Medicare programs. Bella established and served as the first director of the Medicare-Medicaid Coordination Office at the Centers for Medicare and Medicaid Services (CMS).

Other session panelists include Dr. Benjamin Berk and Burt Yarkin.

Berk is a physician and CEO of Attuned Care, which provides coordinated care for residents of senior living communities. Previously, Berk was vice president of population health at Iora Health, serving as business lead for Iora’s Medicare Advantage and risk-contract practices.

Yarkin is managing director of the McLean Group’s San Francisco office, with more than 25 years’ experience in the franchising business and a history of growing businesses. Yarkin advises global companies, franchisors and large multi-unit franchisees and senior care businesses on mergers & acquisitions and capital formation.

Hot New Investment Platforms

The NIC session will highlight several care delivery areas where private investors are currently active. Some examples include:

• Home care. It’s estimated that more than $200 million was invested in home care companies in 2016. Session panelist Yarkin will discuss how venture capital and private equity firms have been shifting their attention from bio-technology and pharmaceuticals to home care, and how home care is changing the way services are delivered.

• Enhanced primary care services. Panelist Berk will discuss his company’s approach to enhance primary care in seniors housing. The model relies on nurse practitioners who care for residents to avert unnecessary trips to the hospital.

Other companies also are grabbing investors’ attention.

Iora Health, which offers digitally-enabled private care services for seniors, closed a $75 million Series D funding round led by a Singapore-based investor. Iora creates special private practices for high-risk, high-cost populations of seniors on Medicare. Each patient has a care team that includes a health coach, a behavioral health specialist, a nurse and doctor. The company also offers an IT platform, known as Chirp that gives patients open communications with the care team and access to medical records.

Chicago-based Oak Street Health, a network of primary care clinics, coordinates care for low-income seniors in Medicare and Medicare Advantage plans, reducing their need for expensive hospital visits. A private equity firm financed Oak Street’s expansion, doubling the company’s size over the past year to serve 25,000 patients.

• Technology. New platforms are evolving that enable organizations to communicate across sites of care to help reduce costs. These include business models that enhance operational capabilities using data for clinical pathway management.

The new platforms and start-ups are not competitors, but collaborators, said Tumlinson, a point that will be emphasized at the NIC session. “Seeing these new platforms as competitors is the old-fashioned, silo-based mentality,” she noted.

Seniors housing providers need to be able to reach out not just to the residents in their buildings, but also to members of the community that may one day be residents of the building. “There is a broader market (of seniors) out there, and how you reach them depends on the relationships you have with organizations that also reach those seniors,” said Tumlinson. [/expand] [cresta-social-share]

Seniors Housing Will Play a Role in Home Care Evolution

Forget the old home care model, and think Uber instead.

While the traditional home care agency still persists, entrepreneurs are launching technology-enabled home care platforms that connect the consumer directly with in-home caregivers. Something like the on-demand ride services such as Uber, these home care start-ups are likely to revolutionize the rapidly growing $17 billion home care industry. [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

The change represents an opportunity for seniors housing and care owners and operators to collaborate with these new home care companies, according to Kelsey Mellard, head of health system integration at Honor, a San Francisco-based technology company that links in-home caregivers and seniors to provide help with the activities of daily living. “Home care companies such as Honor can help senior living communities keep their residents so they can age in place,” said Mellard.

A featured speaker at the 2017 NIC Spring Investment Forum, Mellard recently talked with NIC about what owners and operators can expect to take away from her presentation. She will speak at a session titled, “Seniors Housing’s Role in The Home Care Evolution.”

Mellard will be joined on the panel by Jacquelyn Kung, principal at Atruya, which is based in San Francisco, CA. She is a senior living entrepreneur and consultant who previously co-founded ClearCare, a home care agency software developer and provider. Also speaking on the panel will be Daniel Schwartz, COO of Almost Family, which is a home health nursing, rehabilitation and care services provider that has more than 250 locations in 15 states.

The new home care technologies are being developed in response to an industry ripe for innovation. Honor, for example, was launched about 18 months ago. The company provides an online service that connects caregivers, seniors and their families. Customers can access the service through the Honor software application, or app.

Honor currently operates in San Francisco, Los Angeles and Dallas. It has plans to expand further. The investor community has taken note of its early success. Honor has raised about $62 million in venture capital, including from well-known firms such as Andreessen Horowitz.

Honor’s strategy focuses on four areas:

• Care professionals. The goal is to improve their lives so they can deliver the consumer a better experience. The Honor caregivers are employees of the company and enjoy higher wages than those at many traditional home care companies. They also have the option to decline jobs that don’t fit their schedules.

• Families/care team inclusion. A common complaint among consumers contracting with a traditional home care agency is the lack of information and transparency about the worker’s visit. The Honor app serves as the communications hub. With the caregiver’s input, the app alerts the family when the worker arrives and leaves the home. The worker leaves a “care note” that describes what happened during the visit. The caregiver also provides a quantitative rating from 1-10 on five measures of well being: sleep quality, pain, mood, appetite, and bowel movements. “It gives the family peace of mind,” said Mellard.

• Technology. The Honor app does the heavy lifting. The app increases efficiency by handling scheduling and billing, as well as providing the wellness report. There are no contracts for families, who can sign up for as little as one hour of care, in contrast to traditional agencies that may require a four-hour minimum.

• Health systems. The app can engage with people wherever they need the service. Honor is partnering with health care providers and hospitals to help reduce hospital readmissions and act as a vehicle to help elders transition home, and stay home.

Several opportunities for partnering with seniors housing and care operators are emerging, Mellard said. For example, independent living communities can use the Honor app to help keep residents in their apartments longer as they need more services. Also, assisted living operators can supplement their staffing with Honor, requesting more workers as needed.

Home care companies and seniors housing providers share a common goal, Mellard said. They both want to provide elders with a sense of independence and community.

“We can come together,” said Mellard. “We have the opportunity to redefine what it means to age and leverage services like home care. Collaboration is the key.”

The NIC Spring Investment Forum is being held March 22-24 in San Diego at the Hilton San Diego Bayfront. The Forum will focus on three themes: capturing value; creating successful partnerships; and economic, capital and policy trends. [/expand] [cresta-social-share]

Seeing Opportunity When the Future Is Fuzzy

AHCA’s Mike Cheek Previews Medicaid Session at 2017 NIC Forum

No one is watching for news about Medicaid legislation perhaps as closely as the American Health Care Association (AHCA), a nonprofit federation of affiliate state health organizations.

Probable changes to Medicaid will mean new challenges for the more than 13,000 skilled nursing, assisted living, developmentally-disabled, and subacute care providers the organization represents. But, said Mike Cheek, AHCA’s senior vice president for Reimbursement & Legal Affairs, “along with the risks, there are opportunities.” [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

The changes to Medicaid policy—and three key states’ responses to them—will be the main focus of a session titled “The Medicaid Question: What’s Happening in Leading-Edge States” at the 2017 NIC Spring Investment Forum, March 22–24 in San Diego. Cheek, a health care policy expert with over 20 years of experience, will moderate the session.

Benefits for Skilled Nursing—and Assisted Living

The current regulatory environment has created roadblocks for post-acute care and long-term care operators. Many states have large backlogs of Medicaid eligibility determinations and redeterminations that cause delays in reimbursement. “This is an issue for the beneficiary and a challenge for the provider, as well,” said Cheek. Operators should take a proactive approach to eligibility determinations, he said, to give the state as much information as possible up front to help mitigate delays.

On the assisted living side, obtaining clarification on home- and community-based services (HCBS) regulation would be a “big ticket item,” according to Cheek. It’s unclear if a licensed assisted living property would be eligible for Medicaid reimbursement under the current HCBS rules, and “that is a universal concern,” said Cheek, “for the states, the beneficiaries, and the provider community.”

Overall, he said, collaboration with local providers could be a significant benefit to skilled nursing and assisted living. “Offering some flexibility associated with risk-bearing opportunities—ideally in collaboration with the providers in their community—would be helpful.”

Changing Health Care Policy—What Operators Want

Medicaid reform was mentioned frequently during last year’s Presidential campaign, and many in the industry are expecting to see the Trump Administration roll out new legislation in the near future. This is the time for post-acute care and long-term care providers to make their voices heard by members of Congress, said Cheek, for legislation at both the federal and state levels.

He pointed to some services that are not currently mandatory but profoundly beneficial to people using long-term services and supports (LTSS): dental care, certain types of lab tests, and non-emergency medical transportation. “Stripping away non-mandatory benefits,” Cheek said, “could in turn have significant ramifications for the health and functional stability of older adults.” Skilled nursing providers often provide many of these services, which could present the providers with new opportunities for bearing risk while helping states achieve their goal of paying for value versus volume.

Innovative Approaches for Better Care

In terms of innovation, technology plays a big role. For example, many states have explored linking data systems and assessment tools to “create a more comprehensive resource for care management,” said Cheek.

He cited a data project in Maryland that linked assessment information with claims data so that case managers could view an individual’s historical care in order to better anticipate future needs. In Oregon, a project is underway to create a care management tool that captures behavioral information in addition to health information in order to encourage positive behavior changes.

Overall, Cheek said, states need to be looking to streamline the eligibility determination process and remove barriers between higher and lower intensity care so that Medicaid beneficiaries can get the care they need, when and how they need it

Operators’ Next Steps

While the future of Medicaid policy is unclear, there are a few actions skilled nursing and assisted living operators can take now, according to Cheek.

First, with value-based purchasing expected to “accelerate under a reform to Medicaid,” Cheek recommended that operators begin assessing their quality measures through tools such as AHCA’s Long-Term Care Trend Tracker. The quality metrics are important not only for understanding their own performance, but to prepare for having to demonstrate quality.

Second, Cheek suggested that operators reach out to the Medicaid agency and disease groups in their state to better understand how the care of certain populations is prioritized. Then operators could explore approaches to delivering specialty care. “It could be something as basic as having more innovative, less restrictive dementia care arrangements,” he said, “to offering more in-building or even bedside dialysis.”

Finally, Cheek encouraged relationship-building with acute care providers so that operators have a better understanding of their pressure points with both Medicaid and Medicare—and how these providers plan to interact with long-term care going forward. “Understanding what their pressure points are and learning to work as collaboratively as possible with them will be important,” he said.

For attendees of the session at the 2017 NIC Spring Investment Forum, Cheek promised an in-depth look at Medicaid policy in California, Texas, and North Carolina, so session attendees could better understand what reform will mean in their own states. “While reform brings forward a great deal of risk for long-term care providers,” he said, “there are opportunities—for risk-bearing, for value-based purchasing arrangements, and for developing new lines of service.” [/expand] [cresta-social-share]

2016 Transactions: Volume Down but Deal Flow Still Strong

by Bill Kauffman

Last year marked a significant change in the property sales transactions market for seniors housing and care. Over the past few years, public buyers, dominated by public REITs, have been the primary players in driving large transaction volume. However, as the cost of capital increased in 2016 for public REITs, institutional buyers and private buyers (including private REITs and partnerships) together accounted for the majority of dollar volume. [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Although the institutional and private buyers were the most active during 2016, they were not able to make up for the dollar volume of closed transactions typically produced by public REITs. In turn, volume dropped significantly from 2015. The number of transactions closed was still strong, but the average size of the transactions was smaller in 2016.

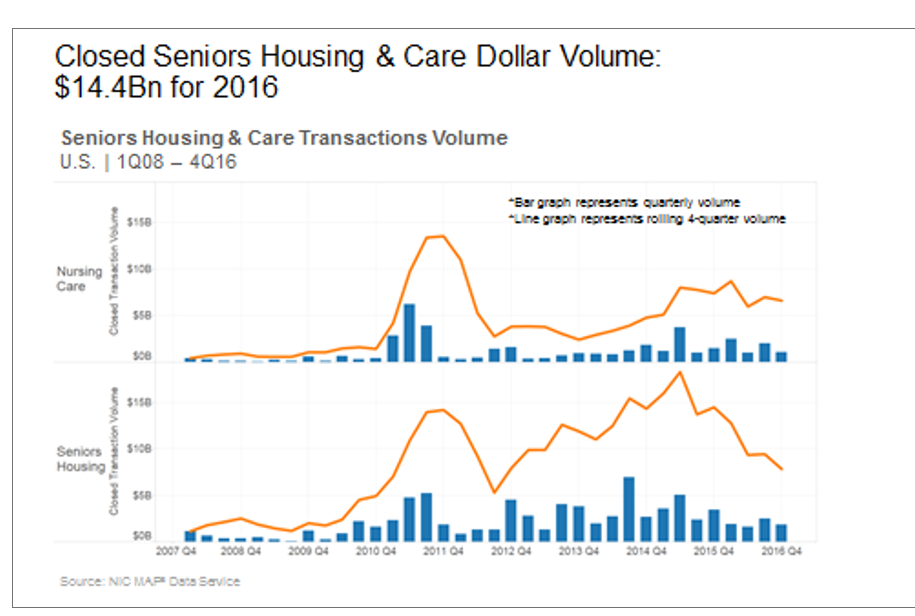

Dollar Volume Trending Down

Transactions volume for seniors housing and care in 2016 registered $14.4 billion, with $7.8 billion in seniors housing and $6.6 billion in nursing care. Total annual volume was down 34% from 2015’s $21.8 billion and down 25% from 2014, when volume totaled $19 billion.

2016 started out as a tumultuous year in the capital markets. Usually, the first quarter of a year starts off slow given the prior rush to close deals at the end of the previous year, which effectively empties the pipeline of deals. Then volume typically picks back up in the second quarter. In 2016, however, the significant increase in cost of capital most likely delayed the finalization of some deals, and we did not see the strong bounce back in deal volume in the second quarter as we had seen the past couple of years. Only $2.6 billion closed in the second quarter of 2016 after a relatively strong first quarter of $4.3 billion.

If we dig deeper and look at seniors housing and nursing care separately, we see that the decrease in volume from year to year was really driven by seniors housing volume, as volume decreased significantly by 46%, from $14.4 billion in 2015 to only $7.8 billion in 2016. Nursing care volume was down, but not as much. Its volume decreased by 11% in 2016, from $7.4 billion in 2015.

Although dollar volume dropped significantly, the number of transactions was still relatively strong in 2016: 513 deals closed in 2016. Transaction deal count was down 9% from 2015, when 563 deals closed—a record high for this database that dates back to 2008. In further comparison, 414 transactions closed in 2013 and 556 in 2014.

A primary reason for the difference between the dollar volume trend and the deal count trend is the decline in the number of large deals over $500 million. In 2015, 10 transactions closed, with only half that in 2016. The drop in large deals can have a significant effect on the dollar amount, but not necessarily the number of deals closed. For example, the only cohort range that increased from 2015 to 2016 was the $10 million to $50 million range, which includes very small portfolios of two to three properties and/or one-off property deals.

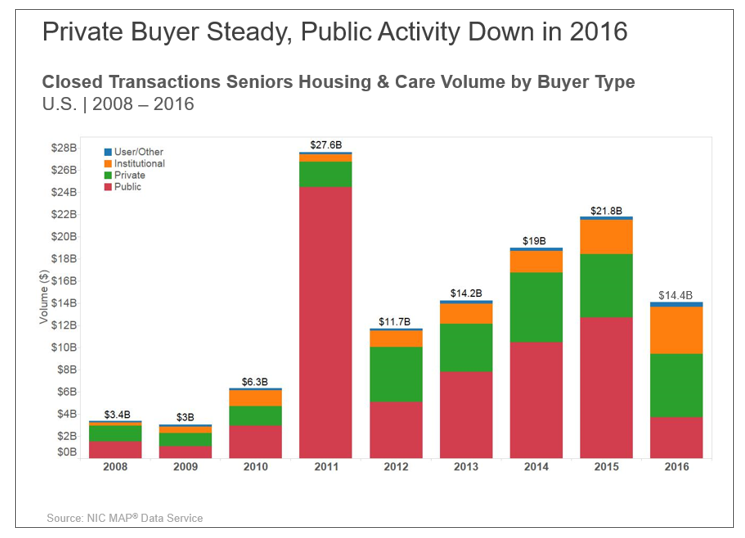

Private Buyer Steady, Public Activity Down in 2016

Over the last few years, the public buyer has been the primary driver of volume in terms of transaction dollars. But in 2016, public buyer volume was down 72% compared to 2015, dropping from $12.7 billion to $3.6 billion. The public buyer represented only 25% of total buyer volume in 2016, compared to 58% in 2015. There are many reasons for the decrease in public buyer activity, including the increasing costs of capital, as stated earlier, and the move by some public REITs to become net sellers. However, the dollar volumes of private and institutional buyers stayed relatively consistent in 2016.

The private buyer type, which includes non-public operators, owners, and partnerships, stayed consistent with $5.9 billion closed in 2016, as strong demand from an acquisition standpoint continued from that group. Private buyers have consistently closed more than $1 billion each quarter, a trend that dates back to the third quarter of 2013. In the fourth quarter of 2016, this group closed $1.1 billion.

The institutional buyer actually increased by 40% from 2015 to 2016, from $3.1 billion to $4.4 billion, as more institutional capital became active over the past year. For example, Formation Capital and Lindsay Goldberg stayed relatively active as buyers.

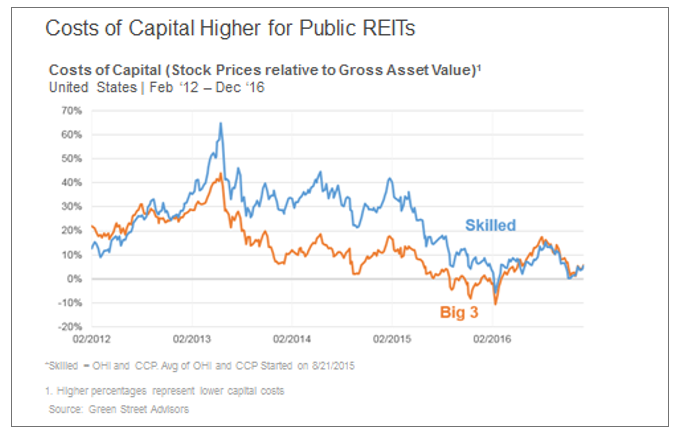

Costs of Capital Higher for Public REITs

As highlighted earlier, one primary reason for the decrease in public buyer volume was the changing cost of the capital landscape. The following Green Street Advisors graph shows the premium at which public REIT stocks were trading relative to their gross asset value, which is based on the private market capitalization rates and the REITs’ portfolio holdings. When REITs trade at a premium to asset value, they can buy properties by raising equity and debt and will get an instant increase in value because the private market value is lower than their publicly-traded equity value. In other words, their costs of capital is low when the premiums are high, and they can make an arbitrage play when these stocks are trading at high premiums.

Starting in 2013, the premiums started to trend down, which in turn effectively raised the REITs’ costs of capital, making it harder to pay up for properties. The premiums fell again in 2015, which was reflected in transactions volume as activity by public REITs started to decrease dramatically after the second quarter of 2015 and continuing through 2016. The premiums dropped at the start of 2016 but bounced back rather quickly; however, the premiums were certainly not anywhere as close to where they had been in 2013 and 2014.

Considering that this cost of capital trend for the public REITs will most likely continue if interest rates rise (both short-term and longer-term rates), it is unlikely that other capital players could make up the difference in terms of dollar volume. However, smaller owner/operators looking to grow, the private and institutional buyers, and possibly international buyers are expected to continue to play a role in the number of transactions, barring any other major capital markets headwinds.

Seniors Housing Price Per Unit Down Year-Over-Year

Seniors housing price per unit ended 2016 at $170,600. It has oscillated around $170,000 to $180,000 for the past couple years. As volume has decreased, the bids for properties has remained relatively strong but decreased from the prior peak of $181,700 in the second quarter of 2015, and has decreased in the latest year-over-year comparison.

The seniors housing price per unit dropped 4% on a year-over-year comparison from $178,500 and dropped 3% from the previous quarter. However, it has increased over 200% from its cyclical low of $58,500 in 2010.

The pricing for nursing care in 2016 saw significant increases in the price per bed. The price per bed for nursing care ended at $95,200 for 2016, which is up 25% from last year’s $76,300. Several high-priced transactions that closed in 2016 contributed to the increase, including the Welltower sale to a Chinese life insurance company and its investment manager, Cindat. The 28 nursing care properties in that transaction traded on average north of the $200,000 price per bed mark. In addition, there have been numerous smaller transactions and one-off transactions trading over $100,000.

There are several reasons for the higher prices for skilled nursing beds. First, interest rates remain relatively low, especially in developed markets around the world. In addition, there have been some properties acquired that have increased the acuity level of patients, which in turn can provide higher cash flow per bed and thereby increase the sale price. Some of these properties have been built out as high-end transitional care businesses. Other buyers are bidding up the price of properties in hopes to increase the Medicare census, which in turn can increase the cash flow at the property as well.

As 2016 marked a major shift in transactions volume activity and much talk about a cyclical peak in pricing for seniors housing, we will need to keep a close eye on the data coming in for 2017 to see if the recent trends continue. Stay tuned for the reporting on the first quarter 2017 data coming in April.

[/expand] [cresta-social-share]

By the Numbers: The Texas Seniors Housing Market

by Beth Mace

As the saying goes, “Everything’s bigger in Texas.” While the state might not host the largest seniors housing market in the country, its busy—and rapidly expanding—metropolitan markets make Texas a big player in the sector.

Population Overview

The NIC MAP® Data Service tracks the performance of the seniors housing sector for six large metropolitan markets (CBSAs) in Texas: Austin, Dallas/Fort Worth, El Paso, Houston, McAllen, and San Antonio. [expand title=”Read More” trigpos=”below” tag=”div” trigclass=”nic-read-more”]

Dallas/Fort Worth and Houston rank as the fourth and fifth largest metropolitan areas in the nation, respectively, with total estimated populations of 7.1 million and 6.7 million people as of 2015. San Antonio ranks as 25th largest, with a population of 2.4 million, while Austin ranks as 33rd, with a population base of 2.0 million. Trailing the pack are McAllen (67th with a population of 842,000) and El Paso (68th with 839,000).

Growth Is Up in Texas

In general, Texas’ larger metropolitan areas are “growth markets.” Indeed, Dallas and Houston were among the largest five fastest growing metropolitan areas between 2010 and 2015. Moreover, of the largest 33 U.S. metropolitan areas, four of the fastest growing between 2010 and 2015 were in Texas: Austin (16.6%), Houston (12.4%), San Antonio (11.3%), and Dallas/Fort Worth (10.5%). Only Orlando grew on par or faster during this period (11.8%).

This context is important, because many of the most rapidly expanding seniors housing markets are also in Texas. Pure growth (both population and employment) in addition to pro-growth attitudes and regulations, land availability, and relatively affordable costs of living and doing business have stoked development in many of the urban areas of Texas.

Inventory and Absorption

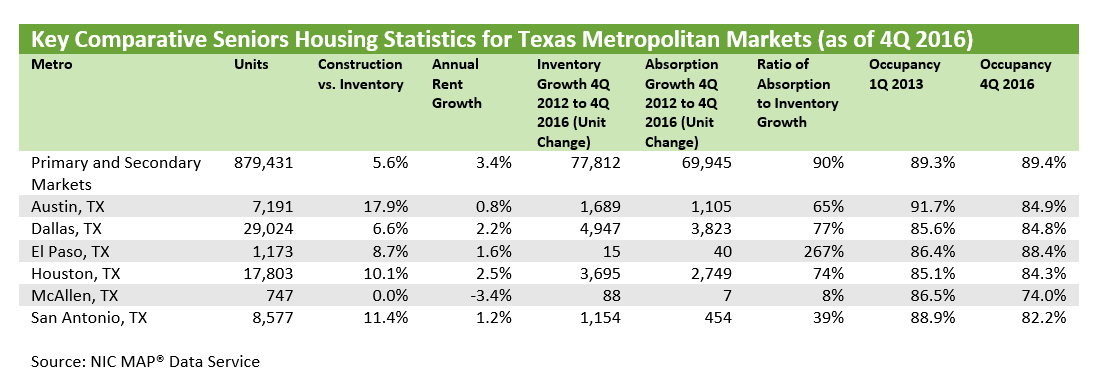

The four largest Texas metropolitan markets represent 7.1% of the largest 99 metropolitan markets’ seniors housing inventory (or 7.3% when McAllen and El Paso are included). Yet these same four markets represented 14.8% of all inventory growth between the end of 2012 and the end of 2016—twice their inventory share (14.9% with McAllen and El Paso). At the same time, however, Texas metropolitan markets also absorbed more than their share of overall net demand, grabbing a lesser, yet still impressive, 11.6% of the largest 99 markets’ net absorption since late 2012.

Since the fourth quarter of 2012, there has been a net inventory change of nearly 78,000 units in the 99 markets, while there has been net demand of nearly 70,000 units. This implies that 90% of the growth in inventory has been absorbed on a net basis. For the six metropolitan markets in Texas, a smaller 71% of the change in inventory has been leased on a net basis. But as the following table shows, there is variation among the Texas markets. For San Antonio, the ratio of absorption relative to inventory growth was only 39%, while for Dallas and Houston, it was 77% and 74%, respectively.

Occupancy Decreasing in Texas

As a result of supply outpacing demand, occupancy rates have decreased in Texas since late 2012. Among the larger four metropolitan markets, the most dramatic drop has occurred in San Antonio, which had an occupancy rate of 88.9% in the first quarter of 2013 which fell to 82.2% by the fourth quarter of 2016. Austin saw its occupancy rate drop by 680 basis points over this same period. By contrast, the NIC MAP primary and secondary markets’ aggregate occupancy increased 10 basis points over this same period.

Because of these weakened market conditions, rent growth has also been restrained. In the year ending in the fourth quarter of 2016, same-store asking rent growth averaged 3.4% for seniors housing in the 99 markets. For all six of the Texas metropolitan markets tracked by NIC MAP, it was less robust; as the previous table shows, rent growth was 0.8% for Austin and 1.2% for San Antonio. Dallas and Houston saw slightly stronger rent growth, although it was only 2.2% and 2.5%, respectively.

In general, Houston has experienced relatively slow economic growth for the last few years due to the sharp drop in oil prices. (West Texas intermediate oil prices fell from $107 per barrel in June 2014 to $29 per barrel in January 2016, and have since risen to $52 in February 2017.) While still positive, annual job growth has decelerated from 4.0% in 2012 to less than 0.5% in 2016 (see the following chart). As the economy has been decelerating, new supply of seniors housing has ramped up, and demand has not been able to keep pace. This has pushed occupancy rates down from 86.9% at the end of 2012 to 84.3% at the end of 2016.

Construction in Texas

Looking ahead, there are roughly currently 49,000 units of seniors housing under construction within the collective 99 primary and secondary markets, representing 5.6% of today’s inventory. This is down slightly from 6.3% in the second quarter of 2016 and reflects the slowdown recently seen in the number of units breaking ground, as measured by construction starts.

Of the current units under construction, roughly 6,100, or 12%, are in the six Texas metropolitan markets, again more than its 7.3% share of the overall 99 markets. In terms of absolute units under construction, Dallas ranks highest with 1,930 units, followed by Houston with 1,800 units.

In terms of units under construction as a share of inventory, Austin ranks highest with 18% of its current inventory under construction—nearly 1,300 units situated within 12 properties. Historically, and for context, it has taken Austin over four years (since mid-2012) to absorb a comparable number of units. It would not be surprising to see Austin’s current occupancy rate of 84.9% (down from 90.4% in mid-2012) drop even lower. That said, Austin’s economy is strong and projected to continue to grow at an above average pace for the next several years, according to projections by Moody’s Analytics. Job growth is expected to stem from technology, professional, consumer, and business services. Strong overall economic growth could support demand for seniors housing.

Another challenge for both incumbent and newly opened properties in Austin as well as other Texas markets may be in finding, building, and maintaining a workforce. As of December 2016, Austin’s unemployment rate was 3.4%, which compares to the national rate of 4.7%. The low unemployment rate reflects labor force expansion in Austin that is twice the pace of the nation. And the labor force expansion in turn reflects the strong population growth referred to earlier in this article.

NIC’s data on current seniors housing construction activity in Texas’ major metropolitan areas suggest that competitive pressures for many of the state’s seniors housing operators will continue to mount. In this environment, it will be critical to have thoughtful strategies about how to maintain market share and a competitive position, and to make realistic assumptions regarding leasing activity, rent growth potential, operations, staffing, and marketing.

[/expand] [cresta-social-share]