What Does the Institutional Investor Want? A Conversation With Blue Moon Capital's Susan Barlow

Susan Barlow

As a long-time adviser to institutional investors, Susan Barlow understands how history repeats itself.

In the late 1980s, Barlow saw pension funds embrace the multifamily sector as an investment property type because of its income-producing potential.

A similar process is playing itself out again with seniors housing. Institutional investors are recognizing the income-producing appeal of seniors housing because it performed relatively well during the recession and has a robust wave of aging baby boomers in its sights.

That context informs Barlow’s work as managing partner and co-founder of Blue Moon Capital Partners, LP. The Boston-based private equity firm matches institutional capital with committed, forward-thinking seniors housing operating companies.

NIC’s chief economist Beth Mace recently spoke with Barlow about Blue Moon’s unique approach and how it’s preparing to meet the dramatic growth in demand for seniors housing over the next decade.

Here’s a recap of their conversation.

Mace: Tell us about yourself and how you became involved in the seniors housing and care industry and co-founding Blue Moon Capital?

Barlow: I started my career as an institutional pension consultant in the days when there was a dramatic shift into real estate. I got a really good sense then of what institutional investors wanted and how real estate was going to play an important role for them going forward.

About five years ago, I met my Blue Moon co-founder Kathryn Sweeney. We had both been working with the public pension fund CalPERS and were invited to speak on a panel at a conference sponsored by Commercial Real Estate Women (CREW) by our mutual CalPERS portfolio manager. That was the first introduction I had to seniors housing when I heard Kathy’s remarks. It seemed clear to me that seniors housing would have a similar appeal as the multifamily sector to investors over time. We kept in touch and decided we would be a good team, and launched Blue Moon in late 2013. We met our capital partner, Hawkeye Partners, in 2014. Hawkeye was also very intrigued with seniors housing and the opportunity for institutional investors. They made a large initial commitment of $175 million, which was later increased to $250 million. We started investing in early 2015. Three years later, we have eight new developments and four acquisitions in our fund, Blue Moon Capital Senior Housing I. We are raising capital for Blue Moon Capital Senior Housing II. We are also fortunate that one of the Hawkeye’s investors, a large public pension fund, has selected us to create a separate seniors housing account for them.

Mace: Why is that important?

Barlow: The pension fund considers this seniors housing account to be a core, income-producing investment. Seniors housing has traditionally not been considered a core investment. It is typically further out on risk spectrum, in the value-add or opportunistic category.

Mace: Can you tell us more about your investors?

Barlow: Hawkeye has seven institutional investors inside its Scout Fund II. The investors are large institutions that might otherwise have a difficult time directly accessing the seniors housing market. Those seven investors are candidates to invest directly with us after they have invested through the Scout Fund. It’s a great door opener for us into the institutional world.

Mace: Seniors housing in 2018 reminds you of the multifamily market of the late 1980s. What are the similarities?

Barlow: There’s an opportunity for institutional investors to grab on to seniors housing like they did with apartments in the late 1980s. As I mentioned, seniors housing is a way to produce income, act as a guardrail during a downturn, and enjoy the upside of an aging population. Recent polling of institutional investors shows seniors housing as a top interest of theirs. (For Institutional Real Estate Inc./Kingsley Associates study click here, and for ULI/PwC Emerging Trends study click here).

Mace: Blue Moon is a fairly new company. What are some of the largest challenges you’ve faced? Any successes you’d like to share or lessons learned?

Barlow: Our goal and our mission is to match institutional capital with leading operators. It’s been important from the beginning to have the right kind of collaborative culture to develop a relationship with operators. We want to be partners with our operators. Kevin Donahue joined us with over 11 years of experience with a highly regarded operator. Chris Kronenberger has a strong institutional background. We’ve made a commitment to get the culture right.

Mace: Why would an operator choose Blue Moon over another private equity group?

Barlow: Capital is somewhat of a commodity. What’s different about Blue Moon is that we are 100 percent focused on the sector. We live by the old adage: an inch wide and a mile deep. We think about seniors housing all day, every day. And it’s the same with our operating partners. We offer capital backed by a strategic and knowledgeable approach.

Mace: How do you choose an operating partner? Or why would an operating partner choose you?

Barlow: We have seven operating partners in our existing portfolio. They range from fairly newly formed from other operating platforms to some of the largest in the industry. We are looking for groups that are committed to the seniors housing sector, and committed to best practices from an organizational standpoint. They must have track records at a current operating platform or within a prior company. We also look for an alignment of interest through capital and heart strings as well.

We do ground-up development and our operators identify development opportunities in line with their business model. Our operators are typically vertically integrated, and have been successful developing and operating their own communities.

Mace: Do you also invest in existing properties?

Barlow: Yes, we do acquisitions. We like to partner on investments where the property is important to the firm. We have a couple of assets that are considered the operators’ flagship properties. We love that. We like the community where the operator’s friends and family are residents, or the headquarters of the company is nearby. The operator has to have more than a financial connection.

Mace: Have you turned down deals? What are the red flags that make you walk away from a deal?

Barlow: We’ve turned down a lot of deals. Often, it’s someone without experience in seniors housing, who’s coming from another property sector. We’re looking for partners with a proven track record in seniors housing that are making a long-term commitment to the operating aspect of the industry. They’re not just looking for a real estate deal.

Mace: Do you provide private equity to all seniors housing segments? Independent living, assisted living, and memory care? Is there one segment or a particular geography that you prefer?

Barlow: We invest in independent, assisted and memory care. They are all private pay and rental. We acquired one investment with a small percentage of skilled nursing, but we typically are not in the skilled area. We have not done senior apartments as we like the care component.

Mace: How do you choose locations?

Barlow: We are national and prefer the 31 NIC MAP® Primary Markets.

Mace: Why big markets?

Barlow: We like the depth and breadth of the top 31 markets—at least for now. We may consider Secondary Markets in the future.

Mace: Do you fund expansions?

Barlow: Yes, we like those.

Mace: Our NIC Spring Investment Forum discussed the shift among operators to add ancillary businesses such as home health. Do you provide private equity for the operations of a seniors housing business?

Barlow: We have not provided private equity for operations, but we are watching that trend very closely.

Mace: What kind of returns do you expect?

Barlow: We look for market returns similar to the mid-teen expectation of a value-add fund.

Mace: Are all your deals joint ventures?

Barlow: Yes, to date they have been. We’re seeking alignment and feel strongly that partnering with an operating company helps achieve that goal. We do not buy an asset and bring in a third party property manager. That is not our approach. Although one group we work with includes a third party operator and a developer that does deals together. But this operator has a 20-30 year history operating as a third party and has an outstanding track record.

Mace: What is your hold period?

Barlow: We think matching institutional investors with operating partners in a long-term strategy makes a lot of sense. It avoids the disruption of recapitalizations for the operator and meets the goals of the institutional investor.

Mace: Sometimes operators prefer a public REIT because it is perceived as having a longer hold period than private equity. What are the advantages of Blue Moon over a public REIT?

Barlow: I think the finite life, private equity vehicle makes sense during the development phase for value creation. There’s a beginning and end to that phase, and it allows investors and operators to be paid for that value. A long-term private vehicle can make sense during the operating phase, and I think there’s room for both public and private alternatives.

Mace: Seniors housing is facing challenges related to supply, a labor shortage, and rising costs. How do you think about that?

Barlow: We are a women-owned business which is a plus because a big segment of the seniors housing market is targeted at adult daughters like us. We spend a lot of time thinking about how to meet their needs. We also think about the labor situation and how to meet the coming demand from the baby boomers. We’ll need a middle market product in the future which will be different from what we have been developing.

Mace: Any worries that keep you up?

Barlow: We want to invest in a responsible way. It’s so important on behalf of all the stakeholders—residents, investors, and operating partners. The standard we deliver is our best. This isn’t like an industrial building where if you forget something here or there, it may not matter. We take the mission aspect of seniors housing very seriously.

Mace: You’re buying at a time when interest rates are rising and cost of capital is rising which impact cap rates and valuations. Are you underwriting differently today than two years ago considering the broader capital or economic environment?

Barlow: We are underwriting differently because cap rates and interest rates have changed. But we are not in the zone where we have concerns yet.

Mace: Any other thoughts?

Barlow: With the forecast for growing demand, we wonder if we will have enough operators. There seems to be a need for more high quality operators. Many operators are going through succession planning or thinking about that. Will there be enough skilled operators to handle the demand?

Mace: How are you responding to that?

Barlow: If someone calls with a new platform, we always take a look to see who it is and what is driving their business model. Two of our seven operators are new. We look for other approaches and models. But we always make sure they are making a commitment to seniors housing.

AI, Robots, Smart Apps and Senior Care – the Future is Near Tech Expert Vivek Wadhwa to Speak at 2018 NIC Fall Conference

Vivek Wadhwa

Global tech entrepreneur, author, academic and advocate, Vivek Wadhwa, will be the 2018 NIC Fall Conference luncheon speaker. Wadhwa will focus his presentation on the practical solutions that new technological advances will make possible in the near future. The concept of robots disrupting seniors housing and care, or artificial intelligence and healthcare apps improving property performance may sound like science fiction today, but, according to Wadhwa, the tech innovations that will change the industry are just around the corner.

For those interested in how tech solutions will impact the way they do business, Vivek Wadhwa’s presentation will be thought-provoking and insightful. A Distinguished Fellow at Harvard Law School’s Labor and Worklife Program, and a, Distinguished Fellow at Carnegie Mellon University’s College of Engineering, he is a globally syndicated columnist for The Washington Post and author of several books: “The Driver in the Driverless Car: How Our Technology Choices Will Create the Future”; “The Immigrant Exodus: Why America Is Losing the Global Race to Capture Entrepreneurial Talent”—named by The Economist as a Book of the Year of 2012; “Innovating Women: The Changing Face of Technology”—a documentation of the struggles and triumphs of women, and the latest “Your Happiness Was Hacked: Why Tech is Winning the Battle to Control Your Brain—and How to Fight Back.” Wadhwa has held appointments at Duke University, Stanford Law School, Emory University, and Singularity University.

In the coming days, NIC will announce our opening general session speaker, a highly sought-after global figure, who will complement Wadhwa’s presentation, and reflect the conference theme, with a conversation on the U.S. and global economic landscape.

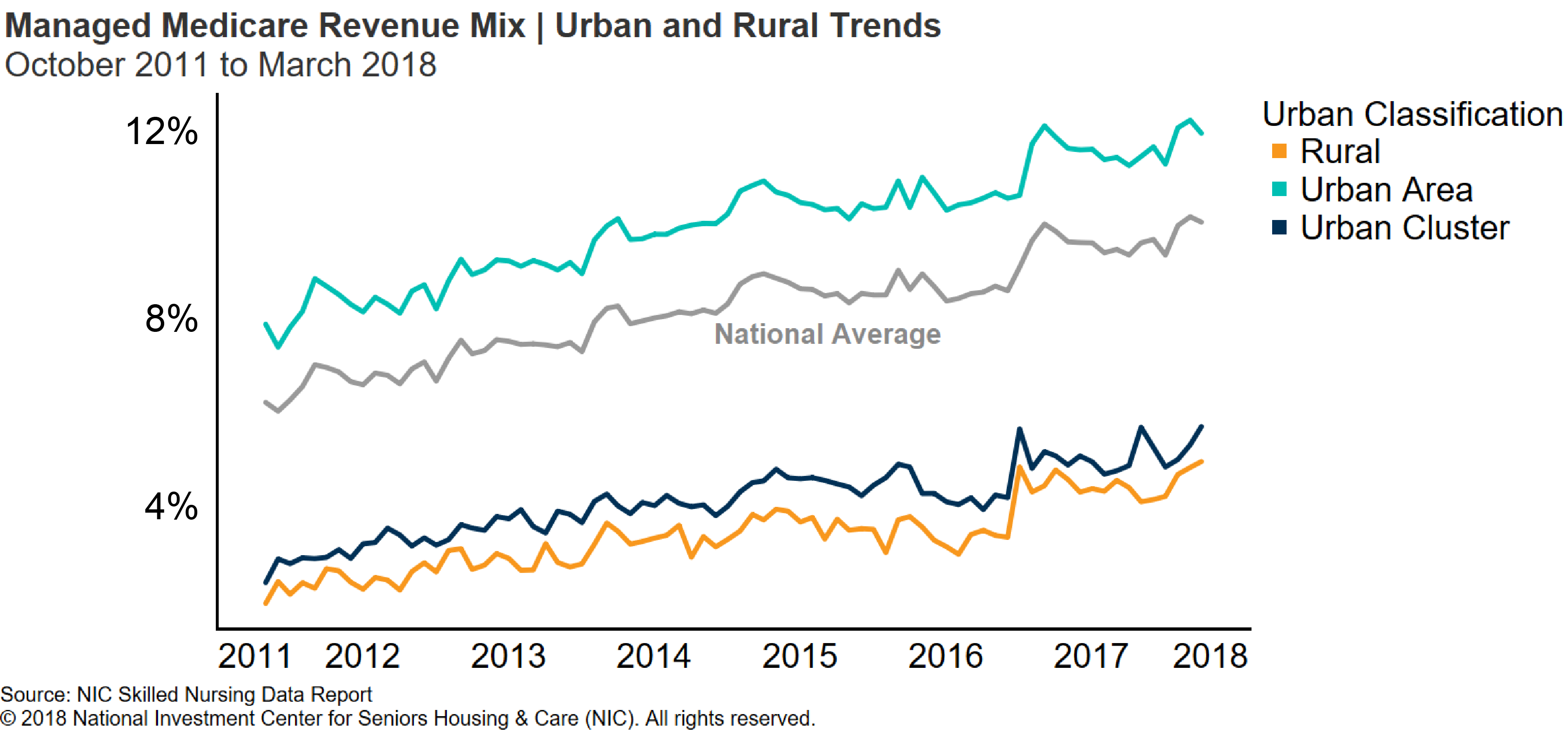

Inside NIC's New Urban and Rural Skilled Nursing Trends

Key Takeaways from the Urban and Rural Skilled Nursing Data:

- Quality mix was about even in all geographic settings until 2015, when it began to increase in rural areas and decrease in urban areas. Today, a large difference exists between the two settings.

- Managed Medicare is more prominent in urban properties than rural properties.

- Private pay for skilled nursing is more prominent in rural areas compared to urban areas.

Liz Liberman

As part of NIC’s commitment to increasing transparency in the seniors housing and care continuum, NIC rolled out two new data perspectives on the skilled nursing sector in 2018. Last May, NIC added to its NIC MAP® Data Service quality metrics at the property level, including metropolitan-level benchmarking powered by our strategic alliance with PointRight. This year NIC also expanded its Skilled Nursing Data Report to include revenue mix as well as urban and rural trends.

Those familiar with NIC’s data offerings know that metropolitan-level data is often among our objectives; however, in the skilled nursing sector, considerable differences exist not only among metropolitan areas, but also between urban and rural geographies. Indeed, one benefit of the Skilled Nursing Data Report is that coverage is national, and therefore includes rural properties, enabling such a comparison.

Consumers of NIC data have long requested additional data comparing these urban and rural geographies, under the assumption that the business case in either setting may be different. As the NIC Board’s Vice Chair, Kurt Read, said, “There appear to be material differences between urban operations and rural operations, and before now, you just had to look at a portfolio or a specific property example.” Now that NIC has expanded the Skilled Nursing Data Report to include urban and rural trends, investors and operators have additional data-driven insight into the sector to make informed decisions.

The Skilled Nursing Data Report at a Glance

Driven largely by the role of government in the skilled nursing sector, this segment is in a period of dynamic change. Policies at both the state and national level, usually geared toward lowering government spending, impact the market for skilled nursing. For investors and operators in the sector, data is key to mitigating the uncertainty associated with policy changes that may directly impact operational revenue. New players in the post-acute care space such as home health and home care, as well as the growth in assisted living, bring additional competition to this market. Investors have few available data resources to understand the market. Meanwhile, changes in demographics and technology suggest that the skilled nursing space is in need of capital to update or replace older buildings and to improve the services available to a patient population with increasingly higher medical needs. Considering NIC’s role as an independent arbiter of data and its history of successfully aggregating data directly from seniors housing providers to bring key metrics to the investment community, we found an opportunity to educate capital on the skilled nursing space by filling an important data gap.

The Skilled Nursing Data Report fills that gap. Through this initiative NIC collects data on a few fundamental metrics that can provide insight into the skilled nursing market—the data points investors need to make educated business decisions and to lower barriers of entry into the space. This data set represents over six years’ worth of data collected directly from a diverse group of skilled nursing operators. Occupancy and revenue data, trended over time, are made available to the public and NIC MAP subscribers quarterly in an effort to boost transparency in the sector. As of March 2018 and updated in June 2018, the report now includes the urban-versus-rural perspective sought after by skilled nursing operators and investors.

Initial Takeaways from Urban and Rural Expansion

An initial finding from the expansion of the urban and rural perspective in the report is how managed Medicare, or Medicare Advantage, differs among geographic settings. A small percentage of skilled nursing residents are covered by this program that resembles private insurance for Medicare beneficiaries. The trends in managed Medicare are important to monitor because they impact margins (typically lower than traditional Medicare) and business strategy, which demands providers be willing and able to find and accommodate partners to gain market share.

The conversation around managed Medicare in skilled nursing business strategy is a “hot topic” these days, but often fails to take into account that managed Medicare is practically negligible in urban cluster and rural areas (see the full report for the Census Bureau definition of each geographic setting). NIC’s data demonstrates just how small a role managed Medicare plays in rural areas, under 5% of revenue mix, compared to urban areas where the revenue share is much higher and growing at a faster rate. One theory driving this difference is that managed Medicare needs an abundance of providers to be successful because the program is based on creating preferred provider networks, which is more difficult to achieve in rural areas.

Another difference the new report illuminates is in quality mix, which represents patient days attributable to Medicare, managed Medicare, private, and other payor types (all but Medicaid patient days). Quality mix is an important metric to track because it represents the payor types that provide the highest daily reimbursement rates, while Medicaid is the lowest daily reimbursement payor and only represents long-term residents. Quality mix includes a mix of both short-term patients and long-term residents; short-term patients receiving rehabilitation following a hospital stay often require high-value care, but also represent higher daily reimbursement amounts.

The urban vs. rural trends started to diverge considerably in the first quarter 2016, when the range between the highest percentage (rural) and the lowest percentage (urban area) was just under 200 basis points. As of the first quarter 2018, two years later, rural properties show approximately 40% of patient days in the quality mix while urban area properties show only around 32%, a difference of almost 800 basis points. These differences are driven in part by Medicaid and private patient day mix. For urban area properties, Medicaid patient day mix grew considerably during this period, while it decreased for rural properties. Meanwhile, for rural properties, private patient day mix has been much higher compared to urban properties throughout the six-year series. Like urban area properties, private patient day mix decreased slightly over time for rural properties. However, at 16% in rural areas compared to just 6% of patient days in urban area properties, private pay in skilled nursing continues to drive higher quality mix for rural properties.

Future of the Skilled Nursing Data Report

While NIC’s addition of urban and rural trends fills an important gap in data resources for skilled nursing stakeholders, opportunities for further transparency exist. Firstly, the data demonstrates that what investors have thought intuitively is true—difference in revenue and occupancy trends exist based on geographic setting. The data does not provide conclusive evidence as to the main drivers of these differences. While we can theorize about how competition, government policies, demographics, and technology play a role in driving such changes in different ways in these settings, more data is needed to understand these drivers. Secondly, these revenue and occupancy trends, while valuable at the national level, will be even more insightful at the state level. NIC is actively recruiting additional volunteer operators to contribute data to this initiative so that state-level data can be made available. The more data we collect, the more transparency we can deliver, but we cannot do it alone. If you are a skilled nursing operator, please consider participating in this important initiative that will help to inform capital in the sector. If you work with operators, please consider encouraging them to participate. To learn more about participation, click here.

Facing Three Big Challenges, the U.K. Senior Living Market Could Follow the U.S. Roadmap to Success

Elyse Hanson

Sarah Peerson

In this article, NIC Future Leaders Council Members, Sarah Peerson, vice president, seniors housing finance group, Wells Fargo, and Elyse Hanson, director, investments, Blue Moon Capital Partners LP, explore three challenges facing today’s U.K. seniors housing market, which is somewhat comparable to the U.S. seniors housing market of the mid- 1980s/early 90s. Of note, while seniors housing in the U.S. is a catchall term for several different product categories, retirement villages in the U.K. are equivalent to our independent living, and care homes in the U.K. refer to assisted living and memory care.

Favorable seniors demographics coupled with longer life expectancy, fewer family caregivers, and a steady housing market are creating the opportunity for the U.K. seniors housing private pay sector to become a mainstream investment class. But the opportunity does not come without its challenges.

The first challenge is that the permitting process in the U.K. is extremely arduous—and that’s for the projects that are lucky enough to make it through the process at all. There is some anecdotal evidence that local planning commissions are becoming more amenable to this product type. New product is difficult to build, and 83% of the existing stock was built prior to the year 2000. These older buildings are typically non-purpose built or government-funded developments that offer few amenities. The existing stock of care homes is quickly growing obsolete, and it is likely that some will not meet regulations in the coming years and be forced to close.

With that said, the addition of purpose-built care homes with attractive amenities could have the effect of increasing the penetration rate in the U.K. Currently, penetration rates are only about 1/10th of the rate as in the U.S. The low penetration rate is partly due to a culture that values having a home of one’s own. However, investors who are currently developing seniors housing in the U.K. hope that once high-quality product is available, more seniors will find it appealing enough to move out of their homes. Similar to the U.S., the population in the U.K. is aging, with seniors making up a larger percentage of the populace each year. By 2026, it’s estimated that the number of 65+ individuals will account for 20% of the U.K.’s population. The U.S. is not expected to hit this milestone until 2030. The rapidly aging population, coupled with the potential to increase penetration rates, presents a compelling opportunity for the seniors housing market in the U.K.

The second big challenge is that the majority of the U.K. care home market today is government subsidized. The accountancy and advisory firm of Moore Stephens reported that 12% of care homes in the U.K. are at risk of becoming insolvent over the next three years.i Among the causes are rising operating costs and the introduction of the National Living Wage, an obligatory minimum wage for U.K. workers.

More importantly, cuts to government funding have decreased by about £4.6 billion over the past five years, representing about 31% of the overall budget.i This insolvency issue has led providers to look towards private funding, therefore increasing the proportion of privately-funded residents, and/or to seek ‘top up’ payments from residents or their families to subsidize government funding. Statistically, strong demand exists for the private pay product given the aging seniors population who are benefiting from accumulated wealth from house price appreciation and pension growth. However, as noted, it is met with a small supply of care homes which are sub-standard, leading to a lack of interest from potential residents.

Lastly, the U.K. currently lacks available information and statistics which help to educate investors, developers and operators, providing confidence for them to invest in the space. Growth in U.S. seniors housing and care over the last 35 years can be attributed to the improved availability of research and data provided by the National Investment Center for Seniors Housing & Care (NIC), the American Health Care Association (AHCA), the American Seniors Housing Association (ASHA), Argentum and others.

“NIC has been credited with bringing the industry to the forefront of becoming an investment class here in the U.S. by having successfully provided seniors housing data and analytics, and therein transparency to advance the industry,” states Dr. Margaret Wylde, CEO of ProMatura Group. A strong U.K. care home organization is eventually expected to emerge to advance the sector and unite owners, operators, developers, capital providers, researchers, public policy analysts and others. One such candidate is the Associated Retirement Community Operators (ARCO), formed in 2012 with the aim to promote confidence in the sector, raise awareness of the retirement community model among older people and stakeholders alike, and increase the volume and quality of expertise within the sector.

Looking ahead, while the market for seniors housing in the U.K. faces many challenges, the sector’s experience in the U.S. provides a roadmap for how some, if not all, of those challenges can be overcome. There are already indications that the industry is on the cusp of maturation.

Institutional investors have deployed a considerable amount of funds. Welltower, for example, closed on their initial acquisition of Signature Senior Lifestyle in 2012 and has since completed $679 million of additional investments and financings with Signature.ii In addition, as mentioned previously, ARCO could become the industry organization that is able to provide the transparency that will help attract more capital to the sector. This, along with the underlying favorable demographics, a low amount of quality care beds, and a strong push towards developing a quality product that appeals to the private pay resident, further advance the case of seniors housing in the U.K. to become a more mainstream investment opportunity in the near future.

References

i DLA Piper: Key issues facing the UK residential care home sector

ii Welltower 2018 Q1 earnings release