A Note From Brian Jurutka

During these unprecedented times, our deepest concerns go out to those directly impacted by the COVID-19 pandemic and those on the frontline keeping residents of seniors housing and skilled nursing communities safe. We understand that seniors housing and skilled nursing operators are bearing tremendous burdens, and NIC applauds your efforts to protect and serve residents of seniors housing and skilled nursing communities.

NIC will help you stay informed and understand trends in these rapidly changing times by doing what we do best − delivering data, analytics, and connections – to provide transparency to the sector.

To that end, NIC is launching initiatives to offer insights during the uncertainty. These include:

- Leadership Huddle Webinar Series: Bringing together experts to offer timely perspectives from across the sector with a focus on the intersection between capital providers and operators of seniors housing and care. Please click here to be notified of the next webinar.

- Executive Survey Insights: Creating an important benchmark, released weekly, on the impact of the COVID-19 pandemic on key metrics − including occupancy rates − that will allow the market to be better informed.

- Leadership braindate™: Facilitating virtual knowledge-sharing meetings among sector participants. Complimentary access to the braindate online platform is available here.

- NIC MAP® Data Delivered Monthly: We’re working to produce certain NIC MAP three-month rolling data on a monthly basis, beginning with the period ending April and delivered in May, to explain trends in the market, while also working to subsequently make the data available in the NIC MAP interface.

NIC joins the industry in supporting prioritization of frontline healthcare workers’ needs as they protect and serve our most vulnerable citizens, older Americans. The challenges ahead of us can only be solved if frontline healthcare workers receive the support they need.

We wish you well during these challenging times.

Brian Jurutka

President & CEO

Leadership Huddle Webinar: The Impact of a Crisis on Seniors Housing and Care

Amid the COVID-19 pandemic, a historic stock market crash, record stimulus spending, and immediately on the heels of a shocking, record-smashing spike in unemployment insurance claims, NIC convened a virtual panel of industry experts for a webinar on March 26th, to assess the impact on the seniors housing and care industry.

NIC Chief Economist Beth Mace began her remarks by saying, “There may be more fog and clouds than sunshine and clarity in my comments today.” She was addressing a virtual audience of 1,863 seniors housing and care industry leaders in the first of a new series of “Leadership Huddle” webinars produced by NIC. Confirming fears that the COVID-19 pandemic would heavily impact the economy, the Department of Labor had just reported that 3,283,000 Americans filed for unemployment insurance benefits the previous week – shattering records. As Mace pointed out in a NIC Notes blog post that morning, the weekly report is among the first economic indicators to show the effects of the virus on the economy.

Titled “COVID-19, Financial Market Uncertainty, and the Impact on Seniors Housing & Skilled Nursing,” the webinar kicked off with Mace’s review of the “new norm,” in which, she said, “shops and stores are being shuttered, entertainment venues closed, and those who can conduct their jobs remotely are working from home, while many of those who cannot are being furloughed and laid off.” After concluding her assessment of this moment in economic history with the statement, “In just a flash, the great American job machine does appear to have ground to a halt as a result of the pandemic,” Mace went on to express support for the seniors housing and care industry’s frontline healthcare workers, many of whom, she pointed out, are working around the clock to ensure the safety of seniors housing residents.

Mace took a moment to point out that NIC is supporting initiatives in the seniors housing, skilled nursing, and healthcare sectors, to ensure these workers get the support they need and deserve. These include the prioritizing of frontline staff for personal protective equipment (PPE), immediate, no-hassle access to COVID-19 testing, and improved support, such as child-care assistance, so that these essential workers can focus on their jobs. A joint statement outlining these needs was released on April 1 by NIC in partnership with leading industry groups AHCA/NCAL, Argentum, ASHA, and Leading Age.

She then went on to summarize results from an Activated Insights survey conducted March 18-19. Approximately 1,100 properties, representing 100,000 units, were surveyed. 79% of these operators reported no significant difference in occupancy or move-outs at the time of the survey in mid-March. And 21% actually reported an increase in occupancy. This was attributed by some operators to families realizing they were now less able to care for their elderly or disabled loved ones at home. Mace then announced that NIC is launching its own survey of operators called the Executive Survey Insights, tracking move-ins, move-outs, occupancy patterns, staffing solutions, and development trends, saying, “Bringing transparency to the industry on important metrics is what NIC is really good at, and we will be sharing our results with you in the coming weeks.”

Each member of NIC’s panel represented components of the financial services industry. First to present was Jim Costello, senior vice president of Real Capital Analytics (RCA). Costello provided an overview of the performance of the seniors housing sector, relative to other commercial real estate types, such as hotels and industrial properties. The seniors housing sector has been performing so well for investors that it actually surpassed the hotel sector in terms of deal volume in February, 2020. Pointing to recent analysis of the sector, Costello said, “While we go into this crisis with a lot of unknowns…we do know that, going in, it was still in a healthy state, and investors were still interested.”

Costello’s presentation indicated that commercial real estate does not always behave the same way from one recession to the next. Pointing to the corporate bond market, where spreads have “exploded,” Costello similarly sees tolerance for risk eroding and cap rates potentially going up. Lenders “are going to be hesitant for some time,” he cautioned. With prices falling in public equity markets, and a lack of further information, Costello cautioned investors not to simply look at equity markets to “infer something about asset prices.” Instead, he said, “I think you have to take it with a grain of salt in looking at the fundamental health of the sector…at least going into the downturn, the seniors housing and care sector was strong. It had deal momentum and investors interested in it.”

Matthew Ruark, senior vice president, head of commercial and healthcare mortgage production, KeyBank Real Estate Capital, and NIC Board member, discussed the situation from the perspective of a lender in the market. Importantly, Ruark stated that there is still financing available, “but the volatility, even since the NIC Spring (Conference in early March), has changed the landscape for sure.” Ruark reviewed indicators such as the 100 basis-point move in the 10-year Treasury, the major drop in the LIBOR rate, significant increases in Fannie Mae investor spreads, and historic shifts in the corporate bond markets. He pointed out that the Federal Reserve has already pumped in as much liquidity as it did during the entire Great Recession. Given the uncertainty that he’s seeing, he said, “it’s understandable why investors and lenders may be more cautious as they think about acquisition prices or loan structures for seniors housing.” He closed his remarks with the statement that, “There is capital out there…but a more limited supply, and not nearly as aggressive as six months ago.”

Middle-market lender Kevin McMeen, president, real estate, MidCap Financial Services and former NIC Board chair, said, “None of us really have any idea of exactly how this (the pandemic and the economic fallout) will play out.” He emphasized how difficult it is to forecast the future of the seniors housing sector at this stage in the crisis, and that his organization would be sitting on the sidelines. He said, “Once we have some level of clarity and can have some foresight, that’s when we’ll look at getting back into originating new business, but until then our focus is on our portfolio and supporting our existing customers.”

Kurt Read, principal at RSF Partners, and long-time NIC Board member and current chair, is also shifting focus from new business to managing existing accounts and relationships. He said RSF Partners is communicating more frequently with its investors, operators, and lenders. “At times like these, what you need to look at first is what are the liquidity needs of all of your assets and relationships.”

Read emphasized the value of information sharing, particularly during times of crisis, to investors and the industry because, “whatever is going on right now will come out in the future, and those who are transparent and forthright in communicating what is going on will be viewed favorably once we get through the crisis that we’re in now.”

Read also expressed concern over the economic impact that the financial crisis will have on capital markets but pointed out that the sector has advantages over other commercial real estate property types. “Seniors housing and care…has a real foundation underneath it that a lot of other property types in real estate don’t have. And that is access to Fannie Mae, Freddie Mac, and HUD lending sources.”

Mace agreed that the sector has some advantages over other commercial real estate property types. During the last recession, she said, “seniors housing was a ‘recession resilient’ sector. It wasn’t completely resistant…occupancy rates did go down, but assisted living performed better than did independent living, for example, because assisted living is more needs-based. And asking rates did not go negative in the seniors housing sector, unlike the other property types. She also pointed to NCREIF data on private investor returns, which shows the sector took “less of a hit” than other property types.

The pandemic is also impacting the ability to transact deals on a logistical level. According to Ruark, “there’s no doubt that the logistics…have gotten more difficult.” Travel restrictions, limited access to properties, and government office closures are creating hurdles in the due diligence process, in some cases making it impossible to conduct title searches, or record mortgages. Although people are continuing to try to close deals, Ruark said, “The important thing to remember is things will take more time.”

NIC Chief Operating Officer Chuck Harry posed several questions, submitted in real-time by webinar attendees, to the panel. Asked about changes in the lending landscape, panelist Ruark indicated that prices are already going to be higher, and leverage lower, while lending activity will most likely be for existing customers.

When asked how these changes would impact new development, Read responded, “I would expect material disruption in the ability…to agree on land value, to get a construction loan, to underwrite a budget, and provide investors with the correct risk-adjusted return; so, yes, I think it is pretty clear anytime we have these disruptions, development activity is one of the first casualties.”

Another audience question, which Harry posed to the panel, was what economic or market indicators would suggest that the crisis might be ending. Mace answered that she’d be looking more frequently at occupancy rates, move-in and move-out rates, the spread of COVID-19, and broader economic factors, noting that the $2 trillion stimulus package that just passed the senate, “wouldn’t take out all of the sting – but would take out some of the sting.” Costello said he’d be looking at the corporate bond rate and spreads, “A daily indicator of how risk-averse people are.” Ruark, answering the same question, added, “I’m watching the 10-year treasury; I’m watching investor spreads to see if things settle down.”

As the webinar came to a close, panelists summarized their outlook and concerns at this stage in the crisis, and reminded attendees that the sector has unique strengths, as well as risks. In his summary, Read emphasized that the seniors housing industry remains open and operating, while others are being forced to shut down. He also pointed to the impact of the end of low unemployment: “If you’re an employee at a senior living facility, and you’re getting paid, doing very meaningful work, and you look around and there are millions of unemployed people in America, that will look like a pretty good position.”

Read summarized his view by reemphasizing the need for the industry to continue to be transparent, saying, “We need to increase the transparency during a time of stress and not decrease it. I know people want to hold on to information, and only release good information, because they’re afraid that any negative information will be bad.” He went on, “That information will come out. It’s better to be transparent today, and to provide insight into what’s going on. That’ll help us all in the long term.”

Thoughts from NIC’s Chief Economist

By Beth Burnham Mace

It’s the end of the world as we know it…and, no, unlike the lyric in the R.E.M song, I am not feeling fine…And let me add that there may be more fog and clouds than sunshine in many of my comments below.

As we all know, there is great uncertainty in the world today related to the breadth and depth of epidemiological causes and spread of the COVID-19 pandemic across the globe and within the United States. We do know that many of our fellow citizens are getting ill, and some are dying, and that the illness is more severe for our seniors. NIC is extremely concerned by the public health challenge facing all of us and, in particular, older Americans. During this unprecedented global public health emergency, we offer our support to owners and operators of seniors housing and skilled nursing properties nationwide, and our fullest admiration to the healthcare personnel working around the clock to ensure the safety of their residents. The challenges ahead of us can only be met if these frontline healthcare workers receive the support they need as they fight to protect and serve our most vulnerable citizens – older Americans.

That is why NIC supports initiatives in the seniors housing, skilled nursing, and healthcare sectors to ensure healthcare workers get the support they need and deserve. These initiatives include:

- First, governmental authorities need to give staff of senior care and long-term care communities priority access to personal protective equipment such as face masks and shields. These communities are a critical part of the healthcare continuum.

- Second, frontline workers in skilled nursing and assisted living also need immediate, no-hassle access to COVID-19 testing in order to keep them safe and stop potential spread of the virus.

- And third, employers need access to better solutions that enable these essential workers to go to work – where their skills are badly needed – without having to be worried about care for their children. About two-thirds of paid caregivers return home to care for children or an elderly family member. Mandatory paid sick leave to help when schools are closed due to COVID-19 is not helpful right now. With that in mind, some employers have stepped up, offering day care cooperatives or per diem babysitting stipends to provide much-needed backup support. Some employers are providing bagged lunches to caregivers to ensure their kids stay well fed. Paid sick leave for those concerned that they may have been exposed to coronavirus is also essential – and employers hope to see Federal action very soon.

Six Areas of Impact. The COVID-19 pandemic has implications for operators, developers, and capital providers across the seniors housing and skilled nursing sectors. I have identified six areas of likely industry impact.

-

- Residents and Health Care Workers. First is the impact COVID-19 is having on our citizens, residents and staff across the country and the high risk of contagion. At the national, state and local level, the numbers change daily and appear to be growing asymptotically. However, the specific impact on the seniors housing and care sector is less clear. Since early March, operators have implemented strict protocols to prevent and limit the spread of the illness across properties. Extra cleaning and contact prevention protocols, limitations on visits, restrictions on group activities, travel restrictions and other rules have been implemented. Thus far, there have been a limited number of properties with infections.Staffing is another issue and, as addressed in my earlier comments, is the most critical part of keeping our residents safe and out of harms way. Safety protocols, flexible schedules, accommodations to the new reality of social distancing rules with school closures, contingency planning for staffing emergencies, and other planning protocols are part of the solution and should be lauded.

- Operations. Second is operations and the impact COVID-19 is having on move-in and move-out rates and occupancy patterns. At this point, there is a lot of speculation and hearsay. Building on its strengths, NIC is therefore launching a new monthly survey to address this need for information. The “Executive Survey” will question operators about move-ins and move-outs, changes in occupancy rates, staffing considerations and construction delivery pipelines.

- Economic Impacts. Third, the economic effects of the COVID-19 pandemic are unprecedented and may ultimately herald back to the days of the Great Depression in the 1930s. What was once unthinkable is now occurring. Quarantines and limited social interaction are becoming the norm, shops and stores are being shuttered, entertainment venues closed, and those who can conduct their jobs remotely are working from home, while those who cannot are losing their jobs and paychecks. As a result, jobless numbers are on the rise, those claiming unemployment insurance are projected to total more than 3 million in a matter of weeks, and the unemployment rate will soon jump from its 50-year low of 3.5% in January 2020. Consumer spending, which accounts for two-thirds of the nation’s overall GDP, is being battered. The prospects for negative growth and recession are now upon us. While the short-term impacts are indeed dire, economists are mixed on the long-term impacts of COVID-19 on the economy with discussions on supply-chain disruptions, globalization trends, and business confidence weighing heavily on these views.

- Financial Markets. Credit makes the economy spin. Without credit, the economy would grind to a halt. For the last several weeks, we have witnessed the Federal Reserve provide a full-throttle effort at keeping the credit markets open, functioning, and operational. In mid-March, the Fed dropped the fed funds rate back to its 2008/2009 recession low of 0%, implemented another and aggressive round of Quantitative Easing (QE), lowered the discount rate, cut reserve requirements, and implemented new credit facilities. In effect, the Fed is doing all within its power to keep credit flowing.For banks and lenders, capital providers, both public and private, the world has shifted. The cost of capital has changed, terms are changing, and loan proceeds are being re-assessed. Debt financing may be tougher to come by. NIC will be holding “Leadership Huddles,” with the first focused on financial markets. This series of webinars will feature C-suite industry leaders’ insights on the impact of COVID-19 on operations, financing, construction trends, capital markets, transaction markets, pricing and more.

- Transactions and Pricing. For many markets, including some in the commercial real estate realm, transactions activity has ground to a screeching halt as a new world order is being called into play. Questions on valuations, comps, and the competitive landscape are emerging. The drop in stock prices for many of the public health care REITS has highlighted concerns about underlying asset values, and this is bleeding over into the private sector valuations as well.As in the Great Financial Crisis (GFC), distressed assets may grow as operational risks unfold, opening up a market for some of investing in distressed assets.

- Construction. What has long been a challenge for existing operators may be less so in the near term as construction slows sharply and project delivery dates become extended—i.e., construction pipelines and inventory growth may slow. Cities such as San Francisco and Boston have mandated that all non-essential commercial real estate construction cease for the immediate future, while skilled construction trades workers, many of whom are older, may stay away in other locales. Disruption may also occur as cutbacks in “nonessential” government workers affects the permitting and inspection processes.

Lastly, supply chain disruptions for materials and supplies may impact construction activity. Since January, when COVID-19 economic effects were first felt, there were limited delays on finished materials from China and South Korea that impacted the U.S. construction market. These disruptions have affected materials pricing and created cost overruns, and they are not expected to end anytime soon.

In wrapping up, the world has changed. And changed a lot. These changes will affect our industry in myriad ways—some of which are listed above and some of which are still to emerge. These changes will provide a new opportunity for some businesses such as telehealth, virtual video communications systems, cleaning and sanitation businesses. And they may provide opportunity for some operators, such as skilled nursing operators who can serve as overflow care and space from a strained hospital system, which is projected to run out of beds in the very immediate future. Perhaps it’s also a time for ghost kitchens for operators who have capacity to prepare nutritious and safe food for more broad commercial use. But the COVID-19 pandemic will also bring unforgettable grief and sadness—for both individuals and businesses. Collectively, let’s help provide support, solutions, encouragement and assistance for those on the frontlines in our industry and for those behind the scenes in management and decision-making roles. Hooray for them!

As always, I welcome your comments and feedback.

A Long-Term Commitment to the Sector: A Conversation with Capital One’s Jim Seymour

Note: This interview was conducted in February 2020.

Where some observers see turbulence in the seniors housing and care market, industry veteran Jim Seymour sees a resilient industry that will face the challenges ahead and position itself for the future.

Where some observers see turbulence in the seniors housing and care market, industry veteran Jim Seymour sees a resilient industry that will face the challenges ahead and position itself for the future.

As senior managing director at Capital One, Seymour was recently named head of healthcare and technology, media and telecom banking, including the healthcare real estate team based in Chicago.

Seymour is dedicated to the industry. He served on NIC’s board of directors for nine years and on the executive committee for seven years.

NIC Chief Economist Beth Mace recently talked to Seymour in February Seymour about Capital One’s approach and the outlook for the industry.

Mace: Capital One is a large bank. Where does seniors housing and skilled nursing fit into the organization and its goals?

Seymour: When most people hear our name, they think of our credit card business. But we also have a large and growing commercial banking business. Seniors housing and care fits into our commercial division under healthcare financing, along with medical office and other medical properties. What may be slightly different is that our healthcare real estate business reports to our corporate bank rather than to our commercial real estate business. The last dollar risk is really on the healthcare side rather than on the real estate side. Also, the healthcare real estate business has always been a close cousin to our healthcare corporate finance business, which lends to a wide variety of companies across the healthcare sector on a cash flow and ABL (asset-based lending) basis.

Mace: Jim, what is your role, and how has it changed during your tenure at the bank?

Seymour: I am currently the head of healthcare and technology, media and telecom (TMT) banking for Capital One. I was the head of the healthcare real estate business at GE Capital for many years. We were acquired by Capital One December 1, 2015 and merged the healthcare real estate businesses. I ran the healthcare real estate business for almost nine years, and just this past year, my partner Al Aria, who ran healthcare and TMT corporate finance, retired. The decision was made to consolidate all healthcare activities under me. My role expanded officially on January 1.

Mace: How long has Capital One been lending to the seniors housing and care sector?

Seymour: The team that runs the Capital One healthcare real estate business has been working in the industry for more than 15 years now. What’s exciting about attending industry meetings is that we have alumni everywhere. We’ve trained many of the risk and underwriting professionals in the seniors housing and care sector, including at the REITs and large equity firms. We’re proud of that, and it’s a testament to our longevity.

Mace: Is Capital One’s portfolio of seniors housing loans expanding? How about skilled nursing?

Seymour: Our healthcare real estate business totals about $10 billion in financial commitments. We’ve been very active. Our largest business is medical office. We’ve grown our business with Fannie Mae and Freddie Mac. Last year, we were a top three lender for both agencies in seniors housing, encompassing $800 million in transactions. We don’t hand clients off to an agency team. We sell all our products through the same sales force which is led by Chris Taylor, our commercial leader for seniors housing and care. We come from a balance sheet culture and are happy to put a loan on the balance sheet. That’s been a big part of our success over the last couple years. Customers love that. They like not being pushed into one product or another. We offer them a variety of solutions.

Mace: Do you lend only in the U.S. or in other parts of the globe as well? Within the U.S., do you have any geographic preferences?

Seymour: We operate primarily in the U.S. We have some credit card operations in a few other countries and our group has some Canadian loans. Overseas is a potential area of expansion for us, but it’s not a focus right now. In the U.S., we don’t have a geographic preference. In terms of underwriting, we understand that our operators are all dealing with wage pressures, supply and demand dynamics, and changing consumer preferences. While national statistics are interesting, we spend our time underwriting at the local level. We want to understand not only the seniors housing market but also local economic activity and demographic trends. We are very sensitive to the conditions in different regions of the country. And we monitor our portfolio carefully in terms of concentrations in different geographies in order to maintain balance.

Mace: Do you lend to all seniors housing segments—independent living, assisted living, memory care, and skilled nursing care? Is there one sector you favor over others?

Seymour: We lend to all segments. We will be building our HUD business going forward, but most of our new business now is seniors housing, typically interim financing towards a permanent financing with Fannie or Freddie two to four years after loan origination.

Mace: Why is that?

Seymour: The terms agencies can offer today tend to be more attractive to clients than what banks and non-banks can offer for long- or intermediate-term financing. The agencies have come a long way, and they offer a very sophisticated financing product which is a better deal for many of our clients.

Mace: Do you lend for development, acquisitions, and expansions?

Seymour: Yes, but we think about development as a product among a suite of products—balance sheet lending, agency lending, and banking products such as treasury services. Most of our development financing is of single assets for our more diversified client relationships. We play best for big complicated transactions with a portfolio of assets—some going to the agencies, and some remaining on our balance sheet.

Mace: Do you believe that seniors housing is an operating business in a real estate setting? If so, how do you evaluate the operating business? How do you evaluate the real estate?

Seymour: Seniors housing is a little bit of both. That’s what makes the asset class unique. The only similar asset class is the hotel or hospitality sector. For us, the operator is critical, especially considering some of the challenges in the space. The experience of the operator through different cycles, and the operator’s specific business plan for the asset is important. An asset may be in lease-up, or a portfolio may be a turnaround situation. We try to assess the operator and their experience on executing on that kind of a business plan in that part of the country. Our assessment involves a rigorous evaluation of the real estate–we look at supply and demand, market trends, economic factors, demographics, cap rates, and transaction comps based on the cash flow of the underlying asset. We thoroughly analyze everything at the market and submarket level.

Mace: What data sources do you use? NIC has an actual rates initiative and just rolled out data on the Atlanta, Philadelphia, and Phoenix metropolitan markets. Operators can submit rent rolls directly to NIC through four software vendors. Would that be helpful?

Seymour: We use NIC MAP data and other services. We take information from other sources for population statistics and demographic data. Actual rates will be a huge step to help underwrite properties. We welcome that.

Mace: What do you look for in a good sponsor? How do you measure the quality of an operator?

Seymour: As a relationship-focused lender, we look for demonstrated performance over time, management experience with specific types of opportunities, and the investment thesis of the properties being presented to us for financing. On the sponsor side, there are two primary factors: First, what is their track record? Have they historically made good investments and made money for their investors? And second, we look at how they handle adverse situations. We do a lot of repeat business, and there are times when projects do not perform the way we or investors had hoped. You learn a lot about your customer when things go sideways. Do they stand behind their investment? Do they work with you to get the best possible outcome? With any relationship, we endeavor to be predictable and add as much value as possible, and with an ideal client, it’s a two-way street.

Mace: What would you say to new borrowers looking to work with you?

Seymour: I would say that we are seeking substantial relationships that can grow over time. Based on the scale of our operation, we are not looking for single ventures.

Mace: How do third-party appraisals fit into your decision-making process?

Seymour: In a regulated banking environment, appraisals are the basis of our valuation policy. That’s important because larger loans are syndicated, and banks base their valuations on appraisals. They are not the deciding factor when we assess a loan, but appraisals are part of the approval process used for loan-to-value underwriting.

Mace: When do you turn a lending opportunity down? Are there any immediate red flags?

Seymour: We have built our careers on being very customer focused and on structuring loans to meet the needs of the client and their business plans. As stewards of a bank balance sheet, we must be able to balance the risk and reward of a deal in our own minds and extrapolate that to our shareholders and regulators in order to lend to our customers. We have always been risk focused, and our loss levels have been low in the healthcare real estate sector. The challenge today is that we believe there is a little bit of a disconnect between the capital markets and asset valuations of the sector from the operating realities that we see. The capital markets have continued to be aggressive. Even though performance may be improving, we see opportunities where the lending package needed to win a transaction is too aggressive for us. We don’t fund non-covenant or long interest-only deals.

Mace: The collateral for your loans is the real estate. Do you make loans to the operations of the business as well?

Seymour: We don’t make loans for operations in seniors housing.

Mace: What are the opportunities as well as the challenges you see for the seniors housing and care sector? In both the near and the long-term?

Seymour: The availability and cost of labor is the number one challenge in the seniors housing and care sector. The oversupply of product appears to be going in the right direction, but there are still a lot of units to be absorbed. Another challenge is the industry’s ability to predict and adapt the product to senior preferences as the boomer wave finally arrives. How is that product going to be different from what we have today? That’s the opportunity. Capital One is committed to this space for the long term. We’re excited to be part of the process as a financing partner to figure out what product will meet changing consumer preferences to help our clients succeed.

Mace: What about serving the seniors housing middle market?

Seymour: Cracking the code on a product for the middle market is a big goal. How do we build an affordable product that meets customer preferences? It’s not an easy problem to solve, but affordability is a priority for the industry as the financial capacity of tomorrow’s seniors continues to evolve.

Mace: What about the emerging active adult sector?

Seymour: We are not financing these projects yet, but we are looking at them. The projects are more similar to a multi-family product than a healthcare real estate product. We are having a conversation about where these projects fit into the structure of our bank.

Mace: Any other thoughts you would like to share?

Seymour: Capital One is committed to the space for the long term. Our leadership has been focused on seniors housing and care for 15-plus years. Ultimately, we want to be the best bank for our clients in this space so that they can achieve their mission of supporting seniors and their families. We look forward to evolving with the markets and helping our customers grow and execute their business plans.

Actionable Insight: Lease-up Trends Over Time

By Beth Mace, Chief Economist, and Anne Standish, Research Statistician

Assumptions about lease-up rates are key to developers and operators preparing pro formas for new seniors housing properties as well as for operators of existing properties as they assess the competitive threat of new units entering the market. Some properties with strong marketing teams and reputations have high levels of pre-leasing prior to a property’s opening, while others struggle with lease-up and have a harder time filling units. While individual property-level and operator-level variation matter, this Actionable Insight article examines the performance of care segments within newly opened properties in the 99 NIC MAP® Primary and Secondary Markets for the last decade and compares recent lease-up patterns to those in the past.

ACTIONABLE INSIGHT: Memory care and assisted living care segments at newly opened seniors housing properties are experiencing slower lease-up performance than in the past. Independent living care segments are also experiencing slower lease-ups than they were five years ago. One contributing factor to the slower lease-ups may simply be that there is more competition today due to a more robust development pipeline and subsequently greater inventory growth. Today, higher levels of new, and often similar, product exists at the time of a property’s opening than in the past.

When planning a new property, it is important to consider recent trends in leasing patterns and to understand where a market is in the cycle of development. The ability to lease and gain strong occupancy may be better in the period following a downturn in the economy, as new development is constrained and pent-up demand is strong. As development ramps up and competition strengthens, lease-up momentum may lag.

METHODOLOGY: We calculated the occupancy rates for care segment cohorts/groups at newly opened seniors housing properties by the first quarter a property was opened. To be included in a specific cohort, the analysis required that a property have open units of a specific care segment in the first quarter that a property opened. This means that expansions were excluded from the current analysis and for phased openings, only the care segments that were open in the quarter a property opened were included. The analysis then looked at the lease-up rates per cohort by care segment across NIC’s time series, with a focus on one quarter and eight quarters after opening.

KEY FINDINGS: Lease-Up Velocity. To investigate how lease-up velocity has changed, this analysis looked at occupancy rates by care segment in the initial first quarter of a property’s opening and after eight quarters. Care segments refer to levels of care such as independent living, assisted living, and memory care.

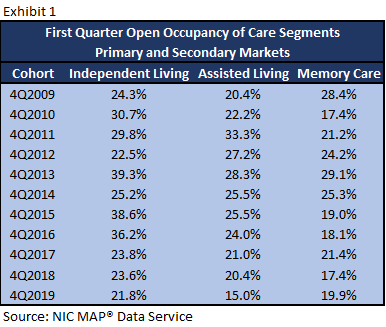

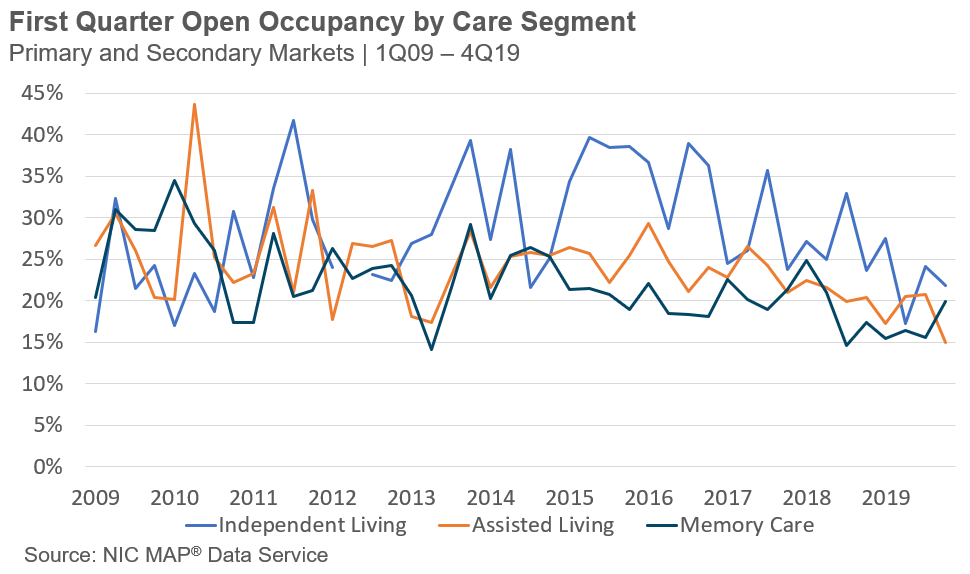

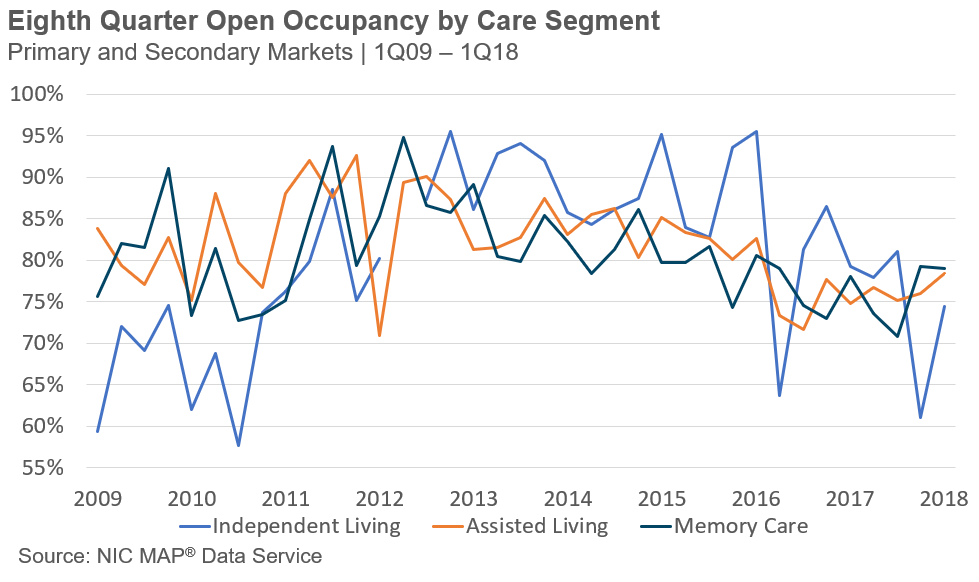

Occupancy After One Quarter. Analysis of NIC MAP data from the 99 Primary and Secondary Markets over the past 11 years shows that care segment occupancy rates for assisted living and memory care segments trended lower at newly opened properties compared to earlier years. Exhibit 1 shows cohorts of care segments at newly opened properties that opened in the fourth quarter of their respective years.

Occupancy After One Quarter. Analysis of NIC MAP data from the 99 Primary and Secondary Markets over the past 11 years shows that care segment occupancy rates for assisted living and memory care segments trended lower at newly opened properties compared to earlier years. Exhibit 1 shows cohorts of care segments at newly opened properties that opened in the fourth quarter of their respective years.

The cohort of assisted living (AL) care segments at properties opened in 4Q19 had an average occupancy rate of just 15.0%, a record low for occupancy in a first quarter open for AL care segment cohorts. By contrast, the cohort of AL care segments for 4Q11 had an occupancy of 33.3% in its first quarter open, more than double that of the most recent period. This was in the period following the recession. Since 2011 as assisted living care segment inventory growth ramped up in the post-recession recovery period, initial occupancy rates at newly opened care segments slowed.

The 99 NIC MAP Primary and Secondary Markets’ group of newly opened memory care (MC) units had an occupancy rate of 19.9% in the first opened quarter in 4Q19, 9.2 percentage points lower than the 4Q13 cohort which had an occupancy rate of 29.1% during its first quarter open.

For the independent living (IL) care segment cohort, the 4Q19 cohort had an occupancy of 21.8% for its first quarter open. This was 17.5 percentage points lower than the 4Q13 cohort’s occupancy of 39.3% in its first quarter open and well below the occupancy pace seen in 2015 and 2016 as well.

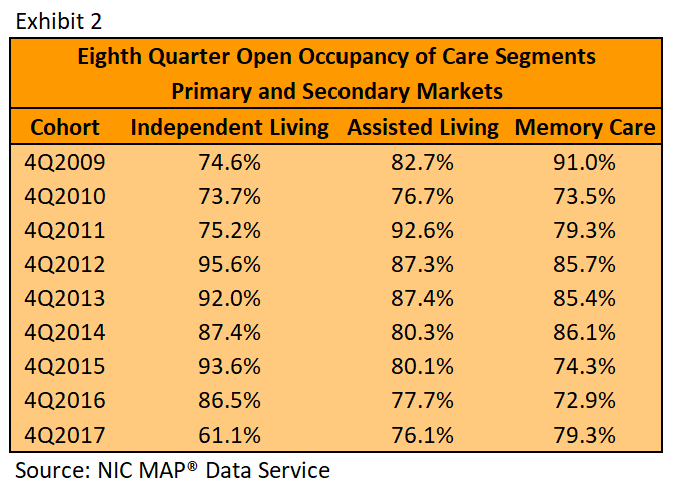

Occupancy Two Years After Opening. The analysis thus far shows that initial occupancy rates have slowed recently for all three care segments compared with historical rates. What about two years after opening?

Occupancy Two Years After Opening. The analysis thus far shows that initial occupancy rates have slowed recently for all three care segments compared with historical rates. What about two years after opening?

To address this, we also looked at occupancy patterns for each of these care segment groupings once they had been open for eight quarters (Exhibit 2).

The 4Q17 independent living cohort had an eighth quarter occupancy of 61.1% for the segment. This value was down notably (34.5 percentage points) from the 4Q12 cohort, which had an occupancy of 95.6% in its eighth quarter open.

For assisted living, the 4Q17 cohort had an occupancy of 76.1% in its eighth quarter of being open. This was 16.5 percentage points lower than the 4Q11 cohort that had an occupancy of 92.6% in its eighth quarter open.

For memory care, the 4Q17 cohort had an occupancy of 79.3% in its eighth quarter open. This was a 6.4 percentage point uptick from the 4Q16 cohort, which had an occupancy of 72.9% in its eighth quarter open. However, the 4Q17 cohort was much lower than the 4Q12 cohort (which had an occupancy of 85.7% in its eighth quarter open) by 6.4 percentage points.

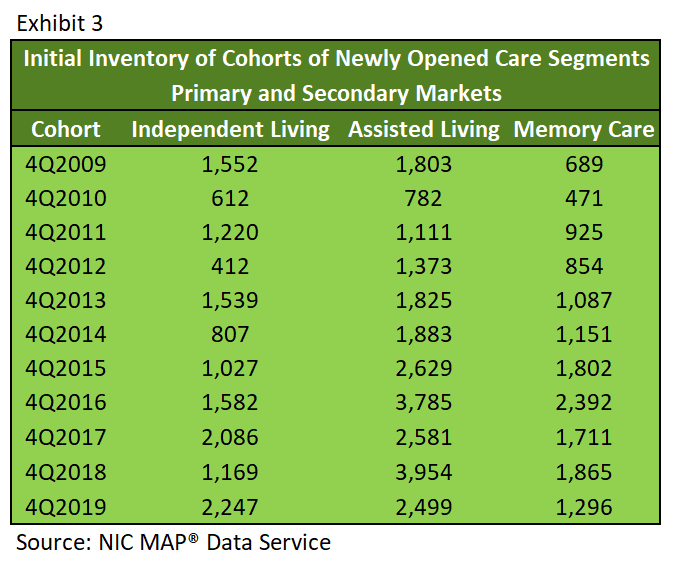

Context. One factor that may be contributing to initial occupancy patterns and eighth quarter occupancy patterns is the amount of new inventory brought online with each cohort. To better understand the inventory associated with these lease-up occupancies, this analysis also examined the initial inventory for each of the cohorts of the three care segments.

Context. One factor that may be contributing to initial occupancy patterns and eighth quarter occupancy patterns is the amount of new inventory brought online with each cohort. To better understand the inventory associated with these lease-up occupancies, this analysis also examined the initial inventory for each of the cohorts of the three care segments.

Of the three care segments, AL also had the most units at newly opened properties in 4Q19 (roughly 2,500). In 4Q19, the independent living cohort was not far behind the assisted living cohort with approximately 2,250 units. Assisted living and independent living care segments had an upward trend of increasing numbers of units per newly opened cohort in the post-recession growth period. The inventory for the memory care cohort in 4Q19 was lower than IL or AL cohorts at nearly 1,300 units. Initial inventory of newly opened cohorts of memory care also had an upward trend following the recession, but recent cohorts suggest that we may be past the peak in the current cycle.

LIMITATIONS AND CAVEATS: This analysis examined care segments for new properties recently opened. It could be that expansions or phased openings have different trends. Sometimes expansions are planned due to rising acuity in the residential population that is already living at the property. In these cases, the property would have a number of leases for higher acuity care segment units already accounted for.

CONCLUSION: Newly opened care segments at recently opened new properties are leasing up at a slower pace than in the past. One factor that may be at play here is there is simply more new supply and greater competition. Management teams at properties facing significant amounts of new competition sometimes consider buying occupancy by offering rate discounts and lowering effective rents. Through the Seniors Housing Actual Rates Initiative, NIC MAP data has shown that this may be happening in Atlanta, a market with a substantial supply pipeline and notable new inventory.

In fact, of the three metropolitan markets for which NIC MAP is currently reporting data (Atlanta, Philadelphia, Phoenix), the largest discounts occurred in Atlanta. As of December 2019, initial rates for assisted living units in Atlanta averaged 16.3% below their average asking rate, which equates to an average initial rate discount of 2.0 months on an annualized basis. This was higher than the comparable discount of 1.0 month for the nation and 0.4 month for Philadelphia. Higher discounts in Atlanta make sense, since that market had the second lowest seniors housing occupancy rate of the 31 NIC MAP Primary Markets in the fourth quarter of 2019 (82.7% versus 88.0% for the Primary Market average), as well as the third highest share of construction versus inventory (12.1% versus 6.7% for the Primary Market average).

Understanding recent trends in leasing patterns, where a market is in the cycle of development, and the implications for the range of rate discounting are all valuable for both planning a pro forma and understanding competitive property dynamics.

NIC Spring Conference Brings Sector Together for Timely Collaboration

Attendees of 2020 NIC Spring Conference at the beginning of March engaged in three days of active discussion, networking, deal making, and engagement around critical trends. A focus on disruption and new partnerships in senior care augmented the annual event’s established focus on real estate debt, equity capital flow, valuations, market trends, and investments.

Educational Program

Building on the conference theme of Investing in Seniors Housing and Healthcare Collaboration, speakers and sessions highlighted the increasing role of healthcare in the seniors housing value proposition.

The first of two general sessions, “Join the Disruption: Convergence of Healthcare and Seniors Housing,” provided real-world examples of healthcare and seniors housing disrupting current models in an increasingly value-based world. The panel discussion focused on the opportunities that now exist to break down old silos, adapt, and partner to improve outcomes. NIC’s Bob Kramer noted that “In the future, a system focused on prevention and wellness will keep people out of hospital and acute care settings. We are moving from a curative model to a preventative model.”

Growth strategist Andy Waldeck presented a thought-provoking keynote titled, “Positioning for the Long Term: The Opportunity for Integrating Senior Care.” Waldeck argued that the unsustainable cost of the U.S. healthcare system has left it ripe for disruption, and that the seniors housing and care industry has an opportunity to reframe its role in the healthcare continuum, saying, “We are in the early innings of the industry transitioning to a new vision.”

Growth strategist Andy Waldeck presented a thought-provoking keynote titled, “Positioning for the Long Term: The Opportunity for Integrating Senior Care.” Waldeck argued that the unsustainable cost of the U.S. healthcare system has left it ripe for disruption, and that the seniors housing and care industry has an opportunity to reframe its role in the healthcare continuum, saying, “We are in the early innings of the industry transitioning to a new vision.”

With educational programming organized along three tracks − Real Estate Strategies, Healthcare Strategies in Real Estate, and Senior Care Collaboration − attendees could easily find sessions aligned with their interests.

Real Estate Strategies

In “Equity and Debt: Financing Private Pay Seniors Housing and Skilled Nursing,” the principals involved in separate seniors housing deals shared their experience in initiating, structuring, and finalizing the deals − including one that was first scratched out on a notepad during a seniors housing conference. Panelists stressed the importance of trust and experience in the industry when choosing to partner.

“Executing a Payroll Play” explored how investors contemplating an opportunity should carefully investigate the financial impact of higher-than-average staff turnover, forecast minimum wage increases, demographic issues like proximity of workforce housing options, and even physical plant quirks that make it difficult for care staff to work efficiently.

Panelists in “Identifying Value Amidst Turbulent Market Conditions” offered varying perspectives on a range of issues affecting valuations today, from margin compression across all property types, to the rising costs of labor and insurance. With audience input on three separate case studies, the panel discussed cap rate drivers (trending downward for seniors housing) and the implications of healthcare collaboration.

Amid rapidly changing market realities, NIC Chief Economist Beth Mace presented, “The NIC Bluebook: Current Market Conditions and the Senior Care Industry.” Mace noted that while it’s easy to worry about plummeting stock markets and worst-case scenario predictions (as of early March) of a 3% drop in global economic growth, historically low interest rates make it easier for people to buy houses and cheaper for companies to finance construction, so there may be a silver lining for seniors housing. She did note however that the COVID-19 virus posed potentially unprecedented challenges to the health system and the economy and its impacts were still unclear.

Healthcare Strategies in Real Estate

“Senior Care and Housing Report Cards: Understanding How Quality Health Care Delivery is Impacting ROI” featured new data, released by ATI Advisory, indicating that integrating healthcare services, such as primary care and nurse practitioners, into seniors housing can reduce costly ER visits and hospital stays by as much as 50%.

Every seat was filled for “PDPM: Five Months In,” to learn how the skilled nursing sector is fairing under the newly implemented Medicare Part A reimbursement system. As panelist Steven Littlehale of Zimmet Healthcare remarked, “The good news is we are the cheapest game in town delivering the best product. We win. That silver wave will help us as well.”

A fun format based on a popular TV show, “Project Healthcare: Designing Integrative Care Models That Work” featured three innovators, a panel of judges, and a real runway, to delve into successful models of care integration in seniors housing.

In “Value-Based Strategy: Partner, Acquire, or Build?” a trio of industry thought leaders shared their approaches for vertical integration strategies to keep afloat, remain competitive, and better serve their residents and their families. “Our mission is about providing the most seamless group of services that we would want for our own families and communities,” said Peter Longo, principal and managing partner of Cantex Continuing Care Network.

“Operators and the Capital Providers Who Love Them,” offered a lively discussion around changes in how capital providers evaluate operators, and how operators are demonstrating their abilities and value to debt and equity providers. As healthcare continues to impact the sector, data, strategic planning, and increasingly, healthcare relationships are factoring into these discussions.

A well-attended town hall session, “Planning for the Care Needs of the Forgotten Middle” explored how the seniors housing industry can provide appropriate care and housing for middle-income seniors, a growing cohort that will present a challenge to the nation going forward. According to Jim Lydiard of CareMore, “We agree that middle market seniors housing is missing, and we need to innovate − perhaps rethinking meals, finding funds from special interest groups, renting first floor space to other companies. We need a multi-industry mindset.”

Senior Care Collaboration

The growth of the cost of healthcare is unsustainable. In “Five Healthcare Trends You Need to Know,” a panel of experts weighed in on healthcare trends impacting the senior living industry. Owners and operators will confront a future of disruption where scale will matter along with a change in the way healthcare is accessed and delivered.

It’s been around since the 1950s, but telehealth is just now entering the mainstream, and at a very important time. In “Telehealth: Boon or Threat to Senior Care?” attendees learned that data prove that using video to bring physicians or specialists into patients’ residential settings generates equivalent outcomes to physical appointments – but without the hassle of transportation or the well-known risks of hospital visits. Speakers concluded that seniors housing operators can help residents overcome technology hurdles and should seriously consider partnering with telehealth market innovators to keep their population safer and healthier.

In the transition to value-based care from a fee-for-service payment system, providers are exploring whether to enter into risk-sharing agreements. The session, “Collaboration or Competition: Who Owns the Healthcare Dollar,” brought together experts who shared their experiences with new models of collaboration. Panelists agreed that risk-sharing is a “team sport” that takes genuine cooperation.

As the rest of the health care industry moves toward value-based care, most physicians are still paid on the basis of fee-for-service. In “What’s the Physician’s Role in the Value Equation?” attendees heard how this mismatch of incentives creates real problems for skilled nursing properties or other providers trying to offer better care at lower prices. An engaged physician can catalyze a team, acting as mentor and inspiring others to higher performance, so it is worth exploring how to keep doctors’ incentives aligned with everyone else’s, through consistent metrics, re-thinking the role of medical directors, and even selecting just a few physicians to be preferred providers.

Learn More

During the conference, NIC announced the certification of its fourth Actual Rates Software Partner. Clients of Medtelligent, the maker of ALIS software for assisted living, memory care, and behavioral health communities, can now use the software for automated, efficient participation in NIC’s powerful Seniors Housing Actual Rates Initiative.

Highlights of the 2020 NIC Spring Conference are available now on nic.org. Session video and audio recordings will be made available to conference attendees later this month.

Submit Your Photos for the NIC Investment Guide

The sixth edition of the NIC Investment Guide: Investing in Seniors Housing & Care is scheduled to publish in fall 2020. We invite your organization to submit photos of seniors housing and nursing care properties to be featured within this publication.

The NIC Investment Guide is a primer for understanding the seniors housing and care sector. It provides the most reliable industry data for investors to help them evaluate risks and returns, and to fine-tune their individual investment strategies.

What We’re Looking For:

- Images of property interiors or exteriors (new and older properties).

- Images of property amenities.

- Images may include shots of residents.

To submit images for the opportunity to be featured in the NIC Investment Guide, review the file requirements and submission form found on our website. Files must be received by May 1, 2020.

How Community Design Affects Wellness and Social Isolation: A Bridge the Gap Interview with Architect Greg Hunteman

Bridge the Gap (BTG) Hosts: Joshua Crisp and Lucas McCurdy

BTG: What does wellness in senior living and healthcare design mean?

BTG: What does wellness in senior living and healthcare design mean?

Hunteman: Right now, a lot of folks will say, “Let’s talk about how you’re doing wellness. What’s your programming? What are you doing?” And the response is, “Well, we have an exercise room.” That’s only one aspect of what we’re doing. The simplified version is it’s the body, the mind, and the spirit. Everybody thinks about the body, but it’s really much more holistic. The National Wellness Institute actually defined wellness as having six or seven different levels or “dimensions,” as they call it. We like to think it’s seven or eight. Thinking about it this way has a huge impact. Basically, we want to feed the body; we want opportunities for exercise; we want to have a good diet; we want to have rationales for residents to get around and out of their apartments.

A lot of older adults have a tendency to self-isolate. There’s a lot of depression, there’s a lot of loneliness. This actually is part of the reason older adults should move out of their home and into a community. But even in the community, if they don’t acclimate well or they don’t get out and be active, this can still be an issue. It’s a good idea to up the types of activities and amenities that they want to be a part of, whether it’s an indoor amenity or an outdoor amenity. There’s a lot of opportunity for wellness outdoors. Then there’s the spiritual aspect, which really means different things to different people. It could be coming to grips with where you’re at in life and what’s next. It could be community with other folks, social engagement, or a lot of different things.

You really want to figure out ways to engage them. What is it they did? How can they mentor? How do you appreciate that? Although there’s a lot of stuff that they’re dealing with, memory care becomes a very exaggerated form of what we do. It’s a lot easier to see the feedback on a space or a program or an activity that is engaging a resident. You can see, wow, this really works. But almost everything that we do in memory care is going to have a similar effect on assisted living to a certain extent. Independent living and active adult are a little bit different but will still be impacted.

BTG: So just mind and body?

Hunteman: That’s the simplified version. The other aspects are emotional, occupational, physical, spiritual, intellectual. We do a lot of education around these aspects in design and planning. Social is probably the biggest one. Studies have concluded that your genes are a much smaller portion of your well-being. We used to think, okay, genes make a big difference. Now, it’s really the lifestyle that you live, how socially engaged you are, and how happy you are. That’s why you see in some communities the biggest relationship is between the caregiver and the resident. Because that is the person that they see every day.

BTG: This is one of the things we talk about frequently. It can be really important to work with people who understand the senior living industry. I’m sitting here listening to this, and I’m thinking, wait, are we talking about architecture? In fact, we are, and it goes a lot deeper.

Hunteman: You can have a really well-organized building that’s not as attractive, but it’s more cost effective. Or you can have a beautiful building that operates really poorly because it might be amazing to walk into, but it’s really complicated to utilize. You want to put them both together. Obviously, it depends on who you’re serving and what the market is, and then try to put together a way that makes sense. I started designing hospitals first. We were taught to learn about how it was run even more than you would think.

Hunteman: You can have a really well-organized building that’s not as attractive, but it’s more cost effective. Or you can have a beautiful building that operates really poorly because it might be amazing to walk into, but it’s really complicated to utilize. You want to put them both together. Obviously, it depends on who you’re serving and what the market is, and then try to put together a way that makes sense. I started designing hospitals first. We were taught to learn about how it was run even more than you would think.

BTG: What are some practical trends that you see in the market, that you’re seeing actually benefiting people through utilization of these wellness spaces?

Hunteman: Right now, assisted living looks like independent living. You want a lot of the amenities because the resident almost doesn’t want to admit they should be in assisted living. So, you want them there, you can still get all the pieces and parts there. What we want to do is understand the programming and how they’re going to utilize it. Like you said, we can put all kinds of things in the building, but they’re not always going to utilize them. I’d rather do one thing better, that they’re going to utilize, than a bunch of things that go unused. Understand that placement is huge. Some people will design where they might have all the amenities, but it might be on all different floors or it might be at the end of a hallway. You want to have the majority of the energy in one spot.

If you can design where they have to walk by the space to get to another space, it’s easier for the staff to manage. The best example would be to have an exterior space that you create, but it’s hard to get to, and the staff can’t see it. Now the staff’s not going to encourage them to use it because they’re afraid someone could get injured. If it’s not designed so they can be seen if they fall, the residents can be afraid to utilize it. So, if you wrap the building around that exterior environment, the utilization will be huge. That’s really the key: to think about how everything interrelates.