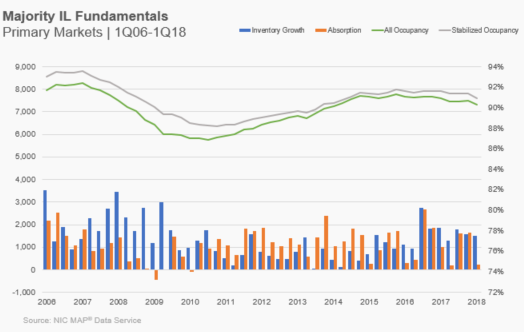

Supply and demand more balanced; occupancy sustained above 90%

In the first quarter of 2018, among the 31 primary markets tracked by NIC MAP, independent living had an occupancy rate of 90.3%, which was about 70 basis points less than stabilized occupancy. Comparatively, assisted living had a differential of 230 basis points, more than three times as large since there are many more units that have opened but are still in lease up for assisted living than for independent living.

The most recent cycle of independent living inventory growth began in the middle of 2015. Despite a 5% increase in stock, occupancy rates have been sustained above 90% since early 2014 as demand has held up reasonably well. Metropolitan markets such as Atlanta, Houston, Kansas City, and San Antonio, have increased their independent living stock, but other markets such as Washington, D.C., Denver, Detroit, Los Angeles, New York, and Philadelphia, among others, have maintained relatively low-to-moderate supply growth.

Of additional note, the data show a 30-basis point quarterly decline in the independent living occupancy rate to 90.3%, which stemmed from a marked slowdown in first quarter absorption and somewhat weaker inventory growth. Reasons for the slower pace of activity could be related to seasonality patterns typically seen in the seniors housing data including influenza and influenza-like illnesses and winter weather, which tend to subdue both inventory growth and demand. Anecdotally, many properties lost marketing days in January and February due to the weather and flu-related property-level quarantines. Given that these factors were especially harsh during 4Q2017 and 1Q2018, there may potentially be a corresponding bounce back in in the second quarter as delayed move-ins from the winter months take place.

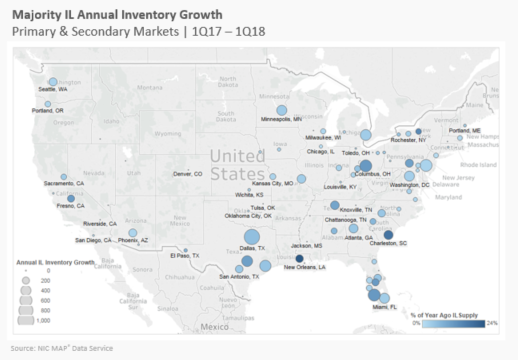

Inventory growth largely concentrated in a few markets

The map below shows the parts of the country that have seen the most change in independent living inventory in the past year. During the past year, there have been more than 11,000 independent living units added to inventory among the primary and secondary markets.

About one third of this growth in inventory occurred in seven metro areas: Dallas, Philadelphia, Columbus, Fort Myers, Houston, Detroit and Austin. While Minneapolis and Miami also saw strong independent living inventory growth over the past year, Baton Rouge, Charleston and Syracuse were geographies that experienced the greatest percentage gains in inventory.

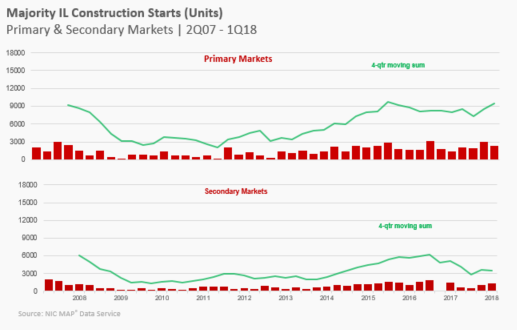

Are construction starts plateauing or rising?

After peaking in mid-2016, construction starts in the secondary markets have been falling on a four-quarter moving-sum basis. In the primary markets, however, the peak was earlier (mid-2015) and the trend for the primary markets appears to be flat or rising.

Of note, anecdotal reports of delays in starts due to the weather and interruptions in starts due to delays in financing and funding may have caused some groundbreaking dates to be pushed back. And while construction starts data are subject to revision for these reasons, the numbers provide insight into what is in the pipeline. Interestingly, while the data shows a potential increase in independent living starts in the 99 primary and secondary metropolitan areas tracked by NIC MAP, it also shows a slowdown in starts for assisted living, which may signal increasing interest in independent living from investors and developers.