Institutional Capital Drives Transaction Volume Higher in 2017

Nursing care prices fall

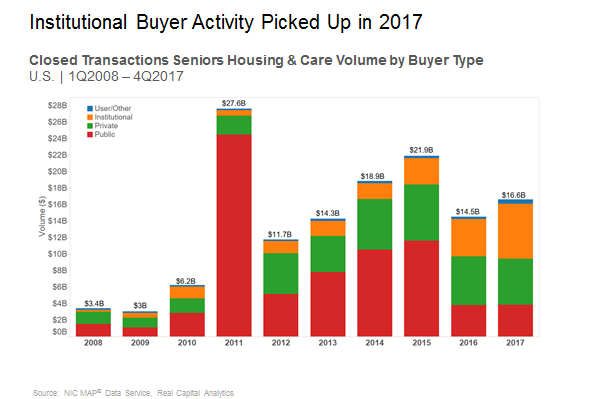

Updated transactions dollar volume for 2017 shows an increase from 2016 as the institutional buyer, comprised of mostly equity funds that manage pension money or other types of institutional money, played a major role in higher volume.

A trend has emerged over the past couple years in which institutional buyers have significantly increased the representation of total buyer volume, while also increasing the dollar volume overall. In 2015 the institutional buyer registered $3.2 billion in closed transactions, representing only 15% of all buyer volume. In 2017, the institutional buyer registered $6.6 billion in closed transactions, a 107% increase from 2015, representing 40% of overall transaction volume.

Some relatively large deals to note from the institutional buyer in 2017 were:

- Kayne Anderson, the institutional alternative investment manager, bought a $633 million portfolio from Sentio Healthcare Properties which consisted of 32 seniors housing and care properties. This deal included some medical office building (MOB) properties which are not reflected in these volume numbers;

- Columbia Pacific purchased 54 seniors housing properties from Hawthorn Retirement Group for $1.8 billion which included over 6,100 units;

- Blackstone closed on 60 Brookdale properties from HCP representing $1.1 billion in volume, with a unit count of over 5,500;

- Blackstone, in another large deal, closed on the Senior Lifestyle’s portfolio from Welltower for $747 billion including 25 properties and over 3,600 units; and

- Lastly, in another large deal, the Chinese life insurance company, Taikang Life Insurance, purchased a partial interest in the Northstar portfolio, which according to a press release totaled about $460 million and included over 200 properties.

While institutional buying activity increased, public buyer activity decreased significantly after 2015 as a share of volume. Public buyer representation also decreased in terms of overall dollar volume. The public buyer type represented 53% of the $21.9 billion in total closed transactions in 2015. But as of 2017, the public buyer now only represents 23% of the $16.6 billion in total volume. Public buyer volume in 2015 was $11.6 billion and in 2017 it had decreased 67% to $3.8 billion.

Last to mention, let’s not forget about the private buyer segment which includes private REITs, private owner operators, and private partnerships. It has been a very steady buyer, averaging $6 billion dollars per year from 2015 through 2017. Indeed, private buyers have accounted for very impressive deal flow. The private buyer registered $6.8 billion in volume in 2015 and represented 31% of all volume. In 2017, the private buyer registered $5.6 billion and represented 34% of all volume. Even with the relatively weak fourth quarter volume in 2017, the private buyer accounted for $1.2 billion in closed transactions to close out the year.

Pricing

The storyline for seniors housing and nursing care pricing has started to diverge over the past year.

Seniors housing price per unit was flat in the fourth quarter of 2017, compared to the third quarter at $180,500. However, on a year-over-year comparison, seniors housing price per unit is up 9.3% from $165,100. And from its cyclical low in 2010 of $58,600, it is up over 208%, which translates into a 16.2% compound annual growth rate over the period.

The trend for nursing care price per bed is another story. The price per bed dropped 1% to $83,800 in the fourth quarter from $84,600 in the third quarter. On a year-over-year comparison, nursing care price per bed is down a significant 16.5% from $100,300 in the fourth quarter of 2016. However, from its cyclical low in 2009 of $48,700, pricing is up 72%, which equals a 6.4% compound annual growth rate.

It looks like the nursing care price per bed drop has stabilized somewhat this past quarter, but we will see how it holds up over the next few quarters.

Stay tuned for the next transactions blog after the first quarter 2018 data is released.