Senior housing has become one of the fastest-growing sectors in commercial real estate. Demand is accelerating, occupancy is climbing, construction remains constrained, and capital is flowing into the sector.

That growth is creating opportunity—but it has also exposed a skills gap. Senior housing isn’t simply another real estate asset class. Success requires understanding the intersection of real estate, healthcare, operations, finance, and demographics, knowledge that most professionals were never formally taught.

Whether you’re expanding into senior housing from commercial real estate, healthcare, lending, or investment management or just want to improve your skills and credibility for your company and your career growth, the question isn’t just whether the market is attractive. It’s whether you can quickly build the expertise needed to participate confidently.

So how do you actually build the expertise to work in this space?

For many, the answer is structured education. While market data, conferences, and industry publications provide valuable insights, they rarely offer the structured, comprehensive understanding needed to evaluate opportunities and make informed decisions across the sector.

That’s where professional certification can help. Whether a senior housing certification is worth the time and investment depends on your goals—and on whether the program teaches the specialized knowledge your role requires. NIC Academy’s Certified Senior Housing Investment Professional (CSHIP) certificate program is the only industry certification designed specifically to build expertise across the senior housing and care sector. The sections below explain what the program covers, who benefits most, and how to determine whether it’s the right investment for your career.

Why Senior Housing Is Harder to Underwrite Than It Looks

Senior housing combines two businesses that most investors learn separately: real estate and operations. The real estate side follows familiar patterns of rent, occupancy, and cap rates. But the operating business underneath determines whether those patterns hold.

- Occupancy does not behave like apartment occupancy. Absorption runs slower and is shaped by care needs, not just price.

- Pricing depends on care level, payer mix, and local competition, not just square footage and amenities.

- NOI margins move with labor costs and regulatory changes as much as with rent growth.

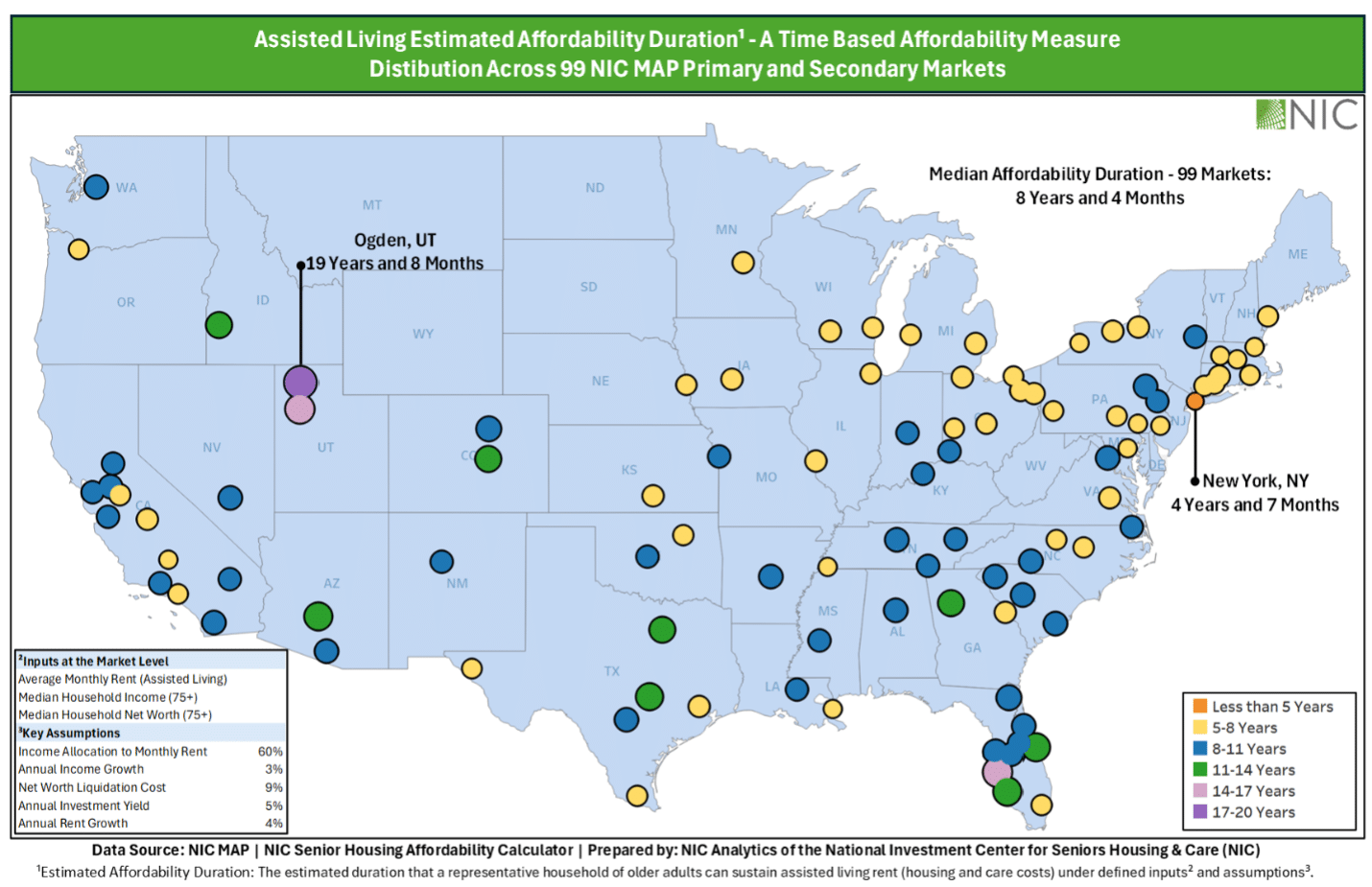

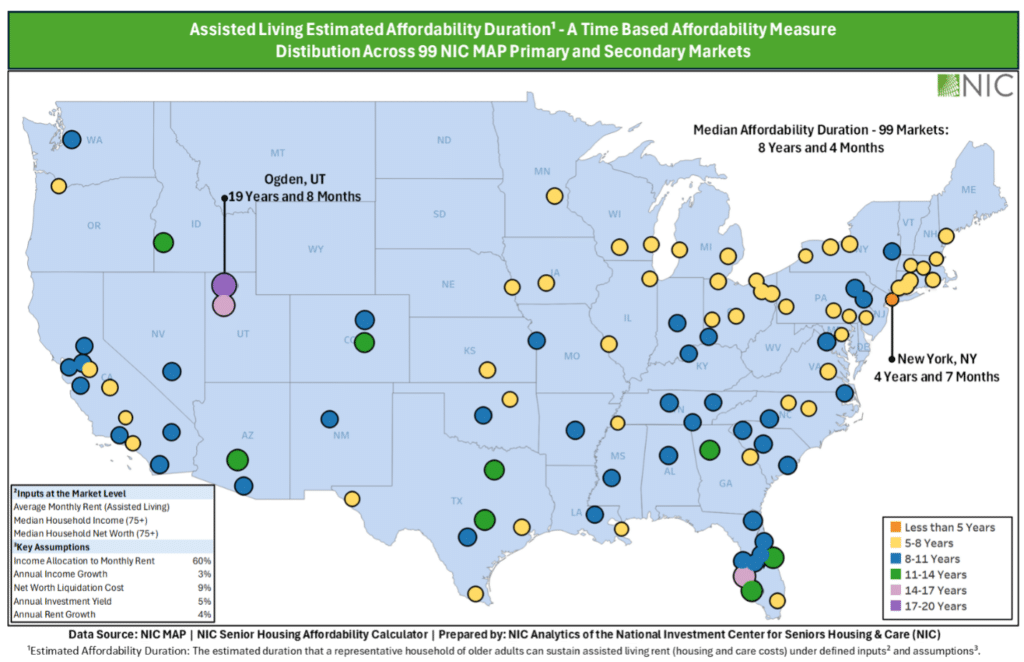

The current market shows how much this matters. According to the National Investment Center for Seniors Housing & Care (NIC), the parent company of NIC Academy and the most trusted resource of objective and timely industry insights and convener of leading decision-makers, senior housing occupancy reached 89.5% in the first quarter of 2026, the 19th straight quarter of growth. At the same time, new construction starts fell to their lowest level since 2012, and year-over-year inventory growth slowed to just 0.4%.

That combination, rising demand against almost no new supply, is precisely the kind of dynamic a general CRE background does not prepare someone to read. It takes sector-specific training to know what these numbers mean for underwriting and where the next opportunity is likely to show up.

Why Can’t I Just Learn This on My Own?

Information about senior housing is not hard to find. NIC publishes data every quarter. Conferences cover underwriting and operations. Trade press tracks deals in real time. The real challenge is not access. It is the organization and trusted real-world lessons from seasoned industry experts.

Self-directed learning tends to deepen knowledge only where a professional already has exposure. That leaves gaps exactly where someone has not yet been tested.

- An investor who has closed a few deals may understand acquisition mechanics but miss operational risk.

- A lender who has financed senior housing may understand credit structure but not why occupancy varies between similar assets in the same market.

- An operator may understand resident care but not how a deal gets underwritten or financed.

There is also simply more to track than there used to be. Knowing what data exists is one skill. Knowing how to use it while underwriting a live deal is another. That second skill is what a structured program is built to teach.

Who is CSHIP Built For?

CSHIP is not an introductory overview of the industry. It is a professional credential for people working in capital markets, investment, operations, or advisory roles who need real depth in a sector where they may not have formal training.

- CRE investors, brokers, and lenders expanding into senior housing

- Capital markets professionals evaluating allocation decisions

- Care executives and operators who want a stronger grasp of the investment side

- Consultants and advisors who need a shared framework with their capital and operating partners

- Professionals early in their careers who want a credential that signals real sector commitment

The program is built for working professionals. Coursework is designed to fit around existing schedules rather than compete with them.

See what’s actually in the curriculum

CSHIP Level I and Level II break down exactly what’s covered, who each level is built for, and how the coursework maps to real underwriting and deal work.

What the Program Actually Covers

CSHIP was built by NIC Academy for professionals who need a complete view of the sector, not just one piece of it. The curriculum includes:

- Senior housing market fundamentals and demographic demand drivers

- Investment analysis and underwriting frameworks

- Capital structures and debt financing

- Operations and NOI dynamics

- NIC MAP data interpretation

NIC’s affiliation with NIC MAP, the primary source of senior housing performance data runs through the whole program. Participants are not reading secondhand summaries of NIC MAP data. They are learning to work directly with the same data that the institutions deploying capital in this sector already rely on.

What Is the Actual Return on Certification?

The value is not mainly the credential line on a resume, though that helps. The bigger return is faster, better-informed decision-making once you have a complete framework for the sector, rather than a patchwork of knowledge.

Senior housing has become a real institutional asset class, and the performance backs that up. According to NIC’s reported market data, senior housing posted a 3.9% total return in the first quarter of 2026, its strongest quarterly performance since late 2017, and outperformed the broader NCREIF Property Index’s 1.2% return over the same period.

As more capital moves toward an outperforming asset class, the operators, lenders, brokers, and advisors working in it need to match that level of sophistication. Professionals who complete CSHIP typically report three concrete gains:

- More confidence in holding sector-specific conversations with capital partners

- A sharper eye for gaps in deal logic or underwriting assumptions

- A wider professional network built on a shared analytical framework

That last point matters more than it sounds. When a lender and an operator speak the same analytical language, deals move faster and with fewer surprises.

Is Certification the Right Move for You Right Now?

The strongest candidates are professionals already working near senior housing who want to formalize their expertise, people transitioning from another CRE sector or healthcare, and anyone who has already identified a specific gap in their knowledge. A few honest questions help clarify these issues:

- What decisions do I make regularly that would benefit from stronger sector knowledge?

- Which parts of senior housing do I currently rely on someone else to explain to me?

- Would a structured program get me there faster than continuing to learn on the job?

If you can answer those with specifics, certification will likely pay off faster than continuing to piece things together informally.

Why the Timing Matters Right Now

The oldest Baby Boomers turn 80 in 2026. According to PwC and the Urban Land Institute, the population age 75 and older is expected to grow by more than 4 million by 2030, and the number of adults 75 and older living alone is projected to more than double by 2040. That kind of demand will need capital, operators, and advisors who understand the sector with real precision.

NIC research indicates senior housing occupancy is on track to surpass 90% before the end of 2026, which would mark the highest level recorded since NIC MAP began tracking the data. Construction starts remain at some of their lowest levels in over a decade. Capital is entering the sector at a moment when fundamentals are strong, and supply is unlikely to catch up soon. Professionals who build real expertise now are entering at the right point in the cycle.

CSHIP gives professionals a direct path to that expertise. The frameworks taught in the program are not borrowed from another asset class. They are the ones the industry itself uses.

Ready to take the next step?

If the case for structured expertise in this article matches how you’re already thinking about your role in senior housing, the next step is simple: look at the program details and enroll when you’re ready.