The Labor Department reported that there were 157,000 jobs created in the U.S. economy in July, below the consensus expectation of 193,000. However, revisions added 59,000 to the prior two months as June was revised to 248,000 from 213,000 and May was revised to 268,000 from 244,000. Payrolls have averaged 215,000 per month so far this year, up from 182,000 last year.

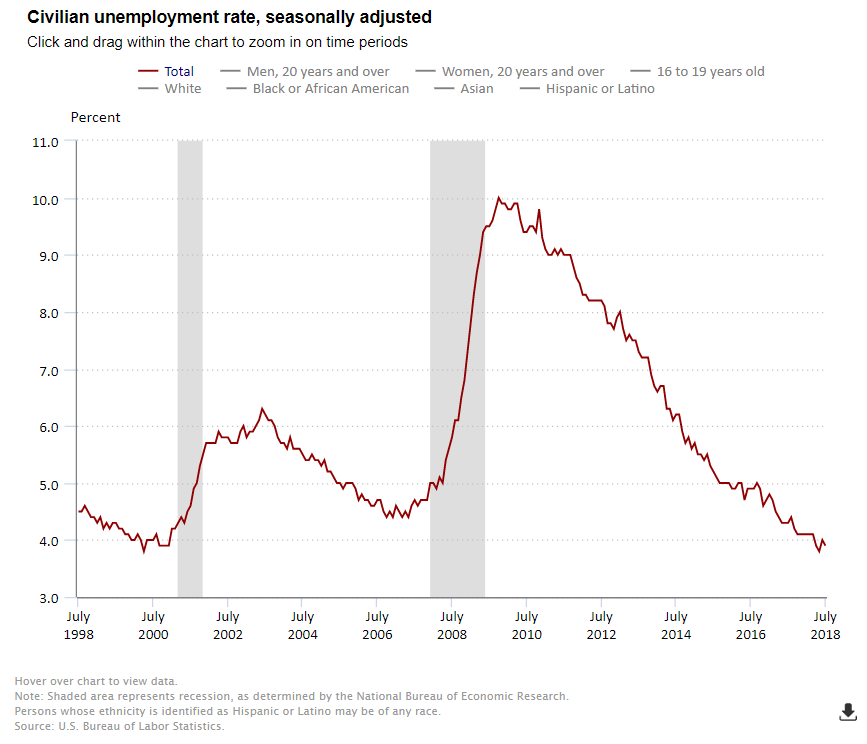

The unemployment rate fell to 3.9% in July from 4.0% in June. The jobless rate remains well below the rate of what is generally believed to be the “natural rate of unemployment” of 4.5% and continues to suggest that there will be growing upward pressure on wage rates. The jobless rate is calculated from a different survey than the survey used to calculate the number of new jobs (the household versus the establishment survey, respectively). Among major worker groups, the unemployment rate for adult men was 3.4%, adult women 3.7% and teenagers 13.1%.

A broader measure of unemployment, which includes those who are working part time but would prefer full-time jobs and those that they have given up searching—the U-6 unemployment rate—fell to 7.5% in July from 7.8% in June and was down from 9.2% as recently as December 2016. The July rate of 7.5% was at a 17-year low.

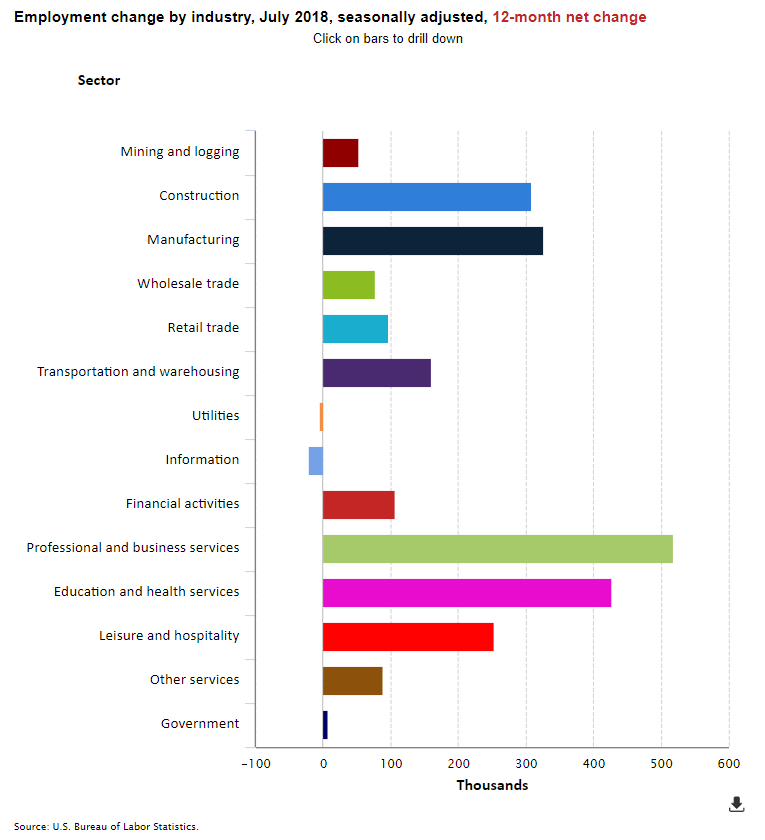

In July, employment in health care and social assistance rose by 34,000. Health care employment continued to trend up over the month and rose by 17,000 jobs in July and has increased by 286,000 over the year. Hospitals added 7,000 jobs over the month. Within social assistance, individual and family services added 16,000 jobs in July and 77,000 jobs over the year. Construction employment continued to trend up in July and increased by 19,000 in July and has increased by 308,000 over the year.

Average hourly earnings for all employees on private nonfarm payrolls rose in July by seven cents to $27.05. Over the past 12 months, average hourly earnings have increased by 71 cents, or 2.7%. This is the same as in June and up from 2.5% on average in 2017. A more comprehensive measure of wage pressure is the Employment Cost Index (ECI), which has shown greater acceleration. In the second quarter, private wages in the ECI were up 2.9% from year-earlier levels. Last year, they averaged 2.6% and in 2016, they averaged 2.3%.

The labor force participation rate, which is a measure of the share of working age people who are employed or looking for work held steady at 62.9%. Nevertheless, this remains quite low by historic standards, although up from a cyclical low of 62.5% in October 2015. The low rate at least partially reflecting the effects of an aging population.

The July jobs report and the report last week from the Commerce Department that GDP expanded at an annual rate of 4.1% in the second quarter will provide further support for increases in interest rates through 2018 by the Federal Reserve. As widely expected, the Fed increased the fed funds rate by 25 basis points at its June FOMC meeting, the second increase in 2018. The Fed has raised rates by a quarter percentage point seven times since late 2015, and most recently to a range between 1.75% and 2.00%, after keeping them near zero for seven years. The June projections by the Fed now show a total of four increases in the fed funds rate are anticipated in 2018 (two of which have already occurred), up from an earlier expectation of three. This would bring the benchmark rate to a range of 2.25% to 2.5% by year end. The Federal Reserve also upgraded its view of the economy by substituting the word “strong” for “solid” in the statement that policy makers released after its meeting. Further increases in the fed funds rate are anticipated in 2019. Their projection for the fed funds rate in 2020 is 3.4%. Hence, it is likely that there will be another 25-basis point increase announced by the Fed at its September and December FOMC meetings.