Part I—Equity Investors Weigh in on How to Make the Numbers Work

Facing a shortage of seniors housing and care options for the growing numbers of middle-income seniors based on new research, NIC convened an investor summit May 21 in New York City. The summit brought together industry stakeholders to brainstorm ideas to create innovative housing models that cut costs and streamline operations to improve affordability for middle class elders. Promising approaches included public-private partnerships, shared suites, new technology, and efficient designs and staffing models.

The investor summit included three separate panels of experts. They explored various solutions from the perspective of equity investors, debt providers, and property operators with successful strategies already in use.

The results of a new study, “The Forgotten Middle,” were also presented at the summit. The study was recently published in the journal Health Affairs and discussed at an April 24 policy forum in Washington, D.C.

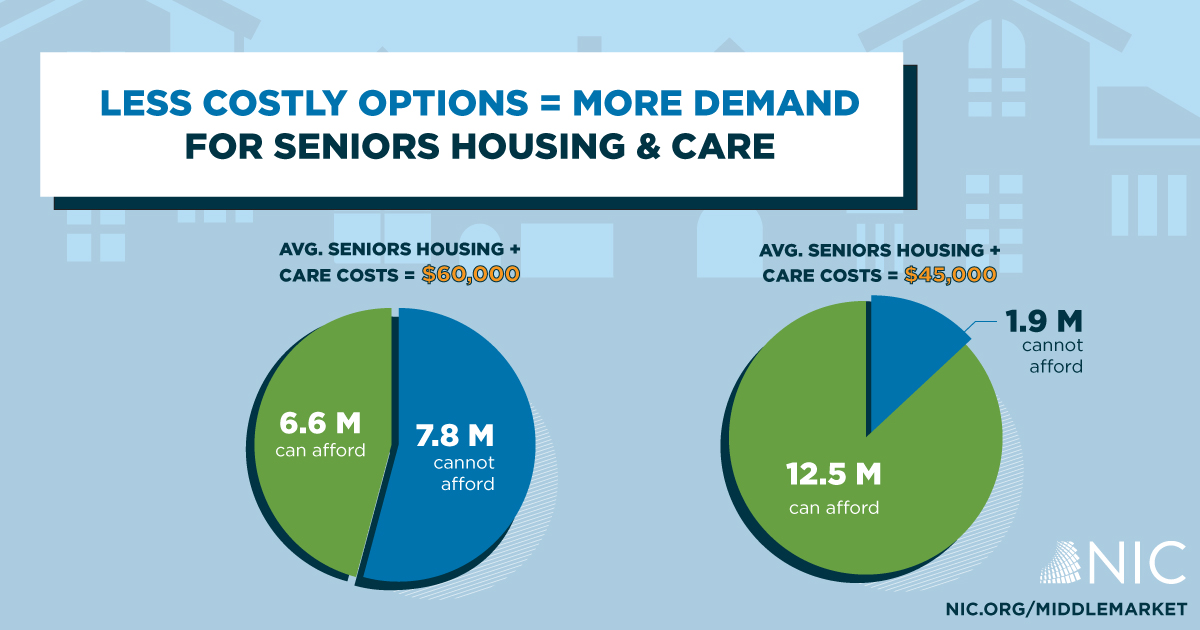

The study shows that fewer than half (46%) of America’s middle-income seniors will be able to afford the $60,000 average annual costs of seniors housing and out-of-pocket medical costs in 2029, even if they use all of their financial resources, including their home equity. But if the costs were cut, millions of older adults could benefit.

The independent research conducted by NORC at the University of Chicago also shows that an additional 5.9 million older adults would be able to afford seniors housing if annual costs were cut by $15,000. Data show that if average annual costs for seniors housing and care fell by just $10,000 a year, an additional 2.3 million older Americans would be able to afford it.

“In only a decade, the number of middle-income seniors will double, and most will not have the savings needed to meet their housing and personal care needs,” said Caroline Pearson, senior vice president at NORC at the University of Chicago and one of the study’s lead authors. “Policymakers and the seniors housing community have a tremendous opportunity to develop solutions that benefit millions of middle-income people for years to come.”

Funding for the study was provided by the National Investment Center for Seniors Housing & Care (NIC), with additional support from AARP, the AARP Foundation, the John A. Hartford Foundation, and The SCAN Foundation.

What follows is an edited Q&A of the first panel discussion which focused on equity investors. (Here is a link to the other panel discussions.) The equity panel was moderated by NIC Chief Economist and Director of Outreach Beth Mace.

Participants of the equity panel included Pam Herbst, managing director, AEW Capital Management; and Andrew Brett, principal, director of Real Assets Research, NEPC.

Mace: To put our discussion in context, what changes have you seen in the acceptance of seniors housing by institutional investors over the last 10 years?

Brett: We’ve been calling seniors housing an emerging asset class for a number of years, but now it’s becoming more of a core investment like the four main commercial real estate asset classes. Not all investors are there yet, but it’s an active conversation. We currently tend to look at seniors housing as a value-add or opportunistic investment.

Herbst: The first time years ago when we went to a client about investing in a stabilized portfolio of seniors housing at a 10.5% cap rate, they were scared to death. But we were able to convince them to invest and we walked out of the room with $100 million in equity for a portfolio and it did amazingly well. We could show clients that the operating risk was not as much as they thought. A lot of them thought assisted living and memory care was like the nursing home where they visited their grandparents.

Over time, the risk perspective has been reduced for clients. They saw during the financial crisis that assisted living did well because it is need driven. We did learn that independent living had a different risk profile because it was a choice and people could not sell their houses. But that risk has come down and now we can meet cash flow and return requirements, so investors are getting more comfortable with that segment.

A number of institutional clients today view seniors housing as a core-plus or value-added strategy. Fifteen years ago, they looked at it as an opportunistic play. But if clients understand the huge opportunity with growing demand for seniors housing, stabilized properties fit comfortably in the core to core-plus strategy space.

For a middle-market product, we have to work on the cost per unit and required investor margins. As a company, we’re looking at developing affordable units in Texas for $140,000 per unit. Discounting land costs by $25,000, the cost is still $115,000 a unit—much higher than the cost it would take to meet today’s return requirements. It’s not just the investment returns that are an issue, but the cost to develop the project.

Mace: Could you get comfortable with middle-market investing?

Brett: Institutional investors do believe in the resiliency of the asset class. But we have to have a compelling scenario to meet their actuarial rate of return of 7+ %.

Mace: Is there a fully private market solution or do we need a public/private partnership?

Herbst: I think we need some kind of subsidy. We’ve looked at shared units with two bedrooms, shared common space and a bathroom. The costs are 20-25% less than for full market private pay units. Greater demand because of a larger population should produce a quicker lease-up which will impact cash flows. Another thought is to look at shared rooms, like college dorms. It could be a suite with 4 bedrooms, and a bathroom with two sinks, and a shower, and 2 toilets. That arrangement would lower the construction and operating costs.

It’s possible now to speed entitlements with a local municipality when 15-20% of units are earmarked for those with 80-120% of the area’s median income. If a developer would agree to target 20% of units for middle market seniors, and the municipality boosts the project’s FAR (floor area ratio) by 25%, you’re essentially eliminating the additional land cost. Also, seniors don’t impact local schools or use many city services which is an argument to reduce property taxes.

Brett: I had a similar thought about shared spaces, but how would that impact residents?

Herbst: We have shared units in four projects and the roommate situation is going great. People have connected with old friends and we’ve had very few problems. It’s important that the bedrooms have room for a chair and TV. At some point, not everyone can afford a ritzy place. As a country, we have to get realistic about what services we can provide to these seniors based on their budgets.

Mace: Maybe the seniors housing industry will have to become more like the hotel industry with a spectrum of products. But 60% of the expenses are labor which is a big challenge. Do we need a different type of capital stack for a middle income product?

Herbst: The capital piece could become a less institutional product. Maybe it would be geared more for retail investors. There are a huge number of people turning 65 looking for fixed income in a world where yields are low. If middle- market seniors housing can lease quickly and stay leased, and generate a return even of below 5%, that’s not bad. Perhaps the product would be almost like a tax free municipal bond backed by the states.

Mace: If a pension fund is not going to earn double digit returns, does it matter to them that they are providing a service to constituents and having a social impact?

Brett: It still comes back to the rate of return. The goal is to invest on the merits of the return and also achieve a social impact. The return potential has to be there. A capital vehicle with a tax benefit is an interesting strategy, but I think it would be tough to package as a fixed income instrument from an institutional perspective.

Mace: What are some innovative ideas to create more seniors housing for the middle market? Could a mall, for instance, be converted into a seniors housing project?

Herbst: I think that would be interesting. We’ve looked at Class B & C office buildings in the suburbs that we could buy for $80 a foot and then renovate for seniors housing. We see more and more medical uses for empty mall space. With its enclosed areas, good for walking, a mall could be right for a rehab or assisted living facility. We need to think outside the box.

Audience Q: Where can we squeeze out extra cost when labor is 60% of the operating expenses?

Herbst: There are ways to make the operating model more efficient. Property taxes and food are a big part of operating costs. It might be possible to partner with programs such as Meals on Wheels which might also bring down dining room labor costs.

Mace: What about bringing in more volunteer labor? Church groups could volunteer or, say, volunteers could bank the time and then use it for themselves when they move into the building. More and more retired people want to be engaged with their communities and it might be a way to change the narrative while lowering labor expenses.

Herbst: Reducing the operating cost is the hardest part. We have to focus on reducing real estate taxes, bringing down development costs, and finding thoughtful ways to deliver services.

###

May 27, 2019

janekadler@gmail.com