NIC MAP® Data Service clients attended a webinar in mid-January on the key seniors housing data trends during the fourth quarter of 2018. Key takeaways included the following:

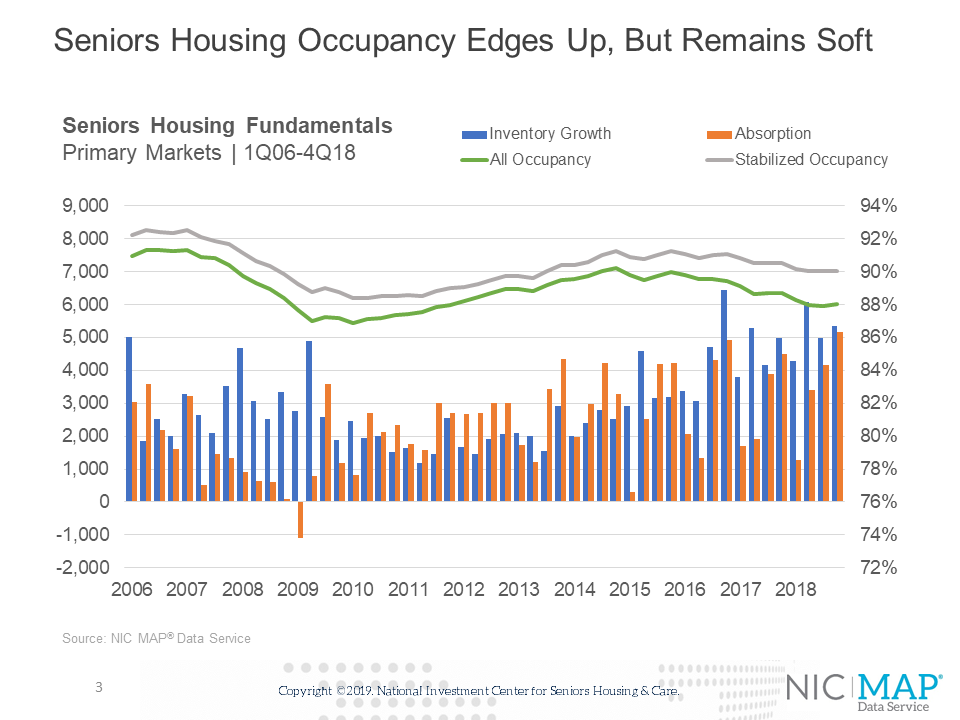

Takeaway #1: Seniors Housing Occupancy Edges Up, but Remains Soft

- The all occupancy rate for seniors housing, which includes properties still in lease up, inched up to 88.0% in the fourth quarter from the seven-year low of 87.9% in the third quarter. The fourth quarter rate was 70 basis points below its level of 88.7% in the fourth quarter of 2017.

- During the quarter, net absorption totaled 5,149 units, the greatest number of units absorbed in a single quarter since NIC began reporting the data in the first quarter of 2006. Historically, we often see a bounce up in demand in the fourth quarter from the third quarter and often the fourth quarter is the strongest quarter of the year.

- On a quarterly basis, there were 5,341 units added to inventory in the quarter, not as much as the record pace of 6,400 units reached two years ago, but still a lot by historical norms (3,100 units per quarter on average since 2006).

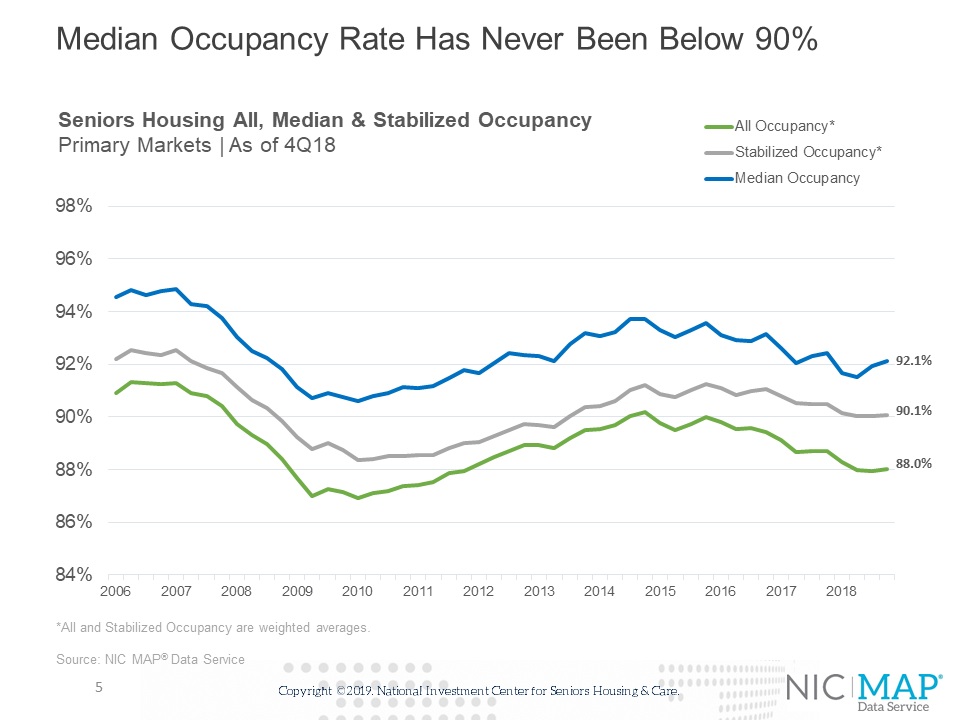

Takeaway #2: Median Occupancy Has Never Been Below 90%

- The median occupancy rate was more than four full percentage points above the all occupancy rate in the fourth quarter of 2018. It has averaged 350 basis points above the all occupancy rate since 2006 and has never fallen below 90%.

- The difference between the median and all occupancy rates can be traced to the fact that poorer performing properties pull down the average occupancy rate. Many institutionally-owned seniors housing properties benchmark to the median occupancy because of this fact.

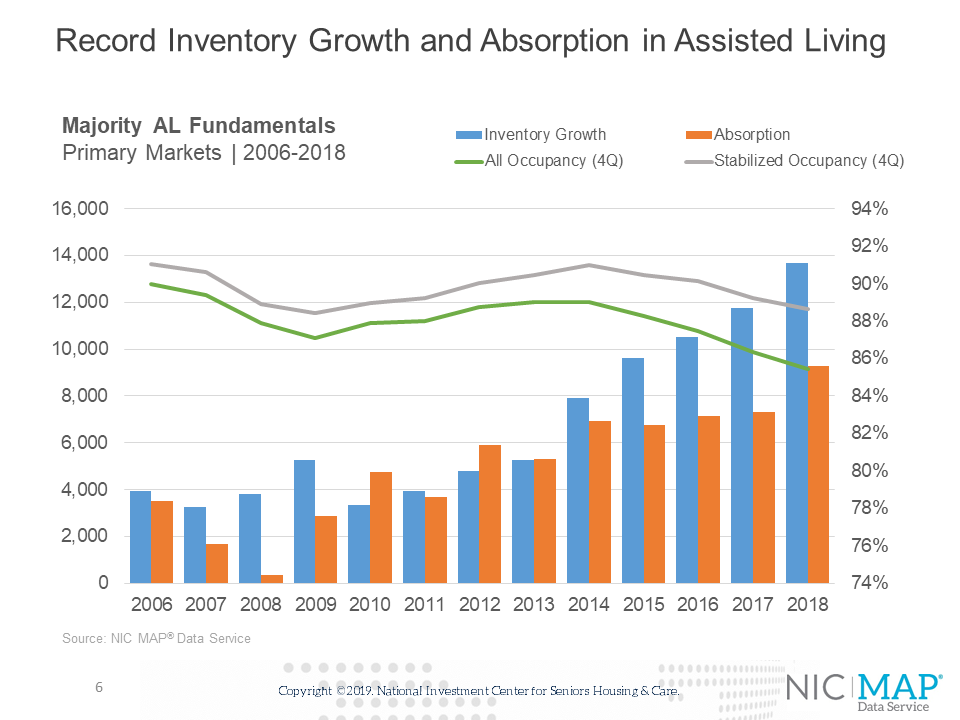

Takeaway #3: Record Inventory Growth and Absorption for All of 2018 for Assisted Living

- For all of 2018, assisted living net absorption equaled 9,283 units, the most in any year since at least 2006.

- Inventory growth also reached a record high of 13,670 units in 2018, making the gap between net absorption and inventory growth equal to 4,387 units, a bit less than the annual results for 2017 (4,473 units), but still very wide.

- Note the wide difference between stabilized and non-stabilized occupancy rates—nearly 320 basis points. This stems from the large number of units that have come online but are not yet leased up.

- It is also notable that net absorption equaled 3,743 units in the fourth quarter, which made the fourth quarter of 2018 the strongest quarter for net demand on record and more than three times the average net quarterly absorption since the time series began to be reported in the first quarter of 2006.

- Occupancy remains very low at a rate of 85.4% during the fourth quarter, which was unchanged from the third quarter. In the second quarter, the rate had reached an all-time low of 85.3%.

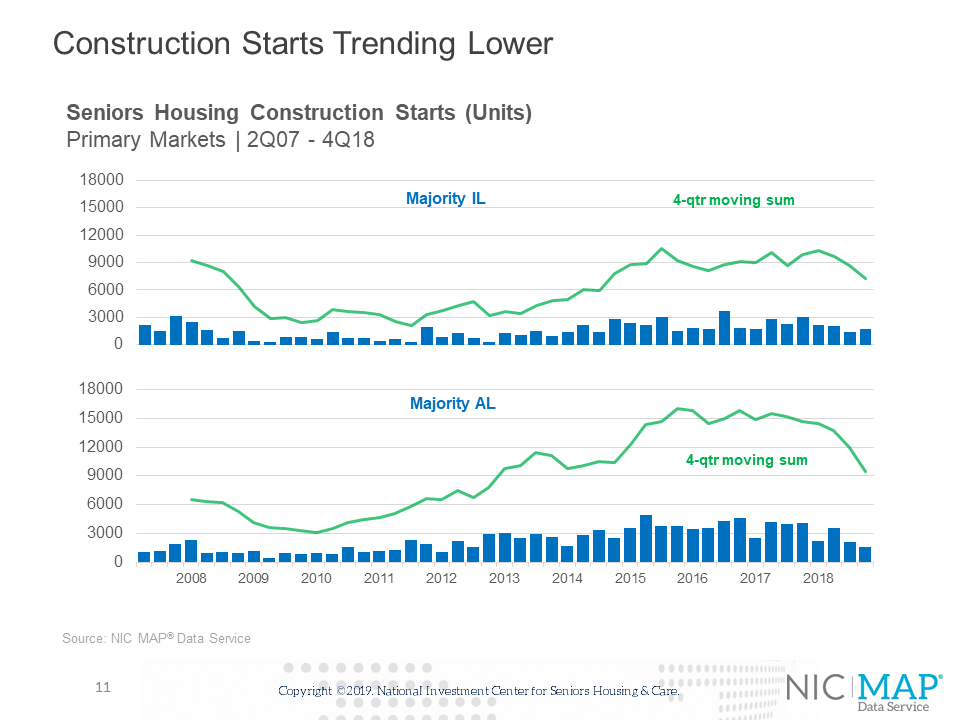

Takeaway #4 Construction Starts Trending Lower

- A key takeaway from the recent data is a slowdown in the four-quarter moving sum of starts for both majority independent living and majority assisted living. Indeed, in the fourth quarter, assisted living starts totaled nearly 1,552 units, the fewest starts since the first quarter of 2012. On a four-quarter aggregate basis, starts totaled 9,393 units, the fewest since 2014. As a share of inventory, this amounted to 3.3%. The last time it was below 4% was 2012.

- For independent living, starts on a rolling four-quarter basis, totaled 7,287 units in the fourth quarter. As a share of inventory, this equaled 2.2%. The last time it was below 2% was 2014.

- It’s worth noting that this data often gets revised up or down in subsequent quarters, due to inherent lags in reliably collecting this often hard-to-capture data.

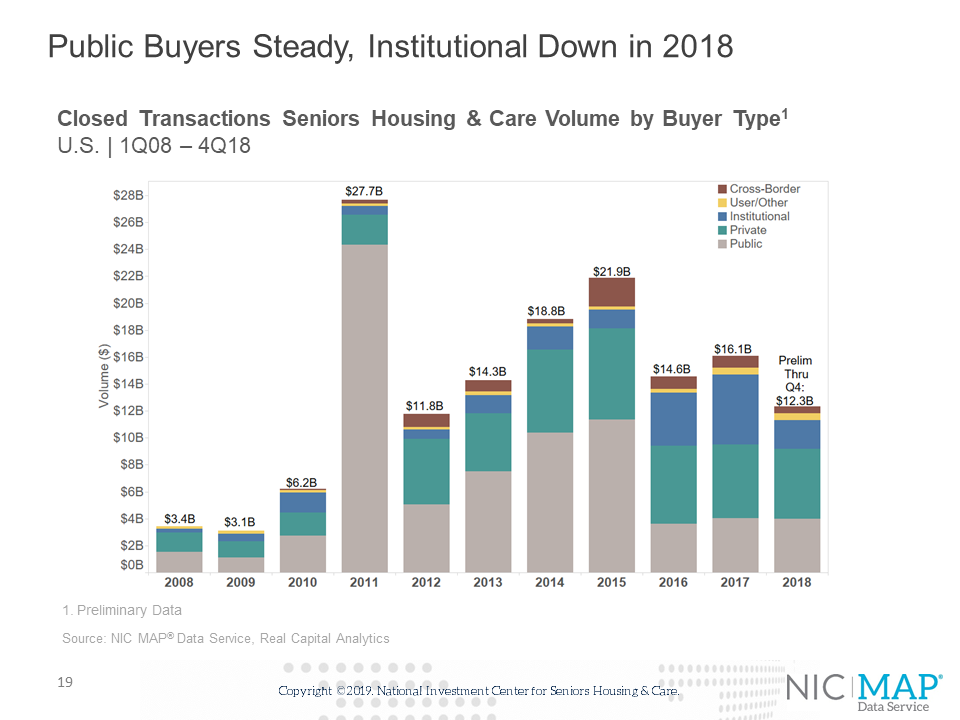

Key Takeaway #5: Seniors Housing and Care Transaction Volumes Less in 2018 Than In 2017

- Preliminary data shows that seniors housing and care transactions volume registered $12.3 billion in 2018. This includes $7.1 billion in seniors housing and $5.2 billion in nursing care. The total volume was down 23.4% from the previous year’s $16.1 billion and down 15% from 2016 when volume came in at $14.6 billion. Total annual closed transactions volumes have not been less than $13 billion since 2012.

- The institutional buyer type represented 17% of the $12.3 billion in closed transactions in 2018 as its total closed dollar volume decreased by 59% from 2017 when it represented 32% of volume and closed $5.2 billion in transactions. However, 2017 was represented in a significant way by Blackstone when they closed some larger deals over $500 million.

- The public buyer share of volume increased from 25% in 2017 to 32% in 2018. In terms of the dollar volume, it held relatively steady as the public buyer closed $4 billion in both 2017 and 2018. In 2018, the volume was carried by the Welltower/QCP deal and in 2017 it was carried by the SABRA/Care Capital Properties deal. The public buyer has averaged $3.8 billion in closed transactions per year over the last three years.

- The private buyer continues to be the most consistent and steady source of capital as it registered over $5 billion in closed transactions in 2018 at $5.2 billion. It represented 42% of all volume in 2018, which was up from 34% in 2017, when it closed $5.5 billion in transactions. Over the past three years, the private buyer has averaged $5.5 billion and it has closed above $5 billion in transactions for five straight years.

- Cross-border activity has seen a steady decrease in dollar volume since 2015 when it registered $2.1 billion. It has averaged about 5% of volume over the past three years and closed $500 million in 2018, which was down from 2017’s $900 million.