Keys to a Successful Middle Market Operating Model

Middle market senior housing is one of the toughest niche offerings to get right. Residents want quality care and lifestyle at a price they can afford, and operators need sustainable margins to make the model work. At Cardinal Senior Living, we have been able to create a middle market offering that leverages a highly efficient operating model with other strategic positioning to serve this growing cohort of older adults.

Below are what we see as key elements of our success.

1. Maximize 3rd shift. Overnight staff should not just monitor hallways. We train them to handle housekeeping and laundry while the residents sleep. It keeps day shifts free for direct care and cuts the need for dedicated housekeeping hours.

2. Leverage EBT (Electronic Benefits Transfer) cards. Many residents qualify for food assistance but do not use it. We help them apply and integrate those benefits into our dining program. It supplements our food budget, adds menu variety, and keeps costs in check without sacrificing quality.

3. Fight property taxes. Real estate taxes can crush middle market margins. We fight assessments aggressively. Every appeal, every exemption, every piece of data that supports our case. Lower taxes go straight to the bottom line.

4. Know your Medicaid waiver inside and out. Rules, rates, and eligibility vary by state—and they change often. We stay on top of every update, build strong relationships with caseworkers, and advocate for fair rates. Medicaid can be the difference between keeping a building full or letting rooms sit empty.

5. Use roommates strategically. For residents who cannot afford a private suite, we offer shared rooms at a lower rate. It keeps our census up, lowers cost per resident, and often gives residents the social connection they need to thrive.

Middle market success comes from doing the hard, unglamorous work, knowing every program, every regulation, and every lever to pull on expenses. It is not about cutting corners. It is about running smarter.

High Energy and High Impact: 2025 NIC Fall Conference

Ray Braun President & CEO / NIC

With its strong mix of educational sessions, networking opportunities, and Texas-style fun, the 2025 NIC Fall Conference once again demonstrated the power of bringing people together. Drawing nearly 3,200 attendees, the Conference was held Sept. 8-10 in Austin, Texas. It marked the 35th anniversary of the NIC Fall Conference and was the second largest event in its history.

“NIC conferences remain the premiere gatherings for industry executives to network and gain insights on current industry conditions,” said NIC CEO Ray Braun. “This underscores both NIC’s role as the sector’s leading convener as well as the momentum driving senior housing today.”

The Conference theme—Rising Demand, Expanding Opportunity—highlighted the industry’s enviable position. Consumer demand is quickly outpacing current supply. New investors are jumping into the sector while experienced owners and operators are expanding and fine-tuning their approaches. One conference participant characterized the current senior housing sector as enjoying a “Goldilocks moment.”

At the same time, the industry faces challenges to address the affordability gap and changing consumer preferences. And while additional supply is vital, capital constraints and cost escalations continue to slow new development.

Rich and Robust Programming

Ground-breaking research was introduced at the Conference. NIC again partnered with NORC at the University of Chicago, building on previous studies, to determine the value of senior housing, including for those living with dementia.

Bob Kramer Co-founder & Strategic Advisor / NIC

The results show improvements in frailty and stability the longer the resident lives in senior housing. In fact, the number of hospitalizations and readmissions were reduced, providing relief for family caregivers, and establishing timely access to care in a supportive environment, ultimately leading to greater longevity.

Lisa McCracken, NIC Head of Research & Analytics, led a panel discussion on the latest NORC research and the implications for senior housing. Panelist Tom Cassels, managing director at Manatt Health, commented, “Senior housing communities bend the trend to be proactive about health.”

Sharing his deep knowledge and extensive expertise, NIC Co-Founder and Strategic Advisor Bob Kramer led a “lessons learned” panel of highly experienced executives on how to prepare for the future of senior living. “By looking back at the past 30 years of growth in our industry, we’re presenting six lessons learned from both the successes — they’ve been notable — and the mistakes and failures so that hopefully we can all be wiser in the next growth cycle,” said Kramer. One lesson: Develop your business model starting with the customer you plan to serve and how you plan to serve them.

The Conference featured a total of 12 educational sessions, curated to provide actionable insights. “You can always take away something from all of the educational sessions,” said attendee Katrina Resch, executive assistant at Priority Life Care.

Highlights from other sessions included:

Experts provided an update on capital markets and valuations: Where they are now and where they’re headed. “The additional capital coming into the sector will allow us to tackle the housing demands that are on the horizon,” said KeyBank Senior Vice President Morgin Morris.

An outlook on policies directly impacting the sector from the new administration in Washington, D.C.

Economist Wendy Edelberg unpacked the domestic and global economic playbook, spotlighting the indicators to watch.

Growing sources of new capital such as family offices, donor-advised funds and pension funds. “It might be hard to understand the space, but understanding the demographics is easy,” said Citrine Investment Group, Founder & President, Lynn Jerath.

New products and new marketing messages for the older consumer—roadmaps to connect with the next generation of older adults.

Overcoming barriers to new development. “The opportunity is significant,” said Stuart Jackson, executive vice president at Greystone.

As part of a session spotlighting the mission and heart of senior living, participants previewed the award-winning documentary Familiar Touch. The film is set in an actual assisted living community and brings the emotional realities of aging and memory loss to life from the perspective of the residents, families and caregivers. The viewing was followed by a panel discussion with the film’s director on the impact of person-centered care.

Lynn Jerath Founder & President | Citrine Investment Group

The Conference also featured seven Innovation Labs where participants came together for hands-on, interactive workshops. Popular topics included data driven insights, healthcare partnerships, and real-world AI solutions.

Attendees enjoyed a number of networking opportunities to engage in value-driven conversations, share lessons learned and grow productive relationships. Several Texas-themed receptions offered a relaxed and vibrant atmosphere. And yes, there were cowboy hats and country music.

“The NIC Fall Conference has allowed us to make connections with other operators, vendors, and people in our network. Everyone is in one place and in one city,” said attendee Laura Bierman, sales executive at Procare HR.

Stuart Jackson Executive Vice President | Greystone

Conference details were thoughtfully planned. Attendees enjoyed café-style meals, a specialty coffee bar, headshot lounge and relaxation station, among other perks.

A women’s meetup and first-time attendee gathering showcased the industry’s evolution and expansion. NIC’s Braun noted that over 500 attendees at the Fall Conference were first-time registrants, along with 150 new companies including many new capital providers.

“NIC continues to fulfill our mission of providing access and choice to older adults,” said Braun. “We foster relationships for the senior housing and care industry; produce groundbreaking research and analytics; develop next generation leadership; and showcase opportunities.”

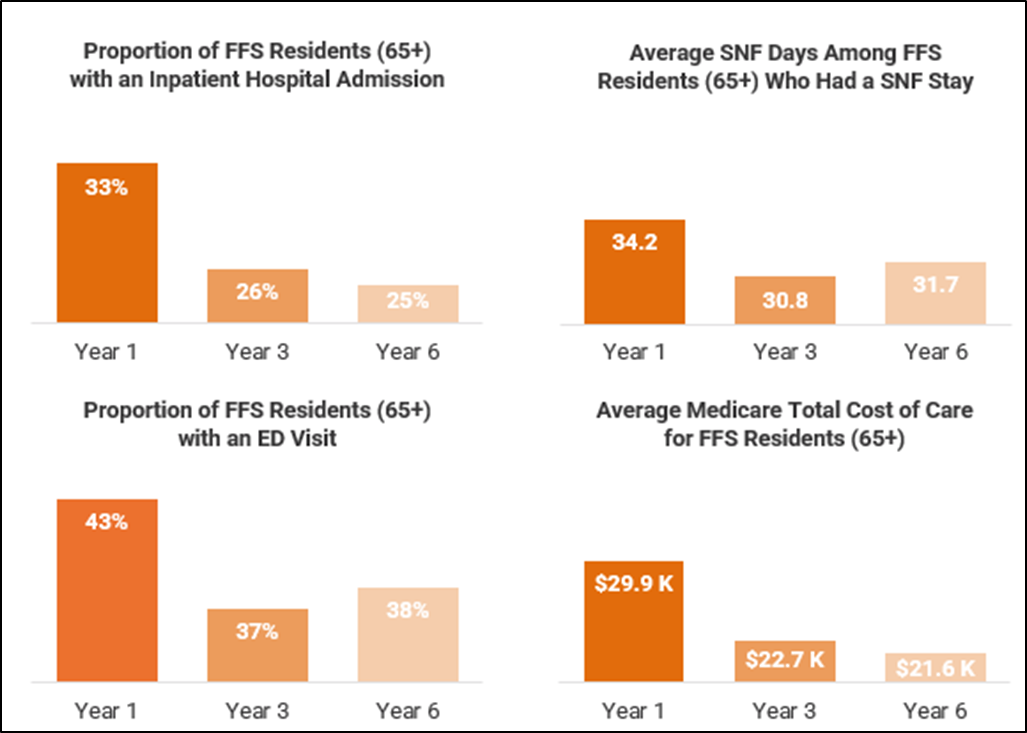

Senior Housing Can Reduce Acute Care Services Needs for Older Adults

New research shows that senior housing’s preventative approach to care contributes to increased quality of life for residents and reduced healthcare costs over time. The analysis was conducted by NORC at the University of Chicago (NORC) and supported by NIC.

Researchers assessed the sustained impact senior housing has on residents’ health and medical costs and found that older adults who remain in senior housing utilize less acute care services and see their health stabilize for several years after moving in.

* FFS refers to Medicare fee-for-service claims data; see Methodology in full report.

Researchers also found that senior housing can promote health and wellness of residents with neurodegenerative diseases(NDD) by reducing the number of hospitalizations and readmissions, providing relief for family caregivers, and enabling timely access to care in a supportive environment, ultimately leading to greater longevity.

Key takeaways:

Approximately one in four residents had a hospital admission in year three, compared to one in three in the first year.

The proportion of residents with an emergency department visit declined by 14% from year one to year three.

Average total Medicare costs per patient were $7.2K lower in year three than in year one.

Top-performing senior housing communities created greater stability and safety for residents with NDD by reducing hospital visits, stays and readmissions—as well as lowering costs.

These findings suggest that senior housing continues to improve residents’ health and well-being for several years post move-in as operators provide effective and efficient solutions that help address unique healthcare challenges.

The research is part of an ongoing initiative led by NIC, in collaboration with NORC, to assess how senior housing supports the health and well-being of older adults. For full methodology and findings, click here.

Future Leaders Council Celebrates Graduates and Welcomes New Members

NIC extends heartfelt congratulations to the Future Leaders Council (FLC) Class of 2025, who celebrated their graduation during the NIC Fall Conference in Austin, Texas. Over the course of their three-year term, these leaders advanced NIC’s mission by contributing to strategic projects, serving on committees, and sharing their expertise through meaningful content and programming.

Madisen Medley, Chair – Vice President, Business Development, Merrill Gardens

James Estes, Vice Chair – Vice President, Asset Management, Sunrise Senior Living

Andrew Katzmann – Vice President, Finance, Juniper Communities

Brandon Phillips – Vice President, Artemis Real Estate Partners

Alongside honoring the graduates, NIC is pleased to welcome the incoming FLC members:

Dushyanth “D” Biyyala – Head of Growth, Sage

Grant Blosser – Managing Director, VIUM Capital

Robb Cozad – Vice President, Investments, Ventas

Mary Kate Cruise – Vice President, Acquisitions, AEW Capital Management

Jeff Durkin – VP New Product Development, NIC MAP

Graham Johnson – Vice President, Investments, LCS

Panayoties “Peter” Kravaritis – VP Asset Management, Sunrise Senior Living

Jacob Swint – VP, Strategic Growth & Operations, National Church Residences

Avery Wallace – Manager of Capital Partnerships, Inspiren

Lexi Zager – VP of Financial Planning & Analysis, Belmont Village Senior Living

The 2025–2026 FLC Leadership Team will guide their peers, collaborate with NIC staff, and champion the FLC’s initiatives in the year ahead:

Brittany Spicer, Chair, Assistant Vice President, National Health Investors

Morgan Graphman, Vice Chair – Director of Business Intelligence, Ascent Living Communities

Ilya Gaev, Vice Chair, Partner, HealthTrust

Mike McMillen, Vice Chair, Executive Vice President of Sales, SafelyYou

“The Future Leaders Council (FLC) was established by the NIC board in 2009 to develop the next generation of volunteer leadership for the organization. Selected through a highly competitive application process, FLC members represent the diversity of perspectives and areas of expertise essential to design, develop, finance and operate the next generation of senior housing and care products. The relationships formed, the knowledge gained, and the leadership skills developed (or ‘honed’) by FLC members during their three-year terms provide a strong foundation for the future of NIC and for the future of the entire senior housing and long-term care industry.” – Bob Kramer, NIC co-founder and former CEO and Chair of the FLC Advisory Committee, current board member and strategic advisor.

NIC sincerely thanks all current and incoming FLC members, and their organizations, for supporting leadership growth and advancing NIC’s mission to expand access and choice for America’s older adults.

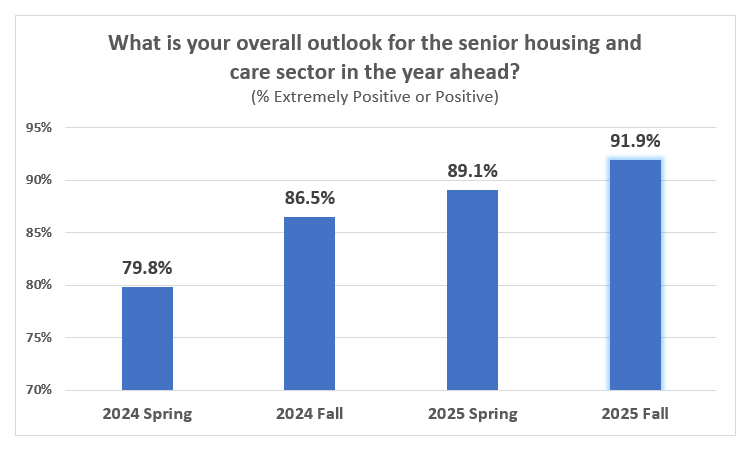

Roughly 3,200 senior housing and care operators, investors and industry professionals traveled to Austin, TX earlier this month to attend the 2025 NIC Fall Conference. Upon check-in, all registrants were asked to rate their overall outlook for senior housing and care in the year ahead. This NIC Industry Sentiment Poll was first launched at the 2024 NIC Spring Conference and has been repeated at each major NIC conference ever since. As detailed in the graph below, the overall outlook of industry participants is the highest it has been since the poll’s inception.

Ninety-two percent (92%) of the almost 2,900 respondents reported an “Extremely Positive” or “Positive” outlook for the year ahead, which is 2.8% above the industry sentiment measured just six months ago at the NIC Spring Conference. Despite acknowledged headlines related to potential tariff impacts, subdued development activity, and a potential supply-demand gap, the energy and optimism were evident throughout the three days of the conference.

The NIC Research and Analytics team will once again measure the industry outlook at the 2026 NIC Spring Conference scheduled for March 30-April 1in Nashville, TN. Be on the lookout for registration information later this year.

We use cookies on our website to give you the most relevant experience by remembering your preferences and repeat visits. NIC's privacy policy can be viewed here. By clicking “Accept”, you consent to the use of ALL the cookies.

This website uses cookies to improve your experience while you navigate through the website. Out of these cookies, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may have an effect on your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Functional cookies help to perform certain functionalities like sharing the content of the website on social media platforms, collect feedbacks, and other third-party features.

Performance cookies are used to understand and analyze the key performance indexes of the website which helps in delivering a better user experience for the visitors.

Analytical cookies are used to understand how visitors interact with the website. These cookies help provide information on metrics the number of visitors, bounce rate, traffic source, etc.

Advertisement cookies are used to provide visitors with relevant ads and marketing campaigns. These cookies track visitors across websites and collect information to provide customized ads.