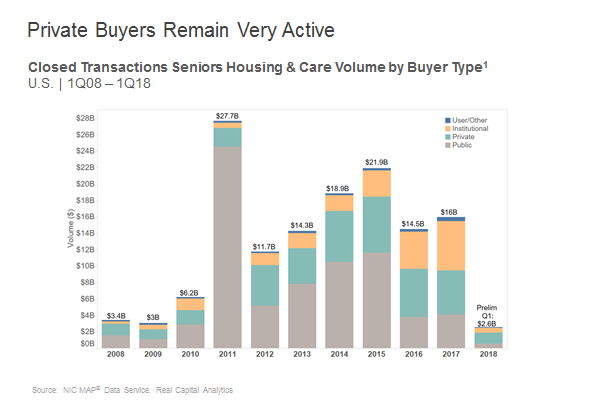

Seniors housing and care updated transactions figures show a total of $2.6 billion closed deals in the first quarter of 2018. That includes $1.7 billion of seniors housing, and $900 million in nursing care transactions. The total volume was down 5% from the previous quarter’s $2.7 billion, and down 45% from the first quarter of 2017 when volume totaled $4.7 billion.

The central theme of the first quarter of 2018 is that activity by private buyers—which include any company that is not publicly traded, e.g. a private REIT or single owner or partnership, family offices, etc.—continues to be very consistent. The first quarter of 2018 represented the 19th consecutive quarter of more than $1 billion in closed transaction volume by private buyers, totaling $1.3 billion. With only $2.6 billion closing in the first quarter overall, private buyers represented half of all closed volume. Private buyer volume was up 9% from the fourth quarter of 2017. However, it was down 8% from a year ago in the first quarter of 2017 when volume registered $1.4 billion.

As far as the other buyer types, both public and institutional buyers each closed on about $600 million worth of transactions in the first quarter. Public buyers registered $547 million in transactions and institutional buyers totaled $606 million. The public buyer represented 21% of total volume in the first quarter, an increase from a year ago in the first quarter of 2017 when it represented only 9% of volume. The institutional buyer represented 23% of the total volume in the first quarter of 2018, which was down from 55% a year ago.

Institutional buyer volume was down 41% from the last quarter when volume registered $1.0 billion. Volume was down 76% from a year ago in the first quarter of 2017 when institutional buyers registered an unusually high amount of volume for a first quarter at $2.6 billion. The first quarter of 2017 was the highest closed volume for the institutional buyer going back to 2008, primarily because of several large Blackstone transactions.

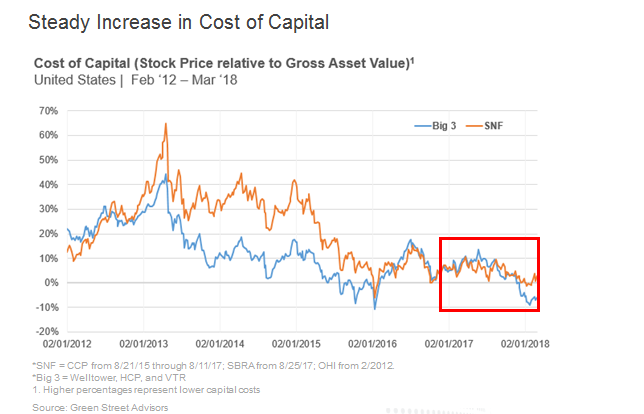

Public buyer volume was up 36% from last quarter, although from a relatively small base of only $403 million, and up 26% from a year ago, again from a relatively small base of only $433 million. The public buyers have had a harder time competing for deals as their cost of capital has significantly increased over the past year. Below is a graphic which is a good measure of the cost of capital within the sector for the public markets. The orange line represents skilled nursing and includes the cost of capital of Sabra Health Care REIT and Omega Healthcare Investors. The blue line represents seniors housing and includes the “Big 3” healthcare REITs: HCP, Ventas and Welltower.

This graphic shows the premium at which the stocks are trading relative to their gross asset value. That means when the REITs trade at a premium to asset value (asset value is based on the private market capitalization rates and the REIT’s portfolio holdings) then the REITs can go out and buy properties by raising equity and realize an instant increase in value because the private market value is lower than their publicly traded equity value. In other words, their cost of capital is low when the premium is high. This can basically be an arbitrage play when these stocks are trading at high premiums. As seen here starting in 2013, the premium began to trend down, which in turn effectively raised their cost of capital making it harder to pay higher prices for properties. This premium took another leg down in 2015, which is reflected in closed transaction volume as public REIT activity decreased dramatically after the second quarter of 2015 and continued to decline through 2017. Now, well into 2018, we see a significant decrease in the premium and, in fact, it turned negative for seniors housing at nearly -10% in the first quarter 2018.

As private equity is still relatively active in the markets and pricing still remains strong, many public REITs are finding it harder to compete for properties, especially larger portfolios. Anecdotally, many deals closed by public REITs include existing operator relationships.