The following analysis examines broader occupancy trends, year-over-year changes in inventory, and same-store asking rent growth – by care segment – within 1,043 Continuing Care Retirement Communities (CCRCs) and 13,737 non-CCRCs in the 99 NIC MAP Primary and Secondary Markets.

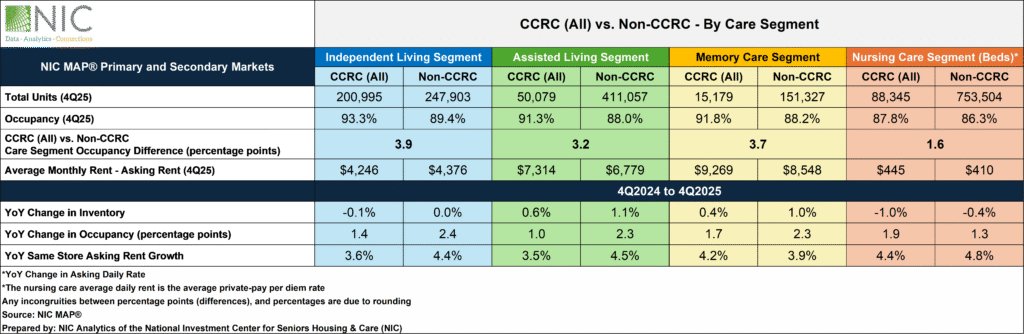

4Q 2025 Market Fundamentals by Care Segment – CCRC (All) vs. Non-CCRC

The exhibit below compares the market performance of CCRCs and non-CCRCs by care segment for the fourth quarter of 2025, highlighting year-over-year changes in occupancy, inventory, and asking rent growth.

Occupancy. Consistent with prior quarterly results, CCRCs continued to outpace non-CCRCs in occupancy rates across all care segments. The largest occupancy difference between CCRCs and their non-CCRC counterparts in the fourth quarter of 2025 was in the independent living segment (3.9pps), followed by memory care (3.7pps) and assisted living (3.2pps) segment, with the smallest gap in the nursing care segment (1.6pps). The independent living segment recorded the highest occupancy rate among both CCRCs (93.3%) and non-CCRCs (89.4%).

Non-CCRCs recorded higher year-over-year occupancy change in all care segments except for the nursing care segment, with independent living recording the highest change from the past year (2.4pps). While CCRCs overall have higher occupancy, the occupancy growth has been slower in recent quarters than the non-CCRC communities.

Asking Rent. In reference to the table above, the average monthly asking rent (in dollars) for CCRCs continues to be higher than that of non-CCRCs across all care segments except for the independent living segment. CCRCs showed higher year-over-year rent growth in the memory care (4.2% to $9,269) segment. Non-CCRCs experienced stronger year-over-year rent growth in nursing care (4.8% to $410*) followed by the assisted living (4.5% to $6,779) segment.

Note, these figures represent asking rates and do not reflect any discounts that may be applied. The nursing care average daily rent is the average private pay per diem rate.

Inventory. Compared to the level a year ago, nursing care inventory declined in both CCRCs (1.0%) and non-CCRCs (0.4%), the largest drops among the care segments. Among CCRCs, positive inventory growth was seen in assisted living (0.6%) and memory care (0.4%), while independent living edged down slightly by 0.1%.

For non-CCRCs, the strongest year-over-year inventory growth was recorded in assisted living (1.1%) and memory care (1.0%) segments, while independent living remained unchanged, and nursing care declined.

Negative inventory growth can occur when units or beds are temporarily or permanently taken offline or converted to another care segment, offsetting any newly added supply.

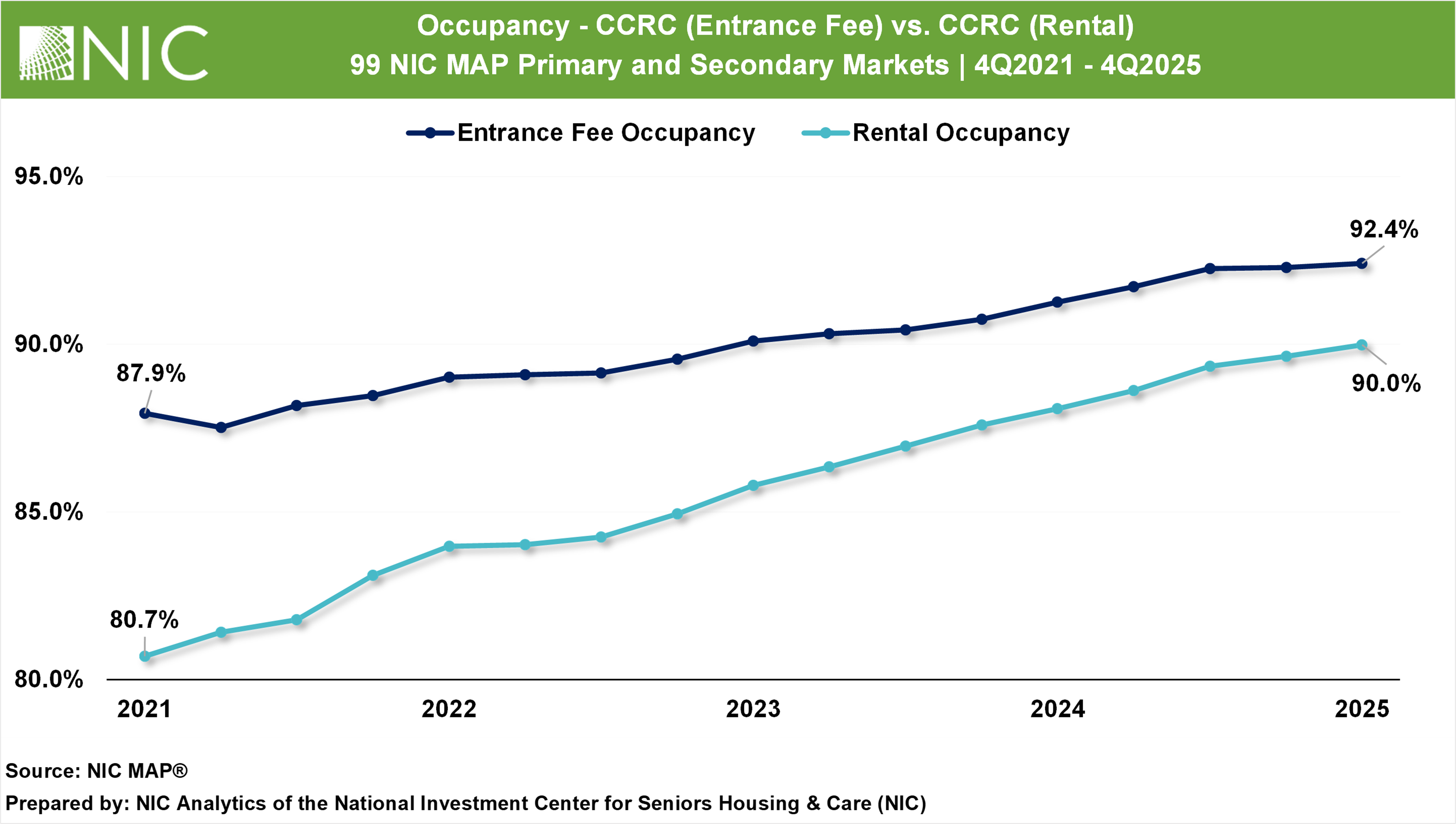

A Five-Year Look at Occupancy in CCRC Models: Entrance Fee vs. Rental CCRCs

While entrance fee communities maintained a higher occupancy rate in the fourth quarter of 2025 at 92.4%, compared to 90.0% for rentals, the gap is narrowing as rental occupancy growth accelerates. In the fourth quarter of 2025, rental CCRCs posted 1.9 percentage points of year-over-year occupancy growth compared to a 1.2 percentage point gain in entrance fee communities.

This occupancy growth differential reflects a larger trend. Since the fourth quarter of 2021, rental CCRCs have experienced faster occupancy growth compared to entrance fee models, accumulating 9.3 percentage points of growth, more than double the 4.5 percentage point gain in entrance fee CCRCs over the same period. This has translated into average annual occupancy gains of roughly 1.1 percentage points for entrance fee CCRCs and 2.3 percentage points for rental CCRCs over the four-year period.

While occupancy across both CCRC models continued to move higher and end 2025 at strong levels, the gap in occupancy between them is gradually narrowing.

Look for future articles from NIC to delve into the performance of CCRCs.