Top Lender Still Bullish On Seniors Housing Mission: A Conversation With Fannie Mae’s Roosevelt Davis

Roosevelt Davis

It’s easy to forget that a big lender like Fannie Mae is a mission-driven enterprise. That’s one point Roosevelt Davis emphasizes in his role as director, seniors housing production, Fannie Mae, Washington, D.C.

In a recent conversation with NIC chief economist Beth Mace, Davis discussed Fannie Mae’s mission to fill the critical need for debt financing to create housing for the growing number of aging Americans. They also addressed current market dynamics and the labor shortage, along with the practical details of how to work with Fannie Mae.

Here is a recap of their conversation.

Mace: Can you tell us about yourself and your role at Fannie Mae? How long have you been there?

Davis: I’ve been in the seniors housing space for about 20 years, and in my current role at Fannie Mae for the last 10 years. I am director of the seniors housing finance team. I am responsible for seniors housing lending and borrower relationships.

Mace: How long has Fannie Mae been involved in the seniors housing and care sector? Why did it enter the space?

Davis: Fannie Mae has been lending in the stabilized seniors housing sector since 1998. Our mission revolves around the need for housing. Fannie Mae entered the space to serve a critical need for our country’s aging population. The seniors housing team is in the Multifamily Division. We wanted to play a role in serving that critical need. We have a dedicated team here who knows the business inside and out from the finance side to asset management.

Mace: What are the opportunities as well as the challenges you see for the seniors housing and care sector, in both the short-term and long-term?

Davis: From our perspective, the long-term demographic trends associated with the aging population are hard to ignore. I believe seniors housing has performed well through all economic cycles. And one of the major contributing factors is that seniors housing has a needs-based component. In a good market or bad market, there is a need for this type of housing, particularly for those in assisted living, memory care and skilled nursing.

The market faces some challenges. There are definitely some new entrants to the seniors housing space that are chasing yields but are underestimating the operating expertise needed to provide quality care to residents. New entrants may not have a full understanding of the intensity of operations. I think, as baby boomers continue to age, opportunities for seniors housing and care providers will grow and expand across most markets. But the silver tsunami has not hit yet, and we are definitely seeing an oversupply in some markets which is causing occupancy rates to fall.

Some of the older assets are struggling to compete with the newer assets coming into the market. From our perspective, important questions in the long run are: How will older assets remain competitive? Will older assets be able to compete with the latest technology and amenities provided by newer assets?

Topping my list of concerns affecting the industry today is the labor issue—the ability to recruit and retain talent. Given the low unemployment rate, this is a huge challenge for our industry. In addition to labor, you can add in the labor costs. Low unemployment and the rise of minimum wage rates in certain states make it more expensive to recruit and retain good workers.

Mace: Some people are walking away from deals because of the labor market considerations. Do you look at a deal today differently than you did in the past because of the labor issue?

Davis: Absolutely, one of the questions I ask is: What is the rate of employee turnover? If it’s high, that’s a sign there are labor issues with that property or in that market. I am also looking at how long the executive director has been at the property and their level of experience. Successful operators build a culture that pays a lot of attention to the staff, creating a place where they’d like to work. That fosters worker longevity. If you take care of employees, they will take care of residents.

Mace: Do you provide debt financing to all seniors housing segments, and to both nonprofit and for-profit providers?

Davis: We offer financing for the breadth of acuity levels: independent living, assisted living, dementia care, and a combination of the three. We have the ability to finance for-profit and nonprofit borrowers, though the majority of our financings are with for-profit borrowers. We also finance continuing care retirement communities (CCRCs), and in those properties, we allow a small proportion of skilled nursing units. In considering CCRCs, we are relatively conservative in evaluating those transactions, recognizing the risks associated with them. But most of our transactions are independent living, assisted living, and memory care. We do not favor one or the other, but we recognize that each segment has its own risk.

Mace: What are some of those risks?

Davis: As you go up the acuity level, there is a need for a certain expertise. The staff at an assisted living or memory care community has to be able to offer the right services. We do finance stand-alone memory care properties, but we are keeping an eye on that segment because we have definitely seen some softness in that space.

In particular, it’s hard to get a handle on combination buildings that offer assisted living and memory care. An owner may add a wing of memory care units—what I call the “shadow market.” When you’re trying to do your research, you’re basically looking at stand-alone memory care numbers, but you’re not taking into account other properties that may be adding memory care units which has caused some softness in that space.

Mace: Do you provide debt only for existing, stabilized purpose-built properties, or do you provide construction financing as well?

Davis: We only provide debt for existing stabilized purpose-built properties. We provide financing for acquisitions and refinancings, including refinances of construction and bridge loans for properties that have been recently stabilized and are seeking long-term permanent debt.

Mace: Can you tell us how Fannie Mae works with Delegated Underwriting and Servicing (DUS®) lenders? Is all of your senior housing lending through DUS lenders?

Davis: We rely on our approved seniors housing DUS lenders to deliver seniors housing mortgage loans to Fannie Mae, so you cannot deliver a seniors housing loan to Fannie Mae unless you are an approved DUS lender. We are proud of our Delegated Underwriting and Servicing model. It has stood the test of time and performed well through all market cycles. Our lenders know our underwriting requirements and have a good understanding of our risk tolerance. What makes our model unique is that we are risk-sharing partners, so lenders retain a portion of the risk in each loan. This enhances the performance of our book of business, assures alignment across all parties, and creates stronger relationships.

Mace: Does Fannie Mae do its own underwriting?

Davis: We look at the underwriting from our DUS lenders. The “D” in DUS stands delegated, and delegation is the cornerstone of our model. We provide underwriting guidelines and communicate our risk tolerance to our lenders so they can take the lead on underwriting. My team reviews the lender’s underwriting to make sure we understand and can support the lender’s approach. The delegation allows for faster decisions, certainty of execution and quicker closings.

Mace: Does Fannie Mae keep the loans on its books?

Davis: We don’t hold debt on our books. Each seniors housing loan is securitized in a single mortgage-backed security and purchased by a mortgage-backed security investor, shortly after closing.

Mace: What are the different financing options you offer?

Davis: We can offer fixed-rate or floating-rate loans. The latest buzz in seniors housing right now is “green” financing. It started on the multifamily side, and over the last two years, we’ve been doing more “green” financing in seniors housing. Fannie Mae is an industry leader in supporting better quality housing that has a positive measurable financial, social, and environmental impact on the greater housing stock in U.S. “Green” refinancings allow borrowers to tap into more proceeds at lower pricing if they agree to make the upgrades necessary to save energy or water consumption. Lower pricing may also be available for properties that have received an eligible green building certification.

Mace: What share of your lending is in the “green” program?

Davis: We have seniors housing loans in the “green” space totaling more than $300 million. Our total book of business in seniors housing is about $15 billion.

Mace: What is the average loan-to-value (LTV) ratio today on your loans?

Davis: Our maximum LTV is 75 percent. Most deals this year have been in the 60-75 percent range.

Mace: Are your loans recourse or nonrecourse loans?

Davis: Nonrecourse.

Mace: Does that put Fannie Mae at risk?

Davis: Yes, a certain amount of risk goes along with that. But nonrecourse lending has not been a major risk for us. Our DUS lenders have a strong understanding of our underwriting guidelines, and our sponsor vetting process is good. We’ve done business before with many of the sponsors. Our seniors housing portfolio has performed extremely well. We do have what we call “bad boy acts” –such as waste, fraud, bankruptcy—which can result in recourse.

Mace: Are your operations national in scope, or are there areas of the country that you avoid?

Davis: We are national in scope and do not avoid any areas. Each deal is local, and we analyze each deal individually. We want to know what is going on within a 10- mile radius, whether there’s new construction or properties being planned. We totally focus on the property in its local market.

Mace: Do you provide financing for the cash-flow side of the business, such as for hospice or other services?

Davis: We finance only existing real estate.

Mace: What do you look for in a good sponsor?

Davis: The first and most important characteristic that we look for in a sponsor is one that has a genuine interest in providing quality care for the residents they serve. It doesn’t matter how beautiful the property is. If the owner does not have a true desire to understand and meet the needs of the people being served, then that is a problem for us.

Mace: How can you determine that?

Davis: Since we’ve been in business since 1998, we have a large book of business. We have a lot of experience with owners, operators, and borrowers who are out there in the market. We have the ability to watch their loans and how they’ve been performing on our books. We conduct site visits and meet with the sponsor and get an understanding of their business plan and strategies. The biggest test for us is a live site inspection, meeting the sponsor, and seeing how that property has performed. Performance is the key. At the end of the day, we make loans and we want them repaid.

Mace: Is there an opportunity for a new sponsor to come in?

Davis: Absolutely, we like to get an understanding of their experience and background. If they are new to seniors housing, we want to know why they are entering the space. We ask a lot of questions: What are their motivations? Are they truly in the business to provide care? We want to get a better understanding of their plan and vision for owning and operating properties.

Mace: What was your debt volume in 2017 and year-to-date in 2018?

Davis: Last year was a historic year for us. We did $5.5 billion, which was amazing. Our biggest year before that was $2.7 billion. Over the past 10 years, on average, we do about $1.5 billion. We get a lot of our production in the last half of the year.

Mace: Why was last year so strong?

Davis: We had a lot of refinance opportunities and a lot of big transactions.

Mace: Is Fannie still under conservatorship? What does that mean?

Davis: Fannie Mae has been under conservatorship since 2008. Basically, the Federal Housing Finance Agency (FHFA) used its authority to place Fannie Mae and Freddie Mac under conservatorship because of deterioration in the housing market during the Great Recession which damaged our financial condition. The overall goal of conservatorship is to help restore confidence in our enterprise and enhance our capacity to fulfill our mission and mitigate any systemic risk that would contribute to the instability in financial markets.

There is a lending cap of $35 billion on Fannie and Freddie for multifamily lending. Seniors housing is subject to that volume cap, but the FHFA will exclude a pro rata share of loan amounts based on the percentage of units that are affordable at 80 percent of area median income or below. A lot of our loans are considered affordable because affordability is based on the area median income in the census tract. That’s different from how conventional multifamily mortgages are evaluated. Those mortgages are based on monthly rent. But in the senior housing space, rent includes food, housekeeping, and other services.

Mace: Any worries that keep you up at night?

Davis: Labor is a huge issue in our industry that we need to resolve. The recruiting and retaining of good labor, and increased labor costs are going to reduce margins at these properties.

The lack of affordable seniors housing is something we as an industry need to figure out. Everyone plays a role—the lenders, providers, owners, operators, cities, and states. As people continue to age and the aging population increases, we need to figure out how to solve the affordable seniors housing conundrum and provide housing for those who need less expensive options.

Mace: Other thoughts?

Davis: Seniors housing is a great industry, and I’m grateful to provide a role in financing seniors housing properties.

NIC Blog Post: Announcing Gary Cohn as NIC Fall Conference 2018 General Session Speaker

Newt Gingrich, Larry Summers, Ben Bernanke, and Timothy Geithner have all presented at the NIC Fall Conference in recent years with the sharp observations and timely insights that can only come from top government officials. These speakers provided their unique perspectives to NIC’s seniors housing and care executive audiences.

This year’s upcoming conference continues NIC’s tradition of featuring nationally prominent speakers. NIC has announced that the opening general session of the 2018 NIC Fall Conference will feature a conversation with the former Director of the National Economic Council and the former President and COO of Goldman Sachs, Gary Cohn.

As seniors housing and care navigates a shifting market and evolving economy, its leading decision makers face a number of potential business challenges, such as the impact of a tight labor market, increasing wages, and rising interest rates.

Cohn will share his insights and observations on the U.S. economy and where it is headed as the influences of a changing global economy, more restrictive monetary policy, and tax reform take root. He will also speak to his views on the potential impact of tariffs on trade, the economy, and inflation; today’s very tight labor market, including staffing challenges for business expansions; regulatory, healthcare, and immigration reform; and the direction of interest rates.

Cohn’s insights on where today’s economy is taking us promise to be highly relevant to our conference attendees, while effectively highlighting the 2018 NIC Fall Conference theme: “Navigating the Present Market and Anticipating the Future.”

The 2018 NIC Fall Conference will be held October 17-19 at the Sheraton Grand Chicago. (Click here to register.)

How Am I Changing the Future of Aging?

Fall Conference NIC Talks

At the 2018 NIC Fall Conference, the highly popular NIC Talks—a series of 12-minute TEDx-style Talks designed to be thought-provoking and perhaps challenge the way people think about aging—returns with seven outside experts and an industry leader all addressing the topic “How am I changing the future of aging?” Below are descriptions for four of this year’s NIC Talks, with the four remaining NIC Talks being highlighted in next month’s issue of the Insider.

Caring as Wise Improvisation

As executive director of Insights and Applied Improvisation at the famed Second City and Second City Works, Kelly Leonard has helped develop the improvisational talents of Tina Fey, Stephen Colbert, Amy Poehler, Seth Meyers, Steve Carell, Keegan Michael Key, and Amy Sedaris among others. After finding himself in tears upon failing to connect with his mother with dementia, Kelly discovered that improvisational skills can be used to successfully engage with Alzheimer’s patients. He tells his story, shares his “Yes, And” method, and discusses the impact of applying improv in the caregiving community.

Connected Intelligence – The Technological Revolution You Need to Know About

Chetan Sharma is fascinated by technology, having written a dozen best-selling books on wireless. He is turning his eye towards seniors housing and care to see how connected intelligence—the Internet of Things—will shape aging and care in the coming decades. He will take you into his world of the Connected Intelligence ecosystem to see exactly how 5G, embedded sensors, AI, Robotics, and autonomous functions are likely to lower costs, improve care and drive consumer demand.

Culture Innovation In Senior Care: Great Workplaces Are Needed Now More Than Ever

Chinwe Onyeagoro, president and chief strategy officer of the analytics firm Great Place to Work®, believes that high-trust cultures pay off. She has the data to prove it. Her work holds up a mirror to over 10,000 organizations each year, showing them the financial impact of great workplaces. For her NIC Talk, she’ll share recent work with senior care organizations, showing you practical steps you can take to survive potentially difficult conversations about culture while learning how creating an atmosphere of trust can impact your bottom line.

Innovation is All About Our People

Dwayne Clark, founder and CEO of Aegis Living, says, “Every time I think about innovation, I come back to people.” He created one of Glassdoor’s Top 50 Best Places to Work by investing in his employees first. He started by hiring from the hospitality industry, where employees had “70% of the skill set we needed.” Then he worked to retain talent through innovative approaches to rewarding and supporting employees. Finally, he built a headquarters that matched the culture he created. He’ll share key takeaways and opportunities to consider when following this innovative path.

Thoughts from NIC’s Chief Economist

Beth Mace

Risk surrounds us. In our personal lives. In our professional lives. In our environment. In our regular day-to-day routines. Many of us try to minimize or at least mitigate risk to simply carry on. Otherwise, we could be caught frozen. However, every once in a while, it’s important to look around and acknowledge the risks in our lives to best prepare for unforeseen circumstances. This article looks at risks facing operators and financiers of seniors housing and care properties. While not comprehensive, it provides a list of considerations in terms of both evolving risks and ongoing risks.

Evolving Risks

Economic Risk. In April, the duration of the U.S. economic recovery reached 107 months, exceeding the 106-month expansion of the 1960s, although still short of the record 120-month job growth period enjoyed in the 1990s. While an economic cycle doesn’t end simply because it is lengthy, increasingly economists are becoming concerned about the effects of tariffs on economic growth and stability, the impact of reduced fiscal stimulus from the tax cuts and spending plans in 2019 and beyond, and a broader global economic slowdown. As business leaders plan ahead, it is important to keep in mind that a slowing economy is a risk to projected NOI expectations.

Interest Rate Risk. The cost of capital is going up. The June jobs report, as well as indications that GDP growth was strong in the second quarter, will provide further support for the Federal Reserve’s interest rates increases through 2018. As widely expected, the Fed increased the fed funds rate by 25 basis points at its June FOMC meeting, the second increase in 2018. The Fed has raised rates by a quarter percentage point seven times since late 2015, and most recently to a range between 1.75% and 2.00%, after keeping them near zero for seven years. The Fed’s June projections now show a total of four increases in the fed funds rate anticipated in 2018 (two of which have already occurred), up from an earlier expectation of three. Further increases are anticipated in 2019. Their projection for the fed funds rate in 2020 is 3.4%.

Inflation Risk. While seemingly benign for years, there is a risk that inflation will start to accelerate. Tariffs on U.S. imports will directly push U.S. prices higher than what would have otherwise been expected. Additionally, wage rates and labor costs are expected to begin to put upward pressure on wage inflation. Over the past 12 months, average hourly earnings have increased by 72 cents, or 2.7%. This is up from 2.5% on average in 2017. Workers are more confident and willing to quit because the economy and the labor markets are strong. Workers who quit experienced a nearly 30% larger pay increase in May than those who remained in the same job over the past 12 months, according to research by the Federal Reserve Bank of Atlanta.

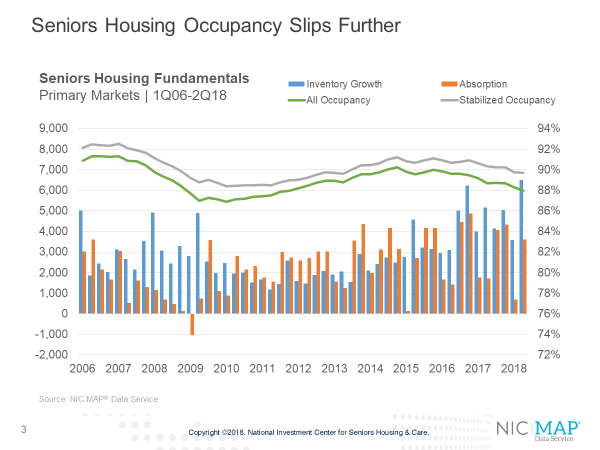

Supply Risk. At 87.9% in the second quarter of 2018, the occupancy rate for seniors housing fell to its lowest level in seven years, while the occupancy level for assisted living slipped back to its lowest level since NIC began reporting the data in 2006 (85.2%). The decline stems from inventory growth exceeding net absorption. While not the case in all markets, 17 of the 31 NIC MAP® Primary Markets had occupancy rates lower than year-earlier rates, as new demand simply could not keep pace with new unit deliveries. Taken together, these data points suggest that operators in many markets will need to pay careful attention to heightened competition and the effects it is having on rate growth and occupancy levels.

Employee Risk. In today’s tight labor market environment, recruiting, training and retaining employees is more challenging than ever. The executive director (ED) or administrator of a property is critical to successful, profitable operations and sets the tone for an entire property, both for residents and staff. However, recruiting, hiring, and retaining a strong ED may sometimes be a challenge. Successful operators manage this risk by financially incentivizing an ED who can build a strong team of employees that have service-oriented personalities and enjoy working directly with residents in an intimate relationship. More broadly, staff turnover can be reduced by establishing incentive programs and offering education and healthcare benefits to reward reliable attendance and longevity.

Increases in Acuity. On average, seniors are older and frailer than they were in the past. The higher average age and greater frailty of residents affects length of stay, turnover rates, occupancy, and, ultimately, operating income. These factors also affect staffing as residents need more help with activities of daily living, medication management, and more personalized care. Higher turnover results in more vacant supply and the need for a more robust pipeline and marketing effort. Circumstances such as these require operator flexibility and the ability to adjust staffing accordingly. The operator also must be able to reassess residents and modify care charges in response to changes in acuity levels, if the operation is to remain profitable.

Technology Risk. Technological innovation is emerging as a great influencer

in seniors housing. From an operations perspective, lead generation is being delivered over the internet. In addition, IT systems and big data are allowing senior management to observe real-time changes in their day-to-day performance and operating systems, and remote monitoring of residents is generating staff efficiencies. From a health and wellness perspective, tele-health and virtual care systems have the potential to reduce health care costs and improve health care coverage by allowing instant video conferencing at call centers with live doctors. Smart phones and appliances, remote sensors, hand-held devices with medical applications, and mobile personalized connectivity applications and software systems have the potential to better allow aging in place, independence, and virtual socialization. As these technologies get tested and winners and losers emerge, the operations, real estate, and social and medical aspects of the sector will be forever changed. Hence, technology could pose a risk (which may be an opportunity, as well) to today’s understanding and perceptions of seniors housing property investments.

Ongoing Risks

Operator Risk. As is often discussed, the operator is key in the financial success of a seniors housing property. Financiers of seniors housing properties need to work with an operator dedicated to serving the needs and desires of their residents in a manner that provides profits to ownership. Operators must have strong systems, policies, and procedures that ensure resident safety and compliance with laws, while simultaneously creating a warm and caring environment that is appealing to their customers.

Liability Risk. Best-in-class operators mitigate liability risk by adopting and implementing policies and procedures designed to ensure quality of care. The use of technology and electronic records creates a comprehensive documentation process and reduces liability risks. On-going communication with the resident’s doctor and adult children can help identify potential health issues and minimize the potential for surprises and/or lawsuits.

Insurance Risk. Unfavorable claims experiences can lead to an increase in a property’s annual insurance premium or a cancellation of coverage. Establishing procedures, documenting appropriate care in following the procedures, outsourcing medical care to certified physicians, and hiring qualified caregivers can minimize the risk of escalating insurance premiums and coverage loss. A strong operator incentivizes its workforce to use best practices to control costs and minimize covered losses.

Credit Risk. Seniors housing operators can mitigate credit risk by conducting credit checks on new applicants, thoroughly vetting the applicant’s financial wherewithal, and carefully monitoring collections. Best-in-class operators have relationships with the adult child (or adult children) and include a regular financial check-in to ensure the resident will be able to meet their financial obligations.

Resident Turnover Risk. Seniors housing resident turnover rates average between 37% and 56% annually, with assisted living/Alzheimer’s turnover at 56% and independent living turnover lower at 37%. Continuing care retirement communities (CCRCs) also called life plan communities, which attract residents based on the lifetime care model, have the lowest turnover at 22%. Turnover can be partly mitigated by integrating some clinical services on-site and may lengthen the stay of some residents. Best-in-class operators maintain a strong pipeline of new residents to fill vacated units.

Reimbursement Risk. Reimbursement risk is the primary reason why cap rates paid for nursing care communities exceed those for seniors housing communities. Nursing care properties typically generate most of their revenue from government payors (Medicare and Medicaid) with a significant portion of the profit generated from Medicare patients. With current fiscal challenges at the state and federal levels, however, government payors are looking to reduce costs by shifting from fee for service to value-based purchasing models through the use of managed care (MCOs) or accountable care organizations (ACOs). These organizations often reduce costs by reducing average length of stay for Medicare patients, pushing patients to lower-acuity, lower-cost settings (i.e. home vs. skilled nursing), and negotiating lower reimbursement rates. Operators can mitigate this risk by achieving strong clinical outcomes and demonstrating their value to ACOs and MCOs, which will direct more patients to providers that demonstrate results.

Most independent living, assisted living, and memory care properties receive bulk of revenue from private payers, which limits reimbursement risk. (Third-

party payors such as long-term-care insurers typically pay a cash benefit to the resident, not to the community, so they have no leverage on the rates charged by a community.) However, certain operators or geographies receive sizable revenue from governments through programs such as Medicaid waivers. Such strategies carry higher reimbursement risk and lower rate growth and need to be underwritten at the time of acquisition.

Regulatory Risk. The seniors housing and care sectors are some of the most heavily regulated industries in the United States. As with all laws and regulations, there is a “stroke of the pen” risk that can have quick and material implications on an operator’s business model. Changes in laws and regulations may impact such areas as licensure, compliance, fire/life safety, and staffing ratios, among others. A prudent operator may look to other state or federal regulations to foresee and plan for regulatory changes.

A lengthier discussion of risks associated with investing in seniors housing and care can be found in the upcoming Fifth Edition of the NIC Investment Guide, to be released at the 2018 NIC Fall Conference in October.

As always, I welcome your feedback, thoughts, and comments. Let’s keep the discussion going.

Beth

Five Key Takeaways from NIC MAP’s Second Quarter Seniors Housing Data Release

Seniors housing occupancy rate dips below 88%

NIC MAP® Data Service clients attended a webinar in mid-July on the key seniors housing data trends during the second quarter of 2018. Five key takeaways emerged:

- The seniors housing occupancy rate fell to 87.9%, which is 80 basis points below its level just one year ago. Assisted living registered its lowest occupancy since NIC began reporting the data series.

- The seniors housing occupancy decline is the result of inventory growth outpacing the absorption of units for both assisted living and independent living.

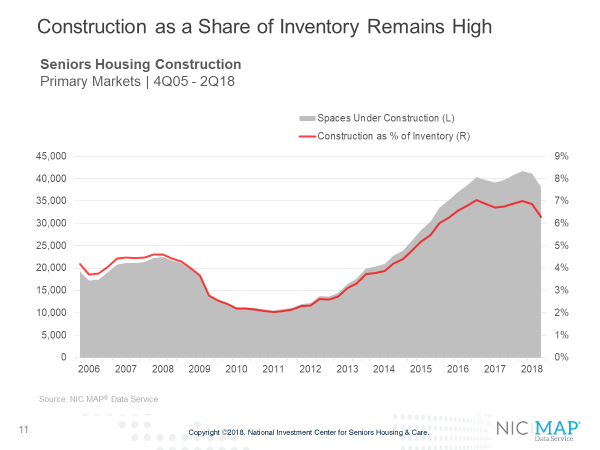

- Construction as a share of seniors housing inventory remains high.

- While the annual growth in average same-store asking rents accelerated for independent living and decelerated for assisted living, both were above 2.5%.

- Although the preliminary data suggests that property sales transaction volume softened, the average seniors housing sales price per unit remains near its recent peak.

Let’s take a closer look at some of these trends.

Seniors housing occupancy fell to 87.9%

- The occupancy rate for seniors housing, which includes properties still in lease up was 87.9% in the second quarter, down 40 basis points from 88.3% in the first quarter of 2018 and down 80 basis points from the second quarter of 2017. This was the lowest occupancy rate in seven years or since 2Q 2011. Meanwhile, assisted living occupancy fell to a record low rate of 85.2% in the second quarter.

- The quarterly decline in the seniors housing occupancy rate stemmed from the largest unit increase in inventory since NIC began reporting the data in 2006. This in turn can be traced to gains in assisted living inventory which also registered the largest increase in unit inventory in the time series. Independent living inventory also increased, but it did not set a record.

Annual inventory growth outpaced annual absorption for both assisted living and independent living

- Assisted living inventory growth has been ramping up for a longer period than independent living in the Primary Markets. In mid-2012, the occupancy rate of independent living was the same as for assisted living at 88.8%. Since that time, there has been a clear divergence in occupancy performance reflecting the differences in supply growth and demand for the two property types.

- As of the second quarter, annual inventory growth for assisted living was 4.8%, up from 4.7% in the first quarter, but below the record high 5.2% pace seen in the middle of 2017. Annual absorption accelerated to 3.5% from 3.2% and was the strongest since the second quarter of 2016.

- For majority independent living properties, annual inventory growth was 2.1%, above the growth in absorption of 1.7%. In contrast, annual absorption outpaced annual inventory growth from the first quarter of 2011 through the second quarter of 2016.

Construction as a share of inventory remains high

- In the second quarter, there were an estimated 38,000 units under construction in the Primary Markets. This was the fewest units actively under construction since the first quarter of 2016, but still very high. Construction includes any project that has broken ground and has not yet been opened.

- As a share of inventory, these 38,000 units represented 6.3% of today’s stock. This was below the two-time recent peaks of 7.0% seen in Q4 2017 and 3Q 2016.

- The most inventory growth in seniors housing in the past year occurred in Chicago, followed by Minneapolis, Atlanta, Houston, Detroit, and Washington, D.C. These six markets each had more than 1,000 units of new inventory brought on line in the past year, with Chicago leading the pack with nearly 1,900 units. These six markets accounted for 46% of all new inventory in the Primary Markets in the past year.

- In terms of percentage growth in inventory, the largest gains took place in Houston, Atlanta, Detroit, Orlando and Minneapolis. The strongest net absorption also occurred in many of these same markets. This includes Atlanta, Houston, Minneapolis and Denver.

Same-store rent growth decelerated

- Same-store year-over-year asking rent growth for assisted living averaged 2.8% for the second quarter, down 20 basis points from the first quarter. For independent living, average rent growth accelerated to 2.6% from 1.9% in the first quarter.

- There is wide variation in rent growth, however. Among the Primary Markets, the top ranked metropolitan markets for year-over-year rent growth in seniors housing were Portland Oregon, San Francisco, Seattle and Los Angeles. Weakest rent growth was in Dallas, Kansas City, San Antonio, Detroit and Atlanta. Many of these same markets have some of the lowest occupancy rates in the nation (Dallas, San Antonio, Atlanta, Houston and Chicago).

Closed seniors housing & care dollar volume: $1.7 billion for second quarter 2018

- Preliminary estimates of seniors housing and care transactions volume totaled$1.7 billion in the second quarter. That includes $1.2 billion for seniors housing and $500 million in nursing care transactions. The total volume was down 40%from the previous quarter’s $2.8 billion and down 25% from the second quarter of 2017 when volume reached $2.2 billion.

- Current figures show a 42% drop in single-property transactions from 110 closed in the first quarter to 64 closed in the second quarter. Portfolio transactions also decreased 42% from 19 closed in the first quarter of 2018 to only 11 closed in the second quarter.

Thought Experiment: Is the Assisted Living Industry Ripe for Disruption?

Andrew Smith

By Andrew Smith, senior director of innovation and growth strategy, Brookdale Senior Living; Vice Chair of NIC’s Future Leaders Council.

Assisted living has quite a lot going for it: Demographics, certainly, but other tailwinds too. Baby Boomers are bringing issues related to aging into the mainstream, congregate care is more and more accepted as a way to combat isolation and reduce healthcare expenses, and investment interest in the sector continues to grow.

For these reasons, there’s general optimism that the assisted living industry will continue to expand, even though it faces meaningful headwinds such as labor shortages, new competition, increased regulatory risk and shifting consumer expectations.

But what could “disrupt” assisted living as a product? What could make it go the way of video rental stores like Blockbuster that no longer fill a need?

To answer that question, let’s review a type of disruption called “Low End Disruption” popularized by Clayton Christensen in his book, “The Innovator’s Dilemma.”

Christensen argues that established industries typically seek “sustaining” innovations, improving their product by enhancing amenities or quality for their market segment. Over time, this can lead to a product that performs better or costs more than what the customer really wants or can pay for. For example, what percentage of the functionality of Microsoft Outlook do you think you use?

So-called low-end disruptors create a significantly cheaper or simpler product, serving customers who don’t want the complexity or the high cost of the established product. Gmail has a fraction of the functionality of Microsoft Office, for example, and it’s free to boot!

When companies with established products experience low-end disruption they tend to retreat to the more defensible higher end of the market, continuing to add features and increase price. This feels good because they experience higher margins, but they often don’t recognize that they’re losing their market to a lower end product until there’s no meaningful market left.

Signs point to disruption

So how might this happen to assisted living? Or might it already be underway? First, assisted living isn’t a product people want to purchase. It’s a product adult children promise their parents they will never force upon them. (And most people do not purchase the product – only a fraction of income-qualified seniors live in senior housing.) Families do everything they can to avoid a move. That said, people need assisted living services: support for activities of daily living, medication management, care coordination, meal preparation, transportation, socialization, and housing. And many of those services are difficult, expensive, and labor-intensive to provide, making it difficult to build a low-end disruptive alternative.

However, the confluence of three trends may create the perfect storm for disruption.

1. Baby Boomers may not have the ability to pay

Baby Boomers may be one of the wealthiest generations in our history, but they also have one of the lowest savings rates of any generation. This means it’s possible that fewer and fewer will be able to afford assisted living, forced to stay at home and depend on coordinating multiple services to meet their needs.

2. Healthcare reimbursement for “non-skilled” services will become more common

The Centers for Medicare & Medicaid Services (CMS) has already begun to experiment with the reimbursement of non-medical services through population health management programs like PACE. CMS will continue to do so, giving Medicare Advantage providers more options on what is reimbursable. Presently, reimbursements are blind to where the senior lives, and while this may change, coverage for these services will make it cheaper and easier for people to stay home.

3. Technology will eliminate the barriers to find and coordinate services

Isolated seniors aren’t isolated because they live alone – they’re isolated because they are home bound. New technologies like ride-sharing services and autonomous vehicles will remove some of those barriers to socialization.

Technology also makes it easier to provide at-home versions of many assisted living services (e.g. meals) and coordinate the various providers required to care for a senior at home (caregiving, housekeeping, maintenance, lawn care, etc.). Add to this the Baby Boomers’ widespread adoption of technology and a growing investment interest in senior-related services, and the timing may be right.

A low-end disruptor may use technology, healthcare reimbursement, and existing services to bundle an alternative to assisted living that is delivered at home, materially cheaper than paying for rent and care in a senior living community, while providing as good or better outcomes.

This isn’t a guarantee, only a possibility. Assisted living may be resilient because congregate living is more likely to combat social isolation than living alone at home. Congregate living is also a more efficient way to provide labor-intensive services like activities of daily living and medical support. If, in the future, healthcare insurers are partially footing the bill for these services, they’ll be motivated to promote congregate living over keeping seniors home bound.