Most are well-aware of the statistics related to the growing prevalence of cognitive decline among older adults throughout the U.S. Alzheimer’s disease is the sixth leading cause of death overall and fifth leading cause of death for Americans aged 65 and older. An estimated 6.9 million Americans aged 65 and older have Alzheimer’s in 2024, with 5.0 million of them aged 75 and older. It is no surprise that senior living organizations are playing an increasingly important role in providing supportive housing and care for older adults with varying degrees of cognitive impairment. This article specifically focuses on the memory care segment within Life Plan Communities (LPCs), an offering that has grown steadily across the past decade.

In the second quarter of 2014, roughly 3% of the total LPC units were devoted to memory care across the NIC MAP Primary and Secondary Markets. In the second quarter of this year, that number was 4.2%. Across the past year alone, the total number of memory care units within LPCs grew by 1.4%. While that year-over-year growth is below the non-LPC community types, which grew by 1.9% across the past year, that is meaningful growth.

Drivers of Memory Care Growth in LPCs

Many factors influence the decision to add or expand dedicated memory care units within a community. The first obvious trend is the growing need and demand for services for older adults who have a degree of impairment. Many LPCs may have been originally developed without a specific unit for memory care and over time, it has been deemed a clear need among the existing resident base. This need also drives expansions to existing units.

Another unfolding trend relates to the downsizing of the skilled nursing footprint. Between the second quarter of 2023 and the second quarter of 2024, the total number of skilled nursing units within LPCs decreased by 1.8%. This decline is on top of the skilled nursing downsizing and in some cases, closures, in the years prior. This downsizing of the skilled nursing footprint will often result in having space that community leaders are charged with repositioning for alternate uses. One common strategy has been to utilize that vacated space for a dedicated memory care unit. In most cases, that memory care is licensed as assisted living memory care rather than a skilled nursing memory care unit.

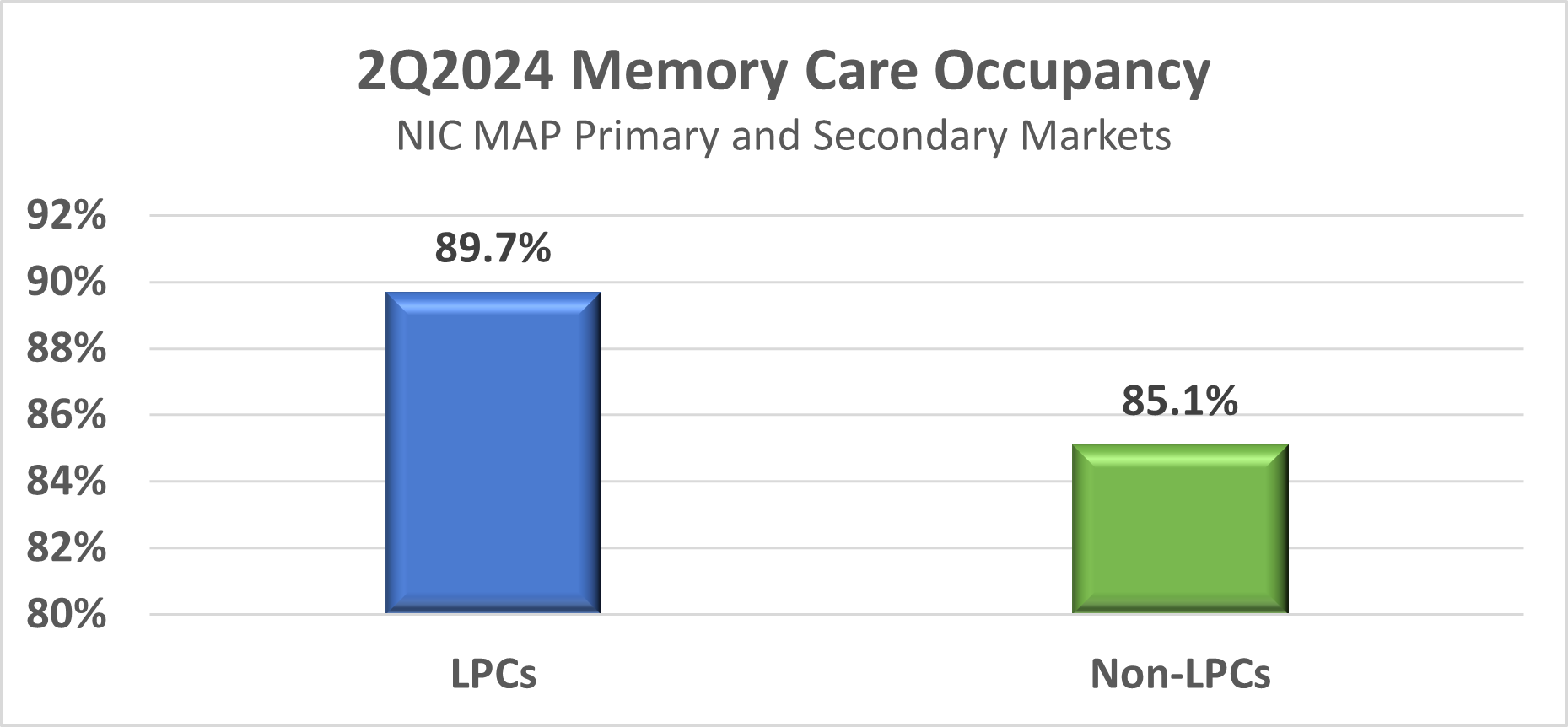

Memory Care Occupancy

The occupancy in memory care units of LPCs follows a similar pattern to the other levels of living within LPCs in that the LPC occupancy is above the non-LPC communities. As of the second quarter of this year, LPC memory care occupancy was 89.7% compared to 85.1% for non-LPCs. That occupancy is 3.7% above one year ago for the LPCs and 2.7% above for non-LPCs. To dig even deeper, when comparing across LPC types, the memory care occupancy for entrance-fee LPCs is 90.3% compared to 88.9% among rental LPCs as of the second quarter of this year.

Concluding Thoughts

Although memory care units within LPCs represent only 4.2% of the total units, they play a meaningful role in the housing and care continuum for older adults. Given recent trends and momentum, it is anticipated that these unit counts will increase over the next several years as LPCs evolve to meet the demands of the Baby Boomer population. This growth in a community’s physical footprint must be accompanied by intentional design elements, robust workforce training and innovative programming that is supportive of the unique needs of this population. NIC will continue monitoring this segment’s growth and share additional data insights as they become available.