March 2018

Opening Session to Examine Healthcare Payment and Delivery Reform

Dan Mendelson

Topic sets tone for upcoming 2018 NIC Spring Investment Forum

Amid unprecedented uncertainty, the healthcare payment and delivery system continues to evolve as it shifts from a fee-for-service model to one focused on value-based care. But where does the push to curtail costs and improve quality stand today? Where is it headed? Why does it matter for seniors housing and care? And what’s the best business strategy?

A panel of the nation’s top healthcare reform experts will address these crucial questions in detail at the opening general session of the 2018 NIC Spring Investment Forum, March 7-9, at the Omni Dallas Hotel.

“The opening session will help attendees understand what is likely to change in the healthcare environment, on what timeframe, and what it means for them,” said Dan Mendelson, opening session moderator and president of Avalere Health, a leading healthcare consulting firm. “Attendees will be able to walk away from the session with a better sense of how to plan for the future.”

The opening session—Trends in Healthcare Payment and Delivery Reform—will set the tone for the Spring Forum by highlighting the critical challenges facing the industry to reduce healthcare costs and improve outcomes especially for frail, high-need elders.

About 1,800 professionals are expected to attend the Spring Forum this year, an annual event held by NIC. Attendees include leaders in healthcare, seniors housing, home care, finance, and care coordination. The three-day event will feature 17 educational sessions as well as networking opportunities.

Building on last year’s programming, the theme of this year’s Spring Forum is “Unlocking New Value in Senior Care Collaboration.” Topic areas include Investing and Valuation, Risk and Return, and Value Creation and Partnerships.

Previewing the opening session, Mendelson noted that the healthcare realignment hasn’t slowed under the current Republican administration. “This government is eager to make changes,” he said. The changes are also being shaped from multiple directions by a variety of other stakeholders including managed care companies, payors, and post-acute and housing providers. Layered on top of that are the long term demographic issues of an aging population.

“We will deal with all of these topics at the session,” said Mendelson, who previously served as associate director for health at the White House Office of Management and Budget. “Change is happening.”

A timely discussion

Healthcare payment and delivery reform comes at a critical time for the industry. Assisted living and post-acute providers are seeking new strategies to successfully navigate the changing healthcare landscape.

Industry participants are exploring partnerships with providers such as home care companies to offer a fuller continuum to make themselves more attractive to payors. Mergers are becoming more attractive as post-acute providers look to acquire assisted living and independent living properties as a viable strategy going forward.

Amid these changes, the opening session will take a deep dive into the following topics:

- An update on recent changes at Medicare (for example, a proposal was recently announced that Medicare Advantage programs in 2019 will be allowed to pay for assistive devices)

- How the new federal government budget accelerates the healthcare realignment

- The impact of the growth of the Medicare Advantage program

- The evolution and increased emphasis on advanced payment model and bundled payments

- Capitated costs and risk sharing

- New program rules for Medicaid waivers amid legislative discussions on possible changes to the program

- How reforms are changing the market dynamics for seniors housing and ancillary service providers

- The role of technology

Mendelson will be joined at the opening session by expert panelists to provide an insider’s look at both short- and long-term business strategies and solutions. The panelists will include:

*Niall Brennan, president of the Health Care Cost Institute (HCCI). He is responsible for the firm’s advancements in price transparency and public reporting. Prior to joining HCCI, he was the chief data officer at the Centers for Medicare & Medicaid Services (CMS). He will speak about how technology is driving changes at Medicare. “The post-acute area is ripe for disruption from the standpoint of care delivery,” said Brennan, previewing his Spring Forum remarks.

*Adaeze Enekwechi, vice president for Policy, Strategy, and Analytics with McDermott+Consulting, an affiliate of McDermott, Will, & Emery, LLC. Most recently, she served as the associate director for health programs at the White House Office of Management and Budget (OMB). As the federal government’s chief healthcare budget official, Enekwechi noted the long-term care space has been the forgotten child of the healthcare continuum. “These folks should be at the policy table advocating for the long-term care sector, which tends not to be front and center when talking about health reform,” she said, in advance of the Spring Forum.

*Kristin Welsh, founding partner of Welsh Rose LLC. She will provide an update on the political landscape with respect to Medicare, as well as insights into merger and acquisition strategies. Welsh previously managed legislative strategy and lobbying for Healthfirst, a nonprofit health plan in New York City, and was deputy health policy director for the Senate Finance Committee under Chairman Orrin Hatch (R-UT).

Looking ahead, panelists will also offer a vision of the future when, in 10 years, the first baby boomers will turn 82—the time when elders typically start to move into assisted living buildings.

“It’s important to understand how payment models will evolve over the coming years,” said Mendelson, who emphasized the lasting impact that payment reform will have on the seniors housing and care industry.

Registration is open for the 2018 NIC Spring Investment Forum. Click here to register.

Predictive Analytics: The Key to Solving the Puzzle of Value-Based Payments

Steven Littlehale

Steven Scott

Dr. Barry Fogel

PointRight to provide critical metrics for post-acute market through NIC MAP® Data Service

As value-based payment models grow in popularity, transparency and access to quality metrics are becoming essential to the success of post-acute providers and investors. To meet this need, NIC has formed an alliance with PointRight, a leader in business intelligence and predictive analytics solutions. PointRight will be providing skilled nursing property quality metrics through the NIC MAP® Data Service, including such measures as statistical area benchmarking, CMS Five-Star Quality Ratings, and other metrics.

NIC Senior Principal Bill Kauffman recently held a virtual roundtable with the executive team at PointRight: Steven Littlehale, executive vice president and chief clinical officer, with 25 years of professional long-term care experience; Dr. Barry Fogel, an inventor and co-founder of PointRight, and a professor of psychiatry at Harvard Medical School; and Steven Scott, president and CEO, with an extensive management background in healthcare analytics.

Here is a recap of the conversation:

Kauffman: Can you give us some background on PointRight? How did PointRight get started?

Littlehale: PointRight was founded by academics and clinicians, some of the finest in the world. They were, and still are, focused on aging and aging services. They created the original Minimum Data Set (MDS and MDS 2.0), which is used in every skilled nursing facility (SNF) in the U.S. and throughout dozens of other countries.

Kauffman: What is PointRight’s main business today?

Littlehale: PointRight bridges the gap between providers and payers with a data-driven solution for quality improvement, cost reduction and performance management. Our solutions leverage data to manage long-term care and post-acute populations across the continuum, and are used by thousands of post-acute providers, hospitals, and payers nationwide.

Kauffman: Who is your typical client?

Littlehale: In today’s value-based world, I like to think of our clients more as stakeholders. They have a direct or indirect interest in how care is rendered and the achieved outcomes. They are often SNF leadership—both clinical and business—and those who have a financial interest in the SNF. The common theme in all our client relationships is that they seek the advantage that analytics affords. Using clinical, operational, regulatory, and financial data from the past, they better understand what is going to happen in the future. These analytics go “from the bedside to the boardroom” in informing resident care, as well as market positioning, mergers, and acquisitions.

Kauffman: What challenges are top of mind for your clients today?

Littlehale: PointRight clients are looking to improve quality, lower rehospitalization, manage risk, and achieve accurate reimbursement. We are also seeing a larger number of clients focused on how to not only improve their quality outcomes, but also to learn how to effectively share those outcomes with referral partners. We’ve worked with clients on both sides of the equation to develop the common language and common data set necessary for an effective partnership.

Kauffman: What is the value of working with PointRight as a consultant?

Scott: PointRight provides current, actionable, real-time data insights that no one else can provide to show what is going on with a facility or market today. Our actionable information and insights at the market level, facility level, and facility comparison level informs consultants (or buyers) on how a building is performing from market and clinical outcomes perspectives.

Kauffman: NIC and Pointright have created a partnership to provide NIC MAP clients with access to select metrics of yours. What is the nature of the partnership, and why did you elect to partner with NIC?

Littlehale: The partnership with NIC is a logical extension of our mission at PointRight and NIC’s mission. As our portfolio of clients in the investor space increases, it became clear that the inclusion of PointRight metrics improve valuation and monitoring capabilities. NIC is unwavering in its goal to provide reliable and transparent data that motivates and educates investors. It’s the perfect fit. Since increasingly valuation is playing out on the quality outcomes field, it’s a perfect partnership.

Kauffman: What PointRight data will be available through NIC MAP, and what is its value to the various players in the market? How do you think the data influences business decisions for investors and skilled nursing providers?

Littlehale: PointRight is providing a large set of metrics to NIC that are being refreshed monthly. The outcomes include CMS Five-Star Quality Ratings, PointRight® Pro 30® and PointRight® Pro Long Stay™ (rehospitalization and hospitalization), survey and regulatory outcomes data. The hospitalization metrics are risk-adjusted so that investors and operators alike will not be distracted by implications of case-mix, but truly have insight into SNF performance. We’re also providing competitive benchmarks. PointRight has found that there is significant variation in certain outcomes data, namely regulatory, that can be best attributed to geography (zip code!). It’s essential to control for this, and one way to do this is with focused benchmarks.

These analytics, to varying extent, impact the future viability of the SNF. The Centers for Medicare & Medicaid Services (CMS) has created many of these relationships, but still others have emerged. For example, a facility must have at least “Three Stars” to participate in several alternative payment models. If the facility is less than “Three Stars,” it is likely excluded from an accountable care organization (ACO) or hospital’s preferred provider referral network. While “Five-Star” designations do little to predict key performance indicators such as rehospitalization or length of stay, “those are the rules.” Additional metrics, such as rehospitalization are also used as inclusion criteria. These are two examples of metrics available to NIC MAP clients as a benefit of the PointRight and NIC partnership.

Kauffman: How has business intelligence and predictive analytics evolved over the past few years? What is most exciting about it now?

Fogel: With the growth of computer-based technology it’s now possible to collect and analyze enormous amounts of data faster and cheaper than ever before. The cost of doing that a decade ago would have been completely prohibitive, but analyzing these complex data sets is now possible. Any company looking to do analytics is no longer limited by the software and tools required for doing it. The second factor is the growth of electronic medical records and billing. Because we now have so many data sources, we can put together clinical data in a way that would have been impossible with paper charts. The ability to manage big data and analyze it efficiently is really exciting.

So, what we’re able to do now in post-acute care is diagnose problems before they turn into overt diseases or episodes. For example, when we look at preventing injuries in the elderly, we often look to prevent falls with fractures. If we look at various fall risk scales, we can look at what the chance is that the person is likely to have a fall. The next step is to apply predictive analytics at the resident level to identify what interventions are likely to prevent a fall and fracture.

Additionally, we’ve done some work here at PointRight on predicting mortality. People often have to make very tough decisions around end-of-life care, palliative care, pain relief, where they should live, etc., so it’s helpful to know what the future probably holds. This is especially a problem for a number of elderly people who have many different diagnoses and are on multiple medications at the same time.

Kauffman: How have you seen predictive analytics affect business in the post-acute space, and in health care for that matter?

Fogel: Predictive analytics informs effective decision making in the post-acute space (and healthcare in general) in three key domains:

-System Level: We use analytics to help make the system work better by enabling the system to send people (based on diagnosis and demographic factors) to the right providers at the right time.

-Provider Level: We use analytics to find the most effective/efficient ways to treat the patient and more efficiently use the resources available at the facility.

-Patient Level: We use analytics to predict risk associated with diagnoses and appropriate treatments.

Kauffman: Where do you see predictive analytics in five years and ten years from now?

Fogel: What I see coming down the pipe is all around personalized medicine. When we’re able to access and process biomarkers and genetic information, and data from mobile devices, etc., the ability to diagnose and treat conditions is going to be vastly greater, as well as the ability to personalize treatments. For example, we’re going to be able to diagnose conditions before they’re obvious clinically and will be able to come up with personalized treatments. There are already people doing these things, but they haven’t entered the main stream of clinical process. We’re looking at predicting disease before it happens based on different combinations of abnormalities.

Kauffman: Given the reality of a value-based health care system and the belief that it will continue to grow, what do you recommend skilled nursing operators do to survive the challenges of today, and in the future?

Littlehale: I like this question very much; it’s the right one to be asking. CMS is forcing the silos to come down. By silos, I mean the walls/barriers that exist between hospitals and post-acute care, and within post-acute care that resulted in poor quality and out of control costs. The metrics that CMS is using to penalize and reward organizations in their value-based purchasing initiatives have a “cross silo” component. You cannot be successful in today’s value-based world unless you have functional relationships with both upstream and downstream partners. Let me boil this down to three key recommendations:

– Create and reinforce data-driven relationships with upstream and downstream partners (providers)

– Ensure that agreed upon key performance indicators are third party verified (like NQF), actionable and current

– From your own data, know what you’re good at and what needs improvement, and be completely transparent with your marketing and quality improvement efforts

Kauffman: What sectors of healthcare do you see thriving in this environment?

Scott: Those entities that can assume downstream risk and manage that risk proactively by managing the population, aligning with proactive partners, and being proactive on the outcome side, are thriving.

In particular, we’re seeing that ACOs and physicians’ groups in particular seem to be the most proactive in managing populations in this environment.

Kauffman: Are there opportunities that have been overlooked in a value-based world by operators, payers, or health systems? If so, what are they?

Scott: There are certainly challenges, and a lot of it has to do with creating a common language across the continuum and evaluating common data. Technology doesn’t always interface well across segments, and each segment operates differently, so how do you make sure you’re measuring the same things the same way?

Common language around reporting is still something being worked on, and is an area that PointRight has a strong focus on. PointRight works with operators, payers, and health systems to ensure they are evaluating common data so each segment is able to proactively manage their populations and outcomes.

Kauffman: What do you see as the main risks to skilled nursing operators? How can they mitigate these risks?

Littlehale: Main risk: navel gazing. I love that expression. Basically, it refers to meaningless or excessive self-contemplation. In limited doses self-contemplation is helpful, but looking to solve today’s and tomorrow’s challenges with yesterday’s strategies doesn’t work. There have been too many rapid-fire changes with the Affordable Care Act to make business as usual a viable option.

Authentically embracing many of these new requirements, such as Quality Assurance & Performance Improvement (QAPI), is a pathway out of yesterday and onto tomorrow. QAPI and its requirements for data-driven systemic improvement is aligned with our new value-based healthcare environment.

Kauffman: What are investors looking for when they connect with you?

Littlehale: Asymmetric Information. In other words, they want to know that their “secret sauce” is valid or find out how to create/modify their “secret sauce.” Because of the increasing importance of many of the outcomes discussed here, many investors are revising how they assess and monitor their portfolios. PointRight has unique and measured ways of achieving this.

Kauffman: Are new capital sources coming in to talk with you, or are your clients and prospects all experienced investors in the post-acute and healthcare sectors?

Scott: The dynamics of the investor community is changing. The biggest change I’ve seen is the transition of seniors housing and assisted living investors to the SNF environment, and being faced with the aspects of regulatory reimbursement that they haven’t faced before.

We usually talk to people who have a portfolio with nursing homes as part of the mix, and are looking for input on how to manage the regulatory/reimbursement aspect that comes along with those.

We also work with M&A groups to provide analysis showing what the clinical outcome performance is for certain clusters of buildings. We help to show how those buildings are performing in the market, and what their performance trend may look like for the future.

2017 Sales Transaction Volume Increases, Driven by Institutional Capital

Bill Kaufman

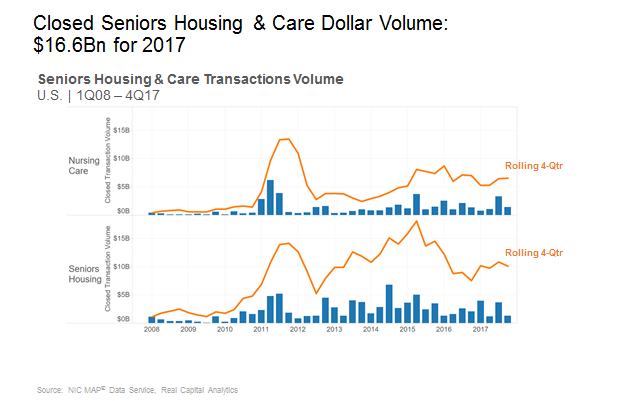

The institutional buyers played a major role in propelling seniors housing and care closed property sales transaction volume in 2017 which registered $16.6 billion. The $16.6 billion includes $10.1 billion in seniors housing property sales and $6.5 billion in nursing care property sales. The total closed transactions volume was up 14.4% from the previous year’s $14.5 billion. Seniors housing saw a 34% increase in volume from $7.5 billion last year, while nursing care volume decreased 6.6% from $7.0 billion last year.

The dollar volume in 2017 was due to a strong first quarter and a very strong third quarter. Those two quarters represented 70% of the dollar volume for the year. The fourth quarter historically is a strong quarter compared to the rest of the year. However, in 2017, that was not the case. Of course, one possible explanation for this could be the wait-and-see approach as the tax bill was unfolding as 2017 was coming to a close. Time will tell if deals were delayed into the first quarter of 2018, or perhaps the second quarter, and then we possibly could see a solid start in transactions volume for 2018.

Smaller transactions dominate

Dollar volume was up in 2017, but when looking at the total number of deals closed—a measure different than dollar volume—we saw the number of transactions closed dropped 9%. The number of deals closed in 2017 was 491 of which 98 were portfolio transactions and 393 single-property transactions. That compares to 539 transactions closed in 2016 of which 109 were portfolio transactions and 430 were single-property transactions. Over the past couple years, portfolio transactions represented 20% of overall closed transactions. This was even the case back in 2015, when the public buyer type, namely the publicly traded REITs, represented the majority share of buyers. Indeed, single-property transactions are very important to the market in terms of the flow of transactions.

We now have seen 17 straight quarters of over 100 total deals close. The fourth quarter of 2017 registered 124 deals closed, which was up from the third quarter of 2017, but down from the fourth quarter of 2016 and 2015 when 161 and 151 transactions closed, respectively.

As far as the size of the deals, small deals of $50 million or less dominate the activity, which makes perfect sense considering the single-property market represents the majority by far of the number of transactions closed. In the fourth quarter of 2017, smaller transactions dominated, more than usual, representing 96% of all transactions closed.

Over the past couple years, as the public buyer type has become less represented within the overall volume, we have seen a decrease in large deals of $500 million or more. While 2015 alone saw 10 transactions of $500 million or more, 2016 and 2017 together registered a combined total of only 10 transactions of $500 million or more.

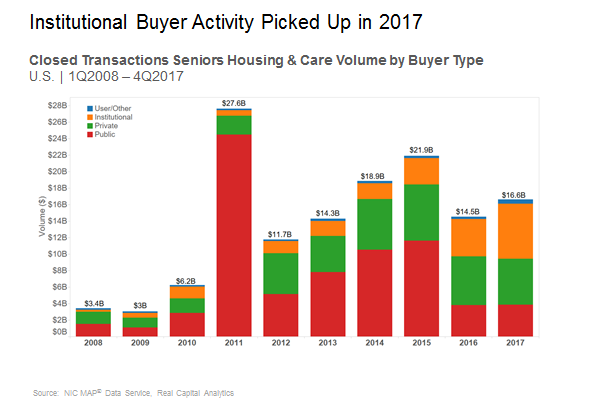

Institutional capital driving dollar volume

As noted above, transactions dollar volume for 2017 registered an increase from 2016 as the institutional buyers, comprised of mostly equity funds that manage pension money or other types of institutional money, played a major role in higher volume.

Over the past couple of years, the institutional buyers have increased their share of total buyer volume significantly, in addition to increasing their dollar volume overall. In 2015, institutional buyers registered $3.2 billion in closed transactions, representing only 15% of all buyer volume. In 2017, institutional buyers registered $6.6 billion in closed transactions, a 107% increase from 2015, and represented 40% of overall transaction volume.

Some relatively large deals of note by institutional buyers in 2017 were:

- Kayne Anderson, the institutional alternative investment manager, bought a $633 million portfolio from Sentio Healthcare Properties, which consisted of 32 seniors housing and care properties. This deal included some medical office building (MOB) properties which are not reflected in these volume numbers;

- Columbia Pacific purchased 54 seniors housing properties from Hawthorn Retirement Group for $1.8 billion, which included over 6,100 units;

- Blackstone closed on a portfolio of 60 Brookdale properties from HCP representing $1.1 billion in volume, with a unit count of over 5,500;

- Blackstone, in another large deal, closed on the Senior Lifestyles portfolio from Welltower for $747 billion, including 25 properties and over 3,600 units; and

- Lastly, another large deal was the acquisition by the Chinese life insurance company, Taikang Life Insurance, closing on a partial interest from Northstar which, per the associated press release, was approximately $460 million and included over 200 properties.

While institutional buyers’ activity has increased, the public buyers’ activity decreased significantly after 2015, including their share of the total volume. As the public buyers’ share has decreased, so has the overall dollar volume. The public buyer type represented 53% of the $21.9 billion in closed transactions in 2015. As of 2017, the public buyer represented only 23%, and total volume was only $16.6 billion. Public buyer volume in 2015 was $11.6 billion, and in 2017 it had decreased by 67% to $3.8 billion.

While mentioned last here, let’s not forget about the private buyers who include private REITs, private owner operators, and private partnerships. The private buyers have been very steady with their rate of acquisitions, averaging $6 billion dollars per year from 2015 through 2017. Indeed, very impressive deal flow. The private buyer registered $6.8 billion in volume in 2015 and represented 31% of all volume. In 2017, it registered $5.6 billion and represented 34% of the total volume. Even with the relatively weak fourth quarter volume in 2017, private buyers registered $1.2 billion in closed transactions.

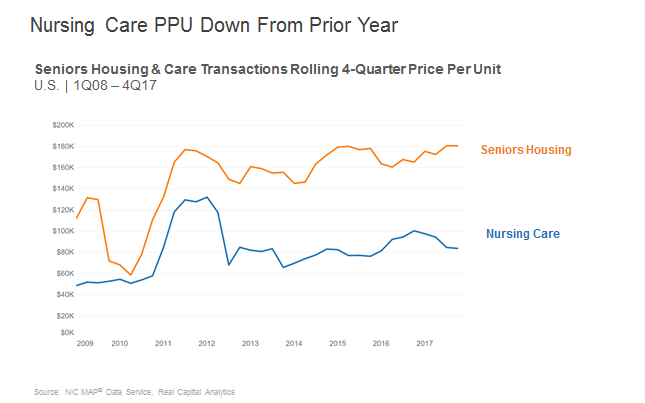

Pricing

The storyline for seniors housing and nursing care pricing has started to diverge over the past year.

Seniors housing’s average price per unit (PPU) of $180,500 was flat in the fourth quarter of 2017 when compared to the third quarter. However, on a year-over-year comparison, seniors housing’s average price per unit is up 9.3% from $165,100. And from its cyclical low in 2010 of $58,600, it is up over 208%, which comes out to be a 16.2% compound annual growth rate over the period.

The trend for the nursing care price per bed is another story. The average price per bed dropped 1% in the fourth quarter, from $84,600 in the third quarter down to $83,800. On a year-over-year comparison, the nursing care average price per bed is down significantly by 16.5% from $100,300 in the fourth quarter of 2016. However, from its cyclical low in 2009 of $48,700, it is up 72%, which comes out to be a 6.4% compound annual growth rate.

It appears that the average nursing care price per bed drop has stabilized somewhat this past quarter, but we will see how it holds up over the next few quarters.

The transactions market appears relatively healthy as volume in 2017, both in terms of dollars and the number of transactions, proved to have momentum. This momentum comes at a time when seniors housing and nursing care are experiencing their own unique challenges, whether it be over supply concerns for seniors housing, or occupancy and length of stay pressure in skilled nursing. However, as shown above there is still strong interest from investors, especially the institutional investors. Barring any capital market shocks, 2018 should also see a relatively strong transactions market.

Employee-First Approach of Great Place to Work Can Help Create Great Senior Living Companies: A Conversation with Kim Peters

Kim Peters

Best Workplaces in Aging Services to be named in September

NIC’s president and CEO, Brian Jurutka, is a passionate advocate for the Great Place to Work Institute and its Best Workplace lists. He is championing new initiatives at NIC that are in alignment with the best practices of organizations that receive the “Best Workplace” designation.

Brian recently spoke with Kim Peters, executive vice president, certification program, at Great Place to Work (GPTW), headquartered in San Francisco. Kim leads the Great Place to Work Institute’s Best Workplace lists, published in partnership with Fortune and People magazines, highlighted on the website greatplacetowork.com. In addition, Great Place to Work partners with Activated Insights, which has senior care operating experience and has developed communication and other processes for senior care, including industry sub-sector benchmarks.

What follows are excerpts from the conversation.

Jurutka: Can you tell me about Great Place to Work?

Peters: Great Place to Work works with companies all over the world, as we have affiliate offices in more than 50 countries, on how to create and sustain high-trust, high-engagement cultures that drive better business performance. Our model is based on 30 years of research representing millions of employees’ experience of the workplace.

Our Trust Index™ employee survey is the most widely taken employee survey, which means we have the most robust benchmarks and best practices across companies, industries, and even job types.

In the U.S., we work with companies such as Wegman’s, Salesforce, Hilton, Edward Jones, Workday, Cheesecake Factory, Scripps Health, St. Jude’s and many more. And, these are just the publicly-recognized companies who make it onto one of our Best Workplace lists, published by Fortune and People magazines.

Jurutka: How do you work with seniors housing and care companies, and how is Fortune magazine involved?

Peters: We work with seniors housing and care companies in three ways:

- These companies can become Great Place to Work® Certified

- Once certified, they can be named to our Best Workplace Lists, and

- Now, we have Activated Insights, an incubated affiliate focused on senior care

Companies can take our Trust Index Employee Survey, and, if 70% of employees say it’s a Great Place to Work, they are GPTW-certified.

If they are GPTW-certified, then they are eligible for one of 20 Fortune and People Best Workplace lists, including a new list called Best Workplaces in Aging Services to be published in September.

If any seniors housing or care organization contacts GPTW, we put them in touch with Activated Insights, our senior care partner company. They have senior care operating experience and have developed communication and other processes that work in senior care, including industry sub-sector benchmarks. They use the same Trust Index™ survey for sectors within senior care.

Jurutka: Why should seniors housing and care investors be interested if individual properties are a Great Place to Work?

Peters: Because it’s better for their business. Our 30 years of research is validated and ties being a Great Place to Work with business performance compared to industry averages, including:

- Lower employee turnover

- Higher revenue growth

- Higher EBITDA margins

My understanding of seniors housing and care is that valuations are based on a multiple of EBITDA and free cash flows. If so, there is a direct link between being a Great Place to Work and higher valuations. For instance, several research studies on publicly-traded companies have shown that being a Fortune 100 Best Company to Work For translates into two-to-three times stock price performance.

Jurutka: Workforce is a major issue in seniors housing and care. What are some tactical tips you recommend to companies in industries with staffing shortages?

Peters: I advise companies to do a few things:

- Workforce issues often mean high employee turnover. If that is the case, establish a well-organized way of welcoming people into the organization, with personal touches, and creating a warm and friendly environment. Building a high trust culture starts with leadership, and it also starts with the new hire experience.

- Do not just offer a laundry list of benefits or programs. Make them uniquely yours by ensuring programs are intentionally linked to your purpose, your mission and your values. It’s less about any particular program and a lot more about offering a workplace where employees understand how they contribute to the mission and that their contributions are valued and making a difference. It really impacts their experience and contributes to creating a great place to work.

- Leaders can inspire their employees by holistically integrating their people policies, benefits and perks, employee programs, and career development programs. When we evaluate a company, we review their employee Trust Index scores, practices, and benefits, and we hope to see a holistic integration of the three. What I mean is that the survey feedback shows that employees are valuing the company’s benefits and practices, and that their comments about programs are truly meaningful.

Jurutka: Women comprise the majority of the senior care workforce. I know you recently released some interesting research with the Best Workplaces for Women list. Can you share some findings relevant to seniors housing and care?

Peters: Sure, some of those takeaways included:

- A great workplace for women helps create a great workplace for all

- Equitable employers are welcoming places to do business

- Involvement inspires loyalty: fully engaged members of the team are five times more likely to plan a long-term future

- Buy-in pays off: women who say they make a difference are 27 times more likely to describe their companies as a great place to work

Unfortunately, women aren’t thriving everywhere yet. What this means is that for companies, it’s really important to take stock of your own employee experience. For example, anyone who surveys their employees using our Trust Index™ survey can compare their experience to not only benchmarks for their size or industry but also to our demographic best workplaces for women, millennials, and diversity. This helps the company understand more about the worker’s experience and to identify areas where there may be gaps in the overall experience.

Then benefits and programs can be used as tools to help bridge any gaps in positive workplace experiences, whether it’s for men, women, hourly, salaried, and individual contributors versus managers.

And, in short: if you fix it for women, you fix it.

Jurutka: NIC is an investor-facing, nonprofit organization. How should investors use the information you are sharing?

Peters: As with most real estate, other than location, the operator is key to good, sustained investments.

You want to look for personable, caring operators that are accessible and transparent with their staff. Ask your operator how employees consistently experience a great place to work, regardless of who they are or what they do in your company. Does the operator have executive directors, GMs, and administrators who are trustworthy, credible leaders who treat people fairly and with respect? Do they create an environment where employees are proud to be a part of the organization, and genuinely enjoy spending time at work?

Lastly, you can ask your operators to get certified and to share their Trust Index survey score and findings with you. This way, you have a proven number and methodology with which to measure and compare your operators in an apples-to-apples way.

Jurutka: The seniors housing and care industry, like much of healthcare, is grappling with changing payment models and value-based purchasing. Can you share how Great Place to Work has helped healthcare companies?

Peters: Healthcare is one of the fastest growing industries for Great Place to Work Institute. I think it is because healthcare has transformed so rapidly, and you need an agile, innovative workforce not only to survive but to thrive in new models of patient care.

I can think of a longtime Great Place to Work company that came to us with operating losses, poor employee and customer morale, declining market share, and organized labor risks. Again, they had no money, but the management committed their time and resources to becoming a high trust, high engagement great place to work. They reached that goal, and when healthcare reform passed in 2009, they were one of the few healthcare providers that could quickly move to take share from competitors and they are still thriving with great margins as a GPTW today.

More information on Kim Peters and the Great Place to Work Institute’s work can be found at: www.greatplacetowork.com