Pricing Remains Relatively Stable

The price per unit/bed for seniors housing and care properties has remained relatively stable through the second half of 2017. As capital continues to flow into the sector with more interest from private buyers and institutional capital, as of late, there remains competitive bidding for properties though deals closing recently have mostly been smaller, single-property transactions.

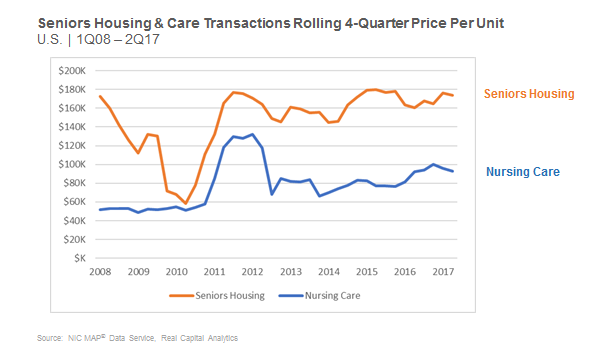

Seniors housing price per unit continues to oscillate between $165,000 to $175,000—the range over the past 4 quarters. Quarter-over-quarter, the price per unit dropped 1.5% to $170,700 from the prior quarter of $173,400. Year-over-year, the price increased 6.1% from $160,900.

The price per bed for nursing care was stable in the second quarter of 2017 at $97,400 compared to $97,200 in the first quarter. Year-over-year, the price per bed is up 5.5% from last year when it registered $92,300.

While the public buyer’s transaction volume has decreased significantly along with overall transactions dollar volume the past few quarters, as discussed in this blog series on July 19, the numerous smaller deals have kept pricing stable. Transaction dollar volume in the quarter fell by 58%, but the number of deals closed only fell by 10%, with the price per bed for nursing care remaining flat and the price per unit for seniors housing only down slightly.

We just have to take a look at the number of transactions closed in the quarter to understand the continued robust transactions market. The second quarter represented the 15th straight quarter of more than 110 closed transactions with 113 in total. Of the 113 closings in the quarter, 24 were portfolios and 89 were single-property transactions. Only one deal was over $100 million in the second quarter. To put that into perspective, there were eight deals over $100 million in the first quarter. Furthermore, 95% of the deals closed were for $50 million or less, which was the largest share of deals closing in that range since the fourth quarter of 2010.

In summary, the main takeaway here is the fact that pricing remains competitive when properties are coming to market. Even though the public REITs are less aggressive and overall volume declined this quarter, pricing remained strong as bids came from other players, like private equity and smaller private buyers. The demand for properties is still strong and capital from investors is still plentiful, even in the somewhat challenging environment.

In regards to skilled nursing pricing, you might wonder how the price per unit is still so competitive given the continued headwinds in that sector, but you have to remember that reported pricing reflects what is being traded. As such, many of the skilled properties being sold are newer properties that have been built for higher acuity patients and therefore have the potential for more cash flow per bed. In addition, some turnaround, or value-add buyers are entering the market and paying higher prices for the potential cash flow, even though the property is not running at the expected level. The price paid is a bet on the future of better operations and/or gaining market share and therefore better cash flow. Not to mention, many investors continue to look for higher yields and income returns in today’s relatively low interest rate environment.

We look forward to continuing to update the transactions data each quarter and providing the transparency that comes along with those updates. Stay tuned for Q3 data.