A Deep Dive into the 2Q2016 NIC Skilled Nursing Data Report

On September 15, at the 2016 NIC Fall Conference, NIC released its 2Q2016 Skilled Nursing Data Report. The report includes key occupancy and revenue metrics from October 2011 through June 2016. In today’s blog post, I’ll walk you through the data.

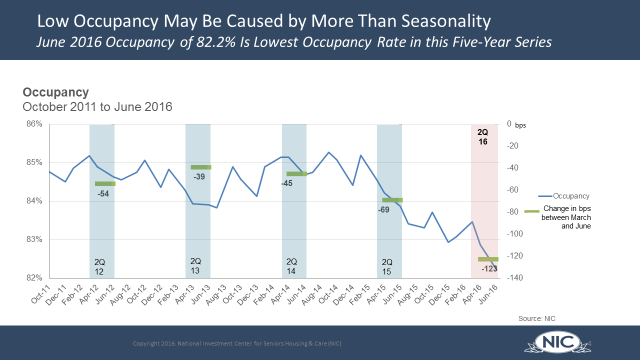

Occupancy Declined to a Five-Year Low

After bouncing back in the first quarter of 2016, occupancy declined 123 basis points quarter-over-quarter to 82.2% as of June 2016, which is the lowest occupancy recorded in the data series. While occupancy usually softens in the second quarter, this year the second-quarter decline was more significant than in previous years, suggesting that lower occupancy is being driven by factors beyond seasonality.

There are a number of care delivery and reimbursement initiatives that could be playing a role in the decline. For example, acute care providers, managed care payors, and conveners have initiatives in place to divert skilled nursing referrals to home health and other community-based care settings. In addition, some patients referred to skilled nursing for post-acute care are managed by payors aiming to reduce length of stay, which creates a reduction in Medicare and managed care days.

Occupancy not only decreased quarter-over-quarter; it also decreased year-over-year, falling 170 basis points from 83.9% in June 2015 to the 82.2% in June 2016.

Occupancy historically has been an important metric to follow, and still is, but it is just as important to understand the relationship between occupancy and the true economics of the operating business. As some operators are transitioning into higher acuity patient care, it’s possible that an operating business captures fewer patient days because of the lower length of stay for, as an example, more Medicare rehab patients. This will cause occupancy to decline. However, it’s also possible that, all else being equal, the higher reimbursement rates for higher acuity patients will mitigate some of the pressure on cash flow from lower occupancy, as long as the volume of patient admissions is strong and expenses (for example, labor expenses) do not increase more than the incremental revenue. In stating that, the large drop in occupancy in the second quarter does seem significant for the operating businesses, especially as skilled mix has decreased.

Skilled Mix Declined due Especially to Medicare

The main driver of lower occupancy was skilled mix, or the share of patient days paid for by Medicare and managed Medicare. It decreased 140 basis points from 25.9% in March 2016 to 24.5% in June 2016. Year-over-year skilled mix declined 130 basis points from 25.8% in June 2015. Medicare patient day mix drove the decline within skilled mix as it declined 107 basis points from the prior quarter to 13.5%. Year-over-year—which can possibly be more telling of the trend—Medicare patient day mix declined 140 basis points from 14.9% in June of 2015. Managed care (managed Medicare) patient day mix also declined from the prior quarter, albeit slightly, to 5.8% of patient days. Year-over-year managed care patient day mix decreased 40 basis points from 6.2% in June 2015.

Decline of Managed Care (Managed Medicare) Revenue per Patient Day May Be Abating

One of the main reasons timely data is so important is for identifying trends as they happen, and this recent data release showed that the decline in managed care revenue per patient day (RPPD) might be subsiding as of the second quarter. The rate of decline within managed care RPPD—the daily reimbursement rate paid to skilled nursing providers per patient by managed care—did slow, which suggests that the managed care rate of decline may be plateauing. The quarter-over-quarter decline to $437.85 per day was only -0.2% compared to the steep declines of -1.2% and -1.7% seen in the prior two quarters. Year-over-year, the rate declined 4.2% from $457.08.

Given the fact that the latest year-over-year data still shows a significant decline, we still need to be cautious in interpreting this quarter’s data. To call this recent quarterly comparison a trend might be foolish as it is only one quarter of data that shows the decline abating, but this development warrants attention as we watch what happens in the third quarter.

This particular data metric, managed care RPPD, has grown in importance over the last few years because of the growth of managed care. Specifically, Medicare Advantage (MA) plans have grown significantly in popularity, as the number of people turning age 65 in our country and are now eligible for Medicare has grown significantly, as well. For skilled nursing operators, who have increasingly felt the effects of pressure from MA plans both in terms of length of stay and reimbursement rates, any leveling off of the rate of decline in per day rates would be a welcome turn of events.

Medicaid RPPD Hit a Five-Year High

In the second quarter of 2016, Medicaid RPPD grew 0.3% to $198.16, which is a change from the prior quarter’s flat growth. Year-over-year Medicaid RPPD grew 0.9% from $196.31 in June 2015. The current June RPPD of $198.16 represents the highest rate within this time series and a compound annual growth rate of 1.3% since October 2011.

Although the growth of Medicaid RPPD seems to be somewhat of a bright spot for operators, one question is if $198 per day is enough to cover the cost of care for a resident in skilled nursing. Answering that question is not so easy, because the rate and expenses can vary significantly by state and county. Operating expenses seem to be growing faster, especially labor wages, which are a significant percentage of total operating expenses. So with such a low reimbursement rate compared to other payors (e.g. Medicare), there’s not only the challenge of covering the cost of care, but if the growth rate of reimbursement continues to trail the growth rate of expenses, it can create significant pressure on profitability.

We will look forward to reporting on the key metrics next quarter to see how these current developments evolve.

Please feel free to reach out with any comments or question

Download the 2Q2016 Skilled Nursing Data Report

The complimentary report is now available to download here: